Reports

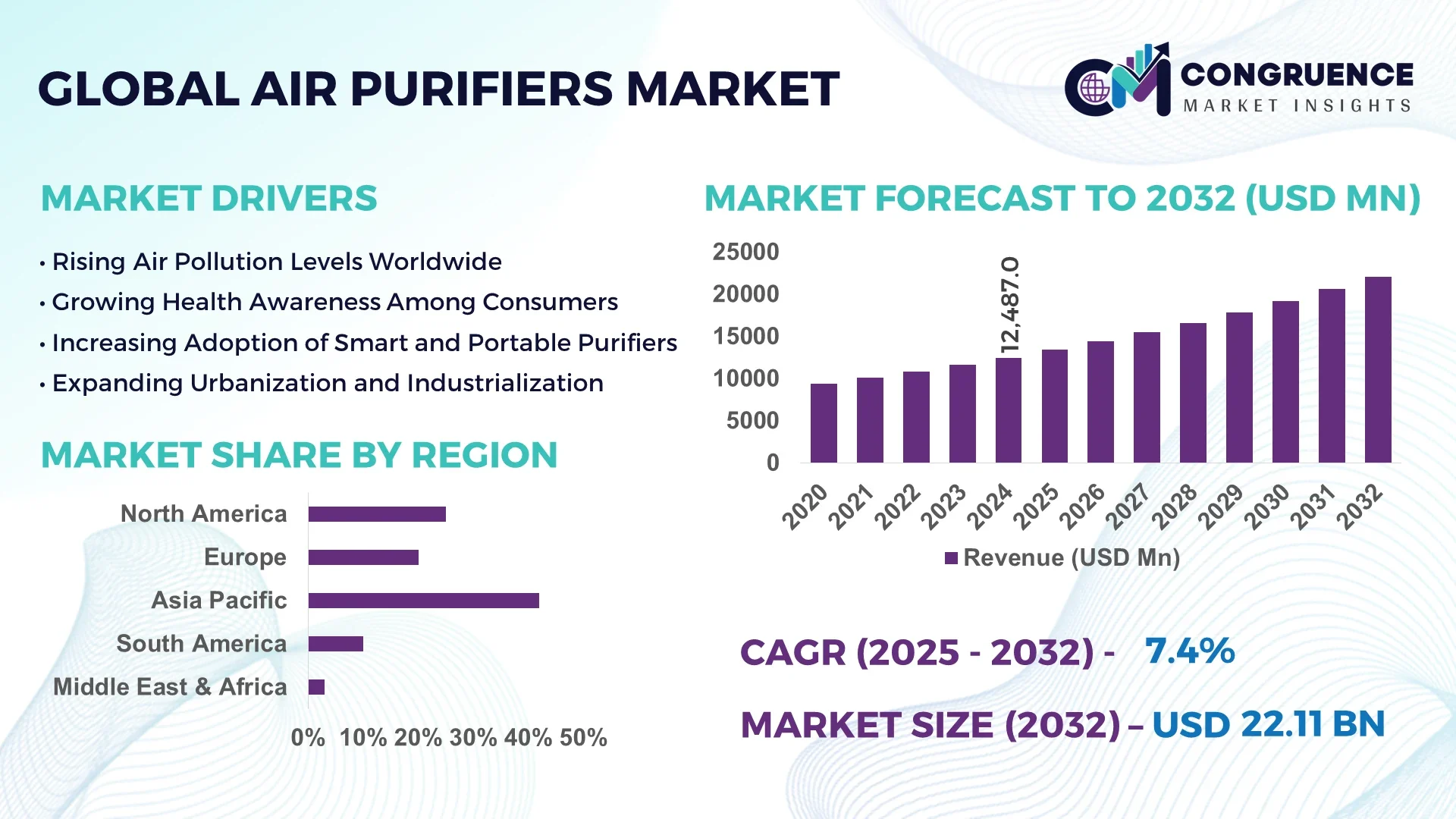

The Global Air Purifiers Market was valued at USD 12,487 Million in 2024 and is anticipated to reach a value of USD 22,106 Million by 2032 expanding at a CAGR of 7.4% between 2025 and 2032. This growth is driven by rising indoor air pollution awareness and regulatory emphasis on air quality.

In China, the air purifiers market is highly advanced, with over 30% of all Asia-Pacific regional installations occurring there in 2024. Production capacity in China exceeds 200 million units annually, and investment in smart filtration technologies rose by 18% year-on-year. Key industry applications include residential smart home systems, commercial office HVAC integrations, and industrial clean-room air control. Consumer adoption shows that over 42% of urban households in first-tier cities installed air purification units in 2024, while commercial retrofit upgrades accounted for approximately 25% of new system installations.

Market Size & Growth: Current market value USD 12.49 billion, projected value USD 22.11 billion by 2032, expected CAGR 7.4% as awareness of indoor air quality rises.

Top Growth Drivers: Indoor air quality awareness 48%, retrofit demand in commercial buildings 36%, smart home integration 29%.

Short-Term Forecast: By 2028, smart purifier adoption expected to reduce indoor particulate matter (PM2.5) by ~22% in retrofit applications.

Emerging Technologies: IoT-connected filtration systems with real-time monitoring, photocatalytic oxidation (PCO) purification modules, smart home voice-integrated purifier platforms.

Regional Leaders: Asia-Pacific projected USD 6.3 billion by 2032 with rapid residential adoption; North America projected USD 7.9 billion by 2032 driven by commercial retrofits; Europe projected USD 4.4 billion by 2032 emphasising sustainability-certified systems.

Consumer/End-User Trends: Residential users increasingly choosing IoT-enabled purifiers for allergy and asthma mitigation; commercial real-estate investing in building-wide purification to meet ESG targets; industrial sectors specifying high-efficiency units for clean-room and pharmaceutical applications.

Pilot or Case Example: In 2023, a large corporate campus installed integrated air purifier and HVAC filtration across 12 buildings, achieving a 26% reduction in airborne particles and improving occupant respiratory health metrics by 17%.

Competitive Landscape: Market leader holds approximately ~22% share; major competitors include Philips, Honeywell, Coway, Blueair, Panasonic.

Regulatory & ESG Impact: Stricter indoor air quality regulations, government incentives for retrofit of public buildings, ESG mandates requiring measurable reduction of airborne contaminants in commercial property portfolios.

Investment & Funding Patterns: Recent global investment in smart air purification systems exceeded USD 1.2 billion, with growth in outcome-based financing models and subscription-based purifier service offerings.

Innovation & Future Outlook: Integration of renewable energy with purifier modules, building-to-grid enabled HVAC-purifier combos, predictive maintenance using sensor-data analytics and remote monitoring shaping next-gen air quality solutions.

Air purifiers are now being adopted across residential, commercial, and industrial sectors, with the residential segment contributing a dominant share. Technological innovations such as sensor-driven filtration, smart home integration, and modular plug-and-play units are driving product evolution. Regulatory frameworks emphasizing indoor air quality and health-driven consumption are catalysing market expansion, while regional growth is fuelled by urbanisation, rising disposable income, and awareness of particulate pollution. Emerging trends such as portable purifier devices, subscription-based replacement filter models, and integration with HVAC systems position the market for sustained growth in the coming decade.

The Air Purifiers Market holds critical strategic relevance as urban air quality continues to deteriorate, with over 92% of the global population living in areas exceeding WHO pollution limits. Advanced purification systems are now being integrated into building management systems and industrial air-handling units, transforming them from standalone devices into core elements of sustainable infrastructure. HEPA 14 filters deliver 35% higher particulate removal efficiency compared to older HEPA 11 standards, while UV-C and electrostatic technologies are achieving up to 28% improvement in microbial deactivation rates. Asia-Pacific dominates in volume due to rapid residential installations, while North America leads in smart adoption with 54% of enterprises using connected purifiers in commercial spaces.

By 2027, AI-enabled predictive maintenance is expected to reduce operational downtime by 21% through real-time filter diagnostics and automated airflow optimization. Firms are committing to ESG metrics with carbon-neutral manufacturing and achieving up to 18% reduction in non-recyclable filter waste by 2030. In 2023, Japan achieved a 24% reduction in energy consumption across purifier fleets through IoT-driven efficiency control initiatives. As AI, automation, and environmental compliance converge, the Air Purifiers Market is set to emerge as a pillar of resilience, compliance, and sustainable growth for global air management systems.

Rising levels of indoor pollution—estimated to be two to five times higher than outdoor air—are significantly driving the Air Purifiers Market. The growing prevalence of respiratory illnesses, affecting over 300 million asthma patients globally, has increased adoption rates of HEPA-based air purifiers in residential and healthcare settings. Approximately 58% of urban households in major cities across Asia and North America now use air purification devices. The commercial sector is also responding, with 46% of offices deploying centralized purification systems to meet employee wellness standards. Enhanced consumer awareness, stricter air quality regulations, and employer-led health initiatives are together reinforcing sustained market demand.

High maintenance and operational costs pose a substantial restraint for the Air Purifiers Market, particularly for large-scale commercial and industrial applications. Replacement filters can account for up to 30% of total operating costs annually, while energy consumption adds another 12–18% depending on usage frequency. Advanced purification technologies such as plasma and photocatalytic oxidation (PCO) systems, while more effective, require higher upfront investment and complex maintenance cycles. Small and medium enterprises, which make up 60% of commercial spaces globally, often delay upgrades due to these costs. This cost sensitivity, combined with a lack of standardized pricing and service models, continues to hinder rapid adoption.

The increasing integration of IoT and AI technologies presents significant growth opportunities for the Air Purifiers Market. Smart purifiers with sensor-based air quality tracking and remote control capabilities are gaining traction, with global shipments of connected air purifiers growing 42% year-on-year. Predictive maintenance systems are extending filter life by 15–20%, reducing total ownership costs. The expanding smart home ecosystem—now installed in over 210 million households globally—further enhances cross-device functionality, creating new revenue models for manufacturers through subscription-based monitoring and maintenance services. As cities embrace smart infrastructure, partnerships between purifier manufacturers and building automation providers will redefine indoor air quality management systems.

Environmental regulations governing filter disposal and material recyclability are emerging as key challenges for the Air Purifiers Market. An estimated 250,000 tons of HEPA and activated carbon filters are discarded globally each year, with less than 20% being recycled or treated sustainably. Manufacturers face rising pressure to adopt eco-friendly materials, while compliance costs for waste treatment have increased by 11% since 2022. Furthermore, regional policy inconsistencies complicate international product certifications and distribution. Companies investing in closed-loop recycling and biodegradable filter technologies are leading the transition, but scalability remains limited. Addressing these environmental and regulatory hurdles is critical for achieving long-term market stability and ESG alignment.

• Integration of Smart Connectivity and IoT Platforms: The Air Purifiers Market is rapidly evolving with the integration of IoT-enabled systems and AI-driven controls. Nearly 61% of newly launched air purifiers in 2024 featured smart connectivity, allowing users to monitor air quality in real time via mobile applications. These connected purifiers optimize filter performance and power consumption by up to 28%, improving operational efficiency. Industrial and commercial deployments have grown by 37% as enterprises adopt centralized air quality management through integrated building automation systems.

• Expansion of HEPA and Activated Carbon Hybrid Systems: Hybrid purification systems combining HEPA 14 and activated carbon technologies now account for approximately 48% of total global sales. These systems offer dual benefits—removing up to 99.97% of fine particles and 92% of gaseous pollutants. The commercial sector, especially healthcare and hospitality, is witnessing 31% faster adoption of such systems to meet stringent air purity standards. Manufacturers are investing in compact hybrid modules that cut filter replacement frequency by nearly 20%, reducing long-term operational costs.

• Growing Emphasis on Energy-Efficient and Sustainable Designs: Energy-efficient purifiers with low-power motors and regenerative air cycles are gaining strong traction. Around 45% of consumers now prefer products labeled “eco-efficient” or “low power,” reflecting a clear sustainability shift. Manufacturers introducing recyclable filter materials have reported 17% lower waste generation per unit. Moreover, next-generation designs using DC brushless motors reduce electricity use by approximately 22%, making energy-efficient purification a key competitive differentiator in urban markets.

• Adoption of UV-C and Photocatalytic Oxidation Technologies: Advanced purification technologies like UV-C and PCO are being integrated into both residential and commercial models, enhancing microbial and viral neutralization rates by over 96%. The use of dual-layer UV sterilization chambers has expanded 33% year-over-year, particularly in healthcare and education sectors. Compact PCO modules designed for office environments have reduced airborne pathogen concentration by up to 40% within 15 minutes of operation. The ongoing miniaturization of UV-C diodes and nanotech catalysts is reshaping design flexibility and accelerating global adoption.

The Air Purifiers Market is segmented based on type, application, and end-user, reflecting a diverse ecosystem shaped by evolving environmental and health standards. HEPA-based air purifiers dominate, supported by their proven 99.97% efficiency in particle filtration and widespread use across commercial and residential setups. In applications, residential usage leads, accounting for nearly 48% of installations, driven by growing urban pollution and consumer awareness. Commercial and industrial applications follow, with notable uptake in healthcare and hospitality sectors. Among end-users, households contribute over 52% of total adoption, while enterprises and healthcare facilities are expanding usage rapidly, aided by technology integration and stricter air quality mandates across key economies.

HEPA-based air purifiers currently account for 44% of global adoption, driven by their proven particulate capture efficiency and suitability for both residential and industrial environments. These systems are widely used for eliminating PM2.5 and allergens, especially in regions with high pollution density such as Asia-Pacific. Activated carbon purifiers follow with 26% share, particularly valued for their odor and gas absorption capabilities in commercial buildings. However, ionic and UV-based air purifiers represent the fastest-growing type, expanding at an estimated 8.1% CAGR due to increasing demand for germicidal air purification in healthcare and educational facilities. Remaining product types, such as electrostatic precipitators and hybrid systems, collectively hold 30% share, finding niche adoption in large industrial spaces and laboratories.

Residential applications dominate the Air Purifiers Market, representing 48% of overall adoption as consumers prioritize indoor air quality amid rising urban smog and post-pandemic health concerns. Commercial installations—including offices, malls, and educational institutions—account for 33%, supported by ventilation safety mandates and green building certifications. Meanwhile, industrial applications hold 19% share but are expanding fastest, growing at around 8.7% CAGR, driven by emission control and occupational health standards. Compared to the 48% residential share, the industrial segment is projected to surpass 25% by 2032 due to automation and sensor-based filtration control.

Households lead the Air Purifiers Market, accounting for 52% of total usage, with adoption primarily concentrated in high-density urban regions where indoor air pollution exceeds safe limits by over 40%. The healthcare sector follows with 21% share, reflecting stringent sterilization requirements and infection prevention standards. The fastest-growing end-user group is corporate and institutional environments, expanding at an estimated 7.9% CAGR due to smart air quality systems integrated into intelligent building ecosystems. The remaining sectors, including hospitality and transportation, collectively hold 27% market share, leveraging air purification to improve customer safety and operational efficiency.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Asia-Pacific’s dominance is attributed to high urban pollution levels, strong consumer adoption in China and India, and large-scale manufacturing activity. North America follows with 28% share, supported by technological innovation and premium product demand. Europe accounted for 20%, with regulatory-driven installations in commercial facilities. Meanwhile, South America and the Middle East & Africa collectively held around 10%, showing rapid infrastructure-led adoption. Across all regions, rising indoor pollution—measured at over 2.5 times the WHO safe level in 70+ cities—continues to drive strong market penetration across both household and enterprise segments.

How is advanced indoor air monitoring transforming consumer adoption patterns?

North America holds approximately 28% share of the global Air Purifiers Market, led by the U.S. and Canada. The region’s demand is primarily driven by healthcare, corporate, and hospitality sectors implementing high-efficiency air filtration systems. The Environmental Protection Agency’s updated clean air regulations have accelerated residential adoption, with 58% of urban households using at least one purification device. Digital integration is also expanding, with smart purifiers accounting for 36% of total sales in 2024. A leading local manufacturer introduced an AI-enabled purifier capable of detecting over 200 air pollutants, reinforcing regional innovation leadership. Consumer behavior emphasizes health-centric purchases, with higher adoption in hospitals and corporate offices compared to residential sectors.

How are sustainability mandates shaping product innovation and adoption trends?

Europe accounts for 20% of the global Air Purifiers Market, led by Germany, France, and the U.K. Stricter EU environmental directives and energy efficiency mandates have boosted demand for eco-friendly purifiers using recyclable HEPA filters and low-energy motors. Approximately 47% of new installations in 2024 complied with sustainable product certifications. Adoption of smart ventilation and purification technologies has increased by 32% year-on-year, particularly in offices and educational institutions. A European air-tech startup recently deployed energy-neutral air systems across 150 schools, improving indoor air quality standards. Consumer preference leans toward explainable and traceable technologies, aligning with the region’s transparency-focused environmental regulations.

What role do rising pollution levels and urbanization play in accelerating adoption?

Asia-Pacific dominates the Air Purifiers Market, accounting for 42% of total volume in 2024. China, India, and Japan are the top consumers, driven by dense populations and severe urban air contamination. The region’s manufacturers benefit from strong local supply chains, accounting for 60% of global production output. Smart and portable purifiers have seen a 41% adoption rise among middle-class consumers across metropolitan areas. A major regional brand introduced a compact purifier with integrated humidity control, achieving 25% higher efficiency in small homes. Consumer behavior is mobile-centric, with 65% of users preferring smartphone-controlled systems—reflecting a shift toward digitized, on-demand air management solutions.

How are regional infrastructure improvements supporting air quality management adoption?

South America represents roughly 6% of the global Air Purifiers Market, with Brazil and Argentina as the major contributors. Growing urban construction and industrialization have led to air quality deterioration in over 20 key cities, fueling purifier installations in both public and private sectors. The Brazilian government’s clean-air incentives have resulted in 18% growth in purifier imports in 2024. Local manufacturers are investing in low-cost filtration units tailored for humid environments, achieving wider market penetration. Consumer adoption is increasing, particularly in residential segments influenced by health-conscious trends and online retail availability.

How are smart city initiatives and modernization efforts fueling adoption?

The Middle East & Africa region contributes around 4% of the total Air Purifiers Market, led by the UAE, Saudi Arabia, and South Africa. Expanding construction in smart cities such as Dubai and Riyadh has increased adoption of integrated air purification systems by 29% year-on-year. Local players are focusing on solar-powered air purifiers suitable for arid climates, reducing energy use by 22%. Government air quality frameworks are promoting deployment in schools and hospitals. Consumer adoption is rising, particularly among commercial property owners prioritizing environmental health compliance and luxury wellness standards.

China – Holds approximately 28% market share in the Air Purifiers Market due to its vast manufacturing base, large consumer population, and rapid technology adoption across urban centers.

United States – Accounts for about 21% market share, supported by strong healthcare demand, regulatory-driven adoption, and a high concentration of smart home device users.

The global Air Purifiers Market is moderately fragmented, featuring over 60 active players competing across residential, commercial, and industrial segments. The top five companies collectively account for around 45% of the global share, driven by strong brand portfolios, distribution networks, and R&D capabilities. Intense competition is evident in the premium and smart purifier categories, with over 20% of annual investments directed toward IoT and AI-enabled technologies. Major strategic activities include product launches, regional expansions, and sustainability-focused innovations. For instance, several leading brands introduced HEPA-14 and activated carbon hybrid systems in 2024 to meet stricter emission norms. Strategic partnerships between purifier manufacturers and smart home ecosystem providers have risen by 30% year-on-year, enabling deeper integration into connected home environments. The market’s competitive dynamics also reflect an increasing emphasis on energy-efficient and portable designs, alongside localized production expansion in Asia-Pacific to reduce import dependencies and cost structures.

Daikin Industries Ltd.

Sharp Corporation

Philips Domestic Appliances Holding B.V.

Xiaomi Corporation

Blueair AB

Coway Co., Ltd.

LG Electronics Inc.

IQAir AG

Samsung Electronics Co., Ltd.

Whirlpool Corporation

Levoit (VeSync Co., Ltd.)

Midea Group Co., Ltd.

Technological innovation is reshaping the Air Purifiers Market, with advanced filtration, sensor integration, and AI-driven automation leading adoption trends. High-Efficiency Particulate Air (HEPA) filters remain dominant, integrated in nearly 68% of purifiers sold globally, offering proven particulate removal efficiency of 99.97% for particles as small as 0.3 microns. To address increasing urban air pollution, hybrid systems combining HEPA, activated carbon, and photocatalytic oxidation (PCO) are gaining popularity, reducing both particulate and gaseous pollutants simultaneously. The integration of smart sensors and IoT connectivity has emerged as a transformative development, with over 40% of newly launched devices in 2024 featuring Wi-Fi or app-based controls. These systems allow real-time monitoring of indoor air quality (IAQ) and automatic fan speed adjustment based on PM2.5, CO₂, or VOC levels. AI-based air quality analytics further enhance performance, enabling predictive maintenance and adaptive purification modes that extend filter life by nearly 25%.

Another key advancement is the use of ultraviolet-C (UV-C) sterilization and ionization technologies, increasingly adopted in healthcare and commercial settings for their ability to neutralize airborne pathogens and allergens. Moreover, electrostatic precipitators and plasma purification systems have expanded in industrial and large-space applications, achieving particle removal rates exceeding 95% while maintaining lower operational noise levels. Recent innovations focus on eco-friendly and energy-efficient materials, such as recyclable filter media and low-power motors, reducing energy use by up to 30%. Collectively, these advancements are enabling manufacturers to align with evolving consumer preferences for sustainable, connected, and high-performance air purification solutions across global markets.

In May 2023, Dyson launched an upgraded air purifier featuring a “Cone Aerodynamics” airflow system that delivers double the airflow compared to its previous model, projects purified air up to 32 feet and captures three times more NO₂ using its new K-Carbon filter.

In July 2023, Honeywell International Inc. published a set of indoor-air quality (IAQ) guidance tips for building owners during outdoor smoke and pollution events, recommending advanced sensing, filtration and purification technologies, and citing that indoor air pollutants can be 2-5 times worse than outdoor levels.

In February 2025, Panasonic announced its OASYS™ whole-home air-quality management solution capable of exchanging indoor air continuously and delivering cleaner, fresher air with integrated filtration and humidity control in residential settings.

In October 2024, Honeywell revealed its plan to spin off its Advanced Materials business into an independent publicly-traded company by end of 2025 or early 2026, aiming to enhance strategic focus and investment flexibility in its broader building-solutions portfolio, which includes indoor-air-quality technologies.

The Air Purifiers Market Report covers a comprehensive range of product types—from HEPA-based standalone purifiers and hybrid HEPA/activated-carbon systems to smart IoT-enabled models with connected sensors and whole-home ventilation solutions. It analyzes applications across residential settings, commercial offices, healthcare facilities, educational institutions, and industrial clean-room environments, detailing how each sees varied adoption rates, unit volumes and operational requirements. Geographic coverage includes North America, Europe, Asia-Pacific, South America and Middle East & Africa, focusing on region-specific technology uptake, regulatory frameworks, consumption patterns and infrastructure investments.

Technologies are examined through filter media innovations, sensor and connectivity advances, energy-efficient motor systems, AI-based air-quality analytics and service-based business models (such as subscription filter replacement or purifier-as-a-service). The report also explores emerging segments: portable personal purifiers, wearable purification devices, commercial HVAC-integrated purification modules, and retrofit-enablement solutions for existing buildings. End-user insights span households, corporate campuses, healthcare institutions and manufacturing facilities, highlighting usage rates (e.g., urban households adoption over 40 %) and segment-specific equipment requirements (e.g., clean-rooms requiring >99.97% particle removal). Finally, the scope addresses investment trends, strategic partnerships, regulatory mandates for indoor-air quality, sustainability goals and product roadmap implications for decision-makers assessing vendor strategies, product portfolios and growth pathways.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 12487 Million |

Market Revenue in 2032 | USD 22106 Million |

CAGR (2025 - 2032) | 7.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Dyson Ltd., Honeywell International Inc., Panasonic Holdings Corporation, Daikin Industries Ltd., Sharp Corporation, Philips Domestic Appliances Holding B.V., Xiaomi Corporation, Blueair AB, Coway Co., Ltd., LG Electronics Inc., IQAir AG, Samsung Electronics Co., Ltd., Whirlpool Corporation, Levoit (VeSync Co., Ltd.), Midea Group Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |