Reports

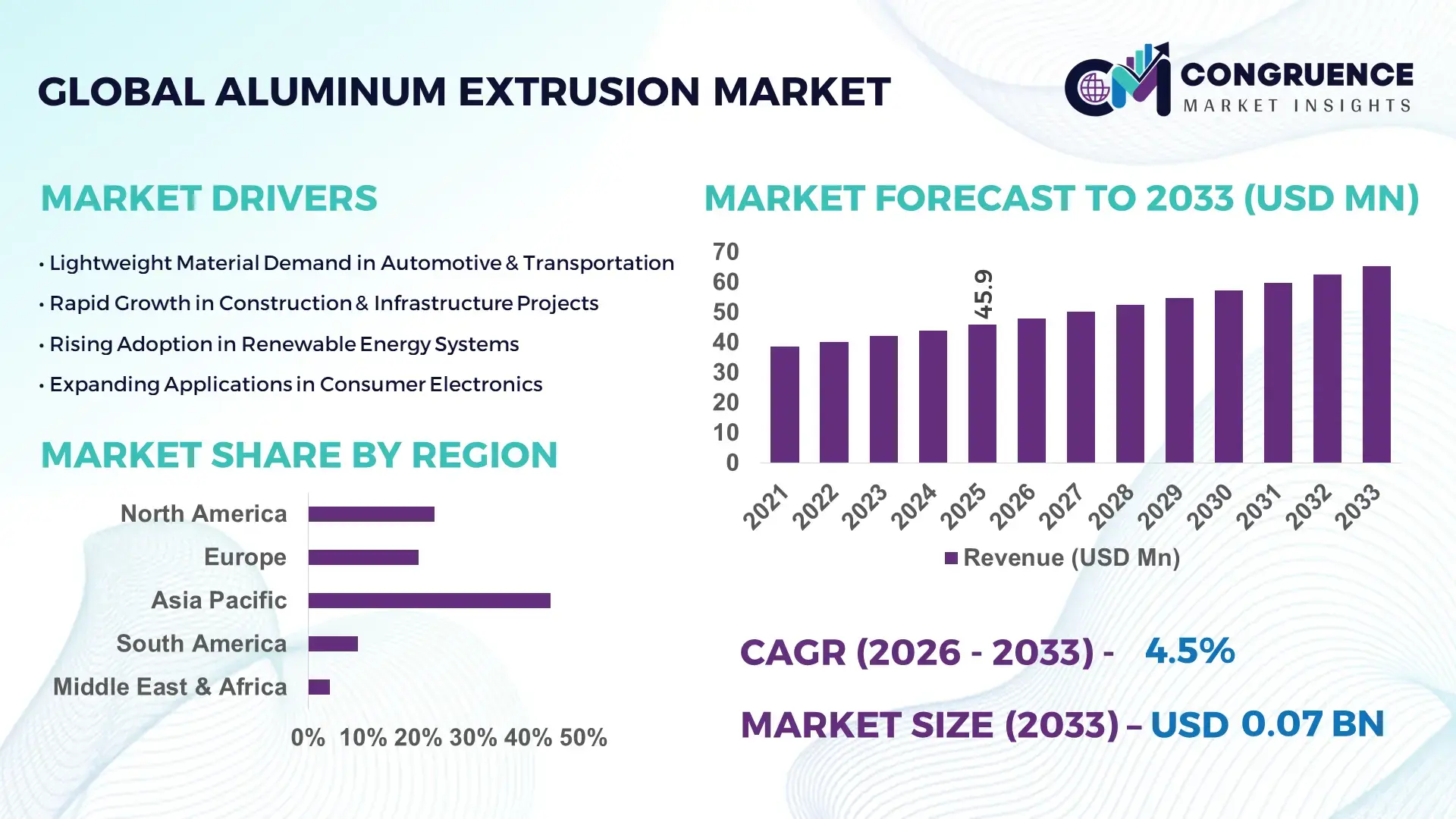

The Global Aluminum Extrusion Market was valued at USD 45.9 Million in 2025 and is anticipated to reach a value of USD 65.27 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. This expansion is fueled by accelerating infrastructure modernization, electric mobility adoption, and the rising preference for lightweight, corrosion-resistant structural materials.

China leads global aluminum extrusion production with installed extrusion capacity exceeding 20 million metric tons annually, supported by hundreds of high-tonnage presses and integrated downstream fabrication facilities. Major industrial clusters supply precision aluminum profiles for rail transport, solar mounting systems, curtain wall systems, and electric vehicle components. Continuous capital investment in automated extrusion lines, intelligent die-change systems, and advanced alloy processing has strengthened manufacturing efficiency and dimensional accuracy. Domestic utilization of extruded aluminum continues to grow across high-speed rail projects, commercial construction, and photovoltaic infrastructure, while export volumes remain substantial due to large-scale production ecosystems and vertically integrated supply chains.

Market Size & Growth: Valued at USD 45.9 Million in 2025 and projected to reach USD 65.27 Million by 2033 at a CAGR of 4.5%, supported by rising demand for lightweight structural aluminum solutions.

Top Growth Drivers: Lightweight vehicle adoption 28%, green building material usage 34%, renewable energy structure deployment 22%.

Short-Term Forecast: By 2028, extrusion process optimization is expected to improve material utilization efficiency by 10% and reduce waste generation.

Emerging Technologies: AI-enabled extrusion process control, high-strength 7xxx series alloy development, digital twin–based die simulation.

Regional Leaders: Asia-Pacific projected to reach USD 28 Million by 2033 with infrastructure expansion; North America USD 17 Million driven by EV manufacturing; Europe USD 14 Million supported by sustainable construction practices.

Consumer/End-User Trends: Construction and transportation sectors dominate demand, with increasing use of thermally efficient window frames and EV battery enclosures.

Pilot or Case Example: A 2025 smart extrusion facility upgrade improved production throughput by 14% and reduced energy consumption per ton by 11%.

Competitive Landscape: Leading producer holds approximately 18% share, followed by major global manufacturers across Asia, North America, and Europe.

Regulatory & ESG Impact: Carbon reduction mandates, recycling targets, and energy-efficient building codes accelerate adoption of low-emission aluminum profiles.

Investment & Funding Patterns: Over USD 1.2 Billion allocated toward modernization of extrusion presses, green smelting integration, and automation systems.

Innovation & Future Outlook: Growth in precision micro-extrusions, modular construction components, and EV structural integration defines future industry direction.

The aluminum extrusion industry serves construction, automotive, aerospace, electronics, and renewable energy sectors, where lightweight metal profiles enhance structural efficiency and durability. Curtain wall framing, EV chassis structures, solar panel mounting systems, and industrial machinery components contribute significant demand. Innovations in high-pressure extrusion, alloy temper optimization, and automated quality inspection improve dimensional consistency and performance. Environmental policies promoting recyclable building materials, along with economic growth in emerging urban regions, sustain regional consumption. Increasing integration of digital manufacturing systems, sustainable production practices, and customized profile engineering supports long-term market evolution for industrial decision-makers.

The Aluminum Extrusion Market holds strategic relevance as industries accelerate lightweight engineering, circular manufacturing, and energy-efficient infrastructure. Aluminum extruded profiles enable up to 40% weight reduction in vehicle structures compared to traditional steel components, directly improving fuel efficiency and EV range performance. From a strategy standpoint, manufacturers are investing in high-tonnage presses, closed-loop recycling systems, and digital process control to enhance yield rates and reduce scrap losses by measurable margins. Advanced profile design and simulation-led die engineering support precision manufacturing for high-load applications in rail, aerospace interiors, and photovoltaic mounting frameworks.

Friction Stir Welding–compatible extrusion technology delivers 18% higher joint strength compared to conventional mechanical fastening standards. Asia-Pacific dominates in production volume, while Europe leads in sustainable adoption with over 45% of enterprises integrating recycled-content aluminum in construction systems. By 2028, AI-driven extrusion line monitoring is expected to improve throughput efficiency by 12% while reducing unplanned downtime. Firms are committing to ESG metrics including a 25% reduction in process emissions and over 50% recycled material utilization by 2030. In 2025, a large-scale smart manufacturing initiative in China achieved a 14% energy-consumption reduction through automated thermal control in extrusion presses. As infrastructure, mobility, and renewable sectors converge on lightweight and low-carbon materials, the Aluminum Extrusion Market is positioned as a pillar of resilience, regulatory compliance, and sustainable industrial growth.

Large-scale infrastructure modernization is significantly expanding demand for aluminum extrusion solutions in transportation networks, smart buildings, and renewable energy facilities. Urban construction increasingly utilizes extruded aluminum curtain wall systems, window frames, and façade structures due to their durability, corrosion resistance, and thermal performance. Rail transit projects deploy lightweight aluminum car body sections that reduce overall train weight by up to 15%, improving energy efficiency. Solar energy installations rely on extruded mounting frames engineered for strength and weather resistance, supporting rapid photovoltaic deployment. Industrial machinery sectors also prefer precision aluminum profiles for modular assembly and automation equipment. As governments emphasize sustainable infrastructure and energy-efficient urban design, aluminum extrusions are becoming a standard material choice across high-performance structural applications.

Aluminum extrusion manufacturing requires high thermal energy inputs for billet heating and press operations, making production costs sensitive to electricity and fuel price fluctuations. Energy expenses can account for a significant share of operational expenditure, particularly in regions with limited renewable power integration. Additionally, environmental compliance obligations related to emissions, waste heat management, and process efficiency add complexity to plant operations. Smaller manufacturers face challenges upgrading legacy presses with energy-efficient systems, limiting competitiveness. Logistics costs for transporting billets and finished profiles further impact margins, especially in export-dependent markets. These constraints collectively restrict expansion capacity and influence investment decisions across the aluminum extrusion value chain.

Electric vehicle platforms present substantial opportunities for aluminum extrusion suppliers, as battery enclosures, crash management systems, and structural frames increasingly rely on lightweight aluminum profiles. EV body structures can incorporate over 30% aluminum content, driving demand for high-strength extruded components. Renewable energy infrastructure also fuels growth, with solar mounting systems and wind turbine components utilizing corrosion-resistant aluminum sections for long service life. Modular construction trends create further prospects for prefabricated aluminum framing systems in commercial and residential buildings. Advances in recycling technologies enable closed-loop material flows, supporting cost-efficient and low-carbon production strategies that align with sustainability-focused procurement policies.

The Aluminum Extrusion market faces challenges from tightening environmental regulations, trade policies, and fluctuating raw material supply. Emission reduction mandates require capital-intensive upgrades such as advanced filtration systems and energy-efficient furnaces. Carbon pricing mechanisms in several regions increase compliance costs for energy-intensive metal processing. Additionally, aluminum billet price volatility linked to global supply-demand imbalances affects production planning and contract pricing. Trade tariffs and cross-border restrictions disrupt supply chains, impacting export-oriented producers. Technical requirements for certification in aerospace, automotive, and construction applications further raise quality assurance costs, making regulatory adherence a critical operational hurdle for manufacturers.

• Surge in Lightweight Electric Mobility Integration: Automotive OEMs are increasing the use of extruded aluminum crash structures, battery enclosures, and side-impact beams, with EV platforms now incorporating up to 35% aluminum content in structural assemblies. Lightweight profile adoption has demonstrated vehicle mass reductions of nearly 20%, improving energy efficiency and extending driving range by measurable margins in new-generation electric vehicles.

• Growth in Solar and Renewable Energy Structures: Utility-scale solar installations are accelerating demand for corrosion-resistant aluminum mounting profiles, with solar framing systems accounting for nearly 18% of industrial extrusion demand. Extruded support structures improve installation speed by 25% and enhance lifecycle durability beyond 25 years, particularly in high-humidity and coastal environments.

• Digitalization of Extrusion Manufacturing Lines: Smart extrusion facilities deploying AI-based process monitoring and predictive maintenance systems have reported up to 12% productivity improvements and 15% reductions in defect rates. Automated die correction and real-time thermal control technologies enhance dimensional precision, supporting high-spec applications in aerospace, rail transport, and electronics manufacturing.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Aluminum Extrusion market, where 55% of new projects report cost benefits from prefabrication methods. Pre-cut and pre-bent extruded components manufactured off-site reduce on-site labor by 30% and shorten construction timelines, particularly across Europe and North America where efficiency-driven building practices are expanding.

The Aluminum Extrusion market is segmented by type, application, and end-user industries, each reflecting distinct performance requirements and demand drivers. Product differentiation is largely based on finishing processes, alloy grades, and fabrication complexity, with mill-finished and surface-treated profiles widely used in structural and aesthetic installations. Application segmentation highlights strong penetration in construction frameworks, transportation structures, electrical housings, and industrial machinery assemblies. End-user segmentation demonstrates concentration in construction and infrastructure, automotive and transportation manufacturing, and renewable energy equipment production. High-strength alloys and precision extrusions increasingly serve specialized sectors such as aerospace interiors and advanced electronics cooling systems. Market structure shows that building-related uses account for a substantial portion of demand, while electrification and sustainable design trends are reshaping consumption patterns. Lightweight engineering requirements, recyclability advantages, and improved corrosion resistance ensure continued cross-sector integration of aluminum extruded components.

Aluminum extrusion product types include mill-finished extrusions, anodized profiles, powder-coated extrusions, and fabricated or machined extrusions. Mill-finished extrusions currently account for approximately 38% of total usage, primarily due to their cost efficiency and widespread use in structural frameworks and industrial assemblies. Anodized extrusions represent nearly 27% adoption, offering enhanced corrosion resistance and aesthetic appeal for architectural and marine applications. Powder-coated profiles are gaining rapid traction, recording an estimated CAGR of 6.2% as demand for color customization and weather-resistant surfaces rises in façade systems and transportation interiors. Fabricated and precision-machined extrusions hold a combined 35% share, supporting high-spec uses in automotive crash management systems and electronics enclosures where tight tolerances are critical.

Key application areas include building and construction, transportation, electrical and electronics, machinery equipment, and renewable energy structures. Building and construction leads with nearly 41% utilization, supported by demand for window frames, curtain wall systems, and load-bearing structural profiles. Transportation applications account for around 26%, where lightweight extrusions reduce vehicle mass and improve fuel or energy efficiency. Renewable energy infrastructure is the fastest-growing application, advancing at roughly 7.1% CAGR due to solar mounting systems and wind energy support structures. Electrical and electronics applications hold close to 18% share, emphasizing heat-dissipation enclosures and cable management systems. Remaining industrial machinery uses collectively contribute about 15%.

Construction and infrastructure firms represent the leading end-user segment, contributing approximately 44% of overall demand due to widespread integration of extruded aluminum in urban development and commercial real estate. Automotive and transportation manufacturers account for about 29%, driven by electrification strategies and lightweight vehicle architectures. The renewable energy sector is the fastest-growing end-user group with an estimated CAGR of 7.5%, fueled by expansion in photovoltaic and wind installations. Industrial equipment manufacturers and consumer durables producers together represent nearly 27% of usage, particularly in modular systems and appliance frames. Adoption rates in EV manufacturing facilities exceed 60% for aluminum-intensive structural components.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Asia-Pacific’s dominance is supported by extrusion output exceeding 25 million metric tons annually, with infrastructure projects representing over 40% of regional consumption. North America shows accelerating electrification-driven demand, where aluminum-intensive EV production increased by 22% in the past year. Europe holds close to 24% share, shaped by sustainable construction mandates and recycling targets surpassing 60% for building materials. South America contributes around 6%, supported by industrial modernization and renewable installations. Middle East & Africa represent nearly 5%, driven by mega construction developments and industrial diversification programs. Regional trade flows indicate over 30% of extruded profiles are used in cross-border industrial supply chains, reflecting globalization of lightweight engineering and modular construction systems.

How Is Lightweight Manufacturing Transforming Industrial Material Demand?

This region represents nearly 21% of global aluminum extrusion consumption, supported by strong demand from transportation, aerospace, and commercial construction sectors. Electric vehicle manufacturing facilities increased aluminum profile usage by over 25% in structural battery enclosures and crash systems. Building efficiency regulations encourage adoption of thermally optimized window and façade extrusions, improving insulation performance by up to 18%. Digital manufacturing integration, including AI-driven process control, has improved plant productivity by 12%. Government infrastructure programs exceeding USD 1 trillion focus on bridges, transit systems, and energy networks that rely on corrosion-resistant aluminum profiles. A leading domestic producer expanded automated extrusion lines to increase output capacity by 15%, while regional buyers prioritize sustainable, recyclable materials, reflecting environmentally conscious procurement behavior.

What Drives Sustainable Engineering Material Choices in Industrial Economies?

Europe contributes approximately 24% of global aluminum extrusion utilization, with Germany, France, and the UK acting as core manufacturing hubs. Stringent sustainability frameworks push recycling rates for construction aluminum beyond 60%, influencing procurement standards. Automotive lightweighting initiatives increased aluminum content in passenger vehicles by nearly 20% compared to conventional platforms. Adoption of Industry 4.0 extrusion technologies, including sensor-based die monitoring, enhanced dimensional precision by 10%. Regional climate policies stimulate demand for energy-efficient façade systems and solar support structures. A major European extrusion firm recently upgraded its press lines with electric heating systems, reducing energy consumption per ton by 14%. Buyers demonstrate preference for low-carbon, certified materials aligned with strict environmental compliance expectations.

How Is Industrial Expansion Reshaping Advanced Metal Processing Demand?

Asia-Pacific ranks first in production volume, with China, India, and Japan leading consumption across construction, electronics, and transportation sectors. Regional extrusion capacity exceeds 25 million metric tons annually, supporting rapid infrastructure deployment and manufacturing growth. Urban rail projects increased aluminum carriage adoption by 17%, improving operational efficiency. Smart manufacturing adoption is accelerating, with automated presses and digital quality inspection improving output consistency by 13%. Renewable energy expansion drives aluminum usage in photovoltaic mounting systems, where installations grew by over 20% year-on-year. A major regional producer invested in high-tonnage presses to manufacture large cross-section profiles for high-speed rail and industrial machinery, while buyers favor cost-efficient, durable materials for large-scale infrastructure projects.

How Do Infrastructure and Energy Investments Influence Material Consumption?

South America accounts for roughly 6% of global aluminum extrusion demand, led by Brazil and Argentina. Regional infrastructure initiatives focus on transportation modernization and renewable energy expansion, where aluminum mounting frames support solar installations growing by 18%. Industrial development programs stimulate machinery manufacturing that uses precision extruded components. Trade incentives and regional manufacturing policies encourage local processing of aluminum profiles, reducing import dependence. A regional extrusion manufacturer upgraded its surface treatment line, increasing corrosion resistance performance by 20% for coastal construction projects. Buyers prioritize cost-effective and durable materials, while demand patterns show increasing adoption in energy and industrial applications aligned with modernization strategies.

How Are Industrial Diversification Strategies Expanding Advanced Material Use?

Middle East & Africa represent approximately 5% of global aluminum extrusion consumption, driven by construction, oil and gas infrastructure, and transport projects. The UAE and Saudi Arabia lead regional demand with large-scale urban developments requiring high-performance façade systems. Industrial diversification initiatives increased manufacturing investment by over 15%, supporting growth in local extrusion capacity. Technological modernization includes automated press systems and improved surface finishing techniques. Trade partnerships facilitate raw material flows across regional supply chains. A prominent producer in the Gulf expanded production of architectural profiles, enhancing output capacity by 12%. Buyers in this region emphasize durability and thermal resistance suited to high-temperature environments.

China Aluminum Extrusion Market – 32% share; extensive production capacity and strong infrastructure-driven demand sustain dominance.

United States Aluminum Extrusion Market – 14% share; high adoption in automotive, aerospace, and infrastructure modernization supports leadership.

The Aluminum Extrusion market exhibits a moderately fragmented structure with more than 250 active medium-to-large manufacturers operating across regional and global supply chains. The top five producers collectively account for approximately 34% of global production capacity, reflecting a competitive yet scale-driven environment where technological differentiation and operational efficiency determine positioning. Large players focus on high-tonnage presses exceeding 60 MN capacity, enabling production of wide cross-section structural profiles for transportation and infrastructure sectors. Strategic initiatives include facility automation upgrades delivering productivity gains of 10–15%, cross-border joint ventures to secure billet supply, and partnerships with EV manufacturers to develop lightweight crash management systems.

Product innovation is centered on high-strength 7xxx and corrosion-resistant 6xxx alloy profiles, thermally broken architectural systems, and precision extrusions with tolerances within ±0.05 mm for electronics and aerospace applications. Sustainability has emerged as a competitive lever, with leading firms achieving recycled aluminum usage levels above 50% in selected product lines. Digitalization trends such as AI-enabled press monitoring and predictive maintenance systems are reducing downtime by nearly 12%, improving delivery reliability. Regional players compete on cost and customization, while multinational firms leverage vertically integrated operations, global distribution networks, and value-added fabrication services to maintain strategic advantages.

China Zhongwang Holdings

Hindalco Industries

Kaiser Aluminum

Gulf Extrusions

Jindal Aluminium

Bonnell Aluminum

China Hongqiao Group

Technological progress in the Aluminum Extrusion market is centered on automation, alloy innovation, energy efficiency, and digital process control. Modern extrusion plants deploy high-tonnage hydraulic presses ranging from 35 MN to over 90 MN, enabling production of large, complex profiles for rail transport, aerospace structures, and EV chassis systems. Advanced billet preheating systems with induction heating reduce thermal loss by nearly 20%, improving energy efficiency and extrusion consistency. Inline quenching technologies ensure controlled cooling rates, enhancing mechanical strength in 6xxx and 7xxx series alloys used in high-load applications.

Digital transformation is reshaping production through AI-enabled process monitoring, where sensor networks track temperature, pressure, and ram speed in real time. Predictive maintenance algorithms have reduced unplanned downtime by up to 15%, while automated die correction systems improve dimensional tolerances to within ±0.05 mm. Computer-aided die design and simulation tools shorten development cycles by nearly 30%, supporting faster customization for specialized sectors such as electronics cooling and lightweight mobility.

Surface engineering technologies are also advancing, with anodizing systems increasing corrosion resistance by over 25% and powder coating lines delivering uniform finishes for architectural and transportation uses. Friction stir welding integration enables strong joints without additional fasteners, improving structural integrity by 18%. Recycling technology improvements allow secondary aluminum to constitute more than 50% of input material in some facilities, reducing energy use by up to 90% compared to primary aluminum production. These technological advancements collectively enhance productivity, precision, sustainability, and application versatility across the aluminum extrusion value chain.

• In June 2025, Constellium SE showcased low-carbon aluminium extrusion solutions at Cenex 2025 in the UK, featuring high-recycled-content battery enclosures and crash management systems made from over 90% post-consumer scrap as part of its £10 million CirConAl circular economy initiative. (Quiver Quantitative)

• In June 2025, Constellium SE highlighted innovations in high-performance aluminium products, including its proprietary Airware® aluminium-lithium solution at the 55th Paris Air Show, emphasizing sustainable aerospace applications and recycled aircraft-derived ingots for future aircraft production. (Nasdaq)

• In 2025, Norsk Hydro invested USD 85 million to build a new aluminium casting line at its Henderson, Kentucky facility, adding 28,000 tonnes of annual recycled aluminium capacity targeted at supplying U.S. automotive manufacturers with sustainable extrusion inputs.

• In July 2025, Constellium extended a long-term aluminium supply partnership with Embraer, reinforcing its role in delivering advanced aluminium solutions across commercial, executive jet, and defence sectors from facilities in France and the United States. (MarketScreener UAE Emirates)

The scope of the Aluminum Extrusion Market Report encompasses a comprehensive analysis of product types, application areas, end-users, and technological innovations shaping global consumption and supply. Product segmentation within the report covers mill-finished extrusions, anodized and powder-coated profiles, and fabricated machined sections, illustrating the performance attributes, tolerances, and usage patterns across structural, architectural, and industrial applications. It also examines key application areas such as building and construction structural frames, transportation assemblies, electrical housings, solar mounting systems, and machinery components, noting cross-industry demand drivers tied to durability, corrosion resistance, and design flexibility. Geographically, the report outlines regional consumption trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing market volumes, infrastructure-led demand, and manufacturing capacity footprints in regions with major industrial clusters and policy incentives. The analysis includes the integration of digital manufacturing technologies, such as AI-based process control and predictive maintenance, as well as surface engineering improvements that enhance finishing quality and performance. Additionally, emerging and niche segments—such as high-strength alloy profiles for aerospace, hollow extrusions for EV battery enclosures, and modular extruded framing systems—are explored. The report further assesses regulatory landscapes, environmental standards, and sustainability initiatives that influence material selection and competitiveness within the aluminum extrusion value chain, providing decision-makers with insights into innovation, regional dynamics, and strategic focus areas for future growth.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hydro Extrusions, Constellium, Arconic Corporation, China Zhongwang Holdings, Hindalco Industries, Kaiser Aluminum, Gulf Extrusions, Jindal Aluminium, Bonnell Aluminum, China Hongqiao Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |