Reports

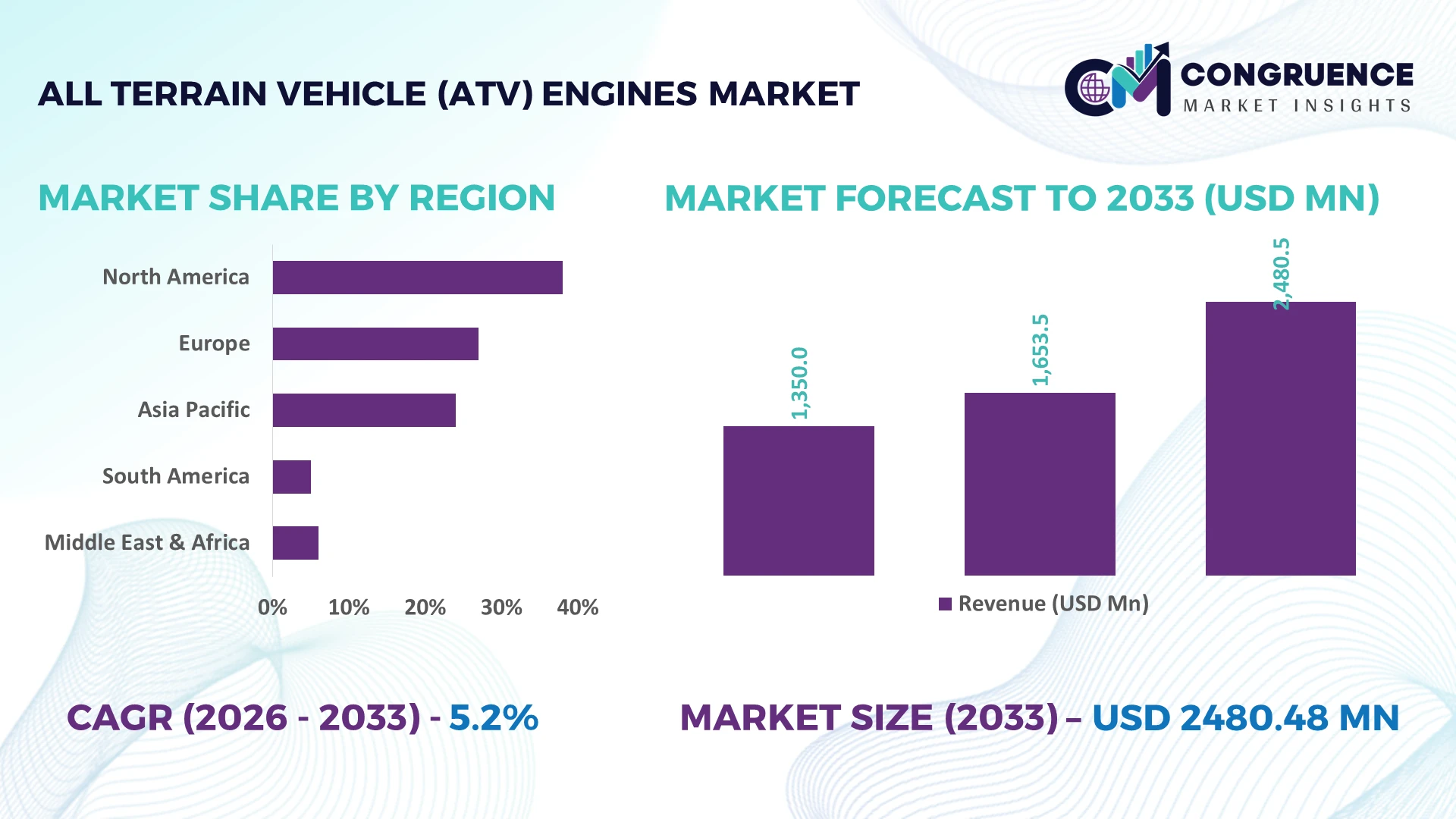

The Global All-Terrain Vehicle (ATV) Engines Market was valued at USD 1653.52 Million in 2025 and is anticipated to reach a value of USD 2480.48 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is supported by rising deployment of high-performance, fuel-efficient engines across recreational, agricultural, defense, and utility ATV platforms alongside increasing adoption of electronic fuel injection and low-emission engine technologies.

The United States leads the global All-Terrain Vehicle (ATV) Engines Market with approximately 39% production share, supported by extensive recreational vehicle usage, agricultural mechanization, and defense applications. More than 70% of newly launched premium ATV platforms integrate advanced electronic fuel injection systems, while Canada records stronger adoption in forestry operations than Mexico. North American manufacturing also benefits from regional supply-chain diversification following evolving global trade realignments in 2026.

Manufacturers strengthening localized production, advanced engine efficiency, and resilient component sourcing are positioned to secure long-term competitive advantages across high-value global markets.

Market Size & Growth: USD 1,653.52 million (2025) to USD 2,480.48 million (2033) at 5.2% CAGR, driven by advanced fuel-efficient engine integration and expanding utility vehicle production.

Top Growth Drivers: Recreational ATV demand +18%, agricultural utility adoption +14%, electronic fuel injection penetration +22% across new premium models.

Short-Term Forecast: By 2028, engine fuel efficiency improves nearly 10% while maintenance intervals extend by approximately 12% through optimized combustion systems.

Emerging Technologies: AI-assisted engine calibration, lightweight aluminum alloys, and smart electronic engine management improve durability by over 15%.

Regional Leaders: North America exceeds USD 900 million, Asia-Pacific approaches USD 760 million, and Europe surpasses USD 480 million, supported by regional manufacturing expansion and off-road fleet modernization.

Consumer/End-User Trends: Utility applications represent over 55% of new engine installations as commercial operators prioritize reliability and lower operating costs.

Pilot/Case Example: In 2026, advanced engine optimization programs delivered approximately 8% lower fuel consumption across commercial ATV fleets.

Competitive Landscape: Leading manufacturers collectively control about 48% market share, with Briggs & Stratton, Yamaha, Kawasaki, Honda, and Polaris maintaining strong global positioning.

Regulatory & ESG Impact: Low-emission engine programs reduce exhaust emissions by roughly 12%, accelerating compliance with evolving environmental standards.

Investment & Funding: More than USD 500 million supports manufacturing expansion, automation, and regional supply-chain localization initiatives.

Innovation & Future Outlook: Next-generation electronic controls, hybrid-ready architectures, and digital diagnostics strengthen performance while supporting global production resilience.

The All-Terrain Vehicle (ATV) Engines Market continues to advance through demand from agriculture, outdoor recreation, defense, and industrial utility applications. Manufacturers are introducing electronically controlled, lightweight, and lower-emission engine platforms that improve operational reliability, with fuel efficiency gains exceeding 10% in premium models. Regional component localization and evolving emissions requirements are reshaping production strategies, creating a strong foundation for the strategic market assessment that follows.

The All-Terrain Vehicle (ATV) Engines Market is becoming strategically important as manufacturers compete on engine efficiency, emissions compliance, and localized production rather than volume alone. Supply-chain restructuring since 2025 has accelerated investment in regional component sourcing, reducing procurement lead times by nearly 18% for selected engine assemblies. This transition is strengthening production continuity while enabling faster product launches for utility, agricultural, and recreational ATV segments.

Advanced electronic fuel injection systems deliver approximately 10–12% better fuel efficiency than conventional carbureted engines while reducing maintenance requirements through digital engine management. The United States maintains leadership through high-volume off-road vehicle manufacturing and extensive commercial usage, whereas Japan continues to lead in compact engine engineering and combustion optimization. Over the next two to three years, electronic engine control adoption is expected to exceed 75% of newly introduced premium ATV platforms as manufacturers standardize intelligent diagnostics and emission-ready powertrain architectures.

A growing number of fleet operators are replacing legacy utility ATVs with digitally monitored models to improve equipment availability and reduce operating downtime. Engine manufacturers are responding through targeted R&D, supplier partnerships, and localized manufacturing investments to strengthen resilience and shorten development cycles. Companies capable of combining regulatory compliance, advanced engine performance, and supply-chain flexibility will secure stronger competitive positioning across both mature and emerging off-road mobility markets.

Rising demand from agriculture, forestry, construction, and defense operations is accelerating deployment of advanced ATV engines with improved durability and fuel efficiency. More than 60% of commercial ATV purchases now prioritize utility applications, while electronic fuel injection adoption has exceeded 70% in premium engine platforms. In the United States, expanding mechanized farm operations continue to increase demand for reliable off-road equipment. Manufacturers are responding through localized engine production, lightweight component innovation, and strategic supplier partnerships that reduce logistics exposure. This structural shift enables faster product development, improves operational reliability, and strengthens long-term competitiveness in professional off-road equipment markets where uptime directly influences customer purchasing decisions.

Persistent volatility in aluminum alloys, electronic control modules, and precision engine components continues to pressure manufacturing economics. Raw material costs have fluctuated by approximately 15% over recent procurement cycles, while semiconductor-related engine electronics still experience lead-time variations exceeding 20% for selected suppliers. China remains a critical source for multiple engine components, increasing supply concentration risks during trade or logistics disruptions. Manufacturers are mitigating these pressures by diversifying supplier networks, increasing localized sourcing, and negotiating long-term procurement agreements. Companies with resilient sourcing strategies are better positioned to maintain production schedules, protect operating margins, and improve delivery consistency despite ongoing global supply-chain uncertainty.

Digital engine management, predictive diagnostics, and lightweight combustion technologies are creating differentiated opportunities beyond traditional recreational ATV demand. Intelligent engine control systems improve fuel efficiency by approximately 12%, while predictive maintenance reduces unexpected service events by nearly 20%. India is witnessing stronger adoption of utility ATVs across agriculture and industrial estates, supported by increasing mechanization initiatives. Manufacturers are expanding R&D programs, collaborating with electronics suppliers, and integrating connected diagnostics into next-generation engines. A significant strategic opportunity lies in combining durable powertrains with digital service ecosystems, allowing companies to generate recurring aftermarket value while improving fleet productivity and customer retention.

Developing high-performance engines that consistently satisfy varying emissions standards, operating environments, and customer expectations remains a complex execution challenge. Calibration complexity has increased by nearly 25% with advanced electronic control integration, while engineering validation cycles require approximately 15% more testing across diverse terrains. Japan and the United States continue to raise performance expectations for durability, emissions, and reliability simultaneously. Manufacturers must expand testing infrastructure, strengthen software engineering capabilities, and invest in advanced simulation technologies to maintain consistent product quality. Organizations that successfully integrate hardware engineering, digital calibration, and robust validation processes will establish stronger long-term operational resilience and sustainable competitive differentiation.

Advanced Engine Control Integration Electronic engine control units and smart fuel injection systems are becoming standard across premium ATV platforms, with installation rates exceeding 70% and fuel efficiency improving by 10–12%. Stricter emissions requirements in the United States are accelerating deployment, prompting manufacturers to expand software engineering capabilities and integrate predictive diagnostics to reduce maintenance frequency and improve operational uptime.

Localized Component Manufacturing Expansion Supply-chain restructuring has encouraged engine producers to increase domestic sourcing, reducing logistics lead times by nearly 18% while lowering inventory exposure by approximately 15%. Japanese and North American manufacturers are expanding strategic supplier partnerships and regional machining capacity, enabling faster production scheduling, improved quality consistency, and greater resilience against component shortages affecting precision engine assemblies.

Lightweight Materials Gain Priority High-strength aluminum alloys and advanced composite engine components now reduce engine weight by nearly 8% while improving thermal efficiency by approximately 6%. Manufacturers are redesigning engine architectures to enhance power-to-weight performance without increasing fuel consumption. This transition supports commercial fleet productivity and creates a competitive advantage through lower operating costs and extended equipment service intervals.

Digital Fleet Maintenance Adoption Connected engine monitoring platforms are reducing unexpected downtime by around 20% while improving maintenance planning accuracy by nearly 25%. Commercial operators increasingly require real-time engine diagnostics to optimize asset utilization. Companies are responding through cloud-enabled service platforms, dealer partnerships, and integrated maintenance analytics, creating stronger aftermarket relationships and improving long-term customer retention beyond traditional engine sales.

Single-Cylinder Engines remain the dominant segment, accounting for approximately 56% of engine installations due to their compact design, lower manufacturing cost, and suitability for utility and recreational ATVs. Their simplified architecture supports easier maintenance and dependable performance across agriculture and off-road applications. Gasoline Engines continue to dominate overall propulsion because of established refueling infrastructure and strong compatibility with existing vehicle platforms. Diesel Engines maintain a niche position in heavy-duty utility operations where high torque and long operating hours remain essential. Manufacturers continue refining combustion efficiency and lightweight engine designs to strengthen competitiveness in mature product categories.

Electric Motors represent the fastest-growing segment as manufacturers expand zero-emission product portfolios and integrate advanced battery management technologies. Adoption has increased by nearly 24% across newly introduced specialty ATV platforms, while Twin-Cylinder Engines are gaining momentum in premium sports and performance-oriented vehicles, delivering approximately 18% higher power output than comparable single-cylinder alternatives. Companies are increasing investment in modular powertrain development, strategic technology partnerships, and flexible manufacturing to address evolving customer preferences and future regulatory requirements.

Utility ATVs remain the largest application segment, representing approximately 48% of engine demand because of widespread deployment across agriculture, forestry, construction, and property maintenance. Fleet operators prioritize durability, towing capability, and fuel efficiency, making utility-focused engine platforms the preferred choice for commercial users. Sports ATVs maintain strong demand among performance enthusiasts, while Recreation continues benefiting from organized outdoor activities and expanding trail infrastructure. Manufacturers are optimizing engine calibration and durability to satisfy intensive daily operating conditions across professional applications.

Agriculture is the fastest-growing application as farm mechanization and precision land management increase demand for reliable off-road mobility solutions. Engine installations supporting agricultural operations have expanded by nearly 16%, while digitally managed utility fleets report maintenance efficiency improvements approaching 14%. Military applications are also advancing through procurement of rugged mobility platforms designed for surveillance and logistics support. Companies are expanding dealer networks, introducing application-specific engine configurations, and strengthening partnerships with OEMs to address specialized operational requirements across multiple industry verticals.

Agriculture remains the largest end-user segment, contributing roughly 42% of engine demand as mechanized farming, livestock management, and field transportation require dependable off-road equipment. High equipment utilization and seasonal workload intensity encourage investment in durable, fuel-efficient engine platforms. Forestry and Recreation continue generating stable replacement demand, while Defense organizations prioritize reliable powertrains capable of operating across challenging terrain under diverse environmental conditions. Manufacturers are responding with application-specific engine tuning, extended service intervals, and enhanced durability testing to strengthen customer value.

Commercial Fleet is the fastest-growing end-user segment as rental operators, industrial facilities, and utility service providers standardize connected fleet management. Fleet utilization has increased by approximately 19%, while predictive maintenance systems reduce unplanned downtime by nearly 20%. Companies are introducing customized service agreements, digital diagnostics, and volume-based procurement programs to strengthen long-term customer relationships. This strategic focus is gradually shifting competition beyond engine performance toward lifecycle cost optimization and integrated aftermarket support.

North America accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.4% CAGR between 2026 and 2033.

Advanced Manufacturing and Utility Deployment Drive Regional Leadership

North America remains the leading production and consumption hub for ATV engines, supported by established OEM manufacturing, extensive off-road infrastructure, and high commercial fleet utilization. The region contributes nearly 42% of global demand, with utility and agricultural applications representing more than 55% of annual engine installations. Manufacturers continue expanding localized component sourcing and automated machining operations, reducing selected production lead times by approximately 18%. Advanced electronic fuel injection and digital engine diagnostics are now integrated across most premium product lines, enabling higher equipment availability and lower lifecycle maintenance costs. Strategic partnerships between engine manufacturers and OEMs continue to strengthen regional supply resilience and accelerate next-generation engine development.

United States Market Outlook: The United States maintains the strongest competitive position through its large off-road vehicle manufacturing ecosystem, extensive agricultural equipment deployment, and mature dealer network. Commercial operators increasingly prioritize electronically managed engines capable of supporting predictive maintenance and emissions compliance. More than 70% of newly introduced premium ATV models incorporate advanced electronic fuel injection, while domestic manufacturers continue investing in localized production capacity and supplier diversification to improve operational resilience and reduce procurement risks.

Emission Compliance Reshapes Product Development

Europe is advancing through stricter emissions standards, engineering innovation, and growing demand for utility-focused off-road equipment. The region represents approximately 24% of global market activity, with manufacturers emphasizing lightweight engine construction, combustion optimization, and digital engine management. Investments in precision manufacturing and advanced testing facilities have improved engine development efficiency by nearly 14%. Commercial forestry, municipal services, and agricultural modernization continue supporting stable demand, while OEMs prioritize modular engine platforms capable of meeting evolving regulatory requirements without compromising durability or operational performance.

Germany Market Outlook: Germany serves as the region's engineering and manufacturing center, supported by advanced precision machining, powertrain development expertise, and industrial automation capabilities. Domestic suppliers continue investing in digitally controlled production systems, improving manufacturing productivity by approximately 12%. Strong collaboration between component manufacturers and vehicle OEMs accelerates innovation in efficient engine architectures while reinforcing Germany's leadership in premium off-road powertrain engineering.

Manufacturing Scale and Export Expansion Accelerate Adoption

Asia-Pacific continues strengthening its competitive position through large-scale manufacturing capacity, expanding industrial supply chains, and increasing domestic demand for utility vehicles. The region accounts for roughly 30% of global engine production, supported by cost-efficient manufacturing and growing investment in advanced machining technologies. Production automation has improved factory productivity by nearly 16%, while export-oriented manufacturers continue expanding component localization to improve delivery reliability. Increasing agricultural mechanization and industrial development are encouraging broader deployment of durable and fuel-efficient ATV engine platforms throughout developing economies.

Japan Market Outlook: Japan remains the regional technology leader due to its globally recognized engine engineering capabilities and continuous investment in combustion efficiency. Premium manufacturers integrate advanced electronic control systems across most new engine platforms, delivering measurable gains in fuel economy and operational reliability. High research intensity and established supplier ecosystems enable Japanese companies to commercialize next-generation powertrain technologies faster than many competing manufacturing markets.

Agricultural Expansion Supports Market Development

South America is experiencing steady demand driven by agricultural modernization, mining activities, and expanding rural transportation requirements. The region contributes approximately 7% of global market demand, with utility applications accounting for the majority of new engine installations. Mechanized farming projects have increased ATV deployment by nearly 13% in selected agricultural zones, although infrastructure limitations continue affecting distribution efficiency. Manufacturers are expanding dealer partnerships and strengthening regional service networks to improve aftermarket support and enhance equipment availability across remote operating environments.

Brazil Market Outlook: Brazil represents the largest national market due to its extensive agricultural production, mining sector, and expanding commercial equipment fleet. Demand remains concentrated in utility-oriented applications where durability and fuel efficiency are operational priorities. Equipment suppliers continue increasing localized assembly and technical service capabilities, while larger agricultural enterprises are adopting connected fleet maintenance systems to improve equipment utilization and reduce operating interruptions.

Infrastructure Investment Expands Specialized Applications

The Middle East & Africa market is progressing through infrastructure development, industrial diversification, and increased deployment of specialized off-road vehicles across construction, mining, and security operations. The region contributes close to 5% of global demand, with infrastructure modernization projects supporting higher utilization of utility ATV platforms. Fleet expansion initiatives have increased equipment deployment by approximately 11% across selected industrial projects. Manufacturers are strengthening distributor partnerships and regional service capabilities to improve product availability while addressing challenging operating environments and maintenance requirements.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through infrastructure expansion, industrial development, and large-scale construction activity. Utility and security applications continue driving procurement of durable engine platforms capable of operating in harsh climatic conditions. Industrial operators are increasingly specifying advanced engine management systems to improve equipment reliability, while suppliers continue expanding technical service infrastructure and localized inventory management to enhance operational responsiveness.

The All-Terrain Vehicle (ATV) Engines Market is led by Honda Motor, Yamaha Motor, Kawasaki Motors, Briggs & Stratton, and Kohler, with the top five companies collectively controlling approximately 58% of global market activity. Global engine specialists compete against regional manufacturers on technology integration, while OEM-aligned suppliers challenge independent engine producers through customized powertrain solutions. Competition is driven by electronic fuel injection, lightweight materials, and localized manufacturing, with advanced engine platforms delivering nearly 12% higher fuel efficiency and reducing maintenance requirements by approximately 15%. Manufacturers are expanding production facilities, strengthening supplier partnerships, and increasing vertical integration to secure critical electronic and precision-machined components. The competitive landscape is shifting toward digitally managed engines, predictive diagnostics, and modular powertrain architectures rather than conventional mechanical upgrades alone. High engineering investment, stringent emissions compliance, and complex supplier qualification remain significant entry barriers for new participants. Winning requires scalable manufacturing, resilient supply chains, rapid product innovation, and application-specific engine customization that consistently delivers superior lifecycle performance.

Honda Motor Co., Ltd.

Yamaha Motor Co., Ltd.

Kawasaki Motors, Ltd.

Briggs & Stratton LLC

Kohler Co.

Suzuki Motor Corporation

CFMOTO

Loncin Motor Co., Ltd.

Lifan Technology Group Co., Ltd.

Kubota Corporation

Yanmar Holdings Co., Ltd.

Chongqing Zongshen Power Machinery Co., Ltd.

Electronic fuel injection, intelligent engine control units, and digital calibration have become the primary technologies shaping competitive differentiation. Compared with legacy carbureted systems, modern electronic fuel injection improves fuel efficiency by approximately 10–12% while reducing cold-start failures by nearly 20%. More than 70% of premium ATV engine platforms now incorporate digitally controlled combustion management, allowing manufacturers to meet stricter emissions requirements while improving throttle response and operational consistency across demanding off-road environments.

Emerging technologies include predictive diagnostics, lightweight aluminum engine blocks, cloud-enabled maintenance platforms, and AI-assisted calibration tools. Lightweight materials reduce engine weight by approximately 8%, while predictive maintenance lowers unexpected downtime by nearly 20% through continuous performance monitoring. OEMs and leading engine manufacturers benefit most from these technologies because integrated software, electronics, and mechanical engineering create stronger aftermarket service opportunities and higher customer retention. Companies are expanding strategic collaborations with electronics suppliers and investing in modular engine architectures to accelerate deployment.

Between 2026 and 2028, hybrid-ready powertrain platforms, connected diagnostics, and advanced thermal management will become major competitive differentiators. Adoption of intelligent engine monitoring is expected to exceed 75% across newly introduced premium models. Companies acting now through software integration, manufacturing automation, and digital engineering will strengthen operational efficiency, shorten development cycles, and secure long-term competitive advantages as performance, emissions compliance, and lifecycle optimization become the industry's defining purchasing criteria.

August 2024 Yamaha Motor introduced its 2025 Proven Off-Road ATV lineup featuring the 700-class Grizzly engine, assembled at its Newnan, Georgia facility for global markets. The expansion reinforced North American manufacturing capacity and strengthened supply continuity for utility and recreational applications.

November 2024 Honda unveiled the world's first motorcycle V3 engine with an electrically driven compressor at EICMA 2024, delivering responsive torque independent of engine rpm. The breakthrough advanced compact engine technology with future relevance for high-performance off-road powertrain development. Source: (Honda公式サイト)

September 2025 Yamaha Motor announced its 2026 ATV lineup, with every full-size ATV manufactured in Newnan, Georgia for global distribution. The portfolio retained advanced fuel injection across utility models, strengthening production localization and premium off-road product competitiveness.

April 2026 Yamaha Motor launched the GRIZZLY 110 for the domestic market with a 112 cm³ fuel-injected four-stroke engine and CVT transmission. The new youth-oriented platform expanded the company's ATV portfolio while improving ease of operation and long-term maintenance efficiency. Source: (Yamaha Motor Global Site)

The report delivers comprehensive analysis across engine types, including Single-Cylinder Engines, Twin-Cylinder Engines, Gasoline Engines, Diesel Engines, and Electric Motors, together with applications spanning Utility ATVs, Sports ATVs, Recreation, Agriculture, and Military. It also evaluates demand across Agriculture, Forestry, Defense, Recreation, and Commercial Fleet end-users while assessing competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 70% of premium platforms now integrate advanced electronic engine management, highlighting the accelerating transition toward digitally controlled powertrains.

The assessment combines technology benchmarking, regional deployment trends, competitive landscape evaluation, and operational analysis between 2026 and 2033. It examines manufacturing strategies, supply-chain localization, emissions-compliant engine technologies, aftermarket opportunities, and evolving customer requirements. The report supports investment prioritization, market entry planning, product portfolio optimization, partnership evaluation, and long-term competitive positioning by identifying high-potential segments, emerging technology pathways, and operational shifts influencing future industry direction.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1653.52 Million |

Market Revenue in 2033 | USD 2480.48 Million |

CAGR (2026 - 2033) | 5.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Honda Motor Co., Ltd., Yamaha Motor Co., Ltd., Kawasaki Motors, Ltd., Briggs & Stratton LLC, Kohler Co., Suzuki Motor Corporation, CFMOTO, Loncin Motor Co., Ltd., Lifan Technology Group Co., Ltd., Kubota Corporation, Yanmar Holdings Co., Ltd., Chongqing Zongshen Power Machinery Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |