Reports

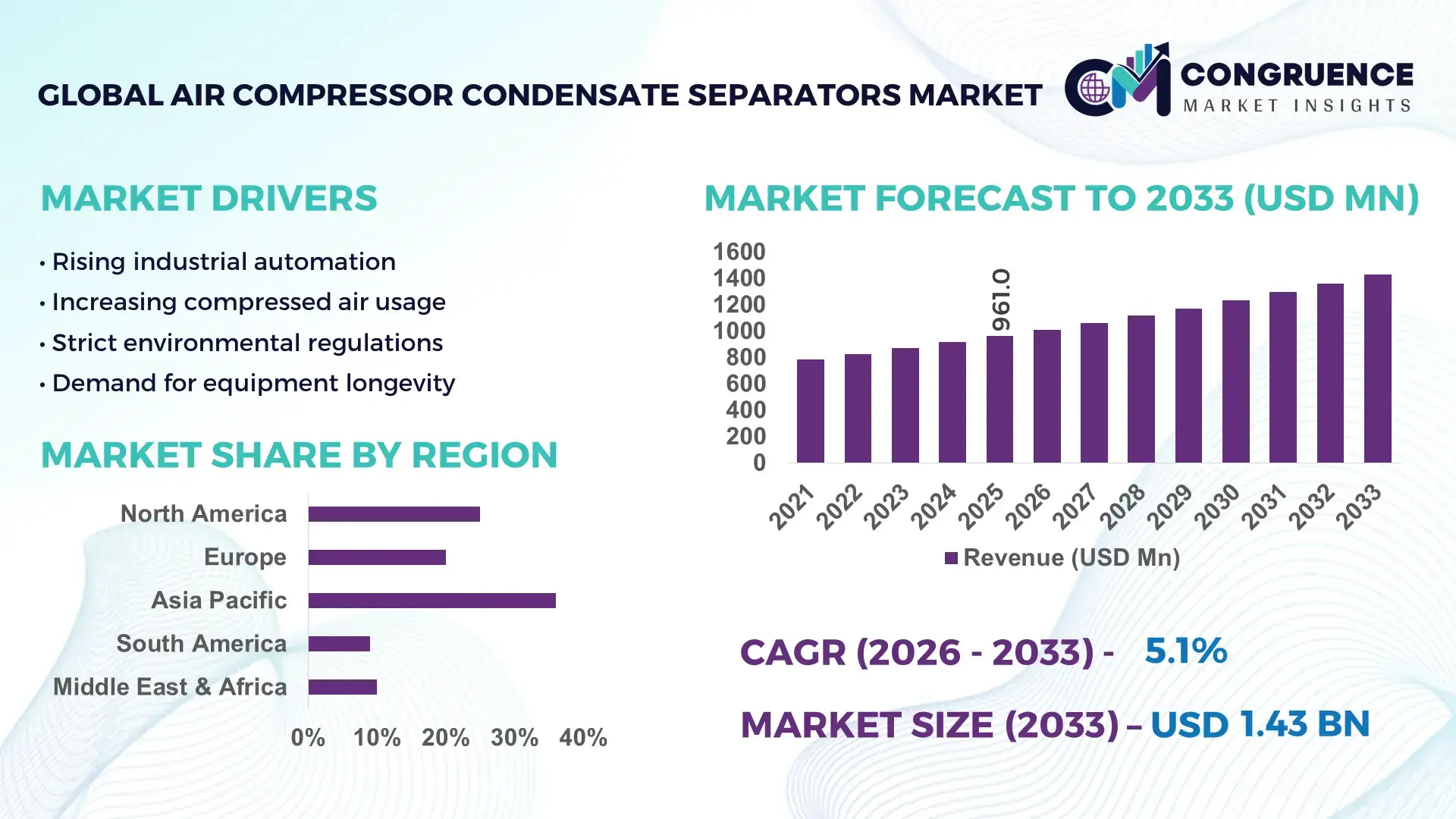

The Global Air Compressor Condensate Separators Market was valued at USD 961 Million in 2025 and is anticipated to reach a value of USD 1430.68 Million by 2033 expanding at a CAGR of 5.1% between 2026 and 2033. This growth is driven by increasing industrial compressed air usage and stringent environmental discharge regulations requiring efficient condensate treatment.

The Asia Pacific region, particularly China, dominates global production and demand, with China alone accounting for an estimated 30–35% of unit output supported by extensive OEM manufacturing clusters and integrated assembly lines in industrial hubs. China’s investment in automated separators and IoT-enabled monitoring systems reflects strong deployment in high-volume manufacturing facilities, while local production capacity enables competitive pricing for both domestic and export markets. By leveraging advancements in separation media and smart monitoring technologies, China continues to expand its industrial compressor condensate management infrastructure, serving key sectors like automotive, electronics, and heavy machinery manufacturing.

Market Size & Growth: Valued at USD 961M in 2025 and projected to reach USD 1,430.68M by 2033 at a 5.1% CAGR, propelled by environmental compliance and industrial automation demand.

Top Growth Drivers: Rising industrial compressor installations (42%), stricter wastewater discharge standards (38%), increasing energy-efficient air systems adoption (27%).

Short-Term Forecast: By 2028, expect a 15% improvement in condensate oil removal efficiency through advanced media and sensor integration.

Emerging Technologies: IoT-enabled real-time condensate monitoring, advanced coalescing media, and predictive maintenance analytics.

Regional Leaders: Asia Pacific – USD ~614M by 2033 with rapid manufacturing growth; North America – strong tech adoption and retrofit demand; Europe – high compliance-driven equipment upgrades.

Consumer/End‑User Trends: Manufacturing facilities and automotive plants prioritizing low‑maintenance, high‑efficiency separators with remote diagnostics.

Pilot or Case Example: A 2025 pilot in Southeast Asia achieved 22% reduction in compressor downtime with smart condensate separators.

Competitive Landscape: Market leader Atlas Copco ~22%, followed by Parker Hannifin, Ingersoll Rand, SPX FLOW, and Donaldson Company.

Regulatory & ESG Impact: Tightening oil‑in‑water discharge limits and ESG commitments driving adoption of high‑performance separation solutions.

Investment & Funding Patterns: Recent investments exceeding USD 120M in smart separator technologies, with growing venture backing for sustainability‑oriented innovations.

Innovation & Future Outlook: Enhanced IoT integration, modular designs for retrofit markets, and predictive analytics shaping next‑generation condensate management solutions.

The Air Compressor Condensate Separators Market is anchored by key industrial sectors such as manufacturing, automotive, food & pharma, and heavy processing industries, each relying on compressed air systems that produce oil‑laden condensate requiring effective separation. Recent product innovations include multi‑stage separation media, automated drainage systems, and connected diagnostics, improving operational uptime and compliance. Regulatory drivers related to wastewater discharge and environmental stewardship continue to influence procurement and deployment, while economic factors such as rising industrial automation and infrastructure build‑out in Asia Pacific fuel regional demand. Consumption patterns show sustained growth in high‑volume manufacturing corridors, with future outlook focusing on sustainability, predictive maintenance, and integrated system solutions.

The Air Compressor Condensate Separators Market holds significant strategic relevance as industries increasingly seek efficient, environmentally compliant solutions for managing compressed air condensate. Advanced coalescing separator technologies deliver up to 30% higher oil-removal efficiency compared to conventional mesh-based systems, providing measurable improvements in operational uptime and maintenance costs. Asia Pacific dominates in volume, while Europe leads in adoption, with over 65% of industrial enterprises deploying high-performance separators in automated production lines. By 2028, IoT-enabled predictive maintenance systems are expected to improve equipment uptime by 18% and reduce unscheduled maintenance interventions. Firms are committing to ESG improvements such as achieving a 25% reduction in oil-contaminated wastewater discharge by 2030, aligning with global environmental compliance mandates. In 2025, a leading Chinese manufacturing plant achieved a 22% reduction in compressor downtime through the integration of smart condensate monitoring and automated drainage technology. Looking ahead, the Air Compressor Condensate Separators Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable industrial growth, providing measurable efficiency gains while supporting environmental stewardship and forward-looking industrial automation initiatives.

The push for higher industrial efficiency and automation is significantly driving the Air Compressor Condensate Separators Market. Facilities adopting automated air compressors and connected production lines require condensate separators capable of consistent oil-water separation without frequent maintenance. Approximately 58% of industrial enterprises integrating high-volume air compressors have implemented advanced separators to optimize operations. Technological enhancements such as multi-stage coalescing media and automated drainage systems improve removal efficiency by up to 25%, reducing operational downtime and maintenance costs. The increasing adoption of Industry 4.0 standards is further accelerating the deployment of IoT-enabled monitoring, allowing real-time performance tracking and predictive maintenance. These trends are particularly evident in automotive, electronics, and heavy machinery sectors, where uptime and energy efficiency are critical. By aligning separator performance with automation strategies, industrial users achieve measurable operational improvements while meeting regulatory requirements for condensate disposal.

High upfront costs of advanced condensate separators and integration complexities are key restraints for market growth. Industrial facilities often face capital expenditures exceeding USD 10,000 per high-capacity automated separator, limiting adoption in smaller plants. Technical integration with existing compressed air systems can require redesigning piping layouts and adding monitoring hardware, increasing project timelines by up to 20%. Additionally, workforce training for automated and IoT-enabled separators is necessary to ensure proper operation, creating an initial operational burden. Regulatory compliance for installation and disposal of separated condensate adds complexity, particularly in regions with stringent environmental standards. These factors collectively delay immediate deployment despite the long-term operational efficiency and environmental benefits. Consequently, the market experiences slower uptake among cost-sensitive or small-to-medium industrial users, even as larger enterprises continue to prioritize performance and compliance.

The growing adoption of smart IoT sensors and predictive maintenance analytics presents significant opportunities in the Air Compressor Condensate Separators Market. By 2027, predictive monitoring is projected to improve separator maintenance efficiency by 20–25%, allowing proactive component replacement and minimizing unplanned downtime. Industrial facilities implementing connected separators gain real-time insights into condensate volume, oil content, and filter performance, enhancing operational decision-making. The shift toward sustainable manufacturing also encourages investment in separators capable of automated oil recovery and environmentally compliant discharge, meeting ESG goals. In regions like North America and Europe, where regulatory enforcement is high, enterprises are actively seeking solutions that integrate seamlessly with existing industrial IoT platforms. Additionally, emerging markets with expanding industrial bases represent a substantial growth opportunity for suppliers offering modular, easy-to-install smart separators tailored for both high-volume and mid-sized operations.

Complex maintenance requirements, regulatory pressures, and high operational costs present ongoing challenges for the Air Compressor Condensate Separators Market. Industrial separators require periodic inspection, filter replacement, and monitoring to maintain separation efficiency, which can increase labor costs by up to 15% annually. Stringent environmental regulations regarding oil-in-water discharge necessitate compliance verification, record-keeping, and often specialized disposal methods, further adding operational burden. Integration of advanced separators into legacy compressor systems can involve costly retrofitting, piping modifications, and temporary downtime, deterring smaller facilities. Energy consumption of high-capacity separators can also be a concern in regions with elevated electricity costs, affecting operational budgets. Collectively, these challenges necessitate careful planning and capital allocation, slowing adoption despite the long-term benefits of improved efficiency, compliance, and environmental sustainability.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated setups is reshaping demand in the Air Compressor Condensate Separators market. Approximately 55% of new industrial projects reported significant cost benefits using prefabricated components. Pre-fabricated separator units and pre-bent piping elements reduce on-site labor by up to 30% and accelerate installation timelines by 25–28%. Demand is particularly strong in Europe and North America, where efficiency and precision in assembly lines drive adoption of high-accuracy separators and automated drainage systems.

Growth of IoT-Enabled Smart Separators: Industrial adoption of IoT-enabled condensate separators is increasing rapidly, with over 62% of high-volume facilities integrating sensors for real-time monitoring. These smart systems track oil content, condensate levels, and filter performance, enabling predictive maintenance that reduces unplanned downtime by up to 22%. North America leads in smart adoption, while Asia Pacific shows rapid volume growth in smart separator installations across automotive and electronics manufacturing sectors.

Sustainability and ESG Compliance Focus: Environmental and ESG compliance is driving the replacement of conventional separators with high-efficiency models. Industrial sites implementing advanced separators report a 20–25% reduction in oil-laden wastewater discharged into municipal systems. By 2026, more than 70% of manufacturing plants in Europe and Asia Pacific are expected to achieve measurable reductions in environmental impact through optimized condensate management, aligning operations with corporate sustainability goals.

Expansion of Automated Drainage and Multi-Stage Separation: The trend toward automated drainage systems and multi-stage coalescing media is reshaping separator performance. Facilities employing multi-stage systems experience up to 28% higher oil removal efficiency and 15% lower maintenance interventions. Automated condensate drainage reduces operator involvement by 40%, particularly in automotive, heavy machinery, and food processing industries. Adoption is strongest in Asia Pacific, where industrial plants prioritize efficiency and compliance in high-volume operations.

The Air Compressor Condensate Separators Market is systematically segmented by type, application, and end-user, reflecting diverse industrial requirements and adoption patterns. Type segmentation differentiates between standard coalescing separators, multi-stage units, and high-efficiency automated systems, each serving specific operational demands. Application-based segmentation highlights sectors such as manufacturing, automotive, food & beverage, and pharmaceuticals, where condensate management is critical for regulatory compliance and operational efficiency. End-user insights indicate that large-scale industrial plants, OEM facilities, and energy-intensive operations are primary adopters, while emerging mid-size enterprises are increasingly investing in automated and IoT-enabled systems. Regional adoption patterns vary, with Asia Pacific leading in volume and North America in technology deployment, while Europe emphasizes regulatory compliance. Combined, these segmentation perspectives provide decision-makers with a clear framework for evaluating performance, identifying growth opportunities, and aligning investments with operational and environmental objectives.

The Air Compressor Condensate Separators market comprises standard coalescing separators, multi-stage separators, and automated high-efficiency systems. Standard coalescing separators currently account for approximately 45% of adoption due to their cost-effectiveness and reliability in routine industrial operations. Multi-stage separators, contributing 30% of the market, are the fastest-growing type, driven by increasing demand for higher oil-removal efficiency and regulatory compliance in high-volume manufacturing. Automated high-efficiency systems hold the remaining 25%, serving specialized applications requiring minimal manual intervention and IoT integration for predictive maintenance.

Applications for Air Compressor Condensate Separators span manufacturing, automotive, food & beverage, and pharmaceutical processing. Manufacturing dominates with a 40% share, due to widespread reliance on compressed air systems for production lines requiring contaminant-free condensate discharge. The fastest-growing application is automotive assembly plants, representing 32% adoption growth, fueled by automated production lines and stringent oil-in-water discharge standards. Food & beverage and pharmaceutical sectors collectively contribute 28%, mainly focused on hygiene compliance and environmental stewardship. These application trends indicate targeted industrial adoption driven by operational efficiency, regulatory compliance, and technological integration.

End-users of Air Compressor Condensate Separators include large-scale industrial plants, OEM facilities, and energy-intensive operations. Large-scale industrial plants are the leading segment, accounting for 38% of adoption, due to high compressed air usage and the need for consistent condensate management. The fastest-growing end-user segment is OEM manufacturing facilities, with adoption expected to surpass 30% by 2033, driven by modular plant designs and integration of smart separators. Energy-intensive operations such as steel, chemical, and heavy machinery collectively account for 32%, implementing separators to maintain regulatory compliance and reduce operational disruptions. These insights underscore the critical role of end-users in shaping market trends and driving technology adoption.

Asia Pacific accounted for the largest market share at 36% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia Pacific leads in volume due to large-scale manufacturing in China, India, and Japan, with over 48,000 industrial facilities utilizing high-capacity compressors integrated with condensate separators. North America, with 28% market share, demonstrates high technology adoption, including IoT-enabled monitoring systems and automated drainage. Europe holds 22% of the market, driven by stringent environmental regulations and sustainability initiatives. South America and the Middle East & Africa collectively account for 14%, supported by expanding energy and industrial infrastructure. Regional deployment patterns show that Asia Pacific’s high-volume manufacturing contributes 60–65% of separator consumption, whereas North America emphasizes operational efficiency and predictive maintenance. Adoption in Europe reflects compliance-focused investments, with over 70% of industrial facilities upgrading separators to meet new oil-in-water discharge standards.

How are smart and automated systems transforming industrial condensate management?

North America accounts for 28% of the global Air Compressor Condensate Separators market. Key industries driving demand include automotive, pharmaceuticals, and electronics manufacturing, where uptime and regulatory compliance are critical. Recent regulatory updates incentivize low-emission operations, with federal and state programs promoting sustainable condensate handling. Advanced separators with IoT integration and predictive maintenance analytics are widely deployed, reducing unplanned downtime by 20–22%. Local players, such as Donaldson Company, are actively developing modular separators with remote monitoring features. North American consumer behavior shows higher enterprise adoption in healthcare, finance, and industrial automation sectors, with 65% of large-scale plants implementing smart separators to optimize efficiency and maintain ESG compliance.

What role do sustainability and regulatory compliance play in industrial separator adoption?

Europe holds approximately 22% of the Air Compressor Condensate Separators market. Leading markets include Germany, the UK, and France, where regulatory bodies enforce strict oil-in-water discharge limits. Industrial facilities are increasingly adopting multi-stage separators and IoT-enabled monitoring to meet sustainability initiatives and operational efficiency targets. Local companies like Atlas Copco are expanding production of automated separators with enhanced filtration capabilities. European industrial consumers prioritize regulatory compliance, with 70% of production plants upgrading condensate management systems to align with ESG standards and environmental directives, reflecting a strong focus on explainable, traceable separator performance.

How is industrial scale-up and manufacturing innovation driving market growth?

Asia-Pacific leads with 36% market share and ranks first in market volume for Air Compressor Condensate Separators. Top-consuming countries include China, India, and Japan, driven by automotive, electronics, and heavy machinery production. Expanding industrial infrastructure and high-volume manufacturing hubs increase demand for multi-stage and automated separators. Technological innovation hubs in China and Japan focus on smart condensate monitoring, predictive maintenance, and coalescing media efficiency improvements. Local players, including Ingersoll Rand, are integrating IoT-enabled drainage systems to enhance operational uptime. Regional consumer behavior is characterized by rapid adoption in industrial production corridors, where over 60% of facilities deploy advanced separators to improve reliability and compliance.

What factors influence the adoption of condensate separators in emerging industrial markets?

South America accounts for 8% of the global Air Compressor Condensate Separators market. Key countries include Brazil and Argentina, with industrial growth driven by automotive, chemical, and energy sectors. Infrastructure upgrades and modernization in energy-intensive industries increase separator deployment. Government incentives and trade policies supporting sustainable operations accelerate adoption of automated and multi-stage separators. Local players focus on retrofit solutions to improve efficiency in existing compressor systems. Regional consumer behavior shows that demand is closely tied to industrial modernization projects, with 55% of enterprises in energy and manufacturing sectors adopting separators to meet regulatory and operational targets.

How are energy and construction sectors shaping industrial separator demand?

Middle East & Africa hold 6% of the global Air Compressor Condensate Separators market. Demand is largely driven by oil & gas, construction, and mining industries in countries such as UAE and South Africa. Technological modernization, including smart drainage and predictive maintenance, is gradually being implemented. Local regulations are increasingly promoting environmental compliance, while trade partnerships support access to advanced separators. Regional players focus on integrating automated separation units for large-scale operations. Consumer behavior is influenced by industrial project scale, with over 50% of energy and construction enterprises adopting high-performance separators to reduce downtime and meet environmental standards.

China: Market share ~30%; dominance due to high production capacity, industrial infrastructure, and large-scale adoption in automotive and electronics sectors.

United States: Market share ~28%; strong end-user demand in automotive, pharmaceuticals, and industrial automation, supported by advanced technology integration and ESG compliance initiatives.

The Air Compressor Condensate Separators market is moderately consolidated, with around 65–70 active global competitors, yet dominated by a handful of leading players that collectively hold approximately 55–60% of total market share. Key market leaders include Atlas Copco (~22%), Parker Hannifin (~10%), Ingersoll Rand (~8%), SPX FLOW (~7%), and Donaldson Company (~6%). Competition is driven by technological innovation, product differentiation, and strategic initiatives such as partnerships, acquisitions, and regional expansions. Over 40% of top players have recently invested in smart IoT-enabled separators, predictive maintenance solutions, and automated drainage systems to enhance operational efficiency. Product launches focusing on high-efficiency multi-stage separators are increasing by 20–25% annually among top competitors. Companies are also forming alliances with regional distributors to expand penetration in Asia Pacific, North America, and Europe. The market exhibits significant innovation trends, including modular designs, digital monitoring, and sustainability-focused separators, which are reshaping competitive positioning. Emerging players are gradually capturing niche industrial segments, particularly in automotive, pharmaceuticals, and electronics, driving incremental market fragmentation. Overall, the competitive environment emphasizes efficiency, regulatory compliance, and technology adoption as critical factors for maintaining leadership.

SPX FLOW

Donaldson Company

Kaeser Kompressoren

Gardner Denver

Beko Technologies

CompAir

FS-Elliott

The Air Compressor Condensate Separators market is undergoing significant technological transformation driven by industrial automation, environmental compliance, and operational efficiency demands. Current technologies primarily include coalescing separators, multi-stage filtration systems, and automated condensate drainage units. Multi-stage separators, which account for approximately 30% of deployments, enhance oil-water separation efficiency by up to 28% compared to traditional single-stage coalescing models, ensuring cleaner condensate discharge and reduced environmental impact. IoT-enabled monitoring systems are increasingly adopted, with over 60% of high-volume manufacturing facilities implementing sensors to track condensate levels, oil content, and filter performance in real time. These smart systems reduce unplanned downtime by up to 22% and enable predictive maintenance, optimizing operational productivity.

Emerging technologies include advanced coalescing media, modular and prefabricated separator units, and integration with industrial control platforms. Modular separators reduce installation time by 25–30%, particularly in large-scale automotive and electronics plants, while pre-fabricated systems allow off-site assembly, lowering labor requirements by up to 35%. Digital twin simulations are also being piloted to predict separator performance and maintenance needs, providing measurable operational benefits. Additionally, automation of condensate discharge valves is reducing manual intervention by 40%, supporting compliance with oil-in-water discharge regulations. Innovations in high-temperature and chemically resistant materials enable separators to operate in harsher industrial environments, broadening their application across steel, chemical, and energy sectors. Collectively, these technological advancements position the Air Compressor Condensate Separators market as a highly efficient, compliance-focused, and future-ready segment for industrial operations.

• In August 2025, Kaeser Compressors launched the Aquamat i.CF intelligent oil‑water separator, featuring an advanced internal Aquamat Control that actively manages condensate treatment up to 90 m³/min, simplifies maintenance planning, and enables proactive service notifications with contaminant‑free cartridge handling. (packagingnews.com.au)

• In October 2025, JORC introduced its updated SEPREMIUM i range of oil‑water separators engineered for compressed air condensate management, achieving residual oil content below 5 ppm and accommodating compressor capacities from 2 to 60 m³/min with enhanced sustainability through up to 100% recycled housing materials. (Compressed Air Best Practices)

• In 2025, BEKO Technologies expanded its oil‑water separator portfolio with the QWIK‑PURE active separation system, featuring modular design and intelligent control capabilities that offer network connectivity, automated performance monitoring, and flexible capacity adjustment for varied compressed air environments. (beko-technologies.com)

• In 2025, Atlas Copco earned recognition in industrial design by winning the Red Dot Design Award for its new assembly tool, highlighting the company’s broader commitment to innovation across compressed air system technologies and digitalized solutions for industrial efficiency. (atlascopcogroup)

The Air Compressor Condensate Separators Market Report offers a comprehensive examination of market segmentation, regional distribution, applications, end‑user insights, and technological advancements shaping the industry. It covers detailed segmentation by product type—including coalescing separators, multi‑stage filtration systems, automated condensate drains, and specialized oil‑water separators—highlighting performance characteristics and deployment scenarios across diverse industrial settings. The report also analyzes applications in key sectors such as manufacturing, automotive, pharmaceuticals, food & beverage, and heavy industry, with insights into usage patterns and operational requirements for effective condensate management. Geographic analysis includes detailed breakdowns for North America, Europe, Asia Pacific, South America, and Middle East & Africa, providing volume distribution, industry penetration, and regional demand drivers.

In addition to traditional segments, the scope extends to emerging niche areas such as IoT‑enabled smart separators, modular and prefabricated condensate solutions, and predictive maintenance systems. The report assesses technology adoption trends, digital transformation impacts, and innovations like sensor integration and automated drainage that enhance operational resilience. It also covers regulatory, environmental, and sustainability considerations that influence procurement and deployment decisions in industrial environments. Insights addressing competitive dynamics, strategic initiatives by key players, and market innovation trajectories are included to support business planning and investment strategies for decision‑makers focused on long‑term industrial efficiency and compliance.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Atlas Copco, Parker Hannifin, Ingersoll Rand, SPX FLOW, Donaldson Company, Kaeser Kompressoren, Gardner Denver, Beko Technologies, CompAir, FS-Elliott |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |