Reports

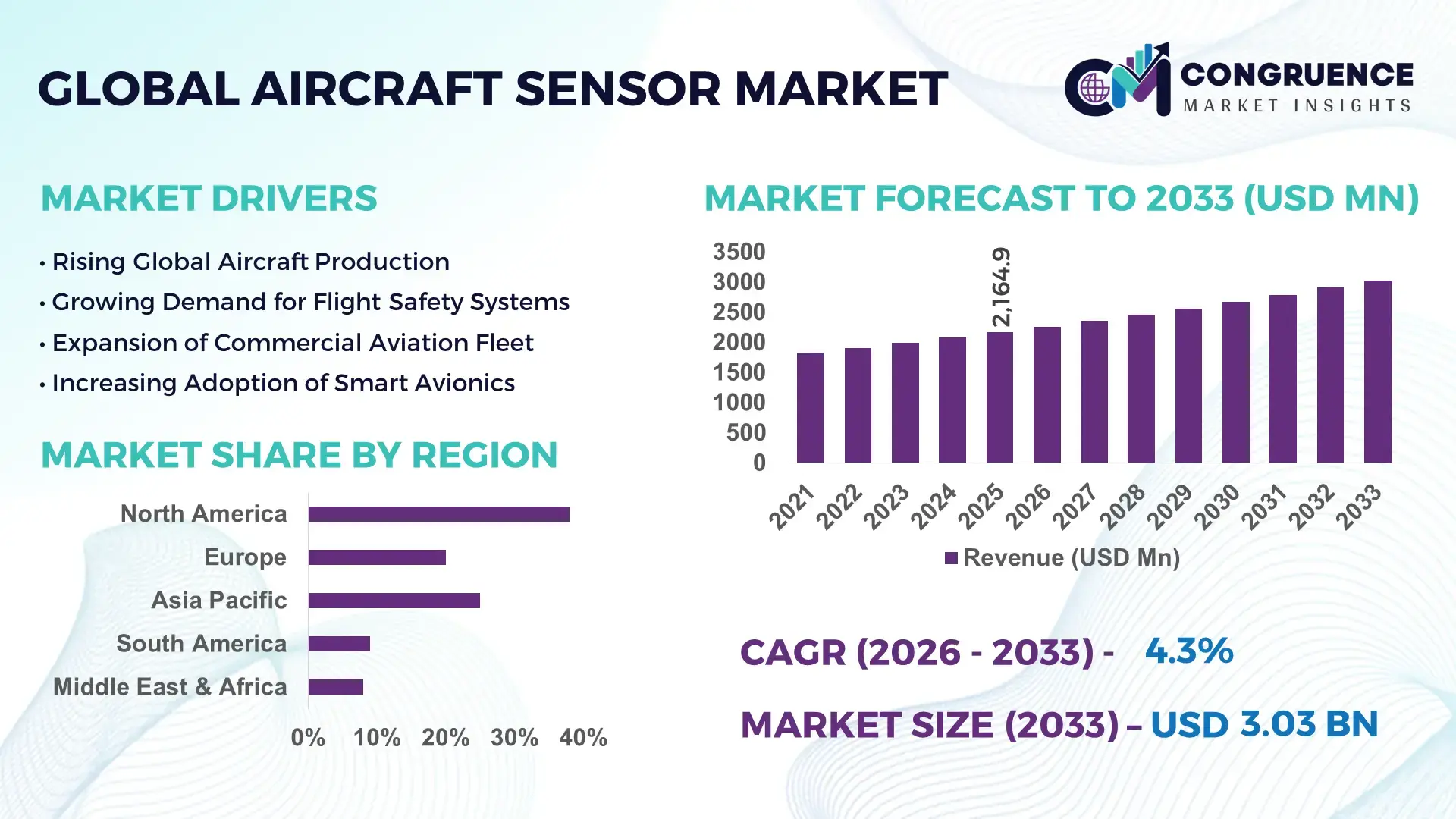

The Global Aircraft Sensor Market was valued at USD 2,164.92 Million in 2025 and is anticipated to reach a value of USD 3,031.92 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. The growth is primarily driven by increasing aircraft production, modernization of defense fleets, and rising adoption of advanced avionics and predictive maintenance technologies across global aviation networks.

The United States remains a central hub for aircraft sensor development and integration due to its extensive aerospace manufacturing ecosystem and advanced aviation technology infrastructure. The country operates more than 220,000 registered aircraft across commercial, military, and private fleets, creating substantial demand for high-performance sensors in flight control, propulsion monitoring, and environmental systems. U.S. aerospace programs such as advanced fighter jet development and next-generation unmanned aerial vehicles are accelerating investments in MEMS-based sensors, radar systems, and infrared sensing technologies. In addition, the country’s commercial aviation sector operates thousands of aircraft, requiring continuous sensor upgrades for engine diagnostics, cabin monitoring, and predictive maintenance systems across large airline fleets.

• Market Size & Growth: The Aircraft Sensor Market reached USD 2164.92 Million in 2025 and is projected to reach USD 3031.92 Million by 2033, expanding at a CAGR of 4.3%, supported by rapid aircraft fleet expansion and increased deployment of smart monitoring systems.

• Top Growth Drivers: Aircraft production growth 18%, predictive maintenance adoption 25%, and UAV deployment expansion 30%.

• Short-Term Forecast: By 2028, digital aircraft health monitoring systems are expected to improve maintenance efficiency by 20% and reduce operational downtime by nearly 15%.

• Emerging Technologies: Integration of MEMS-based sensors, AI-driven predictive analytics, fiber-optic sensing systems, and IoT-enabled avionics monitoring platforms.

• Regional Leaders: North America projected to reach USD 1.2 Billion by 2033 due to strong aerospace manufacturing; Europe expected to reach USD 0.9 Billion driven by aviation safety upgrades; Asia-Pacific forecast to reach USD 0.7 Billion supported by rapid airline fleet expansion.

• Consumer/End-User Trends: Commercial airlines account for approximately 45% of sensor installations, followed by defense aviation at nearly 35%, with growing adoption across UAV platforms and advanced air mobility aircraft.

• Pilot or Case Example: In 2024, a predictive maintenance program implemented in a North American airline fleet reduced unscheduled maintenance events by 22% through real-time aircraft sensor data monitoring.

• Competitive Landscape: Honeywell holds approximately 18% share of advanced aircraft sensor supply, followed by major competitors such as Safran, TE Connectivity, AMETEK, and Collins Aerospace.

• Regulatory & ESG Impact: Aviation regulators are mandating stricter aircraft health monitoring systems and encouraging technologies capable of reducing fuel consumption and emissions by up to 10%.

• Investment & Funding Patterns: Global aerospace sensor R&D investments exceeded USD 1.4 Billion in recent years, with significant funding directed toward autonomous aircraft sensing technologies and digital avionics platforms.

• Innovation & Future Outlook: Continuous innovation in smart sensors, wireless avionics, and integrated aircraft diagnostics platforms is expected to transform aircraft safety monitoring, predictive maintenance, and autonomous aviation capabilities.

Aircraft sensor systems play a critical role in multiple aviation segments including engine monitoring, flight control systems, landing gear operations, and environmental management. Engine and propulsion monitoring applications contribute nearly 35% of overall demand due to the need for continuous temperature, pressure, and vibration measurements in modern aircraft. Pressure sensors account for nearly 29% of installed sensor types, while temperature and position sensors remain widely used in avionics and structural monitoring systems. The market is also witnessing rapid innovation in fiber-optic sensing, wireless avionics sensor networks, and lightweight MEMS sensors that enable real-time aircraft diagnostics. Regulatory safety requirements, increasing air passenger traffic, and growing adoption of unmanned aerial vehicles are strengthening demand for high-precision sensors in commercial aviation, defense aircraft, and next-generation electric aircraft platforms.

The Aircraft Sensor Market holds strategic relevance within the global aerospace ecosystem as aviation operators increasingly rely on real-time data monitoring to improve safety, reduce maintenance costs, and enhance aircraft performance. Modern aircraft incorporate more than 2,000 sensors across avionics, propulsion, and environmental monitoring systems, enabling continuous data collection for flight diagnostics and operational optimization. Advanced MEMS-based sensors deliver nearly 30% improvement in data accuracy compared to traditional electromechanical sensors, allowing airlines and defense operators to monitor critical systems with greater precision and reliability. North America dominates the Aircraft Sensor Market in terms of production volume due to its extensive aircraft manufacturing base and advanced aerospace supply chain, while Asia-Pacific leads in adoption growth with over 40% of new commercial aircraft deliveries expected in the region over the next decade. The expansion of low-cost carriers and regional aviation infrastructure is accelerating sensor installations across newly manufactured aircraft fleets.

By 2028, artificial intelligence-driven predictive maintenance systems are expected to reduce aircraft maintenance costs by nearly 25% through automated diagnostics and sensor-based performance monitoring. Aviation manufacturers are also integrating digital twin technology that allows real-time analysis of aircraft sensor data to optimize performance and safety. Environmental and regulatory compliance is shaping the industry as well. Aerospace manufacturers are committing to sustainability targets including a 20% reduction in aviation emissions by 2035 through improved engine monitoring and fuel efficiency enabled by advanced sensor technologies. In 2024, a European aircraft manufacturer implemented an AI-powered sensor analytics platform that improved engine efficiency by 12% across a test fleet.

The growing global aircraft fleet is one of the most significant drivers of the Aircraft Sensor Market. Commercial aviation demand continues to expand as passenger traffic increases and airlines invest in modern aircraft capable of higher fuel efficiency and improved operational performance. A single commercial aircraft can contain more than 2,000 sensors monitoring parameters such as temperature, pressure, vibration, and altitude, making sensors essential for aircraft safety and performance monitoring. Global airlines have placed thousands of aircraft orders to replace aging fleets and support increasing travel demand, particularly in Asia-Pacific and the Middle East. Defense aviation is also contributing to sensor demand as military aircraft modernization programs integrate advanced radar, infrared, and navigation sensors to enhance mission capability. Additionally, the rapid expansion of unmanned aerial vehicles in surveillance, defense, and logistics operations is creating additional demand for lightweight MEMS sensors capable of delivering real-time flight data.

Despite strong demand, the Aircraft Sensor Market faces significant restraints due to the high costs associated with sensor development, certification, and integration within aviation systems. Aircraft sensors must comply with strict aviation safety and reliability standards before deployment, often requiring extensive testing, validation, and regulatory approval processes. The certification of a new aerospace sensor can take several years due to rigorous environmental and operational testing under extreme conditions including high temperatures, vibration, and altitude variations. In addition, advanced sensor technologies often rely on specialized aerospace-grade semiconductors and precision manufacturing processes that increase production costs. Supply chain disruptions and semiconductor shortages have also affected the availability of critical sensor components used in avionics systems. These factors can delay product launches and increase integration costs for aircraft manufacturers and airlines adopting next-generation sensor technologies.

Emerging aviation technologies such as autonomous aircraft, electric propulsion systems, and advanced air mobility platforms are creating new opportunities for the Aircraft Sensor Market. Autonomous flight systems rely heavily on advanced sensing technologies including lidar, radar, inertial measurement units, and environmental monitoring sensors to enable safe navigation and obstacle detection. Urban air mobility aircraft and electric vertical takeoff and landing vehicles require highly integrated sensor networks capable of supporting automated flight control systems. Industry forecasts suggest that thousands of electric aircraft and air taxi vehicles could enter commercial service within the next decade, each requiring complex sensor architectures to monitor propulsion systems, battery performance, and flight conditions. Additionally, aerospace companies are developing smart sensor networks connected to cloud-based analytics platforms, allowing aircraft operators to analyze flight data in real time and optimize maintenance schedules.

The integration of advanced sensors into modern aircraft platforms presents technical and operational challenges that affect the Aircraft Sensor Market. Modern aircraft increasingly rely on interconnected avionics systems that process large volumes of sensor data in real time. Integrating hundreds or thousands of sensors into a unified aircraft monitoring system requires highly reliable data processing infrastructure and advanced avionics software. As aircraft become more digitally connected, cybersecurity risks are also increasing. Sensor networks connected to aircraft data systems can become potential entry points for cyber threats if not properly secured. Aviation regulators are therefore enforcing strict cybersecurity standards for avionics and onboard data systems. Additionally, integrating new sensors into existing aircraft fleets during retrofit programs can be technically complex and costly, requiring modifications to wiring systems, avionics architecture, and aircraft certification processes. These factors create operational challenges for airlines and aerospace manufacturers adopting next-generation aircraft sensing technologies.

• Expansion of MEMS Sensor Integration Across Aircraft Platforms:

Micro-Electro-Mechanical Systems (MEMS) sensors are increasingly deployed across commercial and defense aircraft due to their compact size, precision, and reliability. Over 65% of newly manufactured aircraft platforms now incorporate MEMS-based pressure, acceleration, and inertial sensors. Modern jetliners typically integrate more than 1,800 sensing components for monitoring flight dynamics, engine performance, and cabin conditions. MEMS sensors reduce system weight by nearly 20% compared with traditional electromechanical alternatives, contributing to improved fuel efficiency and enhanced aircraft diagnostics capabilities.

• Surge in Predictive Maintenance Using Real-Time Sensor Data:

Predictive maintenance systems supported by aircraft sensors are transforming aviation operations. Approximately 72% of major airlines have integrated sensor-driven health monitoring platforms into their fleets. These systems analyze thousands of operational parameters in real time, enabling operators to detect early signs of component wear. Predictive maintenance technologies have reduced unscheduled aircraft maintenance events by nearly 25% and improved fleet operational availability by more than 18%, helping airlines optimize maintenance schedules and minimize operational disruptions.

• Growth of Sensor Networks in Unmanned and Autonomous Aircraft:

The rapid expansion of unmanned aerial vehicles (UAVs) and autonomous flight technologies is significantly increasing demand for advanced aircraft sensors. More than 45% of newly developed UAV platforms utilize integrated sensor networks combining radar, lidar, and inertial measurement units for navigation and obstacle detection. Autonomous flight testing programs have shown that advanced sensor fusion systems can improve navigation accuracy by nearly 30% while enabling automated flight decision-making in complex airspace environments.

• Rising Deployment of Fiber-Optic and Wireless Sensor Systems:

Next-generation aircraft are adopting fiber-optic sensing and wireless sensor networks to improve structural monitoring and data transmission efficiency. Fiber-optic sensors are capable of detecting structural strain changes as small as 1 microstrain and are now used in approximately 28% of newly designed composite aircraft structures. Wireless avionics sensor networks have demonstrated a 35% reduction in aircraft wiring complexity, enabling faster installation, lighter aircraft structures, and more efficient onboard data management systems.

The Aircraft Sensor Market is segmented based on type, application, and end-user industries, reflecting the diverse operational requirements across aviation systems. Sensor types include pressure, temperature, position, speed, and vibration sensors, each designed to monitor specific aircraft components and operational conditions. Applications range from engine monitoring and flight control systems to environmental control and structural health monitoring. Commercial aviation currently represents the largest application segment due to extensive fleet operations and safety monitoring requirements. End-users include aircraft manufacturers, airlines, defense organizations, and maintenance service providers. Increasing aircraft automation and digital avionics integration are further shaping demand across these segments.

Pressure sensors currently represent the leading product type within the Aircraft Sensor Market, accounting for nearly 29% of total sensor installations. These sensors are critical for monitoring cabin pressurization, hydraulic systems, and fuel management operations, making them indispensable for safe aircraft performance. Temperature sensors follow closely with approximately 22% adoption across aviation systems, particularly for engine monitoring and environmental control. Position sensors account for around 18% of the installed sensor base and play a crucial role in monitoring landing gear, flight control surfaces, and throttle positions. Vibration sensors are emerging as the fastest-growing sensor category with an estimated growth rate of approximately 7.2% annually. Their expansion is driven by increasing adoption of predictive maintenance technologies that rely on vibration monitoring to detect early mechanical faults in engines, turbines, and structural components. Speed sensors also play an essential role in aircraft propulsion and navigation systems. Collectively, these remaining sensor types represent nearly 31% of the total market landscape, supporting specialized aviation functions such as turbine monitoring and airflow measurement.

Engine and propulsion monitoring remains the leading application segment within the Aircraft Sensor Market, accounting for approximately 35% of total sensor deployments. Aircraft engines operate under extreme temperature and pressure conditions, requiring continuous monitoring of multiple parameters including fuel flow, vibration, and thermal performance. Flight control systems represent the second-largest application area with nearly 24% adoption, as modern aircraft rely on highly accurate sensor data to manage wing flaps, rudders, and stabilizers during flight operations. Structural health monitoring is currently the fastest-growing application segment, expanding at an estimated rate of 7.5% annually as airlines adopt advanced sensing systems to monitor aircraft structural integrity in real time. Environmental control systems account for approximately 16% of sensor applications, measuring cabin pressure, humidity, and air quality to ensure passenger comfort and safety. Other applications such as landing gear monitoring and avionics diagnostics collectively represent nearly 25% of the overall application landscape.

Commercial aviation currently represents the largest end-user segment in the Aircraft Sensor Market, accounting for approximately 45% of total sensor demand. Large airline fleets rely heavily on integrated sensor systems to monitor aircraft performance, optimize maintenance cycles, and ensure operational safety. Defense and military aviation accounts for nearly 35% of the market, where advanced sensors support navigation systems, radar technologies, and mission-critical surveillance platforms. Unmanned aerial vehicle operators represent the fastest-growing end-user category, expanding at an estimated rate of approximately 8.1% annually. Increasing use of UAVs in surveillance, border security, logistics, and environmental monitoring is driving demand for compact sensors capable of supporting autonomous flight operations. Aircraft manufacturers and maintenance service providers collectively account for approximately 20% of the remaining market demand, supplying sensors for both new aircraft production and retrofit programs.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

North America’s strong aerospace manufacturing base supports over 7,000 commercial aircraft and thousands of defense platforms requiring continuous sensor integration for avionics, engine monitoring, and structural diagnostics. Europe holds approximately 27% of the global Aircraft Sensor Market, driven by advanced aircraft manufacturing programs and strong aviation safety standards across the region. Asia-Pacific accounts for nearly 24% of the market and is witnessing rapid aircraft fleet expansion with more than 17,000 new aircraft expected to be delivered in the coming decades. South America contributes nearly 6% of the global demand, primarily supported by regional aviation modernization programs and increasing airline fleet upgrades. The Middle East & Africa region represents about 5% of the Aircraft Sensor Market, with strong demand driven by expanding airline fleets, large-scale airport infrastructure projects, and increasing investments in aerospace maintenance and engineering services.

How Are Advanced Aerospace Technologies Accelerating Sensor Adoption Across Aviation Systems?

North America accounts for nearly 38% of the global Aircraft Sensor Market volume, supported by the region’s strong aerospace manufacturing industry and advanced aviation technology ecosystem. Commercial aviation, defense aircraft manufacturing, and unmanned aerial vehicle development are the key industries driving sensor demand. The region hosts more than 220,000 registered aircraft, creating continuous demand for advanced sensing systems in engine monitoring, flight control systems, and predictive maintenance platforms. Regulatory bodies have implemented strict aircraft safety standards that encourage real-time monitoring technologies and advanced avionics integration. Technological innovation is accelerating with digital twin systems and predictive maintenance analytics deployed across major airline fleets. A leading aerospace technology provider in the region recently introduced next-generation fiber-optic sensors capable of detecting micro-structural stress variations in aircraft wings. Regional consumer behavior indicates high enterprise adoption of advanced aviation technologies, with over 70% of large airline fleets using integrated aircraft health monitoring systems.

How Are Sustainability Regulations and Aviation Safety Standards Transforming Sensor Demand?

Europe holds approximately 27% share of the Aircraft Sensor Market and remains a key hub for aircraft manufacturing and aerospace technology innovation. Major aviation markets such as Germany, the United Kingdom, and France are driving regional demand through large commercial aircraft manufacturing facilities and advanced aerospace research programs. The region’s aviation regulatory authorities enforce stringent aircraft safety and environmental standards, encouraging airlines and manufacturers to integrate high-precision sensors capable of improving engine efficiency and reducing emissions. Technological adoption is expanding through the use of fiber-optic sensors, smart avionics monitoring platforms, and advanced aircraft diagnostics systems. A major European aerospace supplier recently deployed smart vibration monitoring sensors across several commercial aircraft fleets to enhance predictive maintenance capabilities. Regional consumer behavior reflects strong regulatory pressure for transparent and explainable sensor technologies capable of supporting aviation safety compliance and environmental sustainability goals.

What Factors Are Driving Rapid Aviation Sensor Adoption Across Expanding Aircraft Fleets?

Asia-Pacific ranks as the fastest-growing region in the Aircraft Sensor Market and currently accounts for nearly 24% of global demand. Countries such as China, India, and Japan are the largest consumers of aircraft sensors due to rapid airline fleet expansion and growing domestic aviation industries. The region’s commercial aviation sector is projected to add thousands of new aircraft over the coming years, significantly increasing demand for pressure, temperature, and navigation sensors. Infrastructure expansion including new airport construction and aviation maintenance hubs is further accelerating market development. Technology innovation centers across Japan and South Korea are developing lightweight MEMS sensors designed specifically for next-generation aircraft platforms. A major aerospace manufacturer in the region has introduced advanced sensor fusion systems capable of processing over 5,000 aircraft performance parameters during flight operations. Consumer adoption trends in the region are strongly influenced by rapid digital transformation and increasing investments in smart aviation infrastructure.

How Is Aviation Infrastructure Development Creating New Sensor Deployment Opportunities?

South America represents approximately 6% of the global Aircraft Sensor Market and is primarily driven by aviation modernization programs across countries such as Brazil and Argentina. The region’s commercial aviation industry is expanding as passenger traffic increases and airlines invest in upgrading aircraft fleets with modern avionics systems. Infrastructure improvements including airport expansion projects and aircraft maintenance facilities are contributing to rising sensor installations across regional fleets. Government initiatives supporting aerospace manufacturing and aviation safety improvements are also strengthening market demand. A major aircraft manufacturer headquartered in the region continues to develop advanced sensing technologies integrated into new commercial aircraft platforms. Regional consumer behavior indicates that aviation operators are increasingly prioritizing predictive maintenance technologies and digital monitoring systems to improve aircraft operational efficiency and reduce maintenance delays across growing airline networks.

How Are Aviation Expansion and Technological Modernization Increasing Sensor Adoption?

The Middle East & Africa region accounts for roughly 5% of the global Aircraft Sensor Market and continues to expand as airline fleets grow and aviation infrastructure develops. Countries such as the United Arab Emirates and South Africa are key growth centers due to strong airline operations and increasing investments in aircraft maintenance and engineering services. The region operates some of the world’s largest international airline fleets, each requiring thousands of sensors to monitor aircraft performance and safety systems. Governments are supporting aviation expansion through new airport construction projects and aerospace technology partnerships with global manufacturers. Technological modernization initiatives are introducing advanced avionics systems and predictive maintenance platforms across regional airline fleets. Regional consumer behavior shows a strong preference for high-performance aviation technologies capable of supporting long-haul flight operations and maintaining operational reliability in demanding environmental conditions.

• United States – 34% market share: Aircraft Sensor Market growth in the United States is supported by the world’s largest aerospace manufacturing industry and extensive commercial and defense aviation fleets.

• China – 18% market share: Aircraft Sensor Market expansion in China is driven by rapid aircraft fleet expansion, strong domestic aerospace manufacturing capacity, and increasing aviation infrastructure investments.

The Aircraft Sensor Market features a moderately consolidated competitive landscape with more than 40 active global and regional manufacturers supplying specialized sensors for aviation applications. The top five companies collectively account for approximately 52% of the total market share, reflecting strong technological capabilities and established aerospace partnerships. Leading companies compete through innovation in MEMS technology, fiber-optic sensors, and advanced avionics monitoring systems capable of delivering high-precision aircraft diagnostics. Strategic initiatives such as partnerships with aircraft manufacturers, product innovation, and long-term supply contracts with airlines and defense organizations are key competitive strategies. Several companies are investing heavily in smart sensor technologies capable of supporting predictive maintenance and autonomous aircraft systems. In recent years, the industry has witnessed multiple collaborative research programs focused on developing lightweight sensors capable of monitoring more than 2,000 aircraft parameters simultaneously. Continuous innovation in wireless sensor networks, AI-driven analytics platforms, and integrated avionics systems is further intensifying competition among leading aerospace sensor manufacturers.

Honeywell International

Safran

TE Connectivity

AMETEK

Collins Aerospace

Meggitt PLC

Sensata Technologies

Curtiss-Wright Corporation

Bosch Sensortec

PCB Piezotronics

Crane Aerospace & Electronics

Technological innovation is significantly transforming the Aircraft Sensor Market as modern aircraft increasingly rely on high-precision sensing technologies to monitor thousands of operational parameters in real time. A typical commercial aircraft integrates between 1,500 and 2,000 sensors to track pressure, temperature, vibration, position, and acceleration across critical subsystems including engines, landing gear, avionics, and structural components. The rapid adoption of Micro-Electro-Mechanical Systems (MEMS) sensors is one of the most impactful technological advancements. MEMS-based sensors are up to 80% smaller and nearly 60% lighter than traditional electromechanical sensors while offering higher sensitivity and improved reliability, making them ideal for next-generation aircraft platforms.

Fiber-optic sensors are also gaining traction due to their ability to detect structural strain changes as small as 1 microstrain, enabling advanced structural health monitoring of composite aircraft structures. These sensors can be embedded within aircraft wings and fuselage sections, allowing continuous monitoring of stress distribution during flight operations. Wireless avionics sensor networks represent another emerging technology, reducing aircraft wiring by nearly 30% while improving onboard data communication efficiency.

Artificial intelligence and predictive analytics are increasingly integrated with sensor systems to enable real-time aircraft health monitoring. Advanced sensor analytics platforms can process more than 5,000 aircraft performance parameters during flight, helping airlines detect early mechanical anomalies and reduce unscheduled maintenance events by nearly 25%. Additionally, sensor fusion technologies combining radar, lidar, inertial measurement units, and satellite navigation sensors are improving navigation accuracy and supporting the development of autonomous aircraft and advanced air mobility systems.

• In January 2024, Honeywell announced that Eve Air Mobility selected its navigation, sensor, and lighting technologies for the company’s electric vertical take-off and landing aircraft. The system includes GPS-aided Attitude and Heading Reference Systems and Inertial Reference Systems designed to improve flight navigation and operational safety.

• In April 2024, Honeywell revealed the development of a lightweight resolver sensor for the Lilium Jet electric aircraft. The customized sensing technology uses magneto-resistive sensors and spiral magnet architecture to determine propulsion unit position, enabling precise engine movement control required for vertical take-off and transition to forward flight.

• In June 2025, TransDigm Group announced the acquisition of Simmonds Precision Products for approximately $765 million. The company manufactures proximity sensors, fuel sensors, and aircraft structural health monitoring systems widely used across commercial and military aircraft platforms. Source: www.reuters.com

• In July 2025, Safran finalized the acquisition of Collins Aerospace’s flight control and actuation business to strengthen its capabilities in mission-critical aircraft systems, including advanced sensing and actuation technologies used in flight control and avionics monitoring systems. Source: www.reuters.com

The Aircraft Sensor Market Report provides a comprehensive analysis of the global aerospace sensing industry, covering critical technological, operational, and application-specific aspects influencing demand across commercial, defense, and unmanned aviation sectors. The report examines more than 20 major sensor categories including pressure sensors, temperature sensors, vibration sensors, position sensors, speed sensors, and optical sensors used across aircraft systems such as engines, avionics, landing gear, environmental control units, and structural health monitoring frameworks.

The report evaluates sensor deployment across multiple aircraft platforms including narrow-body commercial jets, wide-body aircraft, military fighter jets, transport aircraft, helicopters, and unmanned aerial vehicles. A modern aircraft platform may incorporate over 2,000 sensors that monitor flight performance, fuel management systems, environmental conditions, and aircraft structural integrity. The report further explores technological advancements such as MEMS-based sensors, fiber-optic sensing systems, wireless avionics sensor networks, and AI-enabled predictive maintenance platforms capable of processing thousands of real-time operational data points during flight.

Geographically, the report covers five major regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, evaluating aircraft fleet sizes, manufacturing capacity, aviation infrastructure development, and sensor integration trends across more than 25 key aviation economies. Additionally, the report analyzes end-user demand from aircraft manufacturers, commercial airlines, military aviation programs, and maintenance service providers responsible for supporting over 30,000 active commercial aircraft worldwide. The scope also includes emerging aviation technologies such as electric aircraft, advanced air mobility platforms, and autonomous flight systems, all of which require highly sophisticated sensor architectures to support safe and efficient flight operations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell International, Safran, TE Connectivity, AMETEK, Collins Aerospace, Meggitt PLC, Sensata Technologies, Curtiss-Wright Corporation, Bosch Sensortec, PCB Piezotronics, Crane Aerospace & Electronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |