Reports

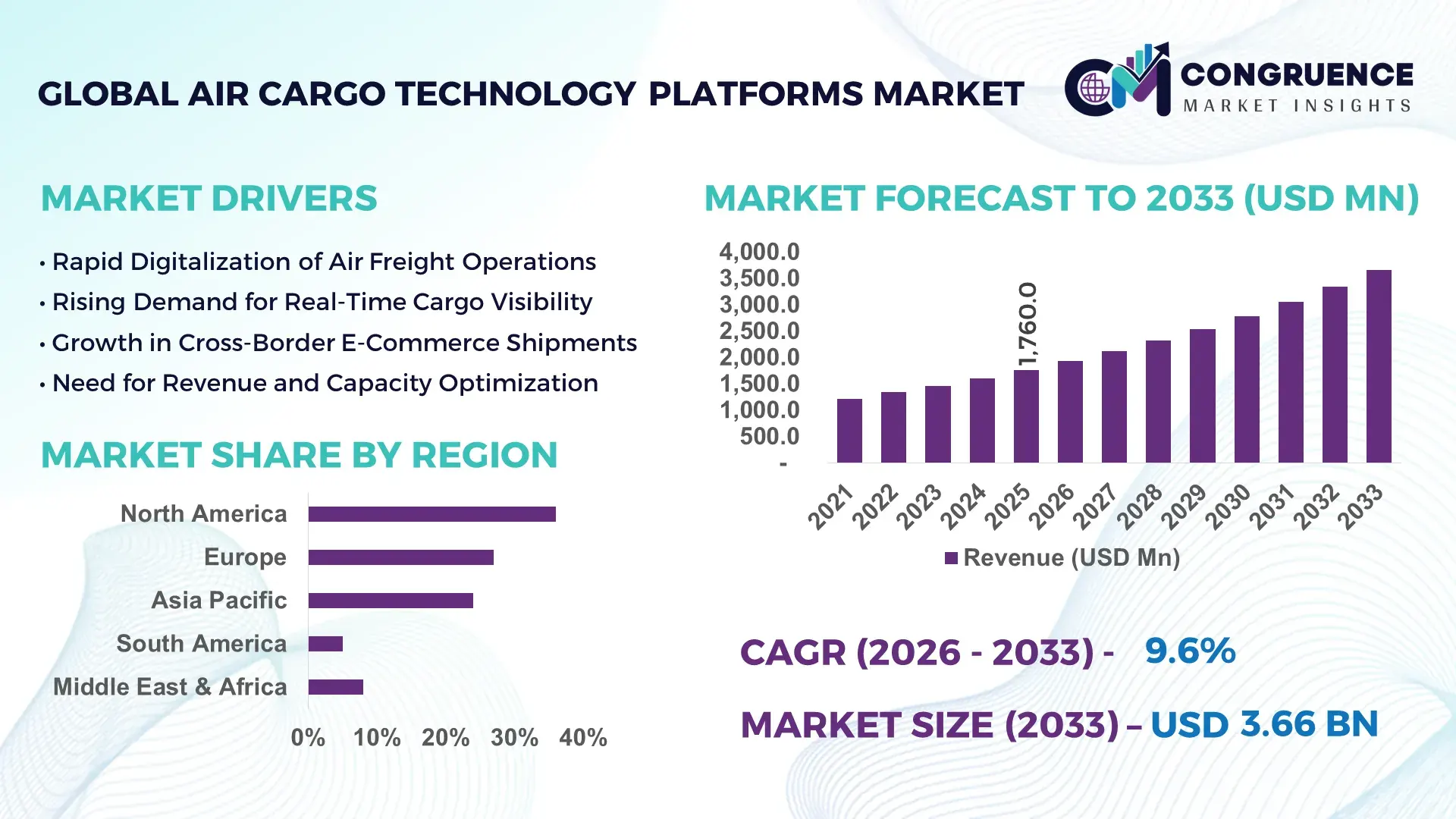

The Global Air Cargo Technology Platforms Market was valued at USD 1,760.0 Million in 2025 and is anticipated to reach a value of USD 3,664.4 Million by 2033 expanding at a CAGR of 9.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by accelerating digitalization across air freight operations, real-time cargo visibility requirements, and API-enabled ecosystem integration among airlines, freight forwarders, and ground handlers.

The United States stands as the dominant country in the Air Cargo Technology Platforms Market, supported by advanced aviation infrastructure and high digital maturity. The U.S. handles over 16 million metric tons of air cargo annually, with more than 70% of major cargo airports deploying automated cargo management and tracking platforms. Over USD 2.5 billion has been invested in air logistics digitization initiatives since 2020, including AI-based route optimization and IoT-enabled cargo tracking. Key applications include pharmaceutical cold-chain monitoring, e-commerce fulfillment integration, and customs pre-clearance automation. More than 60% of Tier-1 freight forwarders in the country use integrated API-driven booking systems, while automated warehouse robotics adoption exceeds 45% across large cargo hubs such as Memphis and Louisville.

Market Size & Growth: USD 1,760.0 Million (2025) projected to reach USD 3,664.4 Million by 2033 at 9.6% CAGR, driven by 40% rise in digital air freight transactions.

Top Growth Drivers: 65% adoption of real-time tracking tools; 48% improvement in cargo handling efficiency; 52% increase in API-based integrations.

Short-Term Forecast: By 2028, AI-based load optimization is expected to reduce cargo handling costs by 18% and improve on-time performance by 22%.

Emerging Technologies: AI-powered predictive analytics, blockchain-enabled airway bills, IoT-enabled smart containers.

Regional Leaders: North America (USD 1,280.0 Million by 2033, high API adoption), Asia Pacific (USD 1,050.0 Million, e-commerce integration surge), Europe (USD 890.0 Million, customs digitization acceleration).

Consumer/End-User Trends: Freight forwarders account for 42% usage; airlines 35%; integrators prioritize automated slot booking and dynamic pricing tools.

Pilot or Case Example: In 2024, a U.S.-based cargo hub implemented AI load planning, achieving 27% reduction in cargo misloads and 19% faster processing times.

Competitive Landscape: IBS Software (~18%), alongside CHAMP Cargosystems, CargoWise, SAP, and Oracle.

Regulatory & ESG Impact: 30% of global cargo operators aligning with digital customs mandates; 25% targeting carbon reporting automation.

Investment & Funding Patterns: Over USD 900 Million invested globally in air logistics tech startups between 2022–2025.

Innovation & Future Outlook: Integration of digital twins and predictive capacity modeling expected to enhance network resilience by 20%.

Freight forwarders contribute approximately 42% of platform demand, airlines 35%, and integrators 23%. Recent innovations include blockchain-enabled e-AWB systems and AI-driven dynamic pricing engines. Regulatory digitization mandates across North America and Europe are accelerating adoption. Asia Pacific shows strong consumption growth due to cross-border e-commerce expansion exceeding 18% annually. Sustainability-linked digital monitoring tools are shaping future procurement strategies among Tier-1 cargo operators.

The Air Cargo Technology Platforms Market holds strategic relevance as global trade becomes increasingly time-sensitive and digitally interconnected. Over 55% of air freight bookings are now processed through digital interfaces, compared to less than 30% a decade ago. Advanced AI-driven cargo optimization platforms deliver 20% improvement in load factor utilization compared to traditional manual planning systems. Similarly, blockchain-enabled electronic airway bills reduce documentation errors by 35% compared to paper-based standards.

North America dominates in cargo volume, while Asia Pacific leads in adoption with nearly 62% of large freight forwarders integrating cloud-based cargo management suites. By 2028, predictive AI analytics is expected to improve demand forecasting accuracy by 25%, reducing cargo spoilage and routing inefficiencies. ESG compliance is becoming integral, with firms committing to 30% carbon-emission visibility improvement by 2030 through automated sustainability dashboards.

In 2025, a leading U.S. cargo integrator achieved 24% reduction in transit delays through AI-enabled route recalibration and IoT-based container monitoring. The strategic pathway ahead includes deeper integration of digital twins, 5G-enabled cargo sensors, and cross-platform API standardization to enable seamless global trade corridors. As global supply chains prioritize resilience and compliance, the Air Cargo Technology Platforms Market will remain a foundational pillar supporting sustainable growth, operational transparency, and digital competitiveness.

The Air Cargo Technology Platforms Market is shaped by accelerating cross-border e-commerce, pharmaceutical logistics expansion, and increasing regulatory digitization mandates. Over 80% of global trade by value is transported by air for high-value goods, necessitating robust digital coordination systems. Airlines and freight forwarders are investing heavily in automated booking engines, cargo tracking dashboards, and AI-driven analytics to improve throughput efficiency and reduce dwell time. Additionally, customs authorities in more than 50 countries now require electronic documentation submission, reinforcing demand for integrated digital platforms. Technology convergence, including IoT sensors embedded in cargo containers and cloud-based data exchanges, is transforming cargo lifecycle visibility. However, integration complexity and cybersecurity risks remain structural considerations for operators deploying large-scale digital cargo ecosystems.

Global cross-border e-commerce shipments have increased by over 20% annually in recent years, significantly intensifying air freight volumes. More than 65% of international express parcels rely on air transport, demanding real-time tracking and automated booking platforms. Digital cargo platforms reduce booking cycle times by nearly 40% and improve shipment visibility accuracy by 30%, enabling operators to manage high parcel volumes efficiently. Additionally, over 70% of large freight forwarders now require API-enabled integration with airline systems to handle fluctuating demand patterns. Pharmaceutical and perishable goods shipments, which require temperature-sensitive monitoring, further increase reliance on IoT-enabled cargo platforms, strengthening demand for predictive analytics and automated exception management systems.

Despite rising adoption, nearly 38% of cargo operators report interoperability challenges between legacy systems and modern cloud platforms. Integration projects can extend deployment timelines by 25–30% due to incompatible data standards. Furthermore, air logistics networks process millions of shipment records daily, increasing exposure to cyber threats. In 2024, logistics-related cyber incidents rose by 17%, prompting stricter data security protocols. Smaller freight operators often lack the IT resources required for advanced encryption and compliance frameworks. These constraints slow platform upgrades and create hesitancy among mid-sized carriers, particularly in emerging economies where digital infrastructure maturity remains uneven.

AI-enabled demand forecasting tools improve route planning accuracy by 25% and reduce cargo spoilage by up to 18% in pharmaceutical shipments. Predictive maintenance analytics for ground handling equipment lowers unplanned downtime by 20%, increasing airport cargo throughput capacity. Emerging markets in Southeast Asia and the Middle East are expanding cargo airport infrastructure by over 15%, creating new deployment opportunities for cloud-native cargo platforms. Additionally, blockchain-based smart contracts reduce customs clearance time by 35%, presenting further efficiency gains. As 5G-enabled IoT sensor penetration in cargo containers surpasses 40% in advanced markets, real-time environmental monitoring offers strong growth potential.

Air cargo operators face increasing compliance requirements across more than 60 jurisdictions mandating digital reporting standards. Maintaining multi-country regulatory alignment raises IT operational costs by nearly 22%. Additionally, implementing advanced analytics and AI modules requires skilled workforce training, with digital transformation budgets rising by approximately 15% annually among Tier-1 operators. High upfront capital expenditure for system migration can delay return on investment. Variability in data-sharing protocols across airlines and ground handlers further complicates unified deployment strategies, limiting seamless cross-border integration.

AI-Driven Cargo Optimization Improving Load Efficiency by 20%: AI-based load planning systems are enhancing aircraft capacity utilization by up to 20% while reducing cargo misloads by 25%. Over 58% of major cargo hubs have implemented predictive analytics modules to optimize slot allocation and reduce dwell time by 18%, improving turnaround performance metrics.

Blockchain-Based e-AWB Adoption Exceeding 60% Across Major Routes: Electronic Air Waybill (e-AWB) usage now covers more than 60% of global air freight lanes, cutting documentation errors by 35% and reducing processing time by 28%. Customs digitization programs across 50+ countries are accelerating blockchain-backed validation systems.

IoT-Enabled Smart Containers Achieving 30% Visibility Gains: Approximately 45% of temperature-sensitive cargo shipments now use IoT sensors, improving real-time condition monitoring accuracy by 30%. Smart containers reduce spoilage incidents by 18% and enhance compliance reporting transparency by 25%.

Cloud-Native API Ecosystems Expanding Integration by 50%: More than 65% of freight forwarders utilize cloud-based APIs to integrate booking, pricing, and tracking functions. API standardization initiatives have improved partner onboarding speed by 50%, enabling faster digital collaboration across airline alliances and logistics providers.

The Air Cargo Technology Platforms Market is segmented by type, application, and end-user, reflecting the diverse operational requirements of airlines, freight forwarders, integrators, and logistics service providers. Platform architectures vary from comprehensive cargo management suites to API-first connectivity systems and visibility-focused tracking platforms. Application segmentation is driven by digital booking, shipment visibility, warehouse automation, revenue optimization, and customs documentation. End-user adoption differs based on operational scale and digital maturity, with Tier-1 airlines and global freight forwarders prioritizing integrated, cloud-native ecosystems, while regional carriers increasingly deploy modular SaaS platforms. Over 65% of enterprise-level cargo operators now utilize at least two interoperable digital systems to manage bookings and tracking. The market also demonstrates varying penetration across regions, where North America and Europe emphasize compliance-driven digital documentation, while Asia Pacific prioritizes high-volume e-commerce integration and automation scalability.

The market is broadly categorized into Cargo Management Platforms, API & Integration Platforms, Real-Time Visibility & Tracking Platforms, and Analytics & Optimization Platforms. Cargo Management Platforms currently account for approximately 38% of adoption, as they centralize booking, pricing, airway bill processing, and capacity management within a unified environment. API & Integration Platforms hold nearly 27%, enabling seamless connectivity among airlines, freight forwarders, and customs authorities. However, Real-Time Visibility & Tracking Platforms are expanding fastest, projected to grow at an estimated 12.8% CAGR, driven by IoT-enabled sensors and regulatory mandates for shipment transparency. Analytics & Optimization Platforms, contributing a combined 20% share alongside niche digital twin modules, are gaining importance for predictive load planning and dynamic pricing. Their adoption is increasing among Tier-1 operators seeking measurable gains in route efficiency and asset utilization.

Key applications include Digital Booking & Capacity Management, Shipment Tracking & Visibility, Warehouse & Ground Handling Automation, Revenue Optimization, and Customs & Compliance Management. Digital Booking & Capacity Management leads with approximately 34% share due to rising demand for instant rate quotation and automated slot allocation. Shipment Tracking & Visibility accounts for 28%, while Warehouse Automation represents nearly 18%. However, Revenue Optimization and Predictive Analytics applications are expanding fastest, growing at an estimated 13.4% CAGR as airlines seek dynamic pricing models and 20%+ improvements in load factor utilization. Other applications collectively contribute around 20%, including sustainability monitoring dashboards and cargo insurance automation. In 2025, more than 46% of global freight forwarders reported deploying AI-enabled booking systems to streamline rate comparison and routing. Additionally, nearly 58% of pharmaceutical logistics providers adopted IoT-based tracking for temperature-sensitive cargo compliance.

The primary end-users include Airlines, Freight Forwarders, Integrated Express Carriers, and Third-Party Logistics Providers (3PLs). Freight Forwarders lead with approximately 42% adoption, leveraging digital platforms for multi-carrier rate comparison, documentation automation, and end-to-end shipment visibility. Airlines account for around 35%, focusing on capacity optimization and revenue management integration. Integrated express carriers represent nearly 15%, while 3PLs and niche operators collectively contribute about 8%. Although freight forwarders dominate usage, airlines represent the fastest-growing end-user segment with an estimated 11.9% CAGR, driven by in-house digital transformation strategies and AI-enabled cargo revenue systems. Over 62% of Tier-1 airlines have invested in predictive load optimization and automated documentation workflows. In 2025, approximately 48% of logistics enterprises globally reported piloting advanced cargo analytics platforms to enhance network planning accuracy.

North America accounted for the largest market share at 36% in 2025 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

North America processed over 16 million metric tons of air cargo in 2025, with more than 68% of Tier-1 cargo hubs operating advanced digital cargo management systems. Europe followed with approximately 27% share, driven by cross-border trade across 27 EU member states and over 60% e-AWB penetration on intra-European routes. Asia Pacific held nearly 24% share, supported by high-volume e-commerce shipments exceeding 3.2 billion cross-border parcels annually. The Middle East & Africa represented about 8%, benefiting from transshipment hubs handling over 6 million metric tons collectively, while South America accounted for roughly 5%, with Brazil managing nearly 2 million metric tons of air freight yearly. Regional variations in customs digitization rates, automation intensity, and API adoption levels significantly influence deployment speed and integration complexity across markets.

North America holds approximately 36% share of the global Air Cargo Technology Platforms Market, supported by large-scale cargo hubs and enterprise digital maturity. Key industries driving demand include pharmaceuticals, aerospace components, high-value electronics, and express e-commerce logistics, which collectively account for more than 55% of technology platform usage. Over 70% of major airports in the region deploy automated cargo community systems integrating booking, tracking, and customs data exchange. Regulatory frameworks mandate electronic documentation and security screening compliance across 100% of international cargo movements. Technological transformation is evident in AI-based load optimization systems improving capacity utilization by up to 20% and IoT-enabled temperature monitoring used in over 50% of pharmaceutical shipments. IBS Software, a regional technology provider, has expanded AI-driven cargo revenue management modules to enhance predictive demand planning for major carriers. Regional enterprise behavior shows higher early adoption among healthcare and express logistics operators, with nearly 60% of large freight forwarders utilizing cloud-based API integrations for multi-carrier operations.

Europe represents approximately 27% of the Air Cargo Technology Platforms Market, led by Germany, the United Kingdom, and France, which collectively account for over 60% of the region’s digital cargo deployments. More than 65% of intra-European air freight lanes utilize electronic airway bill systems, reflecting strong compliance alignment. Sustainability initiatives under EU carbon reduction frameworks are influencing over 40% of cargo operators to integrate emissions tracking dashboards within their platforms. Adoption of blockchain-enabled customs documentation and AI-powered slot allocation tools has increased by nearly 30% across major logistics corridors. CHAMP Cargosystems, headquartered in Luxembourg, continues to expand digital cargo community platforms across multiple European hubs, enabling integrated airline-forwarder data exchange. Regional consumer behavior indicates that regulatory pressure encourages demand for explainable AI modules and standardized API frameworks, particularly among mid-sized carriers managing multi-country operations.

Asia-Pacific accounts for nearly 24% of the global Air Cargo Technology Platforms Market and ranks first in cargo volume growth. China, India, and Japan collectively handle over 45% of the region’s air freight throughput. China alone processes more than 7 million metric tons annually, while India’s dedicated air cargo capacity has expanded by over 18% in the past three years. Infrastructure investments in smart airports and automated cargo terminals exceed 25 major projects across the region. Technology adoption trends highlight over 50% integration of mobile-based booking applications among regional freight operators. Cloud-native cargo systems are widely deployed in cross-border e-commerce, where parcel volumes have grown beyond 3 billion annually. CargoWise, widely used by freight forwarders across Asia-Pacific, continues expanding automation features for customs compliance and multi-modal tracking. Consumer behavior in the region is driven by e-commerce and mobile-first logistics management, with more than 62% of SMEs preferring digital self-service booking tools.

South America holds approximately 5% of the global Air Cargo Technology Platforms Market, with Brazil and Argentina serving as key contributors. Brazil handles nearly 2 million metric tons of air freight annually, supporting pharmaceutical, agribusiness, and automotive exports. Infrastructure modernization projects in São Paulo and Rio de Janeiro have increased automated cargo handling capacity by over 15%. Government trade facilitation programs emphasize electronic customs documentation and digital freight corridors across Mercosur nations. Over 40% of international shipments from major Brazilian hubs now use digital booking and tracking platforms. Regional demand is also linked to agricultural exports requiring temperature-controlled monitoring systems. Logistics operators increasingly deploy API-driven platforms to enhance cross-border compliance and visibility, reflecting a gradual shift toward cloud-based cargo ecosystems.

Can Strategic Transshipment Hubs Drive Next-Generation Cargo Digitization?

The Middle East & Africa region accounts for roughly 8% of the Air Cargo Technology Platforms Market, anchored by the UAE and South Africa. The UAE manages more than 2.5 million metric tons of cargo annually through advanced transshipment hubs, with over 75% of shipments processed using digital documentation systems. Oil & gas equipment, perishables, and re-export trade flows significantly influence platform deployment. Technological modernization includes smart cargo terminals integrating IoT-enabled monitoring and automated customs pre-clearance systems. Emirates SkyCargo continues investing in AI-enabled load optimization and predictive capacity planning modules to streamline global trade routes. Regional trade partnerships across Africa are accelerating cross-border data exchange frameworks. Consumer behavior trends show increasing preference for integrated, multilingual digital platforms that support diverse regulatory environments and multi-country shipping corridors.

United States – 31% Market Share: Strong aviation infrastructure, high enterprise digital adoption, and advanced AI-based cargo management deployment drive leadership in the Air Cargo Technology Platforms Market.

Germany – 12% Market Share: Central European logistics hub status, high electronic airway bill penetration, and regulatory-driven digital compliance frameworks strengthen Germany’s position in the Air Cargo Technology Platforms Market.

The Air Cargo Technology Platforms Market demonstrates a moderately fragmented structure, with more than 45 active global and regional technology providers competing across cargo management, API connectivity, visibility platforms, and analytics solutions. The top five companies collectively account for approximately 48% of total market presence, reflecting a competitive yet innovation-driven landscape. Market leaders differentiate through integrated end-to-end cargo suites that combine booking, tracking, revenue management, and customs data exchange in a single architecture.

Strategic initiatives between 2023 and 2025 include over 30 recorded partnerships between airlines and software vendors to modernize legacy cargo systems. More than 20% of competitive contracts awarded in 2024 involved AI-enabled optimization modules. Product launches increasingly emphasize cloud-native deployment, with nearly 65% of new contracts favoring SaaS-based subscription models over on-premise installations.

Mergers and ecosystem alliances are shaping consolidation trends, particularly among API platform providers seeking standardized data exchange capabilities. Competitive positioning now heavily depends on integration flexibility, cybersecurity compliance, and scalability across high-volume cargo hubs processing over 1 million metric tons annually. Vendors offering IoT-enabled container tracking and blockchain-based e-AWB validation are gaining traction, as approximately 60% of large freight forwarders prioritize real-time visibility as a procurement criterion.

Overall, competition is centered on innovation intensity, interoperability depth, and enterprise-grade analytics capabilities rather than price differentiation alone.

SAP

Oracle

Accelya

Awery Aviation Software

Unisys

Kale Logistics Solutions

SITA

Descartes Systems Group

Freightos

Magaya Corporation

WiseTech Global

Lufthansa Industry Solutions

Technological advancement within the Air Cargo Technology Platforms Market is centered on automation, predictive intelligence, and secure data interoperability. AI-powered predictive analytics systems now improve load factor optimization by up to 20% and reduce route deviation by nearly 18%. Over 58% of large cargo hubs have deployed machine-learning models to forecast peak shipment windows and optimize warehouse throughput.

IoT-enabled smart containers are transforming shipment visibility. Approximately 45% of pharmaceutical and perishable cargo shipments use real-time temperature and humidity sensors, reducing spoilage incidents by nearly 18%. Integration of 5G connectivity at major airports enables latency reductions of up to 30% in real-time cargo status updates.

Blockchain-backed electronic Air Waybill (e-AWB) systems are now implemented across more than 60% of international trade lanes, cutting documentation discrepancies by 35% and reducing customs clearance time by 28%. API-first architectures dominate new deployments, with over 65% of freight forwarders preferring modular integration frameworks for scalability.

Digital twin simulations are emerging in large cargo hubs to model aircraft turnaround times, improving planning efficiency by nearly 15%. Cybersecurity technologies, including zero-trust architectures and encrypted API gateways, have seen adoption increases of 25% since 2023 due to rising logistics-related cyber incidents.

Edge computing is also expanding in automated cargo terminals, allowing data processing at the warehouse level and decreasing system response times by approximately 22%. These advancements collectively enhance transparency, reduce dwell time, and strengthen compliance management across global air freight networks.

• In October 2025, IBS Software launched its new Agentic AI virtual agents across the iCargo platform at the 25th Cargo Forum in New Delhi**, introducing conversational, predictive AI copilots for cargo tasks such as revenue management, customer service, mail management, and sales — designed to reduce manual effort and enhance operational accuracy and responsiveness across airline and handler workflows. Source: www.ibsplc.com

• In November 2025, Delta Cargo completed a full implementation of IBS Software’s iCargo platform across 252 global cargo stations, replacing legacy systems and enabling real-time integration, terminal operations automation, customs and security handling, and enhanced data consistency for over 6,500 users, supporting streamlined shipment processing and improved service delivery. Source: www.pr.comtex.com

• In April 2025, CargoWise expanded carrier connectivity with All Nippon Airways (ANA), enabling freight forwarders to plan, book, confirm, and manage air cargo shipments in real time directly within the CargoWise platform — enhancing operational control and booking automation for one of Japan’s largest airlines. Source: www.cargowise.com

• In April 2025, CHAMP Cargosystems’ 1Neo-Connect service facilitated a ONE Record integration between Saudia Cargo and Worldwide Flight Services (WFS), standardizing shipment data exchange and improving real-time status visibility and planning efficiency for both the airline and ground handler through CHAMP’s flexible API-enabled connectivity platform. Source: www.stattimes.com

The Air Cargo Technology Platforms Market Report provides comprehensive coverage of platform-based digital solutions supporting global air freight operations. The scope encompasses segmentation by platform type, including cargo management suites, API integration frameworks, real-time visibility systems, analytics engines, and blockchain-enabled documentation modules. Applications covered include booking automation, shipment tracking, warehouse digitization, customs compliance, sustainability monitoring, and revenue optimization.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, collectively representing over 95% of global air cargo throughput exceeding 65 million metric tons annually. The report evaluates adoption intensity across leading economies such as the United States, Germany, China, India, the UAE, and Brazil.

Industry focus areas include pharmaceuticals, e-commerce logistics, aerospace components, perishables, and high-value electronics, which together represent more than 60% of air freight digital platform usage. Technology analysis incorporates AI-driven predictive tools, IoT-enabled monitoring devices, blockchain-based e-AWB frameworks, cloud-native SaaS deployment models, cybersecurity protocols, and digital twin simulations.

The report further examines enterprise adoption trends among airlines, freight forwarders, integrators, and 3PL providers, including deployment scale, integration complexity, automation levels, and compliance alignment across over 50 regulatory jurisdictions. Emerging niches such as carbon tracking dashboards and smart cargo corridors are also evaluated, ensuring a forward-looking and decision-centric market perspective.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,760.0 Million |

| Market Revenue (2033) | USD 3,664.4 Million |

| CAGR (2026–2033) | 9.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBS Software; CHAMP Cargosystems; CargoWise; SAP; Oracle; Accelya; Awery Aviation Software; Unisys; Kale Logistics Solutions; SITA; Descartes Systems Group; Freightos; Magaya Corporation; WiseTech Global; Lufthansa Industry Solutions |

| Customization & Pricing | Available on Request (10% Customization Free) |