Reports

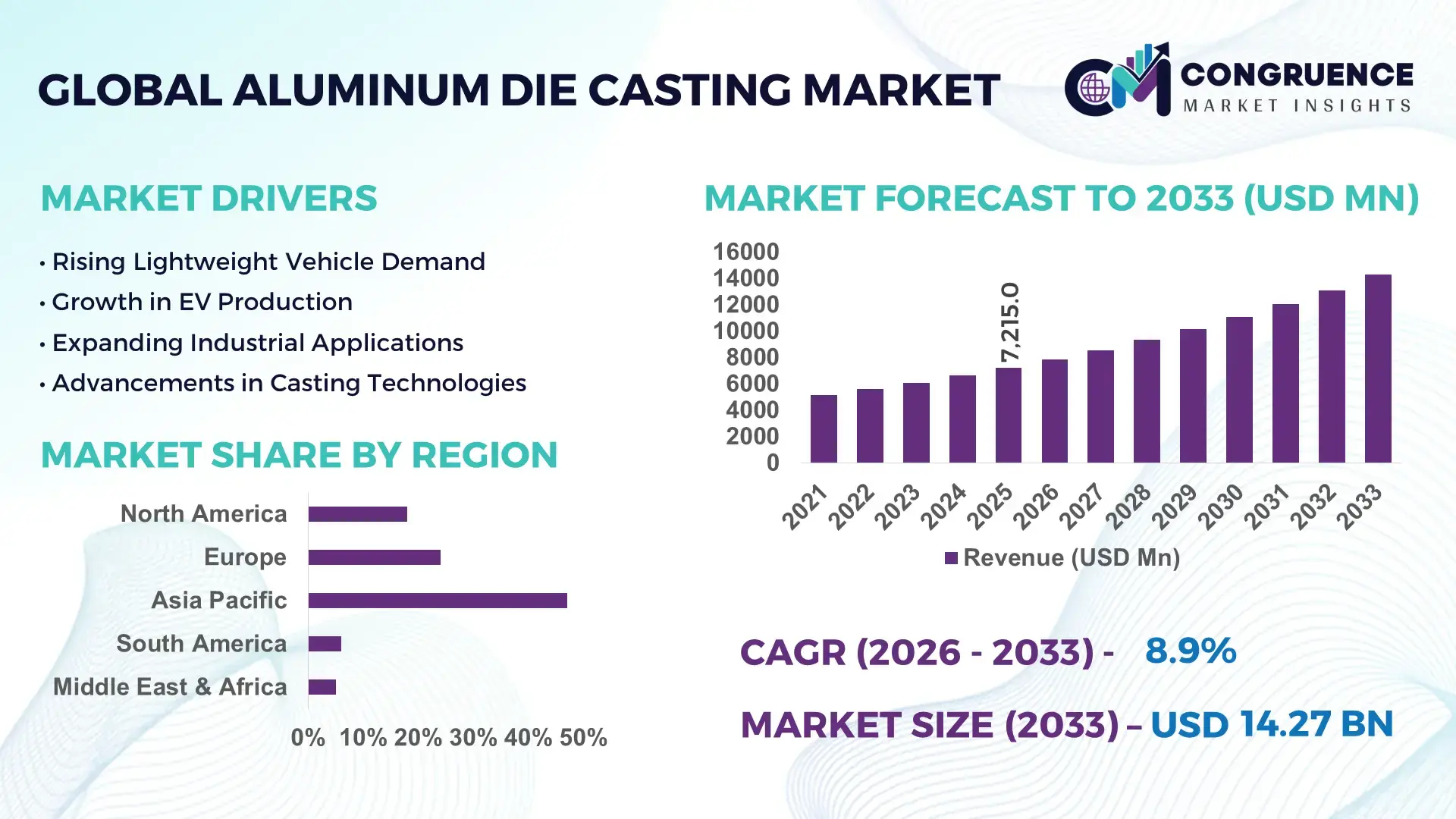

The Global Aluminum Die Casting Market was valued at USD 7,215.0 Million in 2025 and is anticipated to reach a value of USD 14,271.2 Million by 2033 expanding at a CAGR of 8.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by rising lightweight material adoption in automotive, electronics, and industrial machinery applications to enhance fuel efficiency and structural performance.

China represents the dominant country in the Aluminum Die Casting Market, supported by extensive production capacity exceeding 6.5 million metric tons annually across aluminum casting operations. The country hosts more than 3,000 die casting enterprises, including several Tier-1 automotive component suppliers. Automotive applications account for nearly 65% of domestic aluminum die casting demand, particularly for engine blocks, transmission housings, and EV battery enclosures. China’s investment in electric vehicles surpassed USD 120 billion between 2020 and 2024, directly accelerating demand for high-pressure die casting (HPDC) systems. The country has also adopted large-tonnage die casting machines exceeding 6,000 tons clamping force, enabling giga-casting integration in EV chassis manufacturing.

Market Size & Growth: Valued at USD 7,215.0 Million in 2025 and projected to reach USD 14,271.2 Million by 2033 at 8.9% CAGR, driven by 35% higher lightweight component demand in EV platforms.

Top Growth Drivers: 42% EV adoption growth, 28% manufacturing automation expansion, 31% rise in lightweight alloy utilization.

Short-Term Forecast: By 2028, production cycle times are expected to reduce by 18% through advanced high-pressure die casting systems.

Emerging Technologies: Giga-casting machines (6,000–9,000 tons), AI-based mold flow simulation, vacuum-assisted HPDC technology.

Regional Leaders: Asia Pacific projected at USD 6,100.0 Million by 2033 with strong EV manufacturing; North America at USD 3,450.0 Million driven by aerospace demand; Europe at USD 2,980.0 Million supported by lightweight compliance norms.

Consumer/End-User Trends: Automotive contributes over 60% of demand; electronics and industrial machinery collectively account for 25% usage adoption.

Pilot or Case Example: In 2024, an EV OEM implemented giga-casting, reducing component count by 40% and assembly time by 25%.

Competitive Landscape: Nemak (~12%), Ryobi Die Casting, Endurance Technologies, Jaya Hind Industries, Dynacast.

Regulatory & ESG Impact: Emission regulations mandate 15–20% vehicle weight reduction targets; recycling mandates support 75% aluminum reuse rates.

Investment & Funding Patterns: Over USD 2.5 Billion invested globally in die casting plant automation and capacity expansion since 2022.

Innovation & Future Outlook: Integrated casting for EV platforms, digital twin-enabled mold design, and closed-loop aluminum recycling systems are shaping long-term competitiveness.

Automotive accounts for over 60% of Aluminum Die Casting Market demand, followed by industrial machinery (~18%) and electronics (~12%). Structural giga-casting and vacuum HPDC technologies are improving dimensional precision by nearly 20%. Environmental regulations promoting 75% aluminum recycling and lightweight emission compliance are accelerating adoption. Asia Pacific leads consumption volume, while North America demonstrates strong aerospace-driven growth. Increasing EV battery housing integration and modular casting systems are expected to redefine manufacturing efficiency over the next decade.

The Aluminum Die Casting Market holds strategic relevance due to its critical role in automotive lightweighting, EV integration, aerospace engineering, and industrial automation. Lightweight aluminum components reduce vehicle mass by 30–40% compared to traditional steel structures, directly improving fuel efficiency and battery performance. High-pressure die casting (HPDC) combined with vacuum-assisted systems delivers 22% higher structural integrity compared to gravity casting processes.

Asia Pacific dominates in production volume, while Europe leads in advanced adoption with over 48% of automotive OEMs integrating structural aluminum casting platforms. By 2028, AI-enabled predictive maintenance in die casting facilities is expected to reduce machine downtime by 20% and defect rates by 15%. ESG priorities are reshaping manufacturing strategies, with firms committing to 50% recycled aluminum input usage by 2030 and targeting 30% energy consumption reduction in smelting and casting operations.

In 2024, a Chinese EV manufacturer achieved a 35% reduction in assembly complexity by implementing 8,000-ton giga-casting machines for rear underbody structures. Such initiatives illustrate how automation and integrated casting streamline production while reducing cost variability.

Looking ahead, the Aluminum Die Casting Market is positioned as a pillar of resilience, compliance, and sustainable industrial growth, driven by automation, circular material strategies, and EV-centric platform innovation.

The Aluminum Die Casting Market is characterized by strong demand from automotive electrification, aerospace modernization, and industrial equipment manufacturing. Increasing regulatory mandates targeting emission reduction and fuel efficiency are accelerating substitution of steel with aluminum alloys. Manufacturing facilities are increasingly integrating robotics and AI-based defect detection systems, improving yield efficiency by 10–15%. Supply chain localization strategies in North America and Europe are driving capacity expansion projects exceeding 500,000 metric tons annually in selected regions. Raw material price fluctuations and energy-intensive smelting processes remain critical operational considerations. Simultaneously, the growing adoption of giga-casting and modular structural components is transforming production methodologies, reducing part counts by up to 40% in EV chassis manufacturing.

Global EV production exceeded 14 million units in 2024, reflecting a 35% year-over-year increase. Aluminum die casting plays a vital role in manufacturing lightweight battery enclosures, motor housings, and structural frames. A typical EV contains 30–40% more aluminum components compared to internal combustion vehicles. Structural giga-casting reduces welding points by 50% and enhances torsional rigidity by nearly 20%. Major OEMs are integrating single-piece rear underbody castings, reducing component count from over 70 parts to less than 5. Such integration significantly improves assembly efficiency and supports large-scale EV platform standardization.

Aluminum smelting and die casting are energy-intensive, requiring approximately 13–15 kWh per kilogram of primary aluminum production. Rising industrial electricity tariffs—up by 18% in several manufacturing economies between 2022 and 2024—directly impact operational costs. Additionally, molten aluminum handling requires advanced thermal control systems to maintain quality consistency. Carbon emission compliance obligations require capital-intensive filtration and monitoring systems. These factors increase upfront capital expenditure by nearly 20% for new facilities, limiting expansion in cost-sensitive regions.

Giga-casting technology enables single-piece structural components weighing over 100 kg using machines exceeding 6,000 tons clamping force. This reduces part complexity by 40–60% and lowers assembly time by 25%. Automotive manufacturers adopting giga-casting report tooling cost reductions of nearly 15% over lifecycle production runs. The global expansion of EV gigafactories—over 300 announced projects—creates substantial demand for integrated structural casting solutions. Emerging markets in Southeast Asia and Eastern Europe are investing in advanced die casting clusters to meet export demand.

Aluminum prices have demonstrated volatility exceeding 25% within single fiscal years due to geopolitical tensions and supply chain disruptions. Bauxite mining constraints and energy supply uncertainties impact upstream supply consistency. Die casting manufacturers must maintain precise alloy composition tolerances, often requiring premium-grade inputs. Inventory hedging strategies increase working capital requirements by 10–15%. Additionally, global logistics disruptions have increased lead times by up to 20%, affecting just-in-time manufacturing commitments for automotive OEMs.

Expansion of Giga-Casting Platforms: Automotive OEMs are deploying die casting machines exceeding 6,000–9,000 tons clamping force, enabling single-piece structural castings over 100 kg. Component count reductions of 40% and assembly time savings of 25% are being achieved, particularly in EV underbody manufacturing.

Integration of AI-Based Quality Control: AI-powered defect detection systems improve casting yield rates by 15% and reduce scrap levels by 12%. Smart sensors embedded in molds monitor temperature deviations within ±2°C accuracy, enhancing dimensional precision by nearly 18%.

Growth in Recycled Aluminum Usage: Over 75% of aluminum used in automotive die casting in developed markets now incorporates recycled content. Secondary aluminum production consumes up to 95% less energy compared to primary smelting, significantly lowering carbon intensity metrics.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Aluminum Die Casting Market. Research suggests that 55% of new projects report cost benefits through prefabrication. Pre-engineered aluminum components reduce onsite labor requirements by 30% and accelerate project timelines by 20%, particularly in Europe and North America where industrialized construction adoption exceeds 45%.

The Aluminum Die Casting Market is segmented by type, application, and end-user, reflecting diversified industrial demand patterns and technological specialization. By type, high-pressure die casting (HPDC), low-pressure die casting (LPDC), and gravity die casting dominate production frameworks, with HPDC accounting for the majority of structural automotive components due to its dimensional precision and scalability. Application-wise, automotive remains the primary consumption area, followed by industrial machinery, electrical & electronics, aerospace, and construction equipment. End-user segmentation highlights OEM automotive manufacturers as the principal adopters, alongside Tier-1 suppliers and industrial equipment producers. Increasing electrification, automation, and lightweight material mandates are shaping demand concentration across these segments. Precision requirements, energy efficiency targets, and structural integration capabilities continue to influence procurement strategies and capital allocation decisions across manufacturing ecosystems.

High-Pressure Die Casting (HPDC) currently accounts for approximately 68% of total adoption, driven by its suitability for high-volume automotive production and thin-walled complex geometries. Low-Pressure Die Casting (LPDC) holds nearly 18%, while Gravity Die Casting represents around 9%. The remaining 5% includes vacuum die casting and squeeze casting technologies. HPDC leads due to faster cycle times—often 30–40% shorter than gravity casting—and superior dimensional consistency within ±0.1 mm tolerance. While HPDC dominates, vacuum-assisted and giga-casting systems are the fastest-growing types, expanding at an estimated CAGR of 10.8% through 2033. Growth is fueled by EV structural integration, where single-piece castings exceeding 100 kg reduce part complexity by 40–60%. LPDC maintains relevance in wheel manufacturing and aerospace components due to enhanced metallurgical integrity. Gravity casting remains niche but critical for heavy-duty industrial parts requiring thicker wall sections. Combined, LPDC and gravity casting contribute 27% of market demand, reflecting their steady industrial usage.

Automotive applications account for approximately 62% of total Aluminum Die Casting Market utilization, driven by engine blocks, transmission housings, battery enclosures, and structural chassis components. Industrial machinery contributes 15%, electrical & electronics represent 10%, aerospace accounts for 7%, and other sectors collectively contribute 6%. Automotive remains dominant due to increasing EV penetration and regulatory-driven lightweight mandates requiring 20–30% structural mass reduction. Industrial machinery applications are expanding steadily; however, aerospace is the fastest-growing application segment, advancing at an estimated CAGR of 9.6% due to demand for lightweight airframe and propulsion components. Electronics adoption is supported by thermal conductivity advantages, particularly in heat sinks and enclosures. Aerospace growth is reinforced by rising aircraft production volumes exceeding 35,000 projected deliveries over the next two decades. In 2025, more than 41% of global automotive OEMs reported integrating structural aluminum castings into next-generation EV platforms. Additionally, 38% of industrial equipment manufacturers indicated pilot adoption of lightweight aluminum housings to improve energy efficiency metrics.

OEM automotive manufacturers represent the leading end-user segment, accounting for nearly 58% of overall demand. Tier-1 automotive suppliers contribute approximately 22%, while industrial equipment manufacturers represent 10%. Aerospace manufacturers and electronics producers collectively account for 10%. OEM dominance stems from vertically integrated EV production and structural casting consolidation initiatives. While OEMs lead in volume, aerospace manufacturers are the fastest-growing end-user segment, expanding at an estimated CAGR of 9.2%, supported by fleet modernization programs and fuel efficiency requirements mandating 15–20% structural weight reduction targets. Tier-1 suppliers continue expanding die casting capabilities to meet localized supply chain mandates, with 45% of suppliers in North America increasing aluminum casting capacity between 2022 and 2024. In 2025, approximately 44% of global EV manufacturers adopted giga-casting platforms for rear or front underbody structures. Furthermore, 36% of industrial automation firms reported increasing procurement of aluminum die-cast housings for robotics and motion control systems.

Asia Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Asia Pacific’s leadership is supported by production volumes exceeding 7 million metric tons annually across aluminum casting operations, with China, Japan, and India contributing more than 70% of regional output. Over 60% of EV battery housing castings manufactured globally originate from Asia Pacific facilities. Europe accounted for approximately 24% of global demand in 2025, driven by automotive lightweight compliance and aerospace engineering precision standards. North America held nearly 18% share, supported by structural casting integration in EV manufacturing platforms. South America and Middle East & Africa collectively represented 11%, reflecting growing industrialization and infrastructure modernization. More than 55% of newly installed high-tonnage die casting machines above 6,000 tons were commissioned in Asia Pacific, while North America saw a 22% rise in plant automation upgrades between 2022 and 2024.

North America accounted for approximately 18% of the global Aluminum Die Casting Market volume in 2025. The automotive sector drives nearly 65% of regional demand, followed by aerospace at 15% and industrial machinery at 12%. Regulatory frameworks such as Corporate Average Fuel Economy (CAFE) standards require continuous vehicle weight optimization, encouraging aluminum substitution. Over 40% of EV assembly plants in the United States integrated large structural die casting units above 6,000 tons by 2024. Digital transformation is accelerating, with nearly 48% of die casting facilities deploying AI-enabled predictive maintenance systems to reduce downtime by 15%. Nemak operates multiple advanced casting facilities in Mexico and the U.S., focusing on EV battery housings and structural components, increasing automation intensity by 20% since 2023. Regional enterprise behavior reflects higher adoption in automotive and aerospace OEMs, with 44% of manufacturers piloting giga-casting technologies for integrated vehicle platforms.

Europe held nearly 24% share of the Aluminum Die Casting Market in 2025, with Germany contributing over 30% of regional consumption, followed by France, Italy, and the UK. Automotive applications represent approximately 58% of European demand, while aerospace contributes 14%. The European Green Deal and fleet emission targets require 15–20% vehicle weight reduction benchmarks, intensifying demand for lightweight alloys. More than 52% of casting plants in Germany upgraded to energy-efficient furnaces between 2021 and 2024, lowering energy intensity by 18%. Vacuum-assisted high-pressure die casting adoption exceeds 35% among Tier-1 automotive suppliers. Ryobi Die Casting operates advanced facilities in Europe, enhancing structural casting precision for hybrid and EV platforms. Regional enterprise procurement emphasizes traceable recycled aluminum, with over 60% of OEMs mandating documented recycled input ratios in supplier contracts.

Asia Pacific leads global volume production, contributing nearly 47% of total market output in 2025. China alone accounts for more than 60% of regional capacity, followed by Japan, India, and South Korea. Over 3,000 die casting enterprises operate in China, with annual production capacity exceeding 6.5 million metric tons. Automotive applications represent nearly 68% of regional demand. Manufacturing hubs in Guangdong, Zhejiang, and Maharashtra are investing heavily in high-tonnage machines exceeding 8,000 tons clamping force. Japan maintains advanced precision casting standards, particularly in hybrid vehicle systems. Endurance Technologies expanded aluminum die casting capacity in India by 25% between 2022 and 2024 to serve EV OEMs. Consumer demand patterns indicate that 50% of EV manufacturers in the region are integrating modular structural castings to reduce assembly complexity by 30%.

South America represents approximately 6% of global Aluminum Die Casting Market share, with Brazil accounting for nearly 55% of regional demand, followed by Argentina at 18%. Automotive manufacturing remains the principal driver, contributing over 60% of casting utilization, while energy and agricultural equipment account for 20%. Brazil’s industrial modernization programs have increased domestic vehicle production capacity by 12% between 2022 and 2024. Trade incentives within regional economic blocs encourage localized component manufacturing. Several Brazilian casting firms expanded automation adoption by 15% to improve yield efficiency. Regional procurement trends show preference for cost-efficient structural components, with 35% of manufacturers shifting toward higher recycled aluminum input to manage cost volatility.

Middle East & Africa accounts for nearly 5% of global Aluminum Die Casting Market demand, led by the UAE and South Africa. Oil & gas equipment manufacturing and construction machinery contribute approximately 40% of regional demand, while automotive assembly accounts for 35%. Industrial diversification strategies under national development programs have increased manufacturing investments by 18% since 2021. The UAE has implemented advanced manufacturing initiatives integrating robotics in over 30% of industrial facilities. South Africa’s automotive sector produces more than 600,000 vehicles annually, stimulating structural casting requirements. Regional consumer behavior indicates increasing adoption of digitally monitored casting processes, with 28% of facilities integrating IoT-based temperature monitoring systems for quality consistency.

China – 32% Market Share: It leads due to extensive production capacity exceeding 6.5 million metric tons annually and strong EV manufacturing integration.

Germany – 11% Market Share: It's dominance is supported by advanced automotive engineering, precision casting expertise, and strict lightweight regulatory mandates.

The Aluminum Die Casting Market is moderately fragmented, with over 1,500 active manufacturers operating globally, including large multinational corporations and regionally specialized Tier-1 and Tier-2 suppliers. The top five companies collectively account for approximately 38–42% of global production volume, reflecting partial consolidation in high-precision automotive and aerospace segments. Leading participants compete primarily on production scale, technological sophistication, alloy development capabilities, and long-term OEM supply contracts.

Strategic expansion initiatives increased by nearly 22% between 2022 and 2025, largely focused on installing high-tonnage die casting machines above 6,000 tons to support giga-casting platforms. More than 30 large-scale machine installations were commissioned globally during this period. Partnerships between die casting firms and EV manufacturers have risen by 28%, emphasizing structural integration and lightweight platform standardization. Automation investment remains a differentiator, with 45% of top-tier manufacturers integrating AI-based defect detection and robotic extraction systems to reduce scrap rates by 10–15%.

Mergers and acquisitions activity has remained steady, with cross-border acquisitions aimed at securing localized supply chains and recycled aluminum sourcing. Competitive positioning increasingly depends on ESG alignment, where over 60% of major players have committed to achieving at least 50% recycled aluminum input in production by 2030. The competitive environment emphasizes operational efficiency, precision engineering, and advanced process innovation to secure multi-year OEM contracts.

Endurance Technologies

Jaya Hind Industries

GF Casting Solutions

Martinrea International

Alcast Technologies

Pace Industries

Shiloh Industries

Rockman Industries

Bodine Aluminum

Rheinmetall Automotive (KS HUAYU AluTech)

Ahresty Corporation

Consolidated Metco (ConMet)

Technological advancement is central to competitiveness in the Aluminum Die Casting Market. High-Pressure Die Casting (HPDC) remains dominant, accounting for nearly 68% of global production processes due to its ability to achieve thin-wall geometries below 2.5 mm and dimensional tolerances within ±0.1 mm. The integration of giga-casting machines exceeding 8,000–9,000 tons clamping force has enabled production of single-piece structural components weighing over 100 kg, reducing assembly part counts by up to 40%.

Vacuum-assisted die casting technology is increasingly deployed to minimize porosity, improving mechanical strength by nearly 20% compared to conventional HPDC. Real-time thermal monitoring systems equipped with IoT sensors track mold temperature fluctuations within ±2°C, enhancing casting consistency and reducing rejection rates by 12–15%.

Digital twin modeling and AI-driven mold flow simulation software reduce tooling development cycles by approximately 25%, allowing manufacturers to optimize gating systems and metal flow prior to physical trials. Automation integration is also accelerating; more than 50% of new die casting facilities commissioned after 2023 incorporate robotic extraction, automated trimming, and inline X-ray inspection systems.

Sustainability-driven technologies are equally impactful. Secondary aluminum usage consumes up to 95% less energy than primary aluminum production, and over 70% of automotive-grade castings in developed markets now include recycled content. Closed-loop scrap recovery systems can reclaim 98% of internal production scrap, significantly lowering material wastage and carbon intensity. These technological developments collectively enhance structural performance, operational efficiency, and environmental compliance across the market.

• In July 2025, Nemak signs agreement to acquire GF Casting Solutions’ automotive business, marking a strategic move to expand its aluminum die casting capabilities and strengthen its lightweight structural component portfolio across global automotive markets, particularly for electric vehicle chassis and powertrain applications. Source: www.idrawater.org

• On 12 Feb 2026, Nemak completes the acquisition of GF Casting Solutions’ automotive business, integrating approximately US$707 million in annual automotive casting operations and nine production facilities in Europe, China, US, and other regions, significantly broadening its footprint and customer base. Source: www.nemak.com

• In Apr 2025, Hydro and Nemak signed a letter of intent (LOI) to develop low-carbon aluminum casting products for automotive applications, focused on decarbonizing supply chains and developing alloys with CO₂ footprints below 3.0 kg per kilo of aluminum. This collaboration aims to advance circular product solutions for OEMs pursuing sustainability goals. Source: www.hydro.com

• In Jun 2024, Ryobi to expand Mexico‑based factory augmenting its casting facilities expanded its aluminum die casting footprint by increasing capacity at its Mexico plant to meet rising demand for automotive cast components, particularly for electrification and structural applications. Source: www.ryobi-group.co.jp

The Aluminum Die Casting Market Report provides a comprehensive evaluation of structural casting technologies, industrial demand patterns, and geographic expansion strategies. The scope covers segmentation by type—including High-Pressure Die Casting (HPDC), Low-Pressure Die Casting (LPDC), gravity casting, and vacuum-assisted processes—representing over 95% of global casting methodologies. Application analysis spans automotive, aerospace, industrial machinery, electrical & electronics, and construction equipment, collectively accounting for more than 90% of total consumption volume.

Geographically, the report examines five primary regions—Asia Pacific, North America, Europe, South America, and Middle East & Africa—covering over 50 key manufacturing countries. It assesses production capacities exceeding 10 million metric tons globally and evaluates infrastructure investments in more than 300 large-scale casting facilities commissioned in the past decade.

The scope includes analysis of giga-casting adoption trends, automation penetration levels surpassing 45% in advanced facilities, and recycled aluminum utilization rates approaching 75% in developed markets. It also addresses regulatory compliance requirements related to emission standards, lightweight mandates, and circular economy policies. Emerging niche segments such as integrated EV chassis casting and aerospace-grade precision housings are evaluated alongside traditional engine and transmission components.

Overall, the report offers strategic insights into manufacturing modernization, supply chain localization, technological innovation, and sustainability integration, enabling decision-makers to assess risk exposure, capacity expansion planning, and long-term competitive positioning within the Aluminum Die Casting Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 7,215.0 Million |

| Market Revenue (2033) | USD 14,271.2 Million |

| CAGR (2026–2033) | 8.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Nemak; Ryobi Die Casting; Dynacast International; Endurance Technologies; Jaya Hind Industries; GF Casting Solutions; Martinrea International; Alcast Technologies; Pace Industries; Shiloh Industries; Rockman Industries; Bodine Aluminum; Rheinmetall Automotive (KS HUAYU AluTech); Ahresty Corporation; Consolidated Metco (ConMet) |

| Customization & Pricing | Available on Request (10% Customization Free) |