Reports

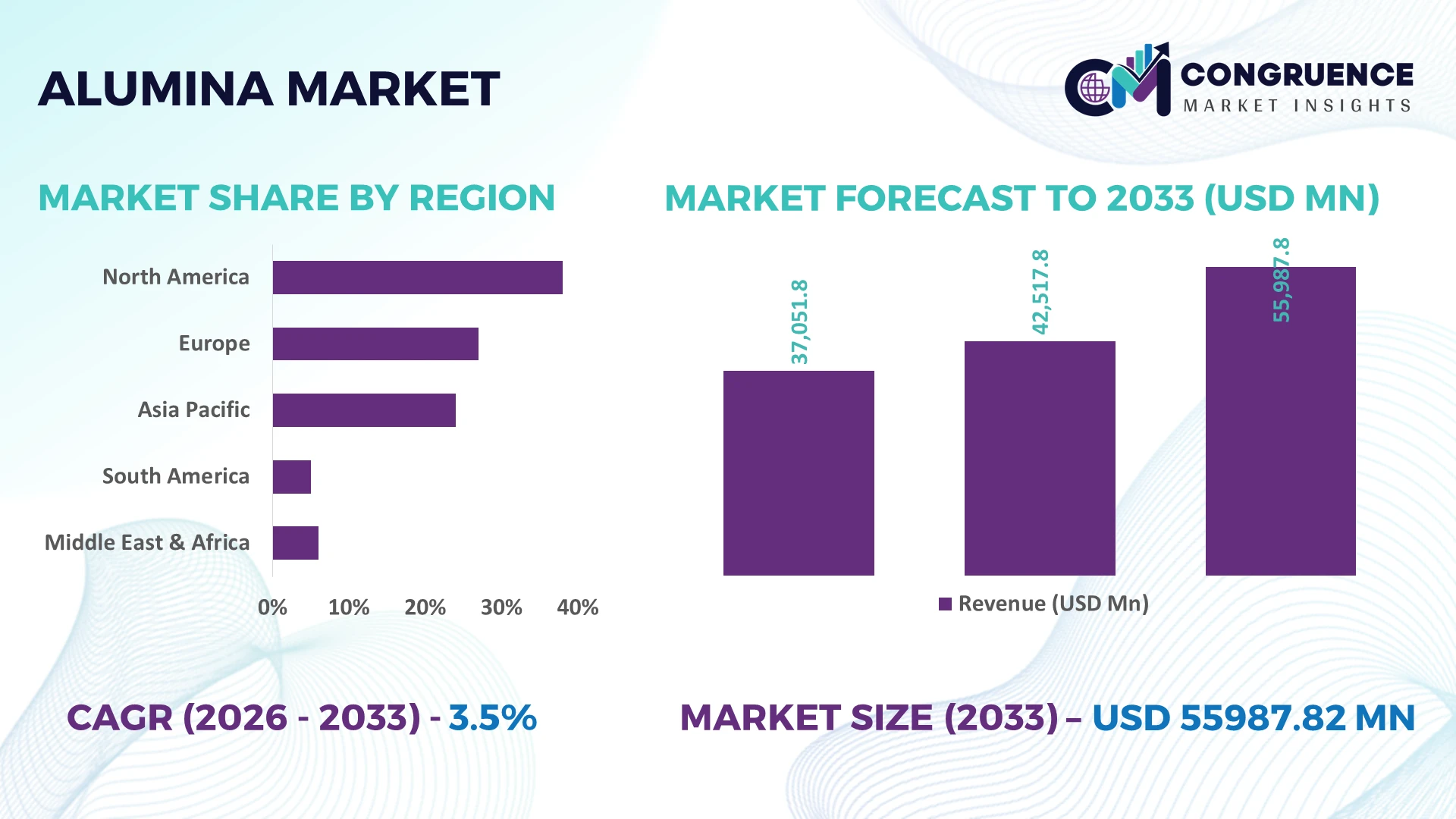

The Global Alumina Market was valued at USD 42517.8 Million in 2025 and is anticipated to reach a value of USD 55987.82 Million by 2033 expanding at a CAGR of 3.5% between 2026 and 2033.

Growth is supported by expanding low-carbon aluminum production, refinery modernization, rising electric vehicle material demand, and energy-efficient alumina refining technologies improving operational productivity.

China remains the dominant alumina producer, accounting for approximately 58% of global refining capacity, supported by integrated aluminum manufacturing, continuous refinery upgrades, and digital process control adoption exceeding 45% across major facilities. Australia, with nearly 18% of global capacity, maintains a stronger export-oriented supply model backed by abundant bauxite reserves. Ongoing global supply-chain diversification following Red Sea shipping disruptions has accelerated regional sourcing strategies and investment in resilient refining infrastructure.

Strategically, producers prioritizing energy-efficient refining, diversified raw material sourcing, and geographically balanced capacity expansion will strengthen long-term competitive positioning.

Market Size & Growth: USD 42,517.8 million (2025) to USD 55,987.82 million (2033) at 3.5% CAGR, supported by refinery modernization and advanced aluminum manufacturing expansion.

Top Growth Drivers: EV materials demand (+18%), low-carbon aluminum production (+22%), refinery automation adoption (+30%).

Short-Term Forecast: By 2028, refining energy consumption declines by nearly 8% through process optimization and digital monitoring.

Emerging Technologies: AI-based process control, predictive maintenance, and advanced calcination systems improve plant efficiency by up to 12%.

Regional Leaders: Asia-Pacific exceeds USD 31 billion, Europe approaches USD 8 billion, North America surpasses USD 6 billion, driven by cleaner refining investments.

Consumer/End-User Trends: More than 55% of alumina consumption supports transportation, construction, and electrical manufacturing applications.

Pilot/Case Example: 2025 refinery digitalization projects improved production consistency by approximately 10% while reducing maintenance interruptions.

Competitive Landscape: Top producers hold nearly 48% market share, led by Rio Tinto, Alcoa, Chalco, Rusal, and South32.

Regulatory & ESG Impact: Low-emission refining initiatives reduce carbon intensity by around 15% under tightening industrial sustainability standards.

Investment & Funding: Over USD 6 billion supports refinery upgrades, capacity expansion, and strategic regional supply-chain diversification.

Innovation & Future Outlook: Next-generation refining technologies, residue valorization, and digital operations accelerate resilient global production strategies.

The Alumina Market continues to benefit from rising demand across electric mobility, aerospace, packaging, and advanced industrial manufacturing. Digital refinery platforms, energy-efficient calcination technologies, and residue recycling innovations improve operational performance, with automated process adoption surpassing 40% in leading facilities. Increasing emphasis on localized supply chains and environmental compliance is reshaping investment priorities, setting the foundation for the following strategic market assessment.

Alumina has become a strategically important industrial material as governments and manufacturers strengthen critical mineral supply chains, modernize aluminum production, and reduce refining emissions. Infrastructure expansion, electric vehicle manufacturing, and aerospace investments are increasing the importance of secure alumina availability, while refinery digitalization and supply-chain restructuring following recent maritime logistics disruptions are reshaping procurement strategies. Producers are increasingly prioritizing vertically integrated operations to improve feedstock security and operational resilience.

Modern digital refinery control systems deliver approximately 10–15% higher energy efficiency than conventional process management while reducing unplanned downtime by nearly 20% through predictive maintenance and real-time optimization. China continues to lead in refining scale and automation deployment, whereas Australia emphasizes export-oriented, low-risk production supported by resource availability and process optimization. Over the next two to three years, digital monitoring adoption across large refining facilities is expected to exceed 55%, with automated quality management becoming a standard operational capability.

Major producers are expanding refinery upgrades, investing in residue utilization technologies, and forming long-term bauxite supply partnerships to stabilize production and improve sustainability performance. For example, advanced sensor-based process optimization has enabled several integrated refineries to improve production consistency while lowering energy consumption per ton. Companies that combine operational efficiency, diversified sourcing, and technology-led refining capabilities will secure stronger competitive positioning as industrial supply chains continue to evolve.

The transition toward lower-carbon aluminum production is driving large-scale investment in efficient alumina refining technologies and integrated production assets. More than 40% of newly upgraded refining capacity incorporates advanced process automation, while energy-efficient calcination technologies reduce fuel consumption by approximately 12%. China continues to modernize large refining complexes to improve productivity and environmental compliance, while India is expanding integrated alumina projects to support domestic aluminum manufacturing. This structural shift improves operational reliability, lowers production costs, and strengthens supply security. In response, producers are expanding refinery capacity, investing in digital process control, and forming strategic mining partnerships to secure long-term bauxite availability. Companies combining efficient refining with integrated resource management are strengthening cost competitiveness across industrial value chains.

High electricity consumption and dependence on stable bauxite supplies remain significant structural constraints for alumina producers. Energy expenses account for nearly 30% of refinery operating costs, while freight cost fluctuations exceeding 20% during supply disruptions directly affect export competitiveness. Australia and Guinea remain essential raw material suppliers, increasing exposure to logistics interruptions and geopolitical uncertainty. These pressures reduce production flexibility, compress operating margins, and delay investment decisions for independent refiners. Companies are mitigating risks by securing long-term mining contracts, diversifying procurement across multiple countries, and increasing localized inventory buffers. Strategic vertical integration has become an increasingly effective approach to protecting operational continuity under volatile market conditions.

Digital operations and circular resource utilization are creating new competitive opportunities across the alumina value chain. AI-enabled process optimization improves production efficiency by approximately 10%, while residue recovery technologies reduce industrial waste volumes by nearly 18%. Australia and India are expanding investments in residue valorization projects that convert refinery by-products into construction materials and industrial minerals. Companies are strengthening research partnerships to commercialize advanced refining technologies while deploying real-time operational analytics across production facilities. Another emerging opportunity lies in renewable-powered refining, where integrated clean-energy solutions reduce operating costs and strengthen compliance with tightening industrial sustainability standards, creating durable competitive advantages beyond conventional capacity expansion.

Executing large-scale refinery modernization while maintaining uninterrupted production remains a major operational challenge. Digital control integration can require capital upgrades affecting over 25% of existing process infrastructure, while skilled automation specialists remain in limited supply across several industrial markets. India and Indonesia continue expanding refining assets, yet workforce capability and technology integration pace differ significantly between facilities. Inconsistent digital maturity reduces productivity gains and complicates enterprise-wide operational standardization. Companies must strengthen workforce training, invest in interoperable industrial control systems, and collaborate with technology partners to accelerate deployment. Organizations capable of scaling modernization without disrupting production will achieve stronger operational resilience and long-term manufacturing competitiveness.

Digital Refinery Intelligence Expands: Integrated AI-based refinery control and predictive maintenance platforms are being deployed across large alumina facilities, improving process stability by nearly 12% and reducing unplanned shutdowns by around 18%. Chinese producers are accelerating smart refinery upgrades as labor optimization and stricter environmental monitoring reshape operations. Companies are standardizing digital workflows, expanding industrial analytics partnerships, and integrating real-time quality control to improve throughput while lowering energy intensity.

Supply Chains Become Regionalized: Refiners are restructuring procurement strategies after shipping disruptions and geopolitical trade adjustments exposed raw material vulnerabilities. Long-term bauxite sourcing agreements have increased by approximately 25%, while localized inventory planning has shortened procurement response times by nearly 15%. Australian and Indian producers are strengthening integrated logistics networks and expanding storage capacity, allowing manufacturers to reduce operational interruptions and improve supply reliability across downstream aluminum production.

Low-Carbon Refining Gains Priority: Energy-efficient calcination systems and renewable power integration are becoming standard investment priorities as industrial decarbonization policies tighten. Advanced refining technologies lower fuel consumption by nearly 10%, while carbon intensity falls by approximately 14% compared with conventional operations. Companies are restructuring capital expenditure toward cleaner process equipment, forming renewable energy partnerships, and optimizing residue management to strengthen compliance without compromising production consistency.

Residue Utilization Creates Value: Alumina producers are increasingly converting bauxite residue into construction materials, cement additives, and industrial minerals, reducing disposal volumes by almost 20% while improving resource utilization by nearly 15%. Environmental regulations and rising landfill costs are accelerating commercial deployment. A less obvious shift is that residue commercialization is evolving into a secondary profit stream, encouraging enterprises to establish technology partnerships and dedicated circular processing facilities.

Smelter Grade alumina remains the dominant product category because of its essential role in primary aluminum manufacturing, accounting for nearly 85% of total alumina consumption. Its standardized specifications, large-scale refining compatibility, and cost-efficient production support continuous deployment across integrated aluminum smelters. Calcined alumina maintains strong demand in ceramics and refractory manufacturing, while Tabular and Fused alumina serve specialized high-temperature industrial applications requiring superior hardness and thermal stability. Producers continue expanding Smelter Grade output through refinery modernization and long-term supply agreements with aluminum manufacturers.

Reactive alumina represents the fastest-growing segment as advanced ceramics, precision polishing, and catalyst applications expand across electronics and specialty manufacturing. Adoption has increased by approximately 11% in high-performance industrial applications, while demand for engineered alumina products continues to strengthen. Companies are investing in specialty-grade processing, product customization, and application-specific research to diversify portfolios beyond commodity production. This shift is redirecting investment toward higher-margin engineered alumina while preserving scale advantages in conventional refining.

Aluminum Production remains the leading application, representing approximately 88% of global alumina consumption due to its indispensable role in primary aluminum refining. Continuous investment in transportation, renewable energy infrastructure, and lightweight manufacturing sustains large-scale demand. Refractories maintain stable consumption across steel and cement operations, while Ceramics and Abrasives continue benefiting from precision manufacturing requirements. Chemical applications are expanding steadily through catalyst production and specialty industrial processing. Producers are strengthening long-term contracts with aluminum manufacturers while improving operational integration across refining and smelting facilities.

Chemicals represent the fastest-growing application segment as demand increases for high-purity catalyst carriers, adsorbents, and environmental treatment materials. Advanced processing technologies improve material consistency by nearly 10%, while industrial automation has shortened specialty production cycles by approximately 12%. Companies are expanding specialty refining capabilities, investing in dedicated processing lines, and collaborating with downstream industrial users to address higher-value applications. Demand is steadily shifting toward engineered alumina grades supporting diversified industrial manufacturing beyond conventional metal production.

The Aluminum Industry remains the largest end-user because alumina is the primary feedstock for aluminum smelting, accounting for nearly 90% of industrial demand. Large integrated producers maintain stable procurement volumes supported by transportation, packaging, electrical equipment, and infrastructure manufacturing. Construction and Steel Industry buyers continue consuming specialty alumina through refractory applications, while the Chemical Industry supports demand for catalysts and filtration materials. Suppliers are strengthening integrated delivery agreements and optimizing logistics to improve production continuity for large industrial customers.

Automotive is the fastest-growing end-user segment as lightweight vehicle platforms and electric mobility increase aluminum component adoption. Alumina demand linked to automotive manufacturing has expanded by approximately 13%, while Electronics applications have grown by nearly 9% through advanced ceramic substrates and semiconductor packaging materials. Companies are developing customized product grades, expanding technical partnerships, and strengthening regional supply ecosystems to serve specialized manufacturing requirements. Competitive positioning increasingly depends on application-specific performance rather than production volume alone.

Asia-Pacific accounted for the largest market share at 69.2% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Integrated Supply Chains Strengthen Industrial Resilience

North America maintains a significant position in the alumina market through integrated aluminum manufacturing, advanced refining technologies, and stable downstream demand from transportation, aerospace, and packaging industries. The region contributes approximately 11% of global alumina consumption, supported by refinery modernization and increased recycling integration. Industrial automation deployment across major processing facilities now exceeds 50%, improving operational efficiency and reducing maintenance interruptions. Companies continue strengthening long-term raw material procurement agreements while expanding digital process optimization to improve production reliability amid changing global trade dynamics and energy cost pressures.

United States Market Outlook: The United States remains the region's strategic center due to its advanced aluminum manufacturing ecosystem, aerospace production capacity, and technology-intensive industrial operations. More than 60% of domestic aluminum demand originates from transportation, construction, and packaging sectors, encouraging producers to secure diversified alumina sourcing and invest in digital manufacturing systems. Industrial partnerships focused on refining efficiency and low-emission production continue strengthening operational competitiveness while improving supply-chain resilience.

Low-Carbon Industrial Modernization Reshapes Production

Europe continues transforming its alumina value chain through decarbonization initiatives, refinery modernization, and stricter industrial sustainability requirements. The region accounts for approximately 10% of global alumina demand, supported by specialty manufacturing, automotive production, and advanced engineering industries. More than 35% of large industrial facilities have accelerated energy-efficiency upgrades to improve production performance and regulatory compliance. Producers increasingly prioritize renewable electricity integration, advanced residue management, and strategic procurement partnerships to strengthen long-term manufacturing stability while maintaining competitiveness in high-value industrial applications.

Germany Market Outlook: Germany leads regional industrial demand through its strong automotive, engineering, and advanced manufacturing sectors. Industrial producers continue increasing high-purity alumina consumption for technical ceramics and precision components, while digital production technologies improve manufacturing consistency across specialized applications. Factory modernization initiatives and industrial automation deployment exceeding 45% across major manufacturing operations continue strengthening demand for reliable, high-quality alumina products supporting advanced industrial production.

Large-Scale Refining Capacity Drives Leadership

Asia-Pacific dominates the global alumina market through unmatched refining capacity, integrated aluminum production, and expanding downstream manufacturing. The region contributes nearly 70% of global alumina production, supported by extensive bauxite processing infrastructure and continuous refinery expansion. More than 55% of newly commissioned refining projects incorporate advanced automation and energy-efficient technologies, improving operational productivity and process consistency. Strong domestic aluminum consumption, export-oriented production, and government-backed industrial investments continue reinforcing the region's leadership across the complete alumina value chain.

China Market Outlook: China remains the world's largest alumina producer with approximately 58% of global refining capacity supported by vertically integrated aluminum manufacturing and continuous technology upgrades. Major enterprises continue investing in intelligent refinery operations, predictive maintenance, and lower-emission processing technologies. Expansion of renewable-powered industrial facilities and long-term raw material partnerships strengthens production stability while supporting growing domestic demand from electric vehicles, infrastructure, and advanced manufacturing industries.

Resource-Based Production Supports Export Expansion

South America plays an important role in the global alumina industry through abundant bauxite reserves and export-focused refining operations. The region accounts for approximately 7% of global production, with continued investment in logistics infrastructure and port modernization improving export efficiency. Refinery productivity has improved by nearly 9% through operational optimization and equipment modernization. While transportation infrastructure limitations remain in selected mining corridors, companies continue strengthening integrated mining and refining operations to improve supply reliability and international competitiveness.

Brazil Market Outlook: Brazil dominates the regional alumina industry through extensive bauxite reserves, established refining capacity, and strong export infrastructure. Integrated mining operations support consistent feedstock availability, while industrial investments continue improving refinery efficiency and environmental performance. Automated process monitoring adoption has expanded across leading production facilities, enabling improved operational stability and positioning the country as a reliable supplier for global aluminum manufacturing supply chains.

Industrial Diversification Accelerates Strategic Investment

Middle East & Africa is strengthening its position through industrial diversification, aluminum value-chain expansion, and infrastructure investment supporting downstream manufacturing. The region represents approximately 4% of global alumina demand but continues expanding refining and aluminum production capabilities through integrated industrial developments. Several large-scale industrial projects have improved logistics efficiency by nearly 12%, while strategic investment partnerships support long-term processing capacity expansion. Governments continue prioritizing industrial localization, energy infrastructure, and export-oriented manufacturing to strengthen global competitiveness.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional industrial development through integrated aluminum production, world-class logistics infrastructure, and continuous investment in advanced manufacturing technologies. Large-scale aluminum producers continue expanding operational efficiency through digital process management and energy optimization initiatives. Industrial diversification programs and modern export infrastructure enable stable alumina utilization while strengthening the country's position as a strategic hub connecting Asian, European, and African manufacturing markets.

The competitive landscape is led by Rio Tinto, Alcoa, Aluminum Corporation of China (Chalco), Rusal, and South32, competing against integrated regional refiners and export-focused producers across Australia, China, Brazil, and the Middle East. The top five companies collectively control approximately 48% of global alumina production, while regional suppliers compete through lower logistics costs and localized customer relationships. Competition centers on refining efficiency, energy consumption, supply-chain security, and specialty product capability. Digital process optimization improves refinery productivity by nearly 10%, while vertically integrated operations reduce raw material procurement risk by approximately 15%. Companies are expanding refinery capacity, securing long-term bauxite assets, forming strategic energy partnerships, and investing in low-carbon processing technologies to strengthen operational resilience. The competitive shift favors supply control and technology-enabled production rather than scale alone, accelerating investment in intelligent refining and integrated mining assets. High capital requirements, environmental compliance, and reliable bauxite access remain major entry barriers. Winning requires efficient integrated operations, diversified sourcing, technology leadership, and consistent product quality.

Rio Tinto

Alcoa Corporation

Aluminum Corporation of China (Chalco)

United Company RUSAL

South32

Norsk Hydro ASA

Emirates Global Aluminium

Hindalco Industries Limited

Vedanta Aluminium

National Aluminium Company Limited (NALCO)

Xinfa Group

China Hongqiao Group

Queensland Alumina Limited

Alumina Limited

Digital refinery automation, AI-driven process optimization, and advanced industrial control systems are transforming alumina production efficiency. Predictive maintenance platforms reduce unplanned equipment downtime by approximately 18%, while AI-assisted process control improves refining efficiency by nearly 12%. More than 50% of newly modernized large-scale refineries are integrating real-time analytics, digital twins, and automated quality monitoring. These technologies enable higher production consistency, lower operating costs, and faster operational decision-making, providing integrated producers with stronger competitive performance.

Emerging technologies focus on energy-efficient calcination, residue valorization, and renewable-powered refining. Compared with conventional refining systems, advanced low-emission calcination technologies lower fuel consumption by around 10% while reducing process-related emissions by approximately 14%. Deployment of residue recovery solutions has expanded across nearly 30% of recently upgraded facilities, creating additional industrial by-products and reducing disposal costs. Large integrated producers benefit most because they can deploy new technologies across multiple refining assets while optimizing enterprise-wide production networks.

Between 2026 and 2028, intelligent process orchestration, autonomous inspection systems, and industrial digital platforms will become standard across high-capacity refineries. Companies investing early in automation, cleaner energy integration, and advanced process intelligence will strengthen production flexibility, improve supply-chain resilience, accelerate regulatory compliance, and establish durable cost advantages over competitors relying on conventional refinery operations.

May 2024 – Rio Tinto declared force majeure on third-party alumina export contracts from its Queensland refineries after gas supply disruptions reduced refinery operating capacity. The affected refineries operated below planned utilization, prompting customers to rebalance procurement strategies and reinforcing supply-chain resilience planning. Source: Reuters

July 2024 – Norsk Hydro's Bauxite & Alumina business joined the Heavy Industry Low-carbon Transition Cooperative Research Centre (HILT CRC) to accelerate industrial decarbonization research for alumina refining. The collaboration connects Hydro with more than 53 partners, strengthening technology development and supporting lower-emission refining pathways. Source: Hydro

July 2025 – Alcoa completed the sale of its 25.1% ownership interest in the Ma'aden joint venture while maintaining stable alumina production of approximately 2.4 million metric tons during the quarter. The portfolio optimization strengthened capital allocation and sharpened focus on core refining operations. Source: Alcoa

February 2025 – Hydro reported record performance from its Bauxite & Alumina business and achieved its 10% operational emission-reduction target one year ahead of schedule through refinery decarbonization initiatives. The milestone reinforced competitive positioning while accelerating commercialization of lower-carbon alumina production technologies. Source: Hydro

This report delivers a comprehensive assessment of the global alumina industry across the 2026–2033 strategic planning horizon. It evaluates five product types, five core application areas, and six major end-user industries while providing detailed regional analysis covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study examines production trends, technology deployment, supply-chain evolution, refinery modernization, digital process optimization, and sustainability initiatives influencing operational performance across integrated and independent producers.

The analysis includes competitive benchmarking of leading producers, investment priorities, manufacturing expansion, procurement strategies, and technology adoption patterns, with operational indicators showing automation deployment exceeding 50% in modern refining facilities and specialty-grade demand steadily increasing. It supports investment planning, capacity expansion decisions, partnership evaluation, competitive positioning, risk assessment, and long-term strategic decision-making by identifying high-priority growth segments, emerging industrial applications, evolving customer demand, and future technology pathways shaping the global alumina value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

C111% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

T1 |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

mplayers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |