Reports

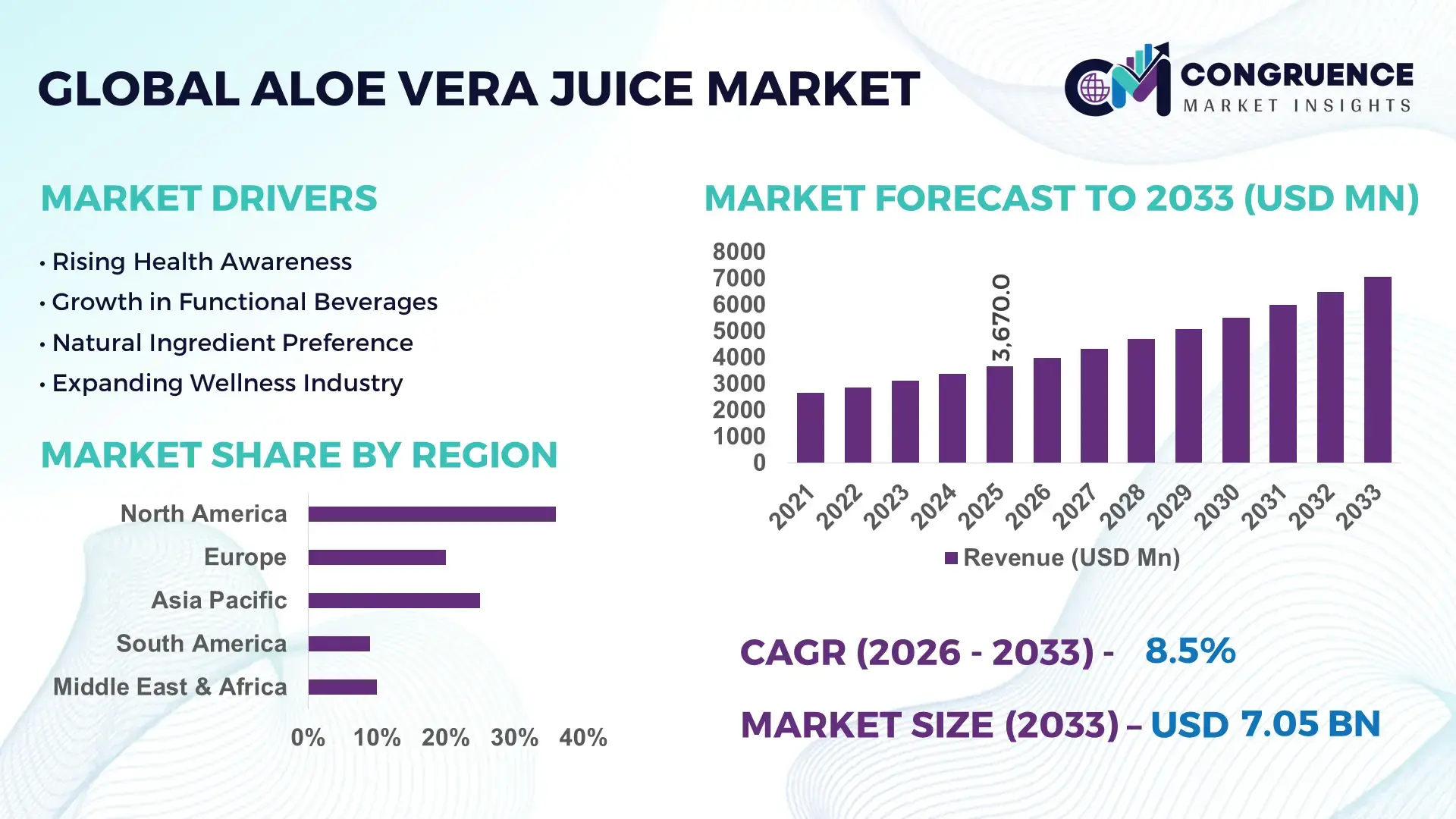

The Global Aloe Vera Juice Market was valued at USD 3670 Million in 2025 and is anticipated to reach a value of USD 7048.61 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033. Growth is primarily driven by increasing utilization of aloe vera juice in functional beverages, digestive health formulations, clean-label nutrition products, and plant-based wellness portfolios across retail and foodservice channels.

The United States remains the dominant country in the aloe vera juice market, accounting for approximately 29% of global consumption, supported by a mature functional beverage industry, advanced cold-chain distribution, and strong penetration of wellness-focused products. More than 65% of premium health drink launches in North America now emphasize natural or botanical ingredients, strengthening aloe vera juice adoption. In comparison, India is emerging as a major production hub, contributing over 20% of global aloe cultivation capacity due to favorable agricultural conditions and expanding processing infrastructure. Investments in advanced extraction technologies have improved yield efficiency by nearly 18%, while supply diversification efforts accelerated following Red Sea shipping disruptions that affected global ingredient logistics in 2025–2026.

Market participants are prioritizing vertically integrated sourcing, processing efficiency, and premium product differentiation to strengthen margins and secure long-term growth opportunities.

Market Size & Growth: USD 3670 million in 2025 rising to USD 7048.61 million by 2033 at 8.5% CAGR, supported by expanding functional beverage portfolios and advanced extraction technologies.

Top Growth Drivers: Digestive wellness demand (+34%), clean-label beverage adoption (+28%), and plant-based nutrition consumption (+24%) drive market expansion.

Short-Term Forecast: By 2028, processing efficiency improves by 15% through automation, reducing production waste and enhancing output consistency.

Emerging Technologies: AI-driven quality monitoring, cold-press extraction, and advanced filtration systems improve product purity by up to 20%.

Regional Leaders: North America exceeds USD 2.1 billion, Asia-Pacific reaches USD 1.9 billion, and Europe surpasses USD 1.5 billion, supported by health-focused consumption trends.

Consumer/End-User Trends: Over 42% of health-conscious beverage buyers actively seek botanical and digestive wellness ingredients in daily drink selections.

Pilot/Case Example: 2025 manufacturing modernization projects improved extraction yields by 18% while lowering processing losses by 12%.

Competitive Landscape: Top producers collectively control roughly 35% market share, with competition focused on premium formulations and distribution expansion.

Regulatory & ESG Impact: Sustainable cultivation initiatives reduced agricultural water consumption by approximately 14% across certified production operations.

Investment & Funding: More than USD 500 million in industry investments supported processing expansion, supply-chain resilience, and product innovation programs.

Innovation & Future Outlook: High-growth formulations combining aloe vera with probiotics and adaptogens increase product differentiation and premium market positioning.

Demand is increasingly concentrated in digestive health beverages, sports recovery drinks, functional nutrition products, and clean-label wellness formulations. Manufacturers are introducing cold-processed aloe vera juice, probiotic-infused variants, and reduced-sugar formulations to address evolving consumer preferences. Nearly 40% of new product launches emphasize multi-functional health benefits beyond hydration alone. Supply-chain diversification, regional processing investments, and stricter ingredient traceability standards are reshaping procurement strategies across major markets. These developments are strengthening competitive positioning while setting the foundation for a deeper strategic evaluation of growth opportunities, investment priorities, and market expansion pathways.

The Aloe Vera Juice Market is becoming strategically important as beverage manufacturers, nutraceutical brands, and ingredient suppliers compete for positioning in the expanding functional wellness ecosystem. Demand is shifting from conventional refreshment beverages toward products with digestive, hydration, and clean-label benefits, prompting portfolio diversification across major consumer goods companies. A notable market shift is the restructuring of botanical ingredient supply chains, with processors increasing local sourcing and contract farming networks to improve raw material availability and quality consistency while reducing logistics exposure.

Technology modernization is reshaping production economics. Advanced cold-processing and membrane filtration systems improve active compound retention by nearly 20% while reducing processing losses by approximately 15% compared with traditional thermal extraction methods. The United States leads in premium product innovation and branded distribution, whereas India maintains an advantage in cultivation scale and processing capacity. Over the next two to three years, automation adoption across large processing facilities is expected to exceed 45%, improving throughput, traceability, and inventory management.

A practical example is the deployment of vertically integrated cultivation-to-bottling models that reduce procurement variability and strengthen quality assurance. Companies are expanding strategic partnerships with agricultural cooperatives, investing in extraction infrastructure, and developing value-added formulations. Organizations that combine sourcing resilience, processing efficiency, and product innovation will secure stronger competitive positioning and long-term relevance in the evolving health beverage landscape.

The accelerating shift toward preventive nutrition and functional beverages remains the primary growth driver for the Aloe Vera Juice Market. More than 42% of health-focused beverage consumers actively seek botanical ingredients, while clean-label product launches have increased by over 30% across major retail channels. In the United States, digestive wellness beverages represent one of the fastest-growing health drink categories, encouraging manufacturers to expand aloe-based portfolios. Enhanced extraction technologies have improved ingredient retention by nearly 20%, increasing product efficacy and premium positioning. This demand-to-innovation cycle is driving investments in cultivation, processing, and product development. Companies are responding through contract farming agreements, new production facilities, and partnerships with wellness brands. A key strategic insight is that supply security has become as important as product differentiation, making vertically integrated sourcing a competitive advantage.

The market faces structural constraints from agricultural dependency, seasonal yield fluctuations, and rising processing costs. Aloe cultivation output can vary by 15–20% depending on weather conditions, while transportation and packaging expenses have increased by approximately 12% in key producing countries. India and Mexico, both major aloe-producing hubs, continue to experience periodic supply imbalances that affect processor planning and inventory management. Product quality consistency remains challenging because bioactive compound concentrations differ across cultivation environments. These factors directly impact manufacturing efficiency, profitability, and premium product scalability. To reduce exposure, companies are diversifying supplier networks, increasing localized processing capabilities, and securing long-term procurement contracts. An important operational insight is that procurement optimization now plays a larger role in margin protection than traditional production efficiency improvements alone.

Significant opportunities are emerging through next-generation functional beverage development and value-added ingredient integration. Products combining aloe vera with probiotics, adaptogens, and plant-based nutrients have demonstrated consumer preference increases exceeding 25% in premium wellness segments. In Japan, advanced formulation technologies are improving ingredient stability by nearly 18%, enabling longer shelf life and broader distribution reach. Digital traceability platforms are also gaining adoption, improving supply transparency and supporting premium brand positioning. Companies are investing in R&D programs, formulation partnerships, and specialized product launches targeting digestive health, sports recovery, and healthy aging applications. A non-obvious strategic opportunity lies in developing pharmaceutical-grade and nutraceutical-grade aloe ingredients, which command higher margins and create differentiation beyond conventional beverage markets.

Maintaining consistent quality standards across expanding supply chains represents a major long-term challenge. Product testing requirements have increased by approximately 20% as manufacturers face stricter ingredient verification and labeling expectations. In the United States and Germany, regulatory scrutiny surrounding botanical ingredient claims continues to intensify, increasing compliance complexity. Rapid production expansion also creates workforce training and operational standardization challenges, particularly when processing facilities operate across multiple sourcing regions. These issues affect deployment consistency, brand credibility, and long-term competitiveness. Companies must invest in laboratory infrastructure, digital quality monitoring systems, and standardized cultivation protocols to maintain product integrity. A critical strategic insight is that future market leaders will be distinguished not by production volume alone, but by their ability to deliver verified quality and traceability at scale across global operations.

Premium Functional Blends Expand Manufacturers are increasingly combining aloe vera with probiotics, adaptogens, and botanical extracts, with premium wellness formulations growing by nearly 28% and new product introductions rising over 20% during 2025–2026. Demand for multi-benefit beverages is reshaping product development workflows, improving shelf differentiation and pricing power. Companies are expanding formulation partnerships and accelerating innovation pipelines to capture higher-margin consumer segments.

Automation Reshapes Processing Operations Processing facilities are deploying automated extraction, filtration, and packaging systems, improving throughput by approximately 18% while reducing production losses by 12%. Labor availability challenges in major agricultural regions and rising operating costs have accelerated technology adoption. Companies are modernizing facilities, integrating digital quality controls, and restructuring production networks to enhance consistency and reduce operational variability.

Traceability Becomes Competitive Priority Ingredient transparency programs have expanded significantly, with digital tracking adoption increasing by more than 25% among large beverage manufacturers. Regulatory scrutiny surrounding botanical ingredient claims and sourcing practices is driving investments in traceability infrastructure. A notable shift is that procurement transparency is becoming a product differentiation tool rather than solely a compliance requirement, encouraging suppliers to strengthen cultivation-to-bottling visibility.

Localized Supply Networks Accelerate Companies are reducing long-distance sourcing dependence by expanding regional cultivation partnerships and contract farming programs. Localized procurement initiatives have shortened ingredient lead times by nearly 15% and improved inventory stability by approximately 10%. Supply-chain disruptions experienced across global shipping routes have reinforced the value of distributed sourcing models, prompting processors to prioritize resilience alongside production efficiency.

Ready-to-Drink remains the leading type segment, accounting for an estimated 38% of market demand due to convenience, established retail distribution, and strong integration within health beverage portfolios. Its scalability and rapid consumer adoption make it the preferred format for beverage manufacturers. Flavored Aloe Vera Juice is emerging as the fastest-growing segment, supported by changing taste preferences and a growing premium beverage category, with product launch activity increasing by approximately 24% during the past two years. Organic variants continue gaining traction among wellness-focused consumers, particularly in the United States and Germany, where clean-label purchasing behavior remains strong. Conventional products maintain substantial volume leadership in price-sensitive markets due to lower production costs and wider accessibility. Concentrated Aloe Vera Juice retains strategic importance for bulk ingredient applications, food processing, and export channels. Companies are investing in flavor innovation, premium formulations, and expanded distribution networks while balancing affordability and product differentiation to capture evolving demand patterns.

Functional Beverages represent the largest application segment, supported by widespread consumer adoption of wellness-focused drinks and increasing demand for hydration and digestive support solutions. The segment accounts for approximately 35% of overall application demand and benefits from extensive retail penetration. Beauty and Wellness Drinks are the fastest-growing application area, with adoption increasing by nearly 22% as consumers increasingly seek products linked to skin health and holistic wellness. Digestive Health Products remain a mature and strategically important category, supported by aloe vera’s established positioning within gut-health formulations. Dietary Supplements and Nutraceutical Products continue expanding through capsule, powder, and liquid delivery formats, while Sports Nutrition applications are gaining momentum through recovery-focused beverage innovations. Companies are increasing production capacity, developing targeted formulations, and integrating automated manufacturing systems to address evolving application-specific requirements and strengthen competitive positioning.

The Food and Beverage Industry remains the dominant end-user group, representing approximately 44% of total consumption due to extensive deployment across beverage manufacturing, formulation development, and large-scale distribution networks. Nutraceutical Companies are the fastest-growing end-user segment, supported by increasing demand for plant-based ingredients and specialized wellness formulations, with procurement volumes rising by nearly 20% across several key markets. Retail Consumers continue driving direct demand through health-conscious purchasing behavior and expanding e-commerce accessibility. The Healthcare Sector is strengthening its role through preventive wellness and nutritional support applications, while Fitness Centers increasingly incorporate aloe-based beverages into recovery and hydration programs. The Hospitality Industry maintains a niche but growing presence through premium wellness offerings. Companies are responding through customized product portfolios, strategic ingredient partnerships, and targeted pricing strategies designed to address the specific operational requirements of each end-user category.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2026 and 2033.

Premium Functional Beverage Integration Accelerates Market Leadership

North America maintains the largest share of the Aloe Vera Juice Market due to strong functional beverage adoption, advanced processing infrastructure, and extensive retail distribution networks. The region contributes approximately 36% of global demand, supported by high penetration of digestive wellness and clean-label beverage products. Manufacturers are increasingly integrating aloe vera into premium hydration, immunity, and wellness formulations. Automation investments have improved production efficiency by nearly 15% across large beverage facilities, while strategic ingredient partnerships continue strengthening supply reliability. Enterprise demand remains concentrated among nutraceutical producers and branded beverage companies seeking differentiated botanical ingredients. Product innovation, advanced packaging technologies, and premium product positioning remain key competitive levers.

United States Market Outlook: The United States serves as the region’s operational and commercial center, supported by mature health beverage infrastructure and strong consumer acceptance of functional ingredients. More than 60% of premium botanical beverage launches include wellness-focused positioning, driving sustained aloe vera integration. Companies continue expanding contract sourcing programs, investing in cold-processing technologies, and strengthening retail partnerships. Advanced manufacturing capabilities and high-value product development allow domestic producers to maintain leadership in premium aloe-based beverage innovation.

Clean-Label Compliance Shapes Product Development

Europe represents a significant market driven by stringent ingredient standards, sustainability priorities, and growing demand for natural wellness beverages. The region accounts for approximately 27% of global consumption, with manufacturers emphasizing traceability, quality verification, and environmentally responsible sourcing. Ingredient transparency initiatives have increased by nearly 20% among leading beverage producers, reflecting evolving consumer and regulatory expectations. Product development increasingly focuses on organic and low-processing formulations. Investments in sustainable packaging and digital supply-chain monitoring continue improving operational efficiency while strengthening premium brand positioning. The market benefits from established nutraceutical and wellness product ecosystems.

Germany Market Outlook: Germany remains the most strategically important market due to its strong nutraceutical industry, advanced food manufacturing capabilities, and rigorous quality standards. Enterprise adoption of certified botanical ingredients continues expanding, supported by sophisticated retail and pharmacy distribution channels. More than 40% of wellness beverage launches emphasize clean-label or natural ingredient positioning. Companies are prioritizing ingredient traceability systems, formulation innovation, and premium product development to meet evolving consumer expectations and strengthen competitive differentiation.

Production Scale and Consumption Expansion Drive Momentum

Asia-Pacific is emerging as the fastest-expanding market due to extensive cultivation capacity, rising wellness awareness, and expanding beverage manufacturing infrastructure. The region accounts for roughly 24% of global demand while contributing a substantial share of aloe vera raw material production. Processing investments have increased extraction capacity by approximately 18% in key production hubs, improving supply availability and export readiness. Growing urban consumption patterns and expanding functional beverage portfolios continue strengthening market penetration. Companies are increasing production integration, investing in cultivation partnerships, and modernizing extraction facilities to improve operational efficiency and quality consistency.

India Market Outlook: India serves as the region’s primary cultivation and processing hub, benefiting from favorable agricultural conditions and extensive aloe vera farming networks. The country contributes more than 20% of global aloe cultivation capacity and continues attracting investment in extraction and value-added processing operations. Domestic beverage and nutraceutical manufacturers are expanding production capabilities while strengthening farmer partnerships. Technology upgrades in processing facilities have improved extraction yields and quality consistency, enhancing India's competitiveness in both domestic and export-oriented supply chains.

Agricultural Resource Utilization Supports Expansion

South America holds a developing position within the market, supported by favorable cultivation environments and increasing investment in value-added agricultural products. The region contributes approximately 7% of global demand and continues expanding processing infrastructure to improve commercial scalability. Strategic partnerships between agricultural producers and beverage manufacturers are improving supply reliability and reducing sourcing costs. Processing modernization projects have enhanced operational efficiency by nearly 12% in selected production facilities. While infrastructure limitations remain in certain markets, expanding domestic wellness consumption and export opportunities continue strengthening long-term industry prospects.

Brazil Market Outlook: Brazil represents the region’s most influential market due to its large consumer base, established food processing sector, and growing functional beverage industry. Manufacturers are increasingly incorporating aloe vera into health-oriented beverage portfolios and wellness product lines. Investments in agricultural processing infrastructure and regional distribution networks are improving commercial reach. Expanding demand for natural ingredients, combined with strong domestic manufacturing capabilities, positions Brazil as a key growth center for aloe-based product development and commercialization.

Investment-Led Modernization Expands Market Presence

The Middle East & Africa market is advancing through investments in food processing modernization, health-focused product diversification, and agricultural value-chain development. The region accounts for approximately 6% of global demand, with growth supported by expanding wellness product availability and increasing retail penetration. Several markets are investing in localized processing capabilities to reduce import dependency and improve supply resilience. Modern production initiatives have shortened distribution lead times by nearly 10% while enhancing product availability. Companies are leveraging partnerships, infrastructure upgrades, and distribution expansion strategies to strengthen market access and operational efficiency.

United Arab Emirates Market Outlook: The United Arab Emirates functions as a regional commercial hub supported by advanced logistics infrastructure, modern retail networks, and strong demand for premium wellness products. Beverage manufacturers and distributors increasingly use the country as a gateway for regional market expansion. Growth in health-focused retail channels and premium beverage offerings continues supporting aloe vera product penetration. Investments in warehousing, distribution technology, and specialty beverage portfolios enhance operational flexibility and strengthen the country's strategic role within regional supply chains.

The Aloe Vera Juice Market is led by global ingredient specialists and branded wellness beverage companies competing against regional processors and cultivation-integrated suppliers. Key competitors include Lily of the Desert, ALO Drink, Forever Living Products, OKF Corporation, Aloe Farms, and Patanjali Ayurved. The top five players collectively control approximately 32% of market activity, creating a moderately fragmented competitive structure. Global brands compete through formulation innovation and distribution reach, while regional producers focus on cost efficiency and cultivation access. Competition centers on product quality, supply-chain control, and premium positioning, with processing efficiency improvements of 15–20% and traceability adoption exceeding 25% among leading operators. Companies are expanding cultivation partnerships, investing in extraction technology, and pursuing vertical integration to secure raw material availability. The competitive shift is increasingly toward supply control and value-added formulations rather than volume expansion alone. Entry barriers include sourcing consistency, quality certification requirements, and processing expertise. Winning requires integrated sourcing, operational efficiency, premium product differentiation, and scalable distribution execution.

Forever Living Products

Lily of the Desert

ALO Drink

OKF Corporation

Aloe Farms Inc.

Patanjali Ayurved Ltd.

Herbalife Ltd.

Terry Laboratories Inc.

Aloe Vera Australia Pty Ltd.

Dynamic Health Laboratories

Pharmachem Laboratories Inc.

Houssy Global

Fruit of the Earth Inc.

Real Aloe Inc.

Advanced extraction and processing technologies are becoming central to product quality and operational efficiency. Cold-pressed extraction systems improve retention of bioactive compounds by approximately 18% compared with conventional thermal methods while reducing ingredient degradation. More than 40% of large-scale processors have adopted automated filtration and aseptic filling technologies to improve consistency and extend shelf life. These systems reduce production losses by nearly 12% and strengthen premium product positioning. Companies with integrated processing capabilities benefit through improved quality control, stronger retailer acceptance, and lower batch variability.

Emerging technologies are focused on digital traceability, intelligent quality monitoring, and precision cultivation. AI-enabled quality inspection platforms improve defect detection rates by approximately 20%, while blockchain-based ingredient tracking systems reduce supply-chain verification time by nearly 30%. Adoption of digital traceability platforms has surpassed 25% among leading beverage manufacturers. These technologies support regulatory compliance, ingredient transparency, and faster supplier qualification. Companies are increasingly integrating farm-to-bottle monitoring systems to strengthen procurement visibility and protect premium brand value.

Disruptive innovation between 2026 and 2028 will center on membrane filtration, smart manufacturing, and functional ingredient enhancement. Next-generation membrane systems improve extraction efficiency by approximately 15% compared with legacy filtration technologies while reducing water consumption. Automated production environments are expected to exceed 50% deployment among major processors. Competitive advantage will increasingly favor vertically integrated producers and technology-enabled beverage brands that combine sourcing control, processing precision, and scalable product innovation.

March 2026 – Emami Ltd. acquired Axiom Ayurveda and strengthened its aloe-based beverage portfolio, expanding presence in wellness drinks and increasing strategic category participation through the AloFrut brand.

February 2026 – ALO Drink announced rollout of new 10.8-ounce slim-can flavors including Passion Fruit & Pulp and Sugarcane & Calamansi, expanding ready-to-drink product innovation and improving on-the-go consumer reach.

September 2024 – OKF Corporation expanded North American distribution through a partnership with KeHE Distributors while introducing organic aloe formulations, strengthening retail penetration and accelerating specialty channel access.

December 2024 – Aloecorp Inc. acquired the aloe vera division of Pharmachem Innovations and added a third processing facility in Mexico, increasing ingredient production capacity and strengthening supply-chain resilience.

This report provides comprehensive coverage of the Aloe Vera Juice Market across product categories, applications, end-users, technologies, and regional ecosystems. The analysis evaluates Organic, Conventional, Flavored, Concentrated, and Ready-to-Drink product segments while assessing demand across Functional Beverages, Dietary Supplements, Digestive Health Products, Sports Nutrition, Beauty and Wellness Drinks, and Nutraceutical Products. End-user assessment covers Food and Beverage Industry participants, Healthcare Sector organizations, Nutraceutical Companies, Retail Consumers, Hospitality Industry operators, and Fitness Centers. More than 40% of market activity is concentrated within functional wellness beverage applications, highlighting evolving consumption priorities.

The report further examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level operational insights. Coverage includes advanced extraction technologies, automated processing systems, digital traceability platforms, and ingredient quality management innovations. Competitive benchmarking evaluates leading manufacturers, supply-chain strategies, deployment patterns, partnership activity, and product innovation initiatives. Strategic insights support investment prioritization, expansion planning, sourcing optimization, market entry evaluation, and long-term competitive positioning through 2026–2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3670 Million |

|

Market Revenue in 2033 |

USD 7048.61 Million |

|

CAGR (2026 - 2033) |

8.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Forever Living Products, Lily of the Desert, ALO Drink, OKF Corporation, Aloe Farms Inc., Patanjali Ayurved Ltd., Herbalife Ltd., Terry Laboratories Inc., Aloe Vera Australia Pty Ltd., Dynamic Health Laboratories, Pharmachem Laboratories Inc., Houssy Global, Fruit of the Earth Inc., Real Aloe Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |