Reports

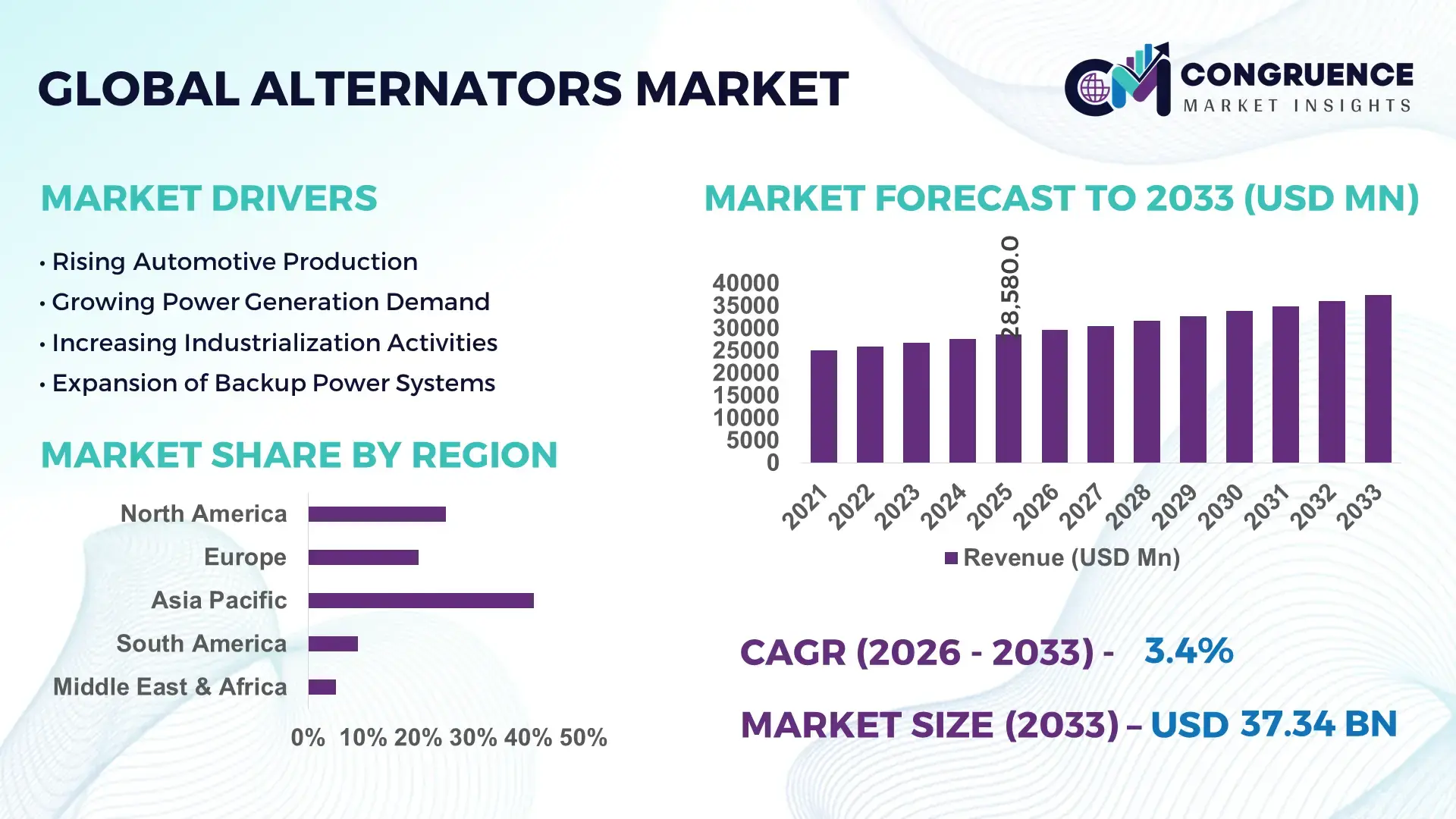

The Global Alternators Market was valued at USD 28580 Million in 2025 and is anticipated to reach a value of USD 37344.49 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033.

Rising electrification across commercial vehicles, industrial backup power systems, and hybrid marine platforms is accelerating demand for high-efficiency alternators with 8–12% better energy conversion performance than conventional wound-field systems. Between 2024 and 2026, tightening emission norms in Europe, North America, and Asia-Pacific, combined with Red Sea shipping disruptions and copper price volatility, pushed manufacturers toward localized production and lightweight alternator designs to reduce supply risk and operational costs.

China remains the dominant country in the global alternators market, accounting for nearly 34% of global production capacity in 2026, supported by large-scale automotive, industrial machinery, and power equipment manufacturing clusters. More than USD 4 billion has been directed toward automotive electrification and advanced component manufacturing upgrades, while over 62% of heavy commercial vehicle production lines now integrate electronically controlled alternator systems. Compared with traditional mechanical charging units, advanced smart alternators improve fuel efficiency by nearly 5% in commercial fleets, strengthening adoption across logistics and construction industries. India and Southeast Asia are also emerging as cost-competitive manufacturing hubs due to lower labor costs and expanding industrial infrastructure investments.

Manufacturers prioritizing regionalized supply chains, high-output smart alternators, and OEM integration partnerships are positioned to secure stronger long-term procurement contracts and operational resilience.

Market Size & Growth: Global market advances from USD 28580 Million in 2025 to USD 37344.49 Million by 2033, supported by vehicle electrification and industrial backup power expansion.

Top Growth Drivers: Commercial vehicle demand contributes 31%, industrial power systems 27%, and marine electrification 14% of incremental market expansion.

Short-Term Forecast: By 2027, smart alternator integration improves fleet fuel efficiency by 6% while reducing maintenance downtime by 11%.

Emerging Technologies: AI-based voltage regulation, lightweight aluminum housings, and high-output smart charging systems increase operational efficiency by 9–13%.

Regional Leaders: Asia-Pacific exceeds USD 15 Billion with manufacturing localization growth; Europe strengthens hybrid vehicle adoption; North America expands data center backup infrastructure investments.

Consumer/End-User Trends: Nearly 58% of commercial fleet operators prioritize high-durability alternators with predictive maintenance compatibility.

Pilot/Case Example: In 2025, a large logistics fleet modernization program reduced charging-system failures by 18% after deploying digitally controlled alternators.

Competitive Landscape: Top manufacturers collectively control nearly 46% market share, with strong positioning from leading automotive and industrial component suppliers.

Regulatory & ESG Impact: Advanced alternators lower vehicle energy losses by up to 7%, supporting stricter global emission compliance targets.

Investment & Funding: More than USD 3.2 Billion has been allocated toward regional production expansion amid global supply chain restructuring.

Innovation & Future Outlook: Next-generation compact alternators with integrated power electronics are accelerating adoption across hybrid mobility and automated industrial systems.

Automotive applications contribute nearly 48% of global alternator demand, followed by industrial machinery at 26% and marine and power generation sectors at 14%. Manufacturers are accelerating adoption of compact smart alternators with digitally controlled voltage regulation and lightweight materials, improving operational efficiency by over 10%. Asia-Pacific continues leading production demand, while Europe strengthens hybrid vehicle integration under stricter emissions policies. Rising localized manufacturing investments and resilient sourcing strategies are reshaping procurement priorities, setting the stage for deeper strategic partnerships and technology-led market competition.

The alternators market is rapidly transforming into a strategic battleground as automotive electrification, industrial automation, and backup power reliability become central to infrastructure investment and fleet efficiency. Commercial vehicle manufacturers are accelerating integration of smart charging systems to reduce fuel consumption and optimize energy distribution across digitally connected platforms. Between 2024 and 2026, tighter emission regulations and regional supply chain restructuring forced manufacturers to shift production closer to OEM hubs, reducing logistics dependency and improving delivery resilience. Brushless smart alternators improve efficiency by 14% while reducing maintenance costs by 18% compared to legacy wound-field systems, strengthening adoption across logistics, mining, and marine industries.

Asia-Pacific leads in production volume with nearly 52% global manufacturing concentration, while Europe leads in smart alternator adoption with over 41% penetration across hybrid commercial fleets. Over the next three years, predictive charging technologies are projected to lower fleet downtime by 12% and improve power management response by 15%. ESG positioning is becoming a competitive advantage as lightweight alternator systems reduce energy losses by 7%, helping OEMs meet stricter fleet emission thresholds and secure procurement eligibility across regulated transport sectors.

In 2025, a major heavy-duty fleet electrification initiative in Germany improved charging efficiency by 16% after deploying digitally regulated alternators integrated with energy management software. Manufacturers are shifting capital allocation toward compact high-output systems, regional assembly expansion, and semiconductor-integrated charging technologies to secure long-term OEM contracts. Companies optimizing smart alternator ecosystems, localized production, and next-generation power efficiency standards are redefining competitive leadership across the global industrial and mobility value chain.

Rapid electrification across commercial transport, industrial equipment, and backup power infrastructure is accelerating demand for advanced alternator systems with higher output stability and lower operational losses. More than 58% of new heavy commercial vehicles now integrate electronically controlled charging systems, while smart alternators improve fuel efficiency by nearly 6% compared to conventional units. Supply chain regionalization after Red Sea shipping disruptions and rising freight costs forced OEMs to localize component sourcing, accelerating manufacturing investments across Asia and Eastern Europe. This shift is driving faster procurement cycles and stronger aftermarket demand. In response, manufacturers are expanding automated production capacity, forming OEM technology partnerships, and increasing investment in lightweight alternator platforms optimized for hybrid mobility and industrial automation systems.

Copper and semiconductor dependency are constraining large-scale alternator production as material price fluctuations continue pressuring manufacturing margins and delivery timelines. Copper costs increased nearly 19% between 2024 and 2026, while semiconductor shortages extended lead times for digitally regulated alternators by over 14%. Concentrated sourcing across limited supplier regions is forcing manufacturers to manage higher inventory costs and operational uncertainty. These disruptions directly impact production scalability, especially for OEM contracts requiring stable high-volume deliveries. Companies are responding through supplier diversification, long-term procurement agreements, and accelerated adoption of aluminum-intensive winding technologies that reduce copper dependency by nearly 11%. Strategic inventory localization and dual-sourcing models are also reshaping procurement strategies to stabilize production continuity and protect profitability.

Integration of smart charging architectures and predictive energy management systems is redefining future opportunities across the alternators market. Digitally controlled alternators improve battery lifecycle performance by nearly 13% while reducing maintenance intervention rates by 17%, creating measurable operational advantages for commercial fleet operators. Emerging economies across Southeast Asia, Latin America, and Africa are accelerating infrastructure modernization and industrial equipment deployment, expanding new demand pockets for compact high-output systems. A significant innovation shift toward AI-enabled voltage regulation and connected diagnostics is strengthening real-time performance optimization. Manufacturers are increasing R&D investment, expanding regional assembly networks, and building integrated software-hardware ecosystems to secure long-term positioning in hybrid mobility, industrial automation, and distributed power generation markets globally.

Performance reliability, thermal management complexity, and infrastructure limitations remain critical execution barriers for next-generation alternator deployment. High-output smart alternators generate nearly 22% greater thermal load than traditional systems, increasing durability risks under heavy industrial and fleet operating conditions. At the same time, inconsistent charging infrastructure integration across emerging markets is slowing adoption of digitally optimized energy systems. Rising compliance requirements for energy efficiency and electromagnetic compatibility are also increasing product validation costs by over 12%. These pressures threaten long-term scalability and product standardization across global OEM networks. To remain competitive, companies must accelerate investment in advanced cooling technologies, semiconductor resilience, and cross-industry engineering partnerships while optimizing software integration capabilities and localized manufacturing adaptability across evolving regulatory environments.

14% rise in smart alternator integration is reshaping commercial fleet operations. Fleet operators are deploying digitally regulated alternators across 48% of new heavy-duty vehicles to improve voltage stability and reduce maintenance intervals by 11%. Manufacturers are accelerating embedded sensor adoption and software-linked charging diagnostics, optimizing service scheduling and lowering operational downtime. Companies are restructuring supplier partnerships to secure semiconductor availability amid continuing electronics sourcing pressure.

22% faster regionalized production cycles are redefining manufacturing execution. Alternator manufacturers are shifting assembly closer to OEM hubs across Asia and Eastern Europe, cutting logistics delays by 18% and inventory holding costs by 9%. Labor shortages in Western Europe are forcing higher automation deployment inside winding and testing operations. Companies are scaling robotic assembly lines and localized procurement strategies to stabilize throughput while improving production consistency under fluctuating material supply conditions.

17% increase in lightweight alternator deployment is shifting product engineering priorities. Automotive and industrial OEMs are replacing conventional copper-heavy units with aluminum-intensive compact systems that reduce component weight by 13% while improving thermal efficiency by 8%. A non-obvious shift is emerging as smaller alternators are enabling tighter engine compartment integration, improving vehicle design flexibility. Manufacturers are accelerating redesign programs and strategic material sourcing agreements to optimize cost-performance balance.

31% expansion in subscription-based maintenance contracts is redefining aftermarket business models. Industrial operators are adopting predictive maintenance packages linked with alternator monitoring systems, reducing unexpected equipment failures by 16%. Companies are bundling diagnostics, remote monitoring, and replacement services into long-term operational agreements, strengthening recurring revenue streams and customer retention. Regulatory pressure around uptime reliability is forcing service-focused competition alongside traditional hardware differentiation.

The alternators market is segmented by type, application, and end-user, with automotive and industrial demand dominating purchasing concentration. Automotive alternators account for nearly 42% of total deployment due to continuous charging requirements across passenger and commercial vehicles, while three-phase systems represent over 38% of industrial installations because of higher power stability and operational efficiency. Demand is rapidly shifting toward brushless and smart-controlled alternators as fleet operators prioritize lower maintenance and improved energy optimization. Industrial manufacturing, energy and utilities, and construction sectors are accelerating adoption of digitally regulated systems, forcing manufacturers to expand localized production, integrated diagnostics, and application-specific product customization strategies.

Three-phase alternators dominate the market with nearly 38% share due to superior power stability, higher load-handling capability, and scalability across industrial machinery, backup power systems, and commercial infrastructure. Their structural advantage lies in consistent voltage delivery and lower operational losses, making them the preferred choice for continuous-duty environments. Automotive alternators are emerging as the fastest-shifting category, recording nearly 15% higher adoption across smart vehicle platforms as OEMs accelerate electrification and digitally controlled charging integration. Compared with brushed systems, brushless alternators deliver nearly 20% lower maintenance requirements and improved operational lifespan, accelerating replacement demand in heavy commercial fleets and industrial operations.

Brushed, single-phase, and conventional automotive alternators collectively account for nearly 44% of market deployment, retaining relevance in cost-sensitive applications, agriculture equipment, and smaller backup systems where affordability outweighs advanced efficiency requirements. However, companies are steadily reallocating investment toward compact brushless platforms and high-output three-phase systems. Manufacturers are expanding automated winding capacity, increasing semiconductor-integrated product development, and optimizing lightweight alternator designs to capture shifting demand. Investment focus is clearly moving toward high-efficiency, digitally controlled systems, while legacy brushed technologies face gradual replacement pressure across industrial and transportation sectors.

Automotive charging systems lead the alternators market with nearly 36% share, driven by continuous vehicle electrification, rising onboard electronics integration, and expanding commercial fleet operations. Usage concentration remains strongest in heavy-duty transport and hybrid vehicle platforms where charging efficiency and battery management directly affect operational performance. Backup power systems are emerging as the fastest-growing application segment, with deployment increasing by nearly 18% as data centers, healthcare facilities, and industrial sites prioritize uninterrupted power continuity amid grid instability and rising energy reliability concerns.

Power generation applications remain structurally important due to large-scale deployment across industrial infrastructure and decentralized energy systems, while industrial machinery and construction equipment collectively account for nearly 34% of application demand because of intensive operational cycles and high energy output requirements. Compared with traditional industrial machinery use cases, marine equipment applications are shifting toward compact corrosion-resistant alternators optimized for hybrid propulsion integration and onboard energy optimization. Manufacturers are responding by scaling high-output product lines, strengthening OEM partnerships, and redesigning systems for application-specific durability and digital monitoring compatibility. Demand is increasingly concentrating around smart-controlled and high-efficiency charging applications where uptime reliability and energy optimization deliver measurable operational advantage.

The automotive sector leads alternator consumption with approximately 41% share due to large-scale vehicle production, continuous charging dependency, and growing integration of advanced electronic systems across passenger and commercial fleets. Demand concentration is strongest among heavy commercial vehicles where alternator durability, charging stability, and fuel optimization directly influence operating costs. Energy and utilities is the fastest-growing end-user segment, with adoption rising nearly 17% as power infrastructure operators accelerate deployment of backup generation systems and digitally monitored energy platforms to strengthen grid resilience and operational continuity.

Industrial manufacturing remains a high-volume buyer because of intensive machinery utilization and continuous operational requirements, while construction, marine, and agriculture collectively contribute nearly 39% of total demand through specialized equipment deployment and rugged operating environments. Compared with traditional agriculture procurement focused on affordability, marine and utilities buyers are prioritizing corrosion resistance, predictive diagnostics, and high-output compact systems. Companies are responding through tiered pricing strategies, customized product engineering, and regional distribution partnerships targeting application-specific performance requirements. Future demand is clearly shifting toward digitally integrated and low-maintenance alternators, forcing manufacturers to prioritize smart diagnostics, localized service networks, and operational reliability differentiation.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2026 and 2033.

Asia-Pacific dominates global alternator production and consumption due to large-scale automotive manufacturing, industrial expansion, and cost-efficient supply chains concentrated in China, India, and Southeast Asia. Europe captures nearly 24% of global demand and leads in smart alternator adoption driven by strict emission regulations and advanced hybrid vehicle integration. North America contributes approximately 21% share, supported by commercial fleet modernization and expanding backup power infrastructure demand. Meanwhile, Middle East & Africa is accelerating infrastructure-linked deployment across energy, construction, and industrial projects. Ongoing supply chain regionalization and localized production strategies are reshaping global procurement patterns. Companies are increasingly prioritizing Asia-Pacific for scale, Europe for technology integration, and Middle East & Africa for expansion-driven infrastructure opportunities.

North America holds nearly 21% of the global alternators market, supported by strong commercial vehicle production, industrial automation, and expanding backup power infrastructure demand. The United States dominates regional consumption due to rising deployment of digitally controlled charging systems across logistics fleets and critical infrastructure facilities. More than 54% of heavy-duty fleet upgrades now prioritize smart alternators integrated with predictive maintenance systems to reduce downtime and improve operational efficiency. Supply chain localization initiatives and stricter energy-efficiency standards are accelerating investment in domestic component manufacturing. Several manufacturers expanded regional assembly capacity by over 12% between 2024 and 2026 to stabilize delivery timelines. Enterprise buyers increasingly favor high-durability, low-maintenance systems, reinforcing North America’s strategic importance for premium alternator technologies and long-term industrial contracts.

Europe accounts for approximately 24% of global alternator demand, with Germany, France, and Italy leading adoption across automotive and industrial applications. Tightened vehicle emission standards and industrial energy-efficiency regulations are forcing OEMs to accelerate deployment of lightweight smart alternators capable of reducing energy losses by nearly 7%. More than 43% of new hybrid commercial vehicle platforms now integrate digitally regulated charging systems to improve operational efficiency and compliance performance. Manufacturers are increasing investment in compact brushless technologies and localized sourcing networks to reduce carbon-intensive supply chain exposure. Enterprise procurement behavior across Europe remains quality-focused and compliance-driven, prioritizing durability, efficiency, and lifecycle cost optimization over low-cost alternatives. This region is redefining competitive standards by forcing continuous innovation in high-efficiency alternator engineering and regulatory adaptability.

Asia-Pacific leads the global alternators market with nearly 46% share, driven by dominant automotive production, industrial machinery expansion, and cost-efficient manufacturing ecosystems across China, India, Japan, and South Korea. China alone contributes more than 34% of regional production capacity due to vertically integrated supply chains and large-scale component manufacturing infrastructure. Over 61% of regional OEMs are accelerating localized sourcing and automated assembly deployment to improve production speed and reduce logistics dependency. Manufacturers are rapidly expanding semiconductor-integrated alternator output and export-oriented production lines to meet growing global demand. Enterprise buyers across the region prioritize scalability, delivery speed, and cost optimization, strengthening Asia-Pacific’s role as the global production hub. Companies targeting volume expansion and manufacturing resilience continue prioritizing this region for long-term operational scaling.

South America represents nearly 6% of the global alternators market, with Brazil and Argentina leading regional demand through automotive manufacturing, agriculture equipment deployment, and industrial machinery modernization. Construction and mining activities are increasing alternator usage across heavy equipment fleets, while backup power requirements are expanding due to infrastructure reliability gaps. However, import dependency and currency volatility continue constraining large-scale procurement flexibility and raising component costs by nearly 9% across certain industrial segments. Companies are responding by strengthening localized distribution networks and increasing regional aftermarket service capabilities. More than 28% of fleet operators are prioritizing low-maintenance alternators to reduce operational expenses and extend equipment lifecycle. The region presents strong expansion potential, but companies must balance pricing sensitivity with localized supply and service adaptability.

Middle East & Africa contributes approximately 3% of global alternator demand, with Saudi Arabia, the UAE, and South Africa driving deployment across oil and gas, infrastructure construction, utilities, and industrial modernization projects. Large-scale infrastructure investments and industrial diversification initiatives are accelerating demand for high-output backup power and heavy-equipment charging systems. More than 32% of industrial project operators are deploying digitally monitored alternators to improve operational continuity and reduce maintenance intervention frequency. Strategic partnerships between regional distributors and global manufacturers are strengthening localized servicing and equipment availability. Enterprise buyers increasingly prioritize durability, thermal performance, and long operational lifespan under harsh environmental conditions. The region is emerging as a strategic infrastructure-driven growth zone where operational reliability and localized technical support determine long-term market positioning.

China – 34% market share in the Alternators market, supported by dominant automotive production capacity, vertically integrated supply chains, and large-scale industrial equipment manufacturing.

United States – 18% market share in the Alternators market, driven by strong commercial fleet demand, expanding backup power infrastructure, and advanced smart charging system adoption.

The alternators market is dominated by competition between global OEM-aligned manufacturers including Denso Corporation, Valeo, Mitsubishi Electric, Bosch, and Cummins, against regional cost-focused suppliers and specialized industrial power equipment producers. The top five players collectively control nearly 46% of global market activity, leveraging scale, technology integration, and long-term automotive and industrial contracts. Competition is increasingly shifting toward smart alternator efficiency, localized production, and supply chain resilience rather than pure pricing pressure. Advanced brushless systems improve operational efficiency by nearly 14%, while localized sourcing strategies reduce logistics costs by approximately 9%, forcing competitors to optimize manufacturing agility and component availability. Companies are expanding semiconductor-integrated product lines, strengthening OEM partnerships, and increasing vertical integration to stabilize raw material access. Rising thermal management complexity and regulatory compliance costs are creating high entry barriers. Winning requires scalable manufacturing, digitally integrated charging technology, and resilient multi-region supply capabilities.

Denso Corporation

Valeo

Mitsubishi Electric Corporation

Robert Bosch GmbH

Cummins Inc.

Hitachi Astemo Ltd.

Mecc Alte S.p.A.

Prestolite Electric Incorporated

Leroy-Somer

Stamford AvK

Nidec Corporation

WEG S.A.

Kirloskar Electric Company

CG Power and Industrial Solutions Limited

Smart alternator systems integrated with digital voltage regulators and predictive diagnostics are becoming the operational standard across commercial fleets and industrial equipment. More than 58% of newly deployed heavy commercial vehicles now use electronically controlled alternators that improve charging efficiency by nearly 12% while reducing maintenance intervention by 15%. Integration with onboard energy management software is optimizing battery performance and lowering fleet downtime. Manufacturers deploying semiconductor-based control modules are gaining competitive advantage through faster response times and improved thermal stability under high-load conditions.

Emerging 48V mild-hybrid alternator technologies are accelerating adoption across automotive and industrial mobility platforms between 2026 and 2028. Compared with conventional stop-start charging systems, 48V belt starter generators improve fuel efficiency by up to 6% while enabling regenerative braking integration and smoother power delivery. Nearly 41% of hybrid commercial vehicle platforms are transitioning toward compact high-output systems with advanced thermal dissipation capabilities. Companies investing in lightweight aluminum-intensive alternators are also reducing system weight by approximately 13%, improving energy optimization and installation flexibility.

Disruptive brushless architectures and AI-enabled charging analytics are redefining performance expectations across industrial and backup power applications. Brushless alternators deliver nearly 20% lower maintenance costs and 14% higher operational reliability compared to brushed systems. Industrial operators are accelerating adoption of digitally monitored alternators to optimize uptime and reduce unexpected equipment failures. Manufacturers scaling software-integrated charging platforms and rare-earth-efficient designs are positioned to capture long-term OEM contracts as intelligent power management becomes a decisive competitive differentiator.

September 2024 – Valeo showcased advanced 48V hybrid systems and alternator-integrated electrification technologies for commercial vehicles at IAA Transportation 2024, with commercial mobility order intake increasing by 100% since 2022. The expansion strengthens Valeo’s position in hybrid fleet electrification and last-mile delivery systems. [Hybrid Fleet Expansion] Source: Valeo

July 2024 – Valeo upgraded its 48V Belt Starter Generator technology with enhanced thermal decoupling and regenerative braking integration, delivering up to 6% fuel economy improvement compared to conventional stop-start systems. The development improves charging efficiency and supports broader mild-hybrid commercial vehicle deployment. [Smart Charging Upgrade] Source: Valeo Technology Overview

June 2024 – Valeo introduced an enhanced 48V mid-drive electric propulsion system at Eurobike 2024 featuring 130Nm torque output and approximately 7dB lower operating noise through redesigned gear geometry and vibration optimization. The launch strengthens high-efficiency electric mobility integration and premium performance positioning. [Noise Reduction Shift]

2024 – Valeo and Renault accelerated development of next-generation rare-earth-free electric motor systems linked with advanced alternator and electrification technologies. One-third of global vehicles now operate with Valeo electrical systems integration, strengthening supply diversification and reducing dependency on constrained magnetic material sourcing. [Rare-Earth Diversification]

The Alternators Market Report delivers comprehensive analysis across product types including brushless, brushed, single-phase, three-phase, and automotive alternators, alongside application areas such as power generation, automotive charging systems, industrial machinery, marine equipment, construction equipment, and backup power systems. The report also evaluates demand behavior across automotive, industrial manufacturing, marine, construction, energy and utilities, and agriculture end-users. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with strategic assessment of production concentration, localization trends, and smart charging technology adoption patterns. More than 58% of commercial fleet deployments and nearly 43% of hybrid platform integrations are analyzed through operational efficiency and deployment metrics.

The report provides detailed competitive benchmarking of leading manufacturers, supply chain positioning, and technology transitions including digitally regulated alternators, 48V belt starter generators, predictive diagnostics integration, and lightweight aluminum-intensive systems. Analytical coverage includes over 10 major companies, key regional manufacturing hubs, and execution-level shifts reshaping procurement and product development strategies between 2026 and 2033. Strategic insights support investment prioritization, regional expansion planning, OEM partnership evaluation, and competitive positioning by identifying where operational demand, infrastructure modernization, and next-generation alternator adoption are accelerating globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 28580 Million |

|

Market Revenue in 2033 |

USD 37344.49 Million |

|

CAGR (2026 - 2033) |

3.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Denso Corporation, Valeo, Mitsubishi Electric Corporation, Robert Bosch GmbH, Cummins Inc., Hitachi Astemo Ltd., Mecc Alte S.p.A., Prestolite Electric Incorporated, Leroy-Somer, Stamford AvK, Nidec Corporation, WEG S.A., Kirloskar Electric Company, CG Power and Industrial Solutions Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |