Reports

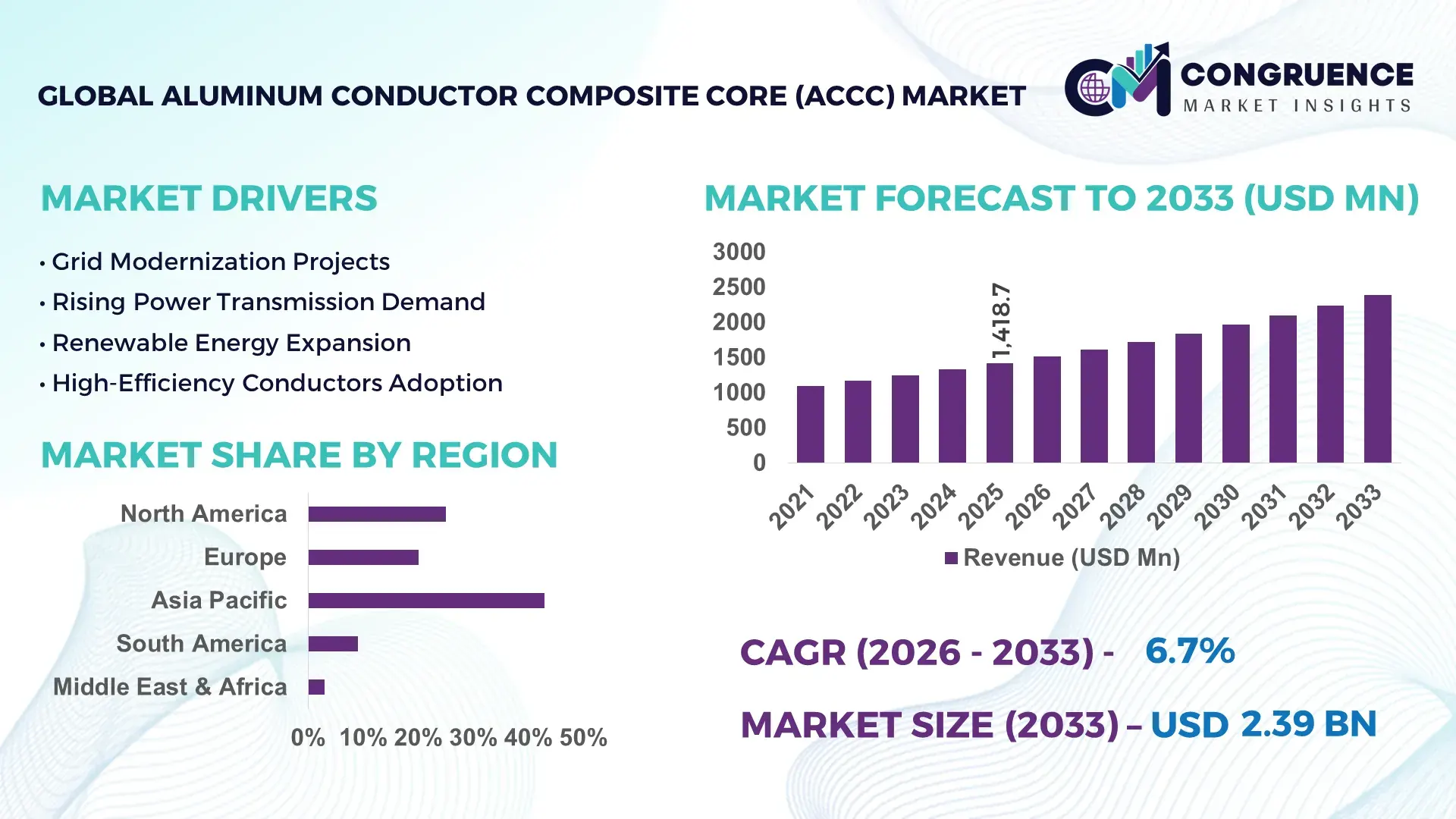

The Global Aluminum Conductor Composite Core (ACCC) Market was valued at USD 1418.7 Million in 2025 and is anticipated to reach a value of USD 2388.81 Million by 2033 expanding at a CAGR of 6.73% between 2026 and 2033. The market is strengthening through rapid transmission grid modernization, renewable energy integration, and replacement of aging steel-core conductors with advanced composite alternatives that improve transmission efficiency by nearly 30% and increase ampacity by over 35% versus conventional conductors.

China leads the market with nearly 34% share of global transmission infrastructure additions, supported by over USD 80 billion in ultra-high-voltage grid investments and integration of more than 520 GW renewable power capacity. Domestic utilities expanded ACCC deployment across western renewable hubs and eastern industrial clusters, while local manufacturers account for approximately 38% of global aluminum conductor production capacity. Compared with conventional ACSR systems, Chinese ACCC installations reduced transmission losses by around 28% in selected high-voltage projects.

Utilities and transmission operators are prioritizing ACCC adoption to improve grid reliability, reduce congestion losses, and strengthen long-distance power transfer economics.

Market Size & Growth: USD 1418.7 million in 2025 reaching USD 2388.81 million by 2033, driven by renewable grid expansion and high-capacity transmission upgrades.

Top Growth Drivers: Renewable integration demand rose 31%, grid modernization spending increased 27%, and transmission efficiency targets improved 22% globally.

Short-Term Forecast: By 2028, advanced ACCC deployment is projected to reduce transmission losses by 18% and improve line capacity by 35%.

Emerging Technologies: AI-based grid monitoring, composite core engineering, and automated conductor inspection improved operational efficiency by nearly 24%.

Regional Leaders: Asia-Pacific exceeds USD 980 million, North America crosses USD 540 million, and Europe surpasses USD 430 million through smart-grid investments.

Consumer/End-User Trends: Nearly 46% of utilities prioritized high-temperature low-sag conductors for renewable-heavy transmission corridors in 2026.

Pilot/Case Example: In 2026, a large-scale Asian transmission project improved power transfer capability by 38% after ACCC installation.

Competitive Landscape: Leading suppliers collectively control nearly 41% market share alongside expanding regional manufacturing partnerships.

Regulatory & ESG Impact: Grid decarbonization programs lowered transmission-related energy waste by approximately 17% across regulated utility projects.

Investment & Funding: More than USD 12 billion entered global transmission modernization programs through utility partnerships and regional infrastructure expansion.

Innovation & Future Outlook: Lightweight composite conductors, digital grid analytics, and cross-border transmission upgrades are reshaping high-growth utility infrastructure strategies.

Power utilities contribute nearly 48% of overall ACCC demand, followed by renewable energy integration projects at 29% and industrial transmission upgrades at 15%. Manufacturers are introducing carbon-fiber composite core technologies with improved thermal stability and lower sag performance to support long-distance power transfer efficiency. Asia-Pacific remains the strongest demand center due to rapid renewable capacity additions, while North America accelerates replacement of aging transmission assets. Supply chain localization initiatives and stricter grid-efficiency regulations are strengthening regional production strategies. Increasing deployment of AI-enabled grid monitoring platforms is expected to further optimize advanced conductor performance and long-term transmission reliability.

The Aluminum Conductor Composite Core (ACCC) market is becoming strategically important as utilities accelerate transmission modernization to support electrification, renewable integration, and grid reliability targets. Governments in China, India, and the United States are restructuring transmission infrastructure investments following supply-chain disruptions and rising peak-load pressure across industrial corridors. Utilities deploying advanced composite conductors are achieving transmission loss reductions of nearly 25% while increasing line capacity by more than 35% without constructing additional towers, creating a significant operational advantage in congested networks.

Compared with conventional steel-core conductors, ACCC systems deliver lower thermal sag and nearly 20% lower lifecycle maintenance costs under high-load conditions. China continues leading large-scale deployment through ultra-high-voltage transmission programs, while the United States focuses on reconductoring aging grids to improve renewable connectivity and wildfire resilience. Between 2026 and 2028, utilities are expected to prioritize digital grid integration, with over 40% of new transmission upgrades incorporating smart monitoring and predictive maintenance technologies.

Large transmission contractors are expanding partnerships with composite material suppliers to secure localized manufacturing and reduce procurement volatility. Companies investing early in high-efficiency conductor technologies, grid analytics integration, and utility-scale deployment capabilities are strengthening long-term competitive positioning across modern transmission infrastructure markets.

Rapid transmission modernization programs are accelerating ACCC adoption across high-load electricity corridors. Utilities upgrading renewable-heavy grids are reporting nearly 30% higher transmission efficiency and over 35% greater ampacity compared with legacy steel-core conductors. India increased interstate transmission investments by approximately 28% during 2025–2026 to support solar and wind integration exceeding 220 GW capacity. Simultaneously, U.S. utilities expanded reconductoring programs to strengthen wildfire resilience and reduce thermal line sag under extreme weather conditions. These operational pressures are pushing manufacturers toward localized composite core production, strategic aluminum sourcing agreements, and utility partnerships focused on long-distance power transfer optimization. A critical strategic shift involves replacing tower expansion projects with high-capacity conductor retrofits, enabling utilities to improve network performance while avoiding land acquisition and permitting delays.

Fluctuating carbon fiber and aluminum prices continue pressuring ACCC deployment economics, particularly across cost-sensitive utility projects. Composite core material costs increased nearly 18% during recent supply-chain disruptions, while specialized installation requirements raised transmission upgrade expenses by approximately 12% compared with standard conductor replacement programs. Several utilities in Southeast Asia and Latin America still operate aging substations and tower configurations incompatible with high-capacity composite conductors, slowing deployment scalability. Chinese manufacturers are responding through domestic carbon fiber integration and long-term procurement contracts to stabilize pricing exposure. Utilities are also diversifying suppliers and adopting phased reconductoring strategies to reduce operational disruption. A significant operational challenge remains the limited availability of certified installation expertise, which directly affects deployment timelines and transmission reliability performance.

Utilities are increasingly positioning ACCC infrastructure within broader digital transmission ecosystems combining AI-based monitoring, predictive maintenance, and dynamic load optimization. Smart conductor monitoring platforms improved fault detection efficiency by nearly 26% in pilot utility deployments during 2026, while automated thermal analytics reduced outage response times by approximately 19%. India and Saudi Arabia are expanding high-voltage transmission corridors linked to renewable energy zones, creating substantial demand for lightweight composite conductors capable of long-distance power transfer under extreme temperatures. Manufacturers are investing in next-generation carbon-glass hybrid cores and modular installation systems to improve scalability and reduce installation complexity. An emerging strategic opportunity involves integrating ACCC systems into cross-border transmission projects, where utilities prioritize higher efficiency without expanding right-of-way infrastructure or constructing additional transmission towers.

Scaling ACCC deployment across national transmission systems requires significant coordination between utilities, EPC contractors, and composite material suppliers. More than 32% of utilities upgrading legacy transmission infrastructure face integration delays caused by incompatible hardware configurations and limited high-voltage testing capacity. In the United States and Germany, stricter grid reliability standards and cybersecurity requirements for digital monitoring systems are increasing project validation timelines by nearly 15%. Utilities also face workforce limitations, as specialized installation and maintenance training for composite conductor systems remains concentrated among a limited group of engineering contractors. Companies must strengthen technical certification programs, expand localized manufacturing, and improve interoperability between smart-grid software and transmission hardware. Long-term competitiveness will depend on execution consistency, utility confidence, and the ability to standardize advanced conductor deployment across complex grid environments.

Localized Composite Core Manufacturing Utilities and conductor manufacturers are restructuring procurement networks as carbon fiber supply volatility and shipping delays continue affecting transmission projects. China and India increased localized composite material sourcing by nearly 24% during 2026, while utility procurement cycles shortened by approximately 18% through domestic manufacturing agreements. Companies are expanding regional production facilities and long-term aluminum contracts to stabilize installation timelines and reduce exposure to imported specialty materials.

AI-Enabled Transmission Monitoring Expansion Utilities are integrating AI-driven thermal monitoring and predictive maintenance platforms into high-capacity transmission corridors. Smart monitoring adoption increased by nearly 31% across newly upgraded grids, while automated fault diagnostics reduced outage response time by approximately 21%. U.S. transmission operators are partnering with grid analytics providers to optimize conductor loading under extreme weather conditions, improving operational reliability without expanding physical transmission infrastructure.

High-Temperature Reconductoring Acceleration Aging transmission networks in Germany, Japan, and the United States are shifting toward high-temperature low-sag reconductoring programs instead of tower replacement strategies. Advanced ACCC deployment improved power transfer capability by over 35% in selected utility corridors while lowering line-loss exposure by nearly 20%. EPC contractors are scaling specialized installation teams and modular deployment processes to accelerate retrofit efficiency and reduce grid downtime during modernization cycles.

Cross-Border Grid Integration Projects Governments are accelerating long-distance interconnection projects to strengthen energy security and renewable balancing capabilities following global power supply disruptions. Cross-border transmission investments increased approximately 27% during 2025–2026, driving demand for lightweight conductors capable of operating under higher thermal loads. Utilities are forming multi-country technology partnerships and prioritizing digitally monitored transmission systems to improve operational coordination, congestion management, and renewable electricity transfer efficiency.

High Capacity Conductors dominate the ACCC market with nearly 36% deployment concentration due to superior ampacity, lower thermal sag, and compatibility with utility-scale transmission upgrades. Utilities in China, India, and the United States are prioritizing these conductors for congested high-voltage corridors where transmission expansion faces land and permitting constraints. ACCC ULS Conductors represent the fastest-growing segment, with adoption increasing by approximately 28% during 2025–2026 as utilities seek lightweight solutions for aging tower infrastructure and renewable-heavy grids. Compared with mature ACCC Helsinki and ACCC Lisbon variants used in established transmission projects, ULS systems offer improved installation flexibility and reduced structural loading requirements. ACCC Oslo conductors continue gaining strategic relevance in colder climate transmission networks due to enhanced thermal stability under variable weather conditions. Manufacturers are expanding product-specific engineering partnerships, automated conductor testing capabilities, and composite core innovations to strengthen deployment scalability and utility customization across high-load transmission systems.

Power Transmission continues leading ACCC application demand with approximately 41% share due to rising electricity loads, industrial electrification, and high-voltage corridor expansion. Utilities are increasingly replacing legacy conductors with advanced composite systems to improve current carrying capacity and reduce thermal losses across long-distance transmission routes. Renewable Energy Integration is the fastest-growing application segment, expanding by nearly 30% during 2025–2026 as countries accelerate solar and wind connectivity into national grids. Grid Modernization and Smart Grid Networks are also strengthening deployment activity through AI-enabled monitoring and dynamic load management integration. Utility Upgrades remain operationally critical in the United States and India, where aging infrastructure replacement programs are accelerating reconductoring investments. Companies are responding through digital monitoring partnerships, specialized installation capabilities, and modular deployment systems designed to improve project speed, reliability, and network efficiency across high-load transmission environments.

Utilities remain the dominant end-user group, accounting for nearly 48% of ACCC deployment activity due to extensive transmission infrastructure ownership and ongoing grid modernization programs. Large power utilities in China, India, and the United States are prioritizing high-capacity conductor upgrades to manage peak electricity demand and renewable integration pressure. The Renewable Energy Sector represents the fastest-growing end-user segment, with deployment activity increasing by approximately 29% during 2025–2026 as developers expand grid connectivity for utility-scale solar and wind projects. Government Power Agencies continue supporting strategic transmission expansion through cross-border interconnection programs and energy security initiatives. Infrastructure Developers and Energy Transmission Companies are increasing partnerships with conductor manufacturers to accelerate reconductoring projects and improve installation efficiency. Industrial Facilities are adopting advanced conductors selectively for captive power transmission systems requiring stable high-load performance and reduced maintenance exposure under continuous operating conditions.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.91% between 2026 and 2033.

Grid Reconductoring and Resilience Investments Accelerating Deployment

North America represents a strategically advanced ACCC market driven by aging transmission infrastructure replacement, renewable integration, and wildfire resilience upgrades. The region contributes nearly 26% of global deployment activity, with the United States accounting for the highest concentration of high-capacity reconductoring projects. Utilities are increasingly replacing legacy steel-core conductors to improve line efficiency and reduce thermal sag across congested transmission corridors. During 2026, several utilities expanded digital transmission monitoring integration, improving operational load management by approximately 22%. Long-distance renewable connectivity projects across Texas and the Midwest continue strengthening demand for lightweight composite conductors. Manufacturers are responding through localized production expansion, utility partnerships, and advanced installation engineering programs focused on faster grid modernization execution.

United States Market Outlook: The United States leads regional ACCC deployment through large-scale transmission modernization, renewable interconnection projects, and wildfire mitigation investments. More than 38% of planned high-voltage reconductoring activity in North America is concentrated in U.S. utility corridors. Utilities are prioritizing advanced conductors to increase transmission capacity without constructing additional towers, particularly across renewable-heavy western states. Federal infrastructure modernization programs and smart-grid integration initiatives are accelerating deployment of digitally monitored transmission systems across interstate electricity networks.

Cross-Border Grid Modernization Driving Advanced Conductor Adoption

Europe is strengthening ACCC deployment through cross-border electricity interconnection projects, renewable balancing infrastructure, and transmission efficiency mandates. The region contributes nearly 21% of global advanced conductor demand, supported by grid decarbonization targets and electrification of industrial operations. Germany, France, and the Nordic countries are prioritizing high-temperature low-sag conductor systems to improve renewable transmission reliability under constrained land availability. During 2025–2026, utilities expanded interconnection investments by approximately 19% to strengthen energy security following regional power supply volatility. Companies are increasing partnerships with composite material suppliers and engineering firms to accelerate reconductoring projects while minimizing grid disruption and permitting complexity across mature transmission networks.

Germany Market Outlook: Germany remains the region’s most strategically significant ACCC market due to extensive renewable energy integration and industrial electricity demand concentration. Utilities are modernizing high-voltage transmission infrastructure linking offshore wind generation with manufacturing hubs in southern Germany. More than 27% of ongoing grid expansion projects involve advanced conductor technologies designed to improve transmission efficiency and lower line congestion. German engineering firms are investing in predictive grid monitoring systems and high-performance reconductoring solutions to strengthen operational reliability across interconnected European electricity networks.

Large-Scale Transmission Expansion Supporting Manufacturing Leadership

Asia-Pacific dominates the ACCC market through extensive transmission infrastructure expansion, renewable energy integration, and large-scale conductor manufacturing capacity. The region accounts for nearly 43% of global deployment activity and over 46% of composite conductor production output. China and India continue leading ultra-high-voltage transmission investments to support industrial electrification and renewable-heavy power systems. During 2026, regional utilities accelerated long-distance transmission projects exceeding 8,000 circuit kilometers linked to solar and wind integration corridors. Manufacturers are expanding localized carbon fiber processing, automated conductor assembly, and utility-specific engineering services to improve delivery timelines and operational scalability. Increasing urban electricity demand and industrial expansion continue reinforcing high-capacity transmission modernization priorities across major economies.

China Market Outlook: China maintains the strongest operational position in the global ACCC market through large-scale ultra-high-voltage deployment programs and vertically integrated conductor manufacturing capabilities. The country accounts for approximately 38% of global aluminum conductor production capacity and continues expanding renewable transmission infrastructure across western energy zones. State-backed utilities are prioritizing advanced conductors capable of reducing line losses and improving long-distance electricity transfer efficiency. Chinese manufacturers are strengthening export competitiveness through automated production systems, localized composite material sourcing, and strategic supply agreements supporting regional infrastructure projects.

Renewable Corridor Expansion Increasing Transmission Demand

South America is emerging as a developing ACCC deployment market driven by renewable energy corridor expansion and transmission reliability upgrades. The region contributes nearly 6% of global advanced conductor demand, with Brazil and Chile leading utility modernization activity linked to solar and hydropower integration. Utilities are prioritizing lightweight conductors for long-distance transmission routes spanning remote energy generation zones and industrial centers. During 2025–2026, transmission infrastructure investments increased by approximately 16% across selected renewable-heavy corridors. However, grid financing limitations and inconsistent permitting structures continue affecting project execution timelines. Companies are responding through regional engineering partnerships, phased deployment models, and utility-focused installation support programs designed to reduce operational disruption and improve grid efficiency.

Brazil Market Outlook: Brazil leads the South American ACCC market through extensive hydropower transmission requirements and expanding renewable electricity infrastructure. Utilities are upgrading transmission corridors connecting northern generation assets with southeastern industrial demand centers. Nearly 24% of planned grid modernization activity involves high-capacity conductor replacement to improve reliability and lower congestion losses. Domestic utilities are increasing collaboration with international transmission engineering firms to accelerate reconductoring efficiency and strengthen operational resilience across geographically dispersed electricity networks.

Grid Diversification and Energy Security Investments Accelerating Adoption

Middle East & Africa is becoming a fast-expanding ACCC market due to rising electricity demand, large-scale infrastructure modernization, and renewable energy diversification programs. The region contributes approximately 4% of global deployment activity but is recording accelerated utility investment momentum across Gulf countries and selected African economies. Saudi Arabia and the United Arab Emirates are prioritizing advanced conductors for high-temperature transmission environments supporting industrial zones and renewable megaprojects. During 2026, several regional utilities expanded transmission modernization budgets by nearly 21% to strengthen grid stability and cross-border electricity connectivity. Companies are increasing EPC partnerships, localized technical training, and smart-grid integration capabilities to improve deployment consistency and long-distance transmission efficiency.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s most strategically significant ACCC market through aggressive transmission expansion and renewable integration programs linked to industrial diversification initiatives. Utilities are deploying high-temperature low-sag conductors across desert transmission corridors requiring stable performance under extreme climate conditions. More than 18% of recent grid modernization contracts involved advanced composite conductor technologies supporting solar generation integration and industrial electricity demand growth. National infrastructure programs are encouraging partnerships between utilities, EPC contractors, and advanced material suppliers to strengthen localized transmission deployment capabilities.

Global leaders including CTC Global, Nexans, Prysmian Group, Apar Industries, and Lamifil compete directly against regional conductor manufacturers and low-cost transmission suppliers across utility modernization projects. The top five players collectively control nearly 52% of advanced composite conductor deployment activity through proprietary core technologies, utility relationships, and vertically integrated supply chains. Competition centers on transmission efficiency, installation speed, lifecycle durability, and localized manufacturing capacity rather than pricing alone. Advanced ACCC systems improve transmission capacity by over 35%, while automated conductor production reduced delivery timelines by approximately 18% for large-scale utility contracts. European technology innovators are competing with Asian cost-focused manufacturers through grid analytics integration, customized conductor engineering, and strategic EPC partnerships. Supply-chain control over carbon fiber materials remains a major competitive pressure point. Winning requires scalable manufacturing, certified installation ecosystems, utility-grade technical support, and the ability to execute large transmission upgrades with minimal operational disruption.

CTC Global

Prysmian Group

Nexans

Apar Industries

Lamifil

Southwire Company

LS Cable & System

Sterlite Power

General Cable

ZTT International

Midal Cables

Taihan Cable & Solution

Sumitomo Electric Industries

Fujikura Ltd.

Advanced composite core technology is reshaping transmission efficiency through carbon fiber reinforced cores, high-temperature low-sag conductors, and digitally monitored overhead systems. Compared with conventional ACSR conductors, modern ACCC systems improve ampacity by more than 35% while reducing line losses by nearly 28% under heavy-load conditions. Utilities across China, India, and the United States increased deployment of advanced reconductoring solutions by approximately 31% during 2026 to expand grid capacity without constructing additional towers. Manufacturers are integrating lightweight composite materials with automated conductor production to reduce installation complexity and improve long-span transmission performance.

Emerging technologies include AI-enabled thermal monitoring, predictive load analytics, and smart conductor sensing platforms integrated into high-voltage transmission corridors. Utilities deploying digital monitoring systems reported nearly 22% faster fault detection and approximately 18% lower maintenance intervention frequency. More than 40% of new utility modernization projects initiated during 2026 incorporated real-time transmission analytics to optimize power flow under renewable-heavy operating conditions. Companies investing in smart-grid-compatible conductors are strengthening competitive positioning through utility partnerships and digitally optimized transmission performance.

Between 2026 and 2028, disruptive developments in hybrid composite cores, recyclable conductor materials, and automated reconductoring systems will accelerate deployment scalability and operational efficiency. Advanced coating technologies are reducing thermal stress exposure by approximately 16%, while modular installation systems are shortening project timelines by nearly 20%. Global utilities prioritizing energy security, renewable integration, and transmission resilience are increasingly favoring suppliers capable of combining high-capacity conductor engineering with digital grid integration capabilities.

June 2024 – CTC Global opened its fifth ACCC® core manufacturing facility in Pune, India, supporting over 20,000 kilometers of advanced conductor deployment and strengthening localized supply-chain scalability for utility modernization projects.

February 2025 – Prysmian launched TransPowr® ACCC conductors using low-carbon and recycled materials, expanding sustainable conductor production while supporting reduced lifecycle emissions across advanced transmission infrastructure applications.

May 2025 – Prysmian and GCCIA deployed E3X overhead conductors across a 400 kV transmission project, increasing transmission capacity by up to 20% while integrating real-time monitoring technology for grid optimization. Source: Prysmian

June 2025 – Google partnered with CTC Global to accelerate advanced conductor deployment across U.S. transmission networks, targeting faster grid-capacity expansion and improved reliability through high-capacity reconductoring initiatives. Source: Silicon UK

The report provides comprehensive analysis of the global ACCC market across conductor types, applications, end-users, and regional deployment dynamics between 2026 and 2033. It evaluates strategic segments including ACCC Helsinki, ACCC Lisbon, ACCC Oslo, ACCC ULS Conductors, and High Capacity Conductors while assessing operational demand across power transmission, renewable energy integration, smart grid networks, and long-distance transmission infrastructure. The study covers utilities, renewable developers, government power agencies, industrial facilities, and transmission companies representing more than 80% of advanced conductor deployment activity.

The report delivers detailed regional intelligence across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing concentration, grid modernization activity, and infrastructure investment patterns. It examines technology trends including AI-enabled grid monitoring, composite core innovation, automated reconductoring systems, and high-temperature low-sag transmission technologies. Strategic insights support investment planning, competitive benchmarking, supply-chain positioning, partnership evaluation, and deployment prioritization for utilities, manufacturers, EPC contractors, and infrastructure developers operating within modern transmission networks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1418.7 Million |

|

Market Revenue in 2033 |

USD 2388.81 Million |

|

CAGR (2026 - 2033) |

6.73% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

CTC Global, Prysmian Group, Nexans, Apar Industries, Lamifil, Southwire Company, LS Cable & System, Sterlite Power, General Cable, ZTT International, Midal Cables, Taihan Cable & Solution, Sumitomo Electric Industries, Fujikura Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |