Reports

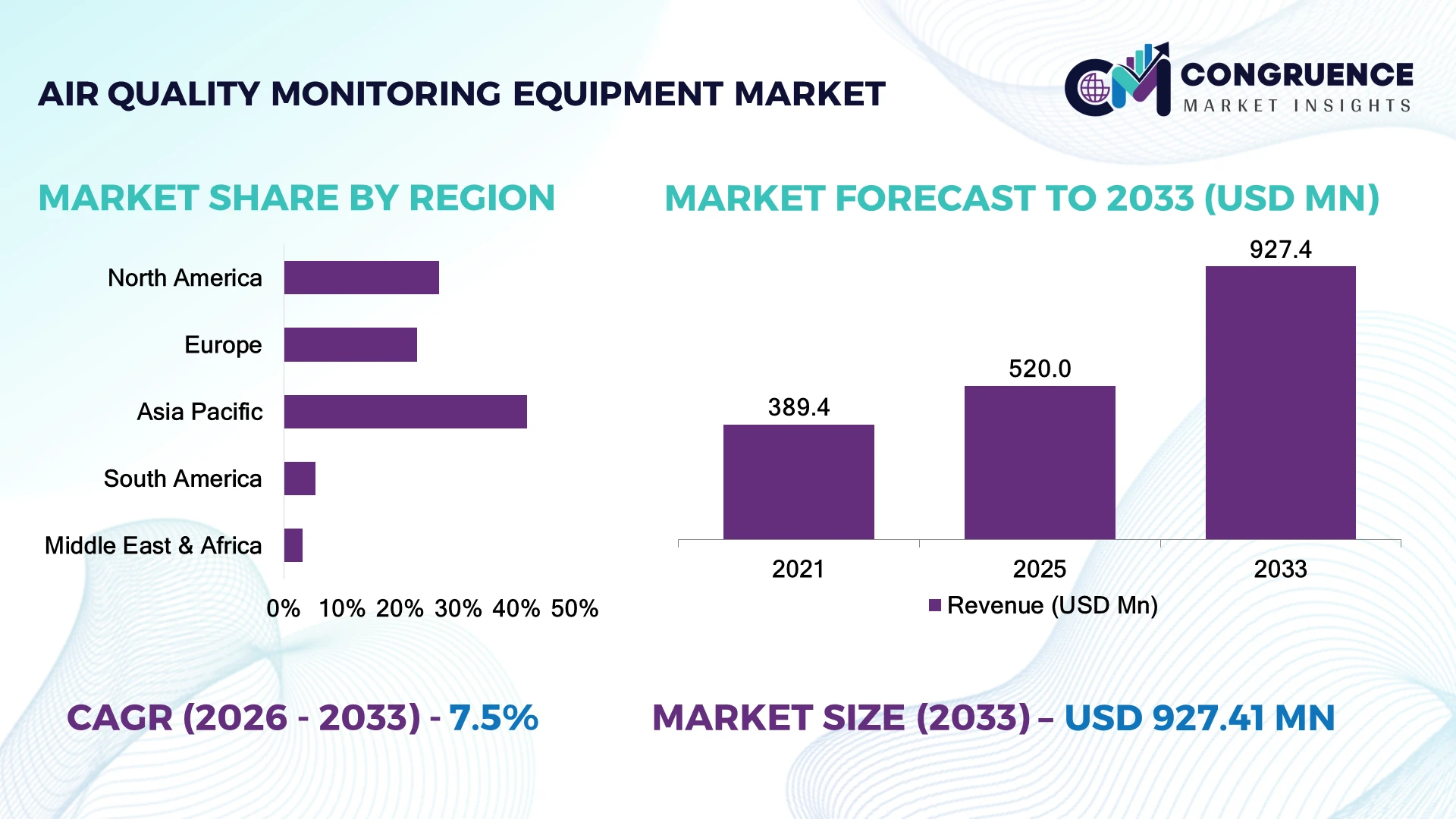

The Global Air Quality Monitoring Equipment Market was valued at USD 520.0 Million in 2025 and is anticipated to reach a value of USD 927.4 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. Stricter industrial emission regulations, expanding smart-city air monitoring networks, and continuous deployment of real-time sensor technologies are accelerating equipment installations across industrial, commercial, and public infrastructure projects.

China accounts for approximately 34% of global air quality monitoring equipment manufacturing capacity, supported by large-scale environmental investments, electronics production, and nationwide pollution control programs, while the United States leads in advanced monitoring deployments across industrial and municipal sectors with over 72% adoption in major metropolitan environmental networks. Rising clean-air initiatives following global climate commitments continue strengthening procurement priorities across developed and emerging economies.

Organizations investing in scalable, connected monitoring platforms gain stronger regulatory compliance, operational visibility, and long-term environmental intelligence.

Market Size & Growth: USD 520.0 Million in 2025, projected to reach USD 927.4 Million by 2033 at a CAGR of 7.5%, supported by smart environmental monitoring and stricter emission compliance.

Top Growth Drivers: Industrial monitoring (+31%), smart-city deployments (+28%), and environmental compliance investments (+24%) remain the primary expansion catalysts.

Short-Term Forecast: By 2028, cloud-connected monitoring systems are expected to improve operational efficiency by nearly 30% through automated data management.

Emerging Technologies: AI-powered analytics, IoT-enabled sensor networks, and edge computing are improving monitoring accuracy and predictive environmental analysis.

Regional Leaders: Asia-Pacific (~USD 350 Million), North America (~USD 235 Million), and Europe (~USD 185 Million) lead through infrastructure modernization, regulatory enforcement, and digital monitoring adoption.

Consumer/End-User Trends: More than 63% of industrial facilities prioritize continuous real-time air quality monitoring for environmental compliance and workplace safety.

Pilot/Case Example: In 2024, smart urban monitoring deployments reduced manual inspection requirements by approximately 40% through automated sensor integration.

Competitive Landscape: Leading manufacturers collectively account for nearly 38% market share, with Thermo Fisher Scientific, HORIBA, Teledyne Technologies, Siemens, and Emerson maintaining strong global positions.

Regulatory & ESG Impact: Updated air quality regulations have increased continuous emissions monitoring installations by over 27% across regulated industrial facilities.

Investment & Funding: More than USD 2.1 Billion has been invested globally in environmental monitoring infrastructure, emphasizing digital expansion and public-private partnerships.

Innovation & Future Outlook: Miniaturized sensors, AI-assisted diagnostics, and integrated cloud platforms are strengthening next-generation environmental monitoring strategies.

Air Quality Monitoring Equipment Market demand continues expanding across industrial manufacturing, urban infrastructure, healthcare facilities, and transportation networks as organizations prioritize continuous environmental intelligence. AI-enabled sensing platforms and compact multi-gas analyzers improve monitoring precision, while over 58% of newly deployed systems now support remote cloud connectivity. Growing environmental compliance requirements and resilient supply-chain localization initiatives continue accelerating deployment across emerging economies, setting the stage for broader strategic investments.

Air quality monitoring equipment has become a strategic investment priority as governments, industrial operators, and infrastructure developers strengthen environmental compliance and operational transparency. Infrastructure modernization, digital environmental management, and stricter emission standards are reshaping procurement strategies, while organizations increasingly integrate monitoring networks into broader smart-facility and industrial automation programs. Competitive differentiation now depends on delivering accurate, continuous, and connected environmental intelligence.

Modern AI-enabled monitoring platforms process environmental data approximately 45% faster than conventional standalone monitoring systems while reducing routine maintenance requirements by nearly 30% through predictive diagnostics and remote system management. Asia-Pacific continues leading large-scale manufacturing and deployment volumes, whereas North America focuses on advanced analytics, cloud integration, and regulatory-driven monitoring networks. Over the next two to three years, connected monitoring platforms are expected to exceed 65% of newly commissioned industrial environmental systems.

Manufacturers are expanding partnerships with software providers, municipal authorities, and industrial operators to deploy integrated monitoring ecosystems across factories, transportation corridors, and smart-city infrastructure. For example, automated sensor networks installed across industrial zones enable continuous compliance reporting while reducing manual inspection frequency. Companies strengthening digital monitoring capabilities, localized production, and integrated service portfolios will secure stronger competitive positioning and greater operational resilience in the evolving environmental monitoring landscape.

Stringent emission compliance frameworks and rapid deployment of intelligent monitoring networks are accelerating demand for advanced air quality monitoring equipment across industrial and public infrastructure. More than 68% of newly installed environmental monitoring stations now incorporate IoT-enabled sensors, while AI-assisted analytics improve pollutant detection accuracy by approximately 32%. China continues expanding national environmental surveillance networks, and the U.S. Environmental Protection Agency has strengthened continuous monitoring initiatives for industrial facilities. This regulatory and digital transformation is driving procurement of connected monitoring platforms. Equipment manufacturers are expanding sensor portfolios, investing in cloud-enabled analytics, and forming technology partnerships to deliver integrated monitoring ecosystems. Organizations offering interoperable, real-time environmental intelligence gain stronger positioning in long-term public infrastructure and industrial compliance projects.

Complex integration requirements and dependence on precision sensing components continue limiting broader deployment, particularly among cost-sensitive industrial users. Advanced gas sensors, optical analyzers, and calibration modules account for nearly 45% of total equipment costs, while imported sensing components represent over 55% of critical procurement in several manufacturing markets. Semiconductor supply disruptions and specialized electronic component shortages have extended equipment delivery timelines in countries including Germany and Japan. These structural constraints increase project costs, delay infrastructure rollouts, and pressure supplier margins. Companies are responding by localizing production, qualifying alternative component suppliers, negotiating long-term procurement agreements, and redesigning modular platforms that simplify installation while reducing dependence on single-source component ecosystems.

The transition from standalone monitoring devices to intelligent environmental management platforms is creating significant opportunities for technology providers. More than 61% of newly specified monitoring projects include cloud connectivity, while predictive analytics reduce maintenance interventions by approximately 28% through automated diagnostics. India is accelerating smart-city environmental programs, creating demand for scalable monitoring architectures integrated with digital municipal infrastructure. Edge computing, digital twins, and low-power wireless sensor networks are enabling continuous environmental intelligence with lower operating costs. Manufacturers are increasing investment in AI software, strategic acquisitions, and open-platform ecosystems that integrate monitoring equipment with industrial automation, ESG reporting, and enterprise asset management, unlocking long-term recurring service opportunities beyond hardware sales.

Long-term deployment increasingly depends on secure integration across diverse environmental monitoring platforms rather than sensor performance alone. Approximately 47% of industrial operators report interoperability limitations between legacy monitoring assets and modern digital systems, while cybersecurity incidents targeting operational technology environments have increased by more than 30% in recent years. Large municipal deployments in the United States and other developed economies require standardized communication protocols, secure cloud architectures, and continuous software updates throughout equipment lifecycles. These execution challenges complicate large-scale monitoring consistency and lifecycle management. Companies must strengthen cybersecurity capabilities, expand software engineering expertise, establish interoperability partnerships, and invest in standardized digital architectures to ensure resilient, scalable, and future-ready environmental monitoring infrastructure.

AI-Powered Monitoring Expansion: AI-enabled air quality monitoring platforms are becoming standard across industrial and municipal deployments, with nearly 64% of newly commissioned systems integrating automated analytics and approximately 35% faster pollutant identification than conventional platforms. Increasing environmental compliance requirements are accelerating digital workflows, while equipment manufacturers are scaling cloud-based software, predictive diagnostics, and remote monitoring capabilities to improve operational efficiency and reduce field servicing requirements.

Compact Multi-Sensor Deployment: Demand is shifting toward compact multi-parameter monitoring equipment capable of simultaneously measuring particulate matter, VOCs, NO₂, SO₂, and ozone. Around 58% of new monitoring projects now specify multi-sensor platforms, reducing installation complexity by nearly 27%. Companies are redesigning modular architectures, improving sensor interoperability, and expanding portable product portfolios to support industrial facilities, smart buildings, and transportation infrastructure with lower lifecycle maintenance requirements.

Localized Manufacturing Strategies: Environmental equipment manufacturers are restructuring production networks as precision electronic component availability and logistics costs remain key operational considerations. Nearly 41% of manufacturers have expanded regional assembly operations, while localized sourcing has reduced procurement lead times by approximately 22%. Companies are strengthening supplier diversification, investing in automated calibration facilities, and standardizing component platforms to improve delivery reliability and operational resilience.

Integrated Environmental Intelligence: Organizations increasingly require air quality monitoring systems to connect directly with industrial automation, ESG reporting platforms, and digital facility management software. More than 61% of enterprise deployments now include cloud connectivity, while automated reporting reduces manual compliance workloads by approximately 38%. Equipment suppliers are expanding software partnerships, developing open communication protocols, and enhancing cybersecurity capabilities to deliver scalable environmental intelligence across manufacturing plants, commercial facilities, and smart-city infrastructure.

The market is segmented into Fixed Monitoring Systems, Portable Monitoring Systems, Indoor Air Quality Monitors, Outdoor Air Quality Monitors, and Wearable Air Quality Monitors. Fixed Monitoring Systems dominate with an estimated 46% market share due to continuous operation, regulatory compliance capabilities, and seamless integration with industrial automation and environmental management networks. Industrial facilities, power plants, and municipal monitoring agencies continue prioritizing fixed installations because they provide uninterrupted real-time data collection, centralized analytics, and high measurement accuracy. Portable Monitoring Systems represent the fastest-growing segment as demand rises for flexible environmental assessments, emergency response, and temporary monitoring projects. Approximately 57% of newly launched portable devices now feature wireless connectivity and cloud synchronization, while miniaturized sensor technologies have improved operational efficiency by nearly 30%. Indoor Air Quality Monitors continue gaining adoption across commercial buildings, hospitals, educational institutions, and smart offices as indoor environmental quality receives greater operational attention. Outdoor Air Quality Monitors remain essential for national monitoring programs and urban pollution management, while Wearable Air Quality Monitors are emerging for occupational safety applications in construction, mining, and manufacturing. Equipment manufacturers are expanding modular product portfolios, integrating AI-enabled diagnostics, and improving sensor calibration technologies to address diverse deployment requirements across multiple industries.

The market is segmented into Ambient Air Monitoring, Indoor Air Quality Monitoring, Industrial Emission Monitoring, Process Monitoring, and Research & Academic Monitoring. Ambient Air Monitoring accounts for approximately 38% of overall demand as governments continue expanding national pollution surveillance networks and urban environmental monitoring programs. Continuous monitoring infrastructure supports regulatory compliance, public health reporting, and environmental planning across metropolitan areas. Industrial Emission Monitoring is the fastest-growing application as manufacturers increasingly deploy continuous monitoring technologies to improve operational transparency and environmental compliance. Nearly 62% of newly installed industrial monitoring platforms now include automated reporting and remote diagnostics, while digital integration reduces manual inspection requirements by approximately 33%. Indoor Air Quality Monitoring continues expanding across healthcare facilities, commercial offices, airports, and educational campuses where occupant health and operational performance remain strategic priorities. Process Monitoring supports manufacturing optimization through continuous environmental measurement, while Research & Academic Monitoring remains important for scientific studies, atmospheric modeling, and environmental innovation. Companies continue investing in integrated software platforms, intelligent sensor technologies, and cloud-enabled monitoring ecosystems to strengthen deployment flexibility across diverse operational environments.

The market is segmented into Government & Environmental Agencies, Industrial & Manufacturing, Commercial Buildings, Healthcare Institutions, Research Organizations, and Residential Users. Government & Environmental Agencies hold approximately 42% of market demand because of nationwide monitoring networks, regulatory enforcement responsibilities, and large-scale environmental surveillance initiatives. Continuous investments in urban air quality infrastructure and pollution management sustain procurement activity across developed and emerging economies. Industrial & Manufacturing represents the fastest-growing end-user segment as enterprises strengthen environmental governance and operational monitoring programs. Around 59% of large industrial facilities now prioritize continuous digital air monitoring to improve compliance management and operational visibility, while automated systems reduce manual reporting workloads by nearly 31%. Commercial Buildings continue increasing deployments through smart building management initiatives, while Healthcare Institutions emphasize indoor environmental quality to support patient safety and operational standards. Research Organizations maintain demand for advanced analytical instruments supporting environmental science and innovation, whereas Residential Users are adopting compact smart monitoring devices integrated with connected home ecosystems. Manufacturers are introducing application-specific solutions, expanding service agreements, and strengthening channel partnerships to address varying procurement priorities across public and private sectors.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America represented approximately 26.7% of the global Air Quality Monitoring Equipment Market in 2025, supported by extensive environmental compliance programs, industrial modernization, and widespread deployment of intelligent monitoring infrastructure. Large manufacturing facilities, power generation assets, transportation corridors, and municipal agencies continue investing in continuous monitoring systems integrated with cloud-based environmental management platforms. More than 69% of newly commissioned industrial monitoring installations now incorporate automated reporting and predictive diagnostics, improving operational visibility and compliance efficiency. Equipment suppliers are strengthening software capabilities, expanding service agreements, and introducing modular monitoring platforms that simplify lifecycle management. Enterprise demand for connected monitoring ecosystems continues to reinforce the region's leadership in advanced environmental intelligence and digital infrastructure deployment.

United States Market Outlook: The United States remains the largest contributor to the regional market due to extensive industrial infrastructure, strict environmental compliance programs, and widespread smart monitoring deployments. More than 74% of major metropolitan environmental monitoring stations operate with continuous digital data acquisition systems. Industrial operators continue integrating AI-enabled analytics, automated emissions reporting, and remote diagnostics into environmental management platforms, while manufacturers expand domestic production capabilities and strategic technology partnerships to strengthen long-term operational resilience.

Europe accounted for approximately 22.9% of the global market in 2025 as governments and industrial enterprises strengthened environmental monitoring through increasingly connected digital infrastructure. Manufacturing facilities, transportation networks, and urban authorities continue replacing legacy monitoring systems with integrated sensor platforms capable of continuous environmental reporting. Nearly 64% of newly deployed monitoring systems across regulated industrial facilities support cloud-based environmental management and automated compliance documentation. Equipment manufacturers continue enhancing calibration technologies, interoperability standards, and predictive maintenance capabilities while expanding partnerships supporting environmental digitalization and industrial sustainability initiatives.

Germany Market Outlook: Germany leads the European market through its advanced manufacturing ecosystem, industrial automation expertise, and strong environmental engineering capabilities. More than 66% of large industrial production sites utilize continuous environmental monitoring integrated with digital process management systems. Domestic equipment manufacturers continue investing in precision sensing technologies, automated calibration platforms, and industrial software integration to strengthen competitiveness across environmental monitoring applications serving manufacturing, utilities, and transportation sectors.

Asia-Pacific captured approximately 41.8% of the global Air Quality Monitoring Equipment Market in 2025, supported by extensive manufacturing capacity, expanding urban infrastructure, and large-scale environmental monitoring initiatives. Industrial production growth, smart-city investments, and stricter pollution management policies continue accelerating deployment of advanced monitoring systems across manufacturing zones and metropolitan regions. More than 63% of newly installed environmental monitoring networks within the region now feature IoT-enabled connectivity and centralized cloud monitoring platforms. Equipment manufacturers continue expanding regional production facilities, increasing sensor localization, and strengthening digital software integration to improve deployment efficiency and supply-chain resilience.

China Market Outlook: China remains the dominant country due to its extensive environmental monitoring programs, electronics manufacturing ecosystem, and large-scale industrial infrastructure. Approximately 34% of global air quality monitoring equipment manufacturing capacity is concentrated in China, while continuous expansion of urban environmental surveillance networks supports sustained equipment deployment. Domestic manufacturers continue investing in AI-enabled sensing technologies, precision manufacturing, and integrated environmental management platforms to strengthen both domestic adoption and export competitiveness.

South America accounted for approximately 5.4% of the global market in 2025, driven by increasing environmental compliance across mining, energy, manufacturing, and urban infrastructure sectors. Governments and industrial operators continue expanding continuous air monitoring capabilities to strengthen pollution management and workplace environmental standards. Nearly 46% of newly procured monitoring systems support remote environmental reporting and centralized operational management, improving regulatory oversight and maintenance efficiency. Equipment providers are expanding regional distribution networks, enhancing technical support services, and introducing scalable monitoring solutions designed for industrial facilities operating across geographically dispersed locations.

Brazil Market Outlook: Brazil represents the largest national market owing to its mining industry, expanding industrial production, and growing environmental monitoring requirements. More than 52% of large industrial environmental monitoring projects are concentrated within major manufacturing and mining corridors. Companies continue adopting automated monitoring technologies integrated with industrial environmental management systems while equipment suppliers strengthen local partnerships and service capabilities supporting long-term operational performance.

The Middle East & Africa represented approximately 3.2% of the global market in 2025 as governments accelerated environmental modernization alongside industrial diversification and infrastructure development programs. Air quality monitoring increasingly supports smart-city initiatives, energy facilities, transportation infrastructure, and large public developments requiring continuous environmental oversight. Nearly 43% of recently deployed monitoring projects include centralized digital management platforms and remote operational capabilities, improving environmental reporting efficiency. Equipment manufacturers continue expanding regional partnerships, establishing localized technical support operations, and delivering integrated monitoring solutions aligned with infrastructure modernization priorities.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through major industrial investments, large-scale infrastructure development, and expanding environmental monitoring requirements linked to national modernization initiatives. More than 48% of newly developed industrial infrastructure projects incorporate continuous environmental monitoring during operational planning. Technology providers continue collaborating with industrial operators and public authorities to deploy intelligent monitoring networks supporting energy facilities, urban developments, and transportation infrastructure while strengthening long-term environmental compliance capabilities.

The competitive landscape is led by Thermo Fisher Scientific, HORIBA, Teledyne Technologies, Emerson Electric, and Siemens, competing against specialized environmental instrumentation firms such as Aeroqual and TSI Incorporated, while regional manufacturers challenge global OEMs through cost-efficient solutions and localized support. The top five companies collectively account for approximately 39% of the global market, reflecting moderate consolidation with strong technology differentiation. Competition centers on sensor accuracy, digital integration, lifecycle services, and deployment speed rather than price alone. AI-enabled monitoring platforms improve data-processing efficiency by nearly 35%, while modular architectures reduce installation time by approximately 28% and remote diagnostics lower maintenance interventions by around 30%. Companies are expanding manufacturing capacity, forming software partnerships, strengthening calibration capabilities, and vertically integrating sensing technologies to improve supply resilience. Competitive momentum is shifting toward intelligent connected ecosystems instead of standalone hardware. High certification requirements, precision sensor expertise, and software interoperability remain major entry barriers. Winning requires integrated digital platforms, reliable service networks, rapid innovation, and scalable manufacturing capabilities.

HORIBA, Ltd.

Teledyne Technologies Incorporated

Emerson Electric Co.

Siemens AG

Aeroqual Limited

TSI Incorporated

AMETEK, Inc.

Testo SE & Co. KGaA

Honeywell International Inc.

Ecotech Pty Ltd.

Enviro Technology Services plc

AI-enabled analytics, edge computing, and IoT-connected sensing platforms are transforming air quality monitoring from periodic measurement into continuous environmental intelligence. More than 62% of newly deployed monitoring systems now incorporate cloud connectivity, while automated diagnostics reduce maintenance requirements by approximately 30%. Multi-parameter sensing platforms simultaneously measure particulate matter and gaseous pollutants, improving operational efficiency and enabling centralized environmental management across industrial and municipal networks.

Emerging technologies include laser-based particulate sensors, MEMS gas sensors, digital twins, and low-power wireless communication. Compared with conventional standalone monitoring equipment, AI-assisted monitoring platforms process environmental datasets nearly 40% faster while improving anomaly detection accuracy by approximately 25%. Industrial manufacturers, environmental agencies, and smart-city operators benefit from integrated software ecosystems that accelerate compliance reporting, predictive maintenance, and operational decision-making. Nearly 58% of enterprise deployments now prioritize interoperable monitoring architectures supporting remote asset management.

Between 2026 and 2028, autonomous sensor calibration, satellite-assisted environmental data integration, and advanced edge AI will reshape competitive positioning. Equipment suppliers investing in software-defined monitoring platforms, cybersecurity, and interoperable digital ecosystems will strengthen long-term differentiation. Organizations acting now gain faster deployment, lower operating costs, stronger regulatory readiness, and scalable environmental intelligence supporting enterprise-wide sustainability and infrastructure modernization initiatives.

May 2024 – Thermo Fisher Scientific announced the launch of its 'Make in India' Air Quality Monitoring System (AQMS) analyzers, engineered and manufactured at its Nashik facility to support India's National Clean Air Programme. The localization initiative significantly strengthens domestic production capacity and shortens supply chains for industrial and government customers. Business impact: Faster deliveries and improved regional manufacturing resilience. Source: www.theprint.in

2025 – Aeroqual entered a strategic partnership with Project Canary to integrate advanced sensor-based air quality monitoring with methane emissions quantification solutions. The collaboration expands continuous environmental monitoring capabilities and enables broader deployment across industrial facilities seeking integrated air quality and methane measurement. Business impact: Strengthens enterprise environmental compliance and multi-pollutant monitoring capabilities. Source: www.aeroqual.com

2025 – Aeroqual signed a landmark agreement with the Government of Thailand, officiated by New Zealand's Deputy Prime Minister, to support national clean air initiatives through expanded deployment of advanced air quality monitoring technologies. Business impact: Accelerates public-sector monitoring infrastructure and strengthens Aeroqual's presence in Southeast Asia. Source: www.aeroqual.com

July 2026 – HORIBA STEC commenced full-scale operations at its Kyoto Fukuchiyama Factory, introducing higher levels of production automation to stabilize semiconductor-related manufacturing. Although serving multiple analytical technologies, the investment strengthens HORIBA's long-term precision instrument manufacturing capacity supporting environmental monitoring products. Business impact: Enhances manufacturing efficiency and supply-chain resilience for advanced analytical instrumentation.

The report provides comprehensive analysis of the Air Quality Monitoring Equipment Market across Fixed Monitoring Systems, Portable Monitoring Systems, Indoor Air Quality Monitors, Outdoor Air Quality Monitors, and Wearable Air Quality Monitors. It evaluates key applications including ambient monitoring, industrial emission monitoring, indoor air quality management, process monitoring, and research activities across government agencies, industrial enterprises, commercial buildings, healthcare institutions, research organizations, and residential users. The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while highlighting evolving deployment patterns, digital monitoring adoption, and enterprise technology integration.

The study evaluates competitive positioning, product innovation, environmental monitoring technologies, AI-enabled sensing platforms, cloud-connected monitoring systems, and intelligent analytics supporting operational decision-making. More than 60% of new enterprise deployments now emphasize connected environmental monitoring ecosystems, while integrated software platforms continue reshaping procurement priorities. The report supports strategic investment planning, product development, geographic expansion, partnership evaluation, competitive benchmarking, and long-term business positioning across the global Air Quality Monitoring Equipment Market between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 520.0 Million |

| Market Revenue (2033) | USD 927.4 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Thermo Fisher Scientific Inc.; HORIBA, Ltd.; Teledyne Technologies Incorporated; Emerson Electric Co.; Siemens AG; Aeroqual Limited; TSI Incorporated; AMETEK, Inc.; Testo SE & Co. KGaA; Honeywell International Inc.; Ecotech Pty Ltd.; Enviro Technology Services plc |

| Customization & Pricing | Available on Request (10% Customization Free) |