Reports

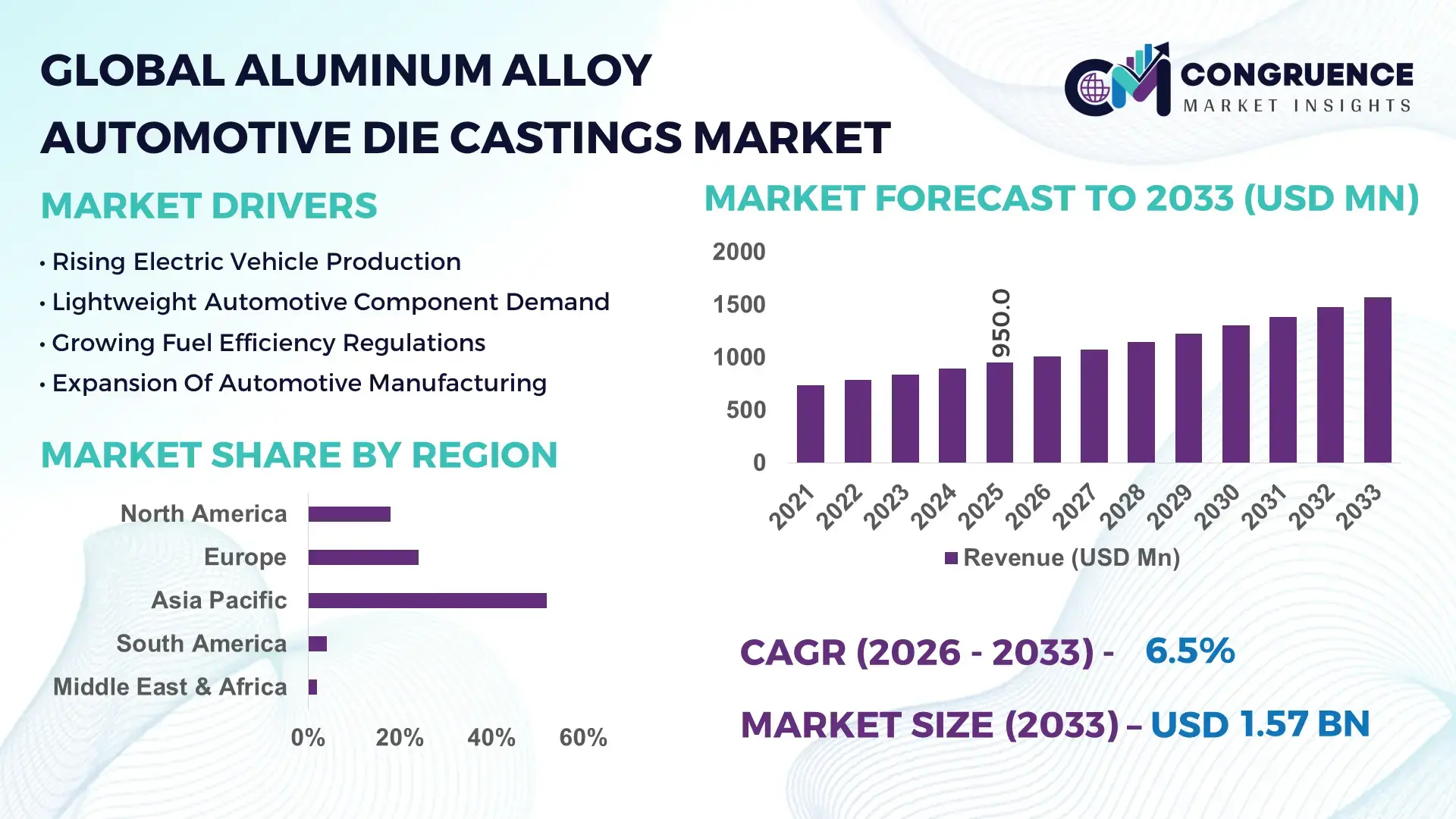

The Global Aluminum Alloy Automotive Die Castings Market was valued at USD 950.0 Million in 2025 and is anticipated to reach a value of USD 1,572.2 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. The market is accelerating due to the rapid transition toward lightweight vehicle architectures, where aluminum die-cast components reduce vehicle weight by 30%–40% compared to conventional steel structures while improving fuel efficiency and EV battery range. Automotive OEMs are aggressively integrating giga-casting and high-pressure die-casting technologies to optimize production speed, reduce part complexity, and lower assembly costs across electric and hybrid platforms. Between 2024 and 2026, global supply chains are shifting toward localized aluminum sourcing and vertically integrated casting operations as geopolitical trade tensions and energy-price volatility continue reshaping automotive manufacturing strategies. Governments across North America, Europe, and Asia-Pacific are tightening vehicle emission regulations, forcing automakers to accelerate adoption of recyclable lightweight materials with lower lifecycle emissions.

China dominates the global Aluminum Alloy Automotive Die Castings Market with approximately 38% production share, supported by over 1,200 large-scale automotive component foundries and aggressive EV manufacturing expansion. The country invested more than USD 8 billion into advanced lightweight automotive manufacturing infrastructure between 2023 and 2025, while EV penetration exceeded 35% of total passenger vehicle sales. Compared to traditional stamped steel structures, Chinese giga-casting facilities are reducing body assembly complexity by nearly 20% and shortening production cycles by 15%, giving domestic manufacturers a substantial operational advantage in cost-sensitive EV segments.

As automakers intensify platform standardization and lightweight engineering investments, companies prioritizing automated die-casting capacity, recyclable alloy innovation, and regionalized production networks are securing stronger long-term competitive positioning across the global automotive value chain.

Market Size & Growth: USD 950.0 Million in 2025 reaching USD 1,572.2 Million by 2033, driven by 35% higher EV lightweight component adoption and giga-casting integration.

Top Growth Drivers: EV production expansion (+34%), lightweighting mandates (+28%), and automated die-casting deployment (+22%) are accelerating market transformation globally.

Short-Term Forecast: By 2028, automated aluminum casting lines are expected to reduce manufacturing cycle times by 18% while improving yield efficiency by 14%.

Emerging Technologies: AI-enabled defect detection, giga-casting systems, and recycled secondary aluminum alloys are improving operational efficiency by over 20%.

Regional Leaders: Asia-Pacific holds USD 380 Million demand, Europe exceeds USD 240 Million sustainability-led adoption, while North America advances EV casting automation rapidly.

Consumer/End-User Trends: Over 42% of electric vehicle platforms now integrate large-scale aluminum structural castings for weight and performance optimization.

Pilot/Case Example: In 2025, an EV giga-casting deployment reduced component count by 70% and assembly labor requirements by 25%.

Competitive Landscape: Top manufacturers control nearly 48% market share, led by Nemak, Ryobi, Dynacast, Endurance Technologies, and GF Casting Solutions.

Regulatory & ESG Impact: Recycled aluminum adoption increased 31% as emission-compliance policies pushed OEMs toward low-carbon manufacturing ecosystems.

Investment & Funding: More than USD 5.2 billion was allocated toward casting automation, EV supply chain expansion, and regional manufacturing localization initiatives.

Innovation & Future Outlook: Integrated mega-casting platforms and digital foundry systems are redefining high-volume automotive component manufacturing efficiency globally.

Passenger vehicles account for nearly 61% of total Aluminum Alloy Automotive Die Castings demand due to rising lightweight platform integration across EV and hybrid segments. Structural body parts and transmission housings together contribute over 46% of component utilization as automakers prioritize assembly simplification and energy efficiency. Asia-Pacific remains the dominant production hub with 52% manufacturing concentration, while Europe is accelerating recycled aluminum adoption following stricter carbon-border regulations. Increasing deployment of giga-casting technology and AI-driven quality inspection systems is reshaping production economics, positioning advanced lightweight manufacturing as a core strategic priority for global automotive suppliers.

The Aluminum Alloy Automotive Die Castings Market is rapidly becoming a strategic battleground for automotive manufacturers seeking cost-efficient lightweight engineering, EV scalability, and production optimization. Automakers are aggressively shifting toward integrated casting architectures as vehicle electrification intensifies pressure on weight reduction, energy efficiency, and manufacturing simplification. Advanced die-casting technologies are transforming production economics by consolidating dozens of individual welded components into single structural castings, dramatically improving assembly speed and operational efficiency across next-generation vehicle platforms.

The market is also experiencing mounting pressure from supply chain restructuring, rising carbon-compliance obligations, and geopolitical realignment of automotive manufacturing networks. OEMs are increasingly localizing aluminum sourcing and casting operations to reduce logistics exposure and stabilize production continuity. High-pressure giga-casting systems now improve production efficiency by nearly 22% while reducing manufacturing costs by approximately 18% compared to traditional multi-part assembly systems. This shift is accelerating competitive differentiation among automotive suppliers and reshaping global capital allocation priorities.

Asia-Pacific leads global production volume with nearly 52% manufacturing concentration, while Europe leads sustainability-driven adoption with over 37% recycled aluminum integration across automotive casting operations. North American manufacturers are rapidly expanding automated casting infrastructure as EV assembly capacity continues scaling aggressively. Over the next two to three years, automated die-casting deployment is projected to reduce defect rates by 16% and shorten vehicle body assembly times by nearly 20%, significantly improving operational throughput.

ESG positioning is emerging as a direct competitive advantage, with low-carbon recycled aluminum reducing energy consumption by nearly 60% compared to primary aluminum production. In 2025, a major EV manufacturer achieved a 25% reduction in body assembly labor after implementing giga-cast rear underbody systems across its premium vehicle platform. Simultaneously, automotive suppliers are accelerating investments into smart foundries, AI-enabled defect monitoring, and closed-loop aluminum recycling ecosystems to strengthen long-term resilience and regulatory alignment. Companies that aggressively optimize lightweight casting innovation, regional manufacturing scalability, and sustainable alloy integration are securing stronger bargaining power, higher OEM alignment, and superior future positioning within the rapidly transforming global automotive manufacturing ecosystem.

The Aluminum Alloy Automotive Die Castings Market is being reshaped by the accelerating convergence of vehicle electrification, lightweight engineering, and manufacturing automation. Automotive OEMs are increasingly replacing traditional steel-intensive structures with aluminum alloy die-cast components to improve energy efficiency, reduce emissions, and optimize vehicle performance. Demand concentration is strongest in EV platforms, structural body components, transmission systems, and battery housing applications where weight reduction directly impacts operational efficiency and driving range. Simultaneously, manufacturers are adopting high-pressure and giga-casting technologies to simplify assembly operations and reduce component complexity. Global automotive supply chains are also undergoing structural transformation as companies localize production networks and secure stable aluminum sourcing amid geopolitical trade uncertainty and energy cost volatility. Europe is prioritizing recycled aluminum integration under tightening carbon regulations, while Asia-Pacific continues scaling high-volume production capabilities through automated casting infrastructure. North American manufacturers are focusing heavily on AI-enabled quality control and digital foundry operations to improve manufacturing precision and throughput. These shifting dynamics are forcing companies to balance production scalability, cost optimization, sustainability compliance, and technological differentiation simultaneously, redefining long-term competitive positioning across the global automotive manufacturing landscape.

The rapid transition toward lightweight vehicle architectures is forcing automakers to accelerate adoption of aluminum alloy die-cast components across EV and fuel-efficient vehicle platforms. Aluminum die-cast structures reduce component weight by nearly 35% compared to steel alternatives while improving battery efficiency and vehicle range performance. EV manufacturers are increasingly integrating giga-casting systems capable of consolidating over 70 individual body parts into single structural castings, reducing assembly complexity and improving production speed by approximately 20%. The global push toward stricter emission compliance and fuel-efficiency standards is intensifying this shift. Europe’s carbon reduction mandates and North America’s EV manufacturing incentives are accelerating investments into advanced lightweight manufacturing ecosystems. Automotive suppliers are responding through capacity expansion, automated die-casting deployment, and strategic partnerships with EV manufacturers. Several large-scale foundries across China and Mexico expanded production capabilities by over 25% between 2024 and 2025 to secure long-term OEM supply agreements. This structural transition is redefining automotive manufacturing economics and strengthening demand for high-performance aluminum casting technologies globally.

The Aluminum Alloy Automotive Die Castings Market faces significant operational pressure from fluctuating aluminum prices, energy-intensive production processes, and concentrated raw material supply networks. Primary aluminum production consumes substantial electricity, and energy costs in Europe increased by nearly 18% during recent industrial disruptions, directly impacting casting profitability and production stability. Additionally, over 55% of global aluminum refining capacity remains concentrated in Asia, increasing supply chain exposure for Western automotive manufacturers. These constraints are creating production delays, margin compression, and long-term procurement uncertainty for die-casting suppliers. Rising environmental compliance costs are further increasing operational complexity, particularly for smaller manufacturers lacking advanced recycling infrastructure. Companies are actively mitigating these risks through diversified sourcing agreements, secondary aluminum adoption, and long-term energy contracts. Recycled aluminum usage increased by approximately 31% across automotive casting operations between 2023 and 2025 as manufacturers pursued cost stabilization and lower-carbon production models. Simultaneously, several automotive suppliers are investing in regionalized smelting and closed-loop recycling systems to reduce dependency on volatile global supply networks and improve operational resilience.

The expansion of giga-casting technology and AI-driven smart foundry systems is opening substantial strategic opportunities across the Aluminum Alloy Automotive Die Castings Market. Advanced giga-casting platforms reduce component count by nearly 70%, lower assembly labor requirements by over 25%, and significantly improve production throughput for high-volume EV manufacturing. These operational advantages are accelerating OEM demand for integrated structural castings and large-scale lightweight components. Automotive manufacturers are also increasing investment into predictive maintenance systems, digital twin manufacturing, and automated quality inspection technologies that improve casting precision and reduce defect rates by nearly 16%. Emerging EV markets across Southeast Asia and Eastern Europe are becoming attractive expansion zones as localized manufacturing incentives and battery production investments continue accelerating. Companies are positioning aggressively through R&D partnerships, regional plant expansion, and recyclable alloy innovation programs to secure future dominance. A growing non-obvious opportunity is the integration of secondary recycled aluminum into premium automotive platforms, enabling both cost optimization and ESG differentiation simultaneously. This dual-value proposition is rapidly reshaping supplier selection criteria across global automotive production networks.

Despite accelerating demand, the Aluminum Alloy Automotive Die Castings Market continues facing execution-level challenges linked to production scalability, process precision, and infrastructure readiness. High-pressure die-casting systems require substantial capital investment, advanced tooling accuracy, and stable energy infrastructure, creating operational barriers for mid-sized manufacturers. Large-scale giga-casting deployment can increase initial equipment costs by over 40% compared to traditional casting systems, limiting rapid industry-wide adoption. Manufacturing consistency also remains a critical challenge as structural automotive castings require extremely low defect tolerance and precise thermal control. Even minor porosity defects can compromise crash-performance reliability and increase rejection rates by nearly 12%. Global labor shortages in advanced foundry engineering and automation management are further constraining production expansion. Simultaneously, tightening sustainability regulations are forcing manufacturers to upgrade filtration systems, emission controls, and recycling infrastructure, increasing operational expenditure significantly. To remain competitive, companies must accelerate investments into AI-enabled defect monitoring, workforce automation, and advanced alloy engineering while strengthening strategic partnerships with OEMs and regional supply chain operators to stabilize long-term production scalability and quality performance.

38% Increase in Giga-Casting Deployment Reshaping Vehicle Assembly Operations: Automotive OEMs are aggressively integrating giga-casting systems capable of consolidating over 70 components into single aluminum structures. Production cycle times declined by nearly 18%, while assembly labor requirements dropped by 25% across EV-focused manufacturing lines. Suppliers are restructuring plant layouts and expanding high-pressure casting capacity to support large-format structural component demand.

31% Rise in Recycled Aluminum Integration Redefining Sustainable Manufacturing: Automakers are accelerating secondary aluminum adoption as carbon-border regulations and energy-cost pressures intensify globally. Recycled aluminum usage improved energy efficiency by nearly 60% compared to primary production while reducing raw material volatility exposure. Foundries are forming closed-loop recycling partnerships and expanding low-carbon alloy portfolios to secure long-term OEM contracts and compliance-driven demand.

24% Expansion in AI-Based Foundry Automation Optimizing Production Precision: Manufacturers are deploying AI-enabled defect detection and predictive maintenance systems to reduce scrap generation and stabilize output consistency. Automated inspection platforms improved defect identification accuracy by 20% while reducing unplanned downtime by 14%. Companies are prioritizing smart foundry investments as labor shortages and production complexity continue forcing operational transformation.

29% Shift Toward Regionalized Automotive Casting Supply Chains Accelerating Localization: Geopolitical trade pressures and logistics instability are driving automotive suppliers to establish localized aluminum casting ecosystems across North America and Southeast Asia. Regional manufacturing expansion reduced component delivery lead times by approximately 17% and improved supply reliability for EV assembly plants. Companies are aggressively pursuing joint ventures and localized sourcing strategies to secure faster response capabilities and production continuity.

The Aluminum Alloy Automotive Die Castings Market is segmented by type, application, and end-user categories, reflecting shifting automotive manufacturing priorities toward lightweight engineering, structural efficiency, and production scalability. Demand remains highly concentrated in high-pressure die-casting technologies and EV-focused structural applications due to their superior integration efficiency and cost optimization capabilities. Approximately 58% of total demand is linked to structural automotive components and transmission systems, where lightweight materials directly improve vehicle performance and energy efficiency. Market momentum is rapidly shifting toward automated casting technologies and integrated EV platform applications as automakers prioritize simplified assembly architectures and higher-volume manufacturing precision. Passenger vehicle manufacturers continue dominating end-user demand, while commercial EV adoption is accelerating specialized casting requirements for battery housings and chassis systems. Companies are responding through giga-casting investments, recyclable alloy innovation, and regionalized production expansion to strengthen supply continuity and manufacturing competitiveness. This segmentation evolution is redefining where production capacity, technological investment, and supplier partnerships are being strategically concentrated across the global automotive ecosystem.

High-pressure die casting dominates the Aluminum Alloy Automotive Die Castings Market with approximately 46% share due to its superior production speed, dimensional accuracy, and scalability for high-volume automotive manufacturing. Automakers increasingly prefer high-pressure systems for structural body components and transmission housings because they reduce assembly complexity and improve manufacturing consistency. Low-pressure die casting remains strategically relevant for precision-oriented components requiring enhanced mechanical strength and surface finish, particularly in premium vehicle platforms. Vacuum die casting is emerging as the fastest-growing segment with adoption growth exceeding 21% as manufacturers pursue defect reduction and improved structural integrity for EV battery enclosures and crash-sensitive components. Compared to traditional high-pressure systems, vacuum-assisted casting significantly reduces porosity levels and improves thermal performance, making it increasingly critical for advanced electric vehicle architectures. Gravity die casting and squeeze casting collectively account for nearly 29% share, serving specialized automotive applications where durability, heat resistance, and smaller production runs remain essential. Companies are rapidly expanding automated high-pressure and vacuum-casting capacity while investing in AI-enabled process monitoring to optimize throughput and reduce rejection rates. The market is clearly shifting toward scalable, precision-driven casting technologies capable of supporting next-generation lightweight automotive platforms.

Engine components continue leading the Aluminum Alloy Automotive Die Castings Market with approximately 34% share due to their critical role in thermal management, fuel efficiency, and lightweight powertrain optimization. Automotive manufacturers heavily rely on aluminum die-cast engine blocks, cylinder heads, and transmission casings to improve operational efficiency and reduce overall vehicle mass. Structural body applications are emerging as the fastest-growing segment with adoption growth exceeding 24%, primarily driven by EV platform expansion and giga-casting integration. Compared to conventional drivetrain-focused applications, structural castings are gaining momentum because they simplify assembly architecture and significantly reduce component count. Battery housing and chassis applications are also accelerating rapidly as EV manufacturers prioritize crash protection, heat dissipation, and platform standardization. Remaining applications, including steering systems and suspension components, collectively account for nearly 27% of market demand and maintain strategic importance in high-performance and commercial vehicle categories. Companies are aggressively repositioning product portfolios toward large structural castings and integrated EV components while expanding smart manufacturing capabilities to support faster deployment cycles and production scalability. Demand concentration is increasingly shifting toward multifunctional lightweight applications that optimize both vehicle efficiency and assembly economics simultaneously.

Passenger vehicle manufacturers dominate the Aluminum Alloy Automotive Die Castings Market with nearly 68% share due to high production volumes, aggressive lightweighting initiatives, and rapid EV platform expansion. This segment relies heavily on aluminum die-cast components to improve fuel efficiency, extend battery range, and optimize vehicle performance while reducing manufacturing complexity. Commercial vehicle manufacturers are emerging as the fastest-growing end-user category with adoption growth exceeding 18% as fleet operators increasingly prioritize fuel savings, durability, and emission reduction compliance. Compared to traditional passenger vehicle demand, commercial vehicle applications require larger structural castings and higher thermal resistance components, particularly in electric buses and logistics fleets. Luxury and performance vehicle manufacturers, along with specialty mobility platforms, collectively account for approximately 19% of market demand and continue driving innovation in precision casting technologies and advanced alloy integration. Automotive suppliers are strategically targeting these segments through customized lightweight solutions, long-term OEM partnerships, and region-specific manufacturing expansion. Buying behavior is increasingly shifting toward integrated casting platforms capable of reducing assembly costs and improving production scalability, creating stronger demand for technologically advanced, high-volume casting ecosystems.

Asia-Pacific accounted for the largest market share at 52% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Asia-Pacific dominates global production through large-scale automotive manufacturing ecosystems, low-cost casting infrastructure, and rapid EV assembly expansion led by China, Japan, and India. Europe contributes approximately 24% share and leads sustainability-driven adoption through aggressive recycled aluminum integration and carbon-emission compliance policies. North America holds nearly 18% share while accelerating automation investments and giga-casting deployment across EV production facilities. South America and Middle East & Africa collectively account for 6% share, supported by localized industrial expansion and infrastructure investments. Global manufacturers are increasingly prioritizing Asia-Pacific for scale, Europe for sustainable innovation, and North America for advanced manufacturing transformation and regional supply-chain resilience.

North America represents nearly 18% of the global Aluminum Alloy Automotive Die Castings Market, driven by rapid EV manufacturing expansion and aggressive lightweight vehicle engineering investments. The United States and Mexico are strengthening regional casting ecosystems as automakers localize supply chains and reduce import dependency amid trade and logistics pressures. Automated giga-casting adoption increased by approximately 27% between 2024 and 2025, significantly improving assembly efficiency across EV platforms. Automotive suppliers are expanding smart foundry infrastructure and AI-enabled inspection systems to reduce defect rates and improve throughput consistency. Consumer preference is shifting toward high-performance electric SUVs and pickup vehicles requiring larger structural aluminum castings. Multiple manufacturers expanded North American casting capacity by over 20% to secure long-term OEM supply agreements, reinforcing the region’s strategic importance for advanced automotive manufacturing scalability.

Europe accounts for approximately 24% of the global Aluminum Alloy Automotive Die Castings Market, led by Germany, France, and Italy through advanced automotive engineering and strict carbon-emission compliance frameworks. The region is rapidly accelerating recycled aluminum integration, with secondary aluminum adoption surpassing 37% across automotive casting operations. EU carbon-border regulations and sustainability mandates are forcing manufacturers to optimize low-emission production ecosystems and improve material traceability. Companies are investing heavily in closed-loop recycling systems and energy-efficient casting technologies to reduce industrial emissions and stabilize energy consumption. Automotive OEMs increasingly prioritize lightweight structural components that support EV efficiency targets and lifecycle sustainability requirements. Several European suppliers improved operational energy efficiency by nearly 15% through smart foundry modernization, making the region a global benchmark for sustainable automotive manufacturing innovation and regulatory-driven transformation.

Asia-Pacific dominates the Aluminum Alloy Automotive Die Castings Market with approximately 52% global share, supported by massive automotive production capacity across China, Japan, South Korea, and India. China alone contributes nearly 38% of global automotive aluminum casting output due to its expansive EV manufacturing ecosystem and integrated raw material supply chain advantages. Manufacturers across the region are aggressively deploying automated high-pressure casting systems and localized giga-casting facilities to improve production speed and reduce component complexity. Export-oriented suppliers increased advanced casting capacity by approximately 30% between 2023 and 2025 to support growing global EV demand. Automotive enterprises prioritize cost-efficient, scalable manufacturing models with faster deployment cycles and localized sourcing flexibility. The region remains strategically critical for global manufacturers seeking large-scale production efficiency, rapid market expansion, and competitive supply-chain optimization.

South America contributes nearly 4% of the global Aluminum Alloy Automotive Die Castings Market, with Brazil and Argentina leading regional automotive manufacturing activities. Demand is increasing steadily due to localized vehicle assembly expansion and growing adoption of lightweight automotive components across commercial transportation sectors. However, infrastructure limitations, currency volatility, and high import dependency continue constraining advanced casting scalability across several regional markets. Automotive suppliers are responding by expanding localized production partnerships and increasing regional component sourcing to reduce logistics exposure and manufacturing costs. Adoption of automated die-casting technologies improved by approximately 14% between 2024 and 2025, particularly within commercial vehicle manufacturing operations. Enterprise buyers remain highly price-sensitive and prioritize durable, cost-efficient casting solutions, positioning the region as both a long-term growth opportunity and an operational risk environment requiring disciplined investment strategies.

The Middle East & Africa region accounts for approximately 2% of the global Aluminum Alloy Automotive Die Castings Market, supported by expanding industrial diversification programs and infrastructure modernization initiatives across the UAE, Saudi Arabia, and South Africa. Automotive component demand is increasingly linked to commercial transportation, construction mobility, and industrial vehicle applications requiring lightweight and corrosion-resistant materials. Governments are accelerating manufacturing investments and industrial partnerships to strengthen domestic production capabilities and reduce import reliance. Automated casting deployment increased by nearly 11% between 2024 and 2025 as regional manufacturers modernized production operations and upgraded process efficiency. Enterprise buyers prioritize durable components with lower maintenance requirements and stable long-term supply availability. The region is emerging as a strategic investment destination for manufacturers seeking industrial expansion opportunities aligned with infrastructure growth and regional manufacturing transformation agendas.

China – 38% Market share: Dominates through massive EV production capacity, integrated aluminum supply chains, and large-scale giga-casting infrastructure expansion.

United States – 16% Market share: Leads advanced automotive casting innovation through aggressive EV manufacturing investments, automated foundry deployment, and localized supply-chain restructuring.

The Aluminum Alloy Automotive Die Castings Market is defined by intense competition between global lightweighting specialists, vertically integrated casting manufacturers, EV-focused innovators, and regional cost-efficient suppliers. Companies such as Nemak, Ryobi Die Casting, GF Casting Solutions, Dynacast, Endurance Technologies, and Ahresty are competing aggressively for OEM contracts linked to EV structural platforms and giga-casting deployment. The top five players collectively control nearly 48% of global market activity, with competition increasingly shifting from conventional engine components toward integrated structural aluminum systems.

Competition is centered on production speed, casting precision, supply-chain control, and automated manufacturing scalability. Advanced giga-casting systems reduce assembly complexity by nearly 20%, while AI-enabled defect monitoring improves yield efficiency by approximately 15%. Leading suppliers are expanding high-pressure casting capacity, pursuing regional manufacturing localization, and integrating recycling infrastructure to stabilize raw material access and improve ESG positioning. Nemak’s acquisition of GF Casting Solutions accelerated competitive consolidation and strengthened technological depth in large structural castings.

The market is rapidly shifting toward technology-led differentiation, where automation, localized supply ecosystems, and EV-specific casting expertise determine competitive positioning. High capital intensity, tooling complexity, and OEM qualification standards remain major entry barriers. Winning against established players now requires scalable smart foundries, vertically integrated operations, and faster deployment capabilities aligned with next-generation automotive manufacturing transformation.

Ryobi Die Casting

Dynacast

Endurance Technologies Limited

Ahresty Corporation

Rheinmetall Automotive AG

Gibbs Die Casting Corporation

Martinrea International Inc.

Georg Fischer Ltd.

Sandhar Technologies Limited

Handtmann Group

Rockman Industries Ltd.

Pace Industries

The Aluminum Alloy Automotive Die Castings Market is undergoing rapid technological transformation as automakers prioritize lightweight structural integration, automated manufacturing, and EV production scalability. High-pressure die casting (HPDC) remains the dominant production technology, accounting for nearly 46% deployment across automotive component manufacturing due to its speed, dimensional accuracy, and high-volume efficiency. However, giga-casting systems are rapidly reshaping the industry by consolidating over 70 individual vehicle components into single structural castings, reducing assembly complexity by approximately 20% and improving manufacturing throughput significantly.

Vacuum-assisted die casting and AI-enabled smart foundries are emerging as critical competitive technologies. Vacuum die casting reduces porosity defects by nearly 18% compared to conventional casting systems, making it increasingly essential for EV battery housings and crash-sensitive structural applications. Simultaneously, AI-powered inspection systems and predictive maintenance platforms are improving defect detection accuracy by approximately 20% while reducing production downtime by nearly 14%. Suppliers investing in these systems are gaining stronger OEM alignment through improved consistency and lower rejection rates.

Traditional multi-part welded assemblies are increasingly being replaced by integrated aluminum structural castings that improve production efficiency by over 22% while lowering manufacturing costs by approximately 18%. Companies with advanced giga-casting infrastructure, digital process control, and recyclable alloy capabilities are strengthening long-term competitive positioning within EV manufacturing ecosystems.

Between 2026 and 2028, deployment of automated mega-casting systems and closed-loop aluminum recycling technologies is expected to accelerate further as OEMs prioritize low-carbon manufacturing, localized supply chains, and higher-volume EV platform standardization. Early technology adopters are positioned to secure faster production cycles, lower operational costs, and stronger global supply-chain leverage.

May 2024 – Ryobi Die Casting announced a USD 50 million expansion of its Mexico aluminum die-casting facility, adding 91,500 square feet and five large high-pressure die-casting machines to support EV demand growth. The expansion also created 124 new jobs, strengthening North American production localization and EV supply-chain responsiveness. [Capacity Scale-Up] Source: www.foundrymag.com

July 2025 – Nemak signed a definitive agreement to acquire GF Casting Solutions’ automotive business, expanding its lightweight structural casting portfolio and strengthening expertise in aluminum and magnesium vehicle components. The acquisition significantly expanded Nemak’s high-pressure casting footprint and advanced sustainable mobility capabilities across global automotive markets. [Strategic Consolidation]

February 2026 – Nemak completed the acquisition of GF Casting Solutions’ automotive operations after regulatory approvals, strengthening global production capabilities and expanding advanced structural component manufacturing. The deal added nine strategically located production sites and HPDC equipment with up to 6,100-ton clamping force, accelerating large-component EV manufacturing scalability. [Global Footprint Expansion]

May 2024 – YIZUMI delivered its LEAP9000 ultra-large die-casting machine designed for new-energy vehicle production, enabling manufacturing of integrated rear aluminum vehicle structures. The advanced platform supports higher energy efficiency and large-format casting integration, reinforcing rapid industrial transition toward giga-casting-based EV assembly systems. [Mega-Casting Deployment]

The Aluminum Alloy Automotive Die Castings Market Report provides comprehensive coverage of the global industry across major casting technologies, automotive applications, end-user categories, and regional manufacturing ecosystems. The report analyzes high-pressure, low-pressure, vacuum, gravity, and squeeze die-casting technologies while evaluating their operational relevance across structural body components, engine systems, transmission housings, battery enclosures, and chassis applications. Passenger vehicles account for nearly 68% of analyzed end-user demand, while structural EV applications represent one of the fastest-shifting manufacturing segments within the report scope.

The study delivers strategic analysis across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering regional production concentration, supply-chain restructuring, sustainability adoption, and manufacturing localization trends. More than 12 major industry participants are profiled with detailed competitive benchmarking focused on technology deployment, production scalability, recycling integration, and giga-casting expansion strategies. The report also evaluates emerging technologies including AI-enabled smart foundries, automated defect monitoring, and integrated mega-casting systems, which are improving manufacturing efficiency by over 20% across advanced automotive facilities.

Additionally, the report provides forward-looking assessment for 2026–2033 covering evolving EV production ecosystems, recycled aluminum adoption exceeding 31% in key regions, and increasing deployment of localized automated casting infrastructure. The analysis supports investment planning, production expansion, supplier selection, competitive positioning, and long-term strategic decision-making for automotive manufacturers, component suppliers, investors, and industrial technology providers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 950.0 Million |

| Market Revenue (2033) | USD 1,572.2 Million |

| CAGR (2026–2033) | 6.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Nemak; Ryobi Die Casting; GF Casting Solutions; Dynacast; Endurance Technologies Limited; Ahresty Corporation; Rheinmetall Automotive AG; Gibbs Die Casting Corporation; Martinrea International Inc.; Georg Fischer Ltd.; Sandhar Technologies Limited; Handtmann Group; Rockman Industries Ltd.; Pace Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |