Reports

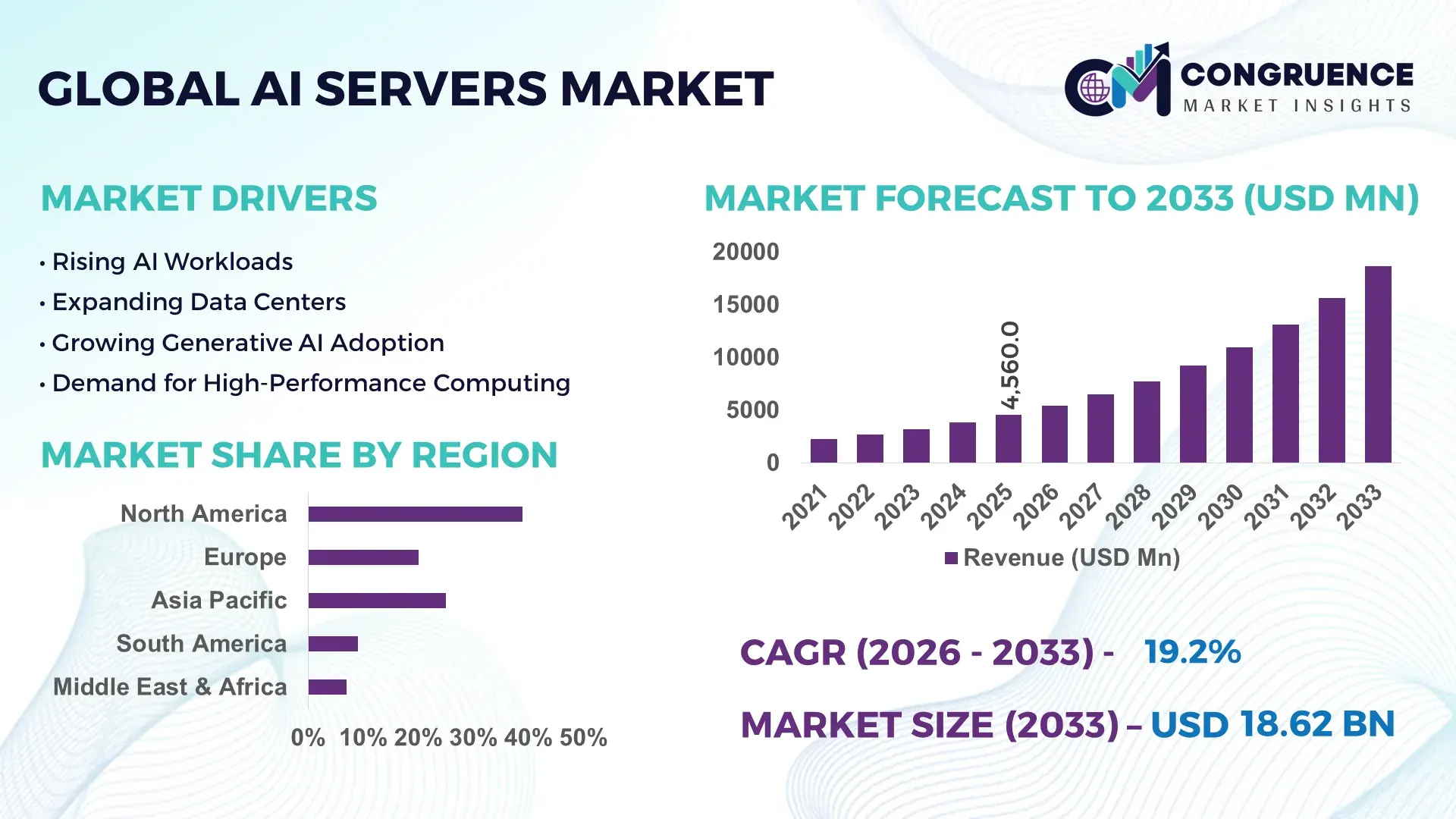

The Global AI Servers Market was valued at USD 4560 Million in 2025 and is anticipated to reach a value of USD 18622.98 Million by 2033 expanding at a CAGR of 19.23% between 2026 and 2033. Rising deployment of generative AI workloads, accelerated hyperscale data center expansion, and enterprise migration toward GPU-intensive computing platforms are driving high-performance AI server adoption across cloud, telecom, healthcare, and automotive sectors.

The United States leads the global AI servers market with nearly 38% deployment share, supported by over 45 GW hyperscale data center capacity and aggressive investments from cloud and semiconductor firms focused on advanced AI infrastructure. China follows with strong domestic AI chip integration and state-backed computing expansion, accounting for approximately 27% of regional AI server installations despite ongoing semiconductor export restrictions. Japan and South Korea are accelerating liquid-cooled AI server deployments, with enterprise AI adoption rates surpassing 41% in manufacturing and robotics-driven industries by 2026.

Strategic competition around AI compute sovereignty, energy-efficient architectures, and advanced chip packaging is reshaping vendor expansion priorities and long-term infrastructure investment decisions across global enterprise markets.

Market Size & Growth: USD 4560 Million in 2025 reaching USD 18622.98 Million by 2033 at 19.23% growth, driven by generative AI training clusters and hyperscale GPU server expansion.

Top Growth Drivers: AI model training demand increased 42%, liquid cooling adoption rose 31%, and enterprise edge AI deployments expanded 28% in 2026.

Short-Term Forecast: By 2028, AI server power efficiency improves 26% while data center processing latency declines nearly 19% through advanced accelerator integration.

Emerging Technologies: High-density GPU racks, liquid immersion cooling, and AI-specific ARM architectures improve compute utilization by over 33% across advanced server environments.

Regional Leaders: North America exceeds USD 6.8 Billion with hyperscale expansion, Asia-Pacific crosses USD 5.9 Billion via sovereign AI programs, and Europe reaches USD 3.7 Billion through industrial AI automation.

Consumer/End-User Trends: Over 61% of large enterprises prioritize AI-ready server infrastructure to support generative AI, predictive analytics, and real-time inference workloads.

Pilot/Case Example: In 2026, a telecom AI infrastructure upgrade reduced inference processing time by 37% and lowered server energy consumption by 18%.

Competitive Landscape: NVIDIA-linked AI server ecosystems control approximately 36% market influence, with Dell, Supermicro, HPE, Lenovo, and Inspur expanding high-density AI portfolios.

Regulatory & ESG Impact: Liquid-cooled AI servers reduce cooling-related energy use by nearly 30% amid tightening European and Asian data center efficiency regulations.

Investment & Funding: Global AI infrastructure investments surpassed USD 48 Billion in 2026, supported by cloud partnerships, sovereign AI initiatives, and semiconductor localization programs.

Innovation & Future Outlook: Rack-scale AI systems, photonic interconnects, and modular accelerator designs are accelerating next-generation high-growth AI computing infrastructure strategies.

AI servers are witnessing accelerated adoption across cloud computing, autonomous mobility, financial analytics, and healthcare imaging environments where large-scale AI processing requires high-density computing architectures. Advanced liquid cooling systems and next-generation GPU integrations improved workload efficiency by nearly 29% in 2026 while reducing thermal bottlenecks in hyperscale facilities. Simultaneously, regional semiconductor localization initiatives and stricter energy-efficiency mandates are reshaping procurement strategies, supply-chain partnerships, and long-term infrastructure planning across the global AI servers ecosystem.

AI servers have become strategically critical as enterprises compete for AI processing capacity, low-latency inference infrastructure, and sovereign computing control. The market is reshaping hyperscale investment strategies, semiconductor alliances, and enterprise IT modernization programs across finance, automotive, telecom, and healthcare sectors. Supply-chain restructuring after U.S.–China semiconductor restrictions accelerated localized AI server manufacturing and advanced chip packaging investments in Taiwan, South Korea, and India. By 2026, over 58% of hyperscale operators are prioritizing AI-optimized rack deployments over traditional compute expansion to support generative AI workloads and real-time analytics environments.

Modern GPU-accelerated AI servers deliver nearly 4.5x higher parallel processing efficiency than legacy CPU-centric enterprise systems while reducing training-cycle completion time by approximately 36%. The United States leads in large-scale AI cluster deployment through hyperscale cloud ecosystems, while Japan and Germany are focusing on energy-efficient AI infrastructure for industrial automation and smart manufacturing. Liquid-cooled AI server installations increased by 31% in 2026 as operators targeted lower thermal overhead and improved rack-density utilization.

A practical example is telecom providers deploying edge AI servers to reduce network inference latency by nearly 28% for 5G traffic optimization and cybersecurity analytics. Companies are expanding strategic partnerships with semiconductor firms, cooling technology providers, and cloud infrastructure operators to secure long-term compute capacity. Over the next three years, competitive advantage will increasingly depend on AI infrastructure scalability, energy efficiency, and integrated hardware-software optimization capabilities.

Enterprise demand for high-density AI computing infrastructure is accelerating due to large language model deployment, autonomous systems, and industrial AI automation. In 2026, AI-related workloads accounted for nearly 43% of new hyperscale server procurement, while liquid-cooled rack adoption expanded by 31% across major data center operators. U.S. cloud providers and Taiwan-based hardware manufacturers increased advanced AI server production capacity following semiconductor export restrictions and rising GPU allocation pressure. This shift directly improved deployment speed and compute availability for enterprise AI training clusters. Companies are responding through vertical integration, strategic GPU supply agreements, and co-development partnerships with semiconductor and cooling technology vendors. A key operational insight is that enterprises prioritizing AI-specific infrastructure are reducing model training turnaround times by over 34%, strengthening competitive positioning in AI-driven digital services.

The AI servers market faces structural pressure from semiconductor concentration risk, rising energy consumption, and infrastructure bottlenecks. More than 68% of advanced AI server deployments remain dependent on limited high-performance GPU supply chains concentrated in Taiwan and South Korea, exposing manufacturers to geopolitical and logistics disruptions. In 2026, average AI server power density exceeded 40 kW per rack in large training clusters, creating grid and cooling limitations for older data center facilities. These constraints are increasing deployment costs and slowing enterprise-scale implementation timelines. Companies in Germany, Japan, and India are responding through localized component sourcing, long-term semiconductor procurement contracts, and investment in alternative accelerator architectures. A major strategic concern is that insufficient power and cooling modernization directly reduces server utilization efficiency and weakens operational scalability for high-performance AI workloads.

Rapid adoption of edge AI processing and modular server architectures is creating high-value expansion opportunities across telecom, manufacturing, and smart mobility industries. By 2027, nearly 46% of enterprise AI inference workloads are expected to shift closer to edge environments to reduce latency and bandwidth costs. Japan and India are accelerating deployment of compact AI server nodes for industrial robotics, video analytics, and smart city applications, while modular liquid-cooled systems are improving rack-space efficiency by approximately 29%. Governments are also supporting sovereign AI infrastructure initiatives to strengthen domestic computing capacity and reduce external semiconductor dependency. Companies are increasing investment in edge-focused AI server platforms, advanced networking integration, and regional data center partnerships. A notable strategic advantage is that modular AI infrastructure enables faster deployment cycles and lower operational overhead for distributed AI environments.

Long-term market scalability is increasingly challenged by integration complexity, thermal management pressure, and AI infrastructure sustainability requirements. More than 52% of enterprises deploying AI servers report compatibility issues between legacy enterprise systems and accelerator-driven architectures, particularly in financial services and industrial automation environments. At the same time, high-density AI clusters generate substantially higher cooling demand, with some hyperscale facilities recording cooling-related energy loads above 35% of total operational consumption in 2026. Cybersecurity risks linked to AI inference networks and distributed training environments are also expanding operational vulnerability. Companies are investing in unified orchestration software, advanced liquid cooling systems, and zero-trust security frameworks to stabilize deployment consistency. A critical strategic insight is that firms unable to optimize interoperability and infrastructure efficiency risk lower AI workload performance and weaker long-term infrastructure competitiveness.

Liquid Cooling Deployment Surge AI server rack densities crossed 40–60 kW in 2026, pushing liquid cooling adoption above 31% in hyperscale facilities across the United States and Japan. Operators are restructuring data center layouts to reduce thermal overhead by nearly 27% while improving compute utilization rates. Stricter energy-efficiency regulations and rising electricity costs are accelerating immersion cooling partnerships between server manufacturers and infrastructure providers, particularly for large language model training clusters.

Localized AI Hardware Ecosystems Semiconductor export controls and logistics instability are driving localized AI server manufacturing and component sourcing strategies. India increased domestic AI infrastructure incentives in 2026, while Taiwan-based suppliers expanded regional assembly operations to shorten deployment cycles by nearly 22%. Enterprises are reducing dependence on single-country GPU supply chains through multi-vendor procurement, advanced chip packaging collaboration, and regional integration hubs focused on operational continuity and faster AI infrastructure scaling.

Edge Inference Infrastructure Expansion Enterprise edge AI server deployments increased approximately 34% in telecom, manufacturing, and retail environments where real-time inference is becoming operationally critical. Compact AI servers integrated with 5G networks reduced industrial processing latency by nearly 26% in smart factory applications. Companies are scaling distributed inference nodes and adopting modular server architectures to support video analytics, predictive maintenance, and autonomous operational workflows without excessive cloud-processing dependency.

AI-Optimized Server Automation AI server vendors are integrating automated workload orchestration and predictive infrastructure management tools to improve operational efficiency. Automated resource allocation reduced server idle capacity by approximately 19% in large enterprise environments during 2026. Germany-based industrial operators and U.S. hyperscale firms are expanding software-defined infrastructure partnerships to streamline GPU utilization, lower maintenance intervention, and stabilize AI training performance amid increasing computational complexity and workforce shortages.

GPU servers dominate the AI servers market due to superior parallel processing capability, high-bandwidth memory integration, and optimized support for generative AI training workloads. In 2026, GPU-based systems accounted for nearly 57% of advanced AI infrastructure deployments across hyperscale cloud operators and enterprise research environments. Their ability to reduce AI model training time by approximately 38% compared to traditional CPU-centric systems continues to strengthen adoption in financial modeling, autonomous systems, and healthcare analytics. Major server manufacturers are expanding GPU-focused product portfolios through direct semiconductor partnerships, liquid-cooled rack integration, and scalable accelerator architectures to secure long-term enterprise contracts.

Edge AI servers are emerging as the fastest-growing segment as telecom providers, manufacturers, and retail operators prioritize low-latency inference processing closer to operational environments. Deployment volumes for edge AI servers increased by nearly 33% in 2026, particularly in Japan and India where industrial automation and smart surveillance projects are accelerating. CPU servers remain strategically relevant for hybrid workloads and enterprise orchestration layers, while rack servers continue dominating hyperscale installations due to scalability advantages. Blade servers are gaining traction in space-constrained enterprise facilities requiring higher compute density and centralized infrastructure management.

Cloud computing remains the leading application segment within the AI servers market due to hyperscale AI training demand, enterprise migration toward AI-as-a-service platforms, and large-scale data orchestration requirements. In 2026, nearly 49% of AI server deployments were linked directly to cloud-based AI infrastructure environments supporting generative AI, predictive analytics, and enterprise automation platforms. Hyperscale operators increased deployment of AI-optimized rack systems by approximately 29% to support rising inference traffic and multi-tenant AI processing. Companies are expanding cloud partnerships, integrating accelerator-specific architectures, and automating infrastructure scaling to stabilize operational efficiency and reduce AI processing latency.

Natural Language Processing is emerging as the fastest-growing application as enterprises integrate conversational AI, multilingual automation, and AI-driven enterprise search tools into customer operations and workflow systems. NLP-focused server demand expanded by approximately 36% in 2026 following rapid adoption of generative AI platforms across banking, healthcare, and telecom sectors. Machine Learning and Data Analytics continue supporting mature enterprise AI workloads, while Computer Vision adoption is accelerating in manufacturing quality inspection, autonomous mobility, and intelligent retail analytics. Vendors are prioritizing optimized inference servers and distributed processing architectures to support increasingly complex AI application ecosystems.

IT and Telecom represent the dominant end-user segment due to large-scale hyperscale infrastructure ownership, AI-driven network optimization requirements, and continuous demand for low-latency computing environments. In 2026, the sector accounted for nearly 41% of enterprise AI server deployments, supported by accelerated 5G infrastructure expansion and growing generative AI traffic management requirements. Telecom operators deploying AI inference servers reduced network anomaly response times by approximately 24%, improving operational continuity and service reliability. Leading vendors are strengthening telecom-focused AI infrastructure offerings through edge-compute partnerships, customized rack-scale systems, and integrated network orchestration platforms.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and research institutions expand AI-powered imaging, genomic analysis, and clinical decision support systems. AI server deployment in healthcare environments increased nearly 32% during 2026, particularly across the United States and South Korea where diagnostic automation initiatives accelerated. BFSI firms continue investing in fraud detection and risk analytics infrastructure, while manufacturing companies prioritize predictive maintenance and machine vision processing. Government agencies and retail enterprises are also increasing AI server procurement for cybersecurity, surveillance analytics, and personalized digital commerce operations.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2026 and 2033.

Hyperscale Infrastructure Dominates AI Compute Expansion

North America maintains leadership in the AI servers market through hyperscale cloud concentration, advanced semiconductor integration, and aggressive enterprise AI deployment activity. The region accounted for approximately 39% of global AI server installations in 2025, supported by large-scale data center clusters across the United States and Canada. AI-focused server rack density increased by nearly 28% during 2026 as hyperscale operators expanded GPU-intensive training infrastructure for generative AI workloads. Telecom and financial enterprises accelerated adoption of liquid-cooled AI systems to reduce thermal inefficiencies and stabilize inference performance. Strategic partnerships between cloud providers, semiconductor firms, and infrastructure specialists are strengthening deployment scalability and accelerating integrated AI compute modernization across enterprise ecosystems.

United States Market Outlook: The United States remains the core operational hub for AI server deployment due to hyperscale cloud leadership, advanced semiconductor ecosystem integration, and enterprise AI acceleration. More than 45 GW of hyperscale data center capacity supports large-scale AI infrastructure expansion, while enterprise AI workload deployment increased by approximately 34% in 2026. Government-backed semiconductor manufacturing incentives and localized chip packaging investments are improving supply-chain resilience. Major enterprises are prioritizing vertically integrated AI infrastructure strategies combining GPU acceleration, advanced cooling systems, and AI orchestration software to secure long-term compute availability and operational efficiency.

Energy-Efficient AI Infrastructure Reshaping Deployment Priorities

Europe is strengthening its AI servers market position through sustainable infrastructure modernization, industrial AI adoption, and stricter energy-efficiency frameworks. Germany, France, and the Netherlands are leading deployment of advanced liquid-cooled AI servers across industrial automation and enterprise cloud environments. In 2026, nearly 32% of newly commissioned AI server facilities in Europe incorporated high-efficiency cooling architectures to reduce operational energy loads. Regulatory pressure around carbon reduction and data sovereignty is driving investment in localized AI infrastructure and sovereign cloud ecosystems. Enterprises are increasingly adopting modular AI server designs and workload optimization tools to improve compute efficiency while controlling power consumption across high-density AI clusters.

Germany Market Outlook: Germany leads the European AI servers market through strong industrial automation infrastructure, advanced manufacturing ecosystems, and enterprise AI modernization initiatives. Manufacturing firms increased AI-enabled server deployments by approximately 27% in 2026 to support machine vision, predictive maintenance, and digital twin applications. The country’s emphasis on industrial AI integration and energy-efficient computing environments is accelerating demand for compact high-performance AI server systems. Domestic enterprises are also strengthening partnerships with semiconductor and infrastructure vendors to improve deployment scalability and compliance with evolving European sustainability standards.

Large-Scale Manufacturing and AI Deployment Acceleration

Asia-Pacific is emerging as the fastest-expanding AI servers market due to semiconductor manufacturing concentration, hyperscale data center expansion, and rising enterprise AI integration across China, Japan, South Korea, and India. The region accounted for nearly 34% of global AI server deployment activity in 2025, supported by strong electronics manufacturing ecosystems and state-backed AI infrastructure programs. AI-focused data center construction activity increased by approximately 36% during 2026 as enterprises scaled generative AI and industrial automation capabilities. Semiconductor packaging innovation and localized hardware production are also reducing deployment lead times and improving infrastructure availability. Companies are prioritizing regional manufacturing expansion and strategic supply-chain diversification to support rapidly growing AI compute demand.

China Market Outlook: China remains a major AI server deployment and manufacturing hub due to strong domestic AI adoption, large-scale cloud ecosystems, and government-backed semiconductor development programs. Enterprise AI infrastructure procurement increased by approximately 31% in 2026 across smart manufacturing, financial analytics, and intelligent surveillance applications. Domestic firms are accelerating investment in alternative accelerator architectures and localized server manufacturing to reduce external semiconductor dependency. High-density AI server installations are also expanding rapidly within major urban data center corridors to support growing generative AI inference and enterprise automation workloads.

Enterprise Digitalization Expands AI Infrastructure Demand

South America is witnessing gradual expansion in AI server adoption driven by enterprise digital transformation, telecom modernization, and increasing cloud infrastructure deployment. Brazil and Chile are leading regional AI infrastructure investment as enterprises modernize analytics environments and adopt AI-driven automation systems. In 2026, enterprise AI server deployment activity in the region increased by nearly 19%, supported by rising demand for real-time analytics and cloud-based AI processing. However, limited hyperscale infrastructure and higher hardware import dependency continue affecting deployment scalability and operational cost structures. Companies are responding through regional cloud partnerships, localized integration services, and modular AI infrastructure strategies designed for lower-power enterprise environments and mid-scale operational workloads.

Brazil Market Outlook: Brazil remains the dominant AI servers market in South America due to expanding cloud infrastructure investment, financial-sector AI adoption, and telecom modernization programs. AI-enabled enterprise infrastructure deployment increased by approximately 24% in 2026, particularly within banking, retail analytics, and cybersecurity operations. Domestic enterprises are prioritizing scalable rack-based AI server systems and localized cloud integration partnerships to improve operational agility. Ongoing expansion of regional data center facilities is also strengthening AI processing capacity and reducing latency constraints for enterprise AI workloads.

Sovereign AI Investments Accelerate Infrastructure Modernization

The Middle East & Africa AI servers market is advancing through sovereign AI infrastructure initiatives, smart city investments, and expanding hyperscale cloud partnerships. The United Arab Emirates and Saudi Arabia are leading deployment activity through government-backed digital transformation programs and enterprise AI modernization projects. In 2026, AI-focused data center investment activity in the region increased by approximately 29%, particularly across cloud computing and public-sector AI analytics environments. Energy-efficient AI infrastructure and modular server deployments are gaining traction as operators target improved scalability and lower cooling overhead in high-temperature operating conditions. Companies are strengthening regional partnerships and localized deployment capabilities to support long-term AI infrastructure development.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as a strategic AI infrastructure hub due to strong sovereign investment capacity, advanced smart city programs, and hyperscale cloud expansion activity. AI-related enterprise infrastructure deployment increased by approximately 26% in 2026 across government services, financial analytics, and intelligent mobility applications. The country is prioritizing advanced AI data center development and energy-efficient compute environments to strengthen regional digital leadership. Strategic partnerships with global semiconductor and cloud infrastructure providers are also accelerating deployment of next-generation AI server ecosystems.

The AI servers market is led by technology-driven competition between Dell Technologies, Supermicro, Hewlett Packard Enterprise, Lenovo, Inspur, and ODM manufacturers competing for hyperscale cloud contracts and enterprise AI infrastructure expansion. NVIDIA-linked ecosystem providers dominate accelerator-optimized deployments, while regional manufacturers in China compete aggressively through cost-efficient integrated server architectures. The top five players collectively control approximately 58% of advanced AI server deployments due to strong semiconductor partnerships, supply-chain integration, and liquid-cooling capabilities. Competition is centered on GPU availability, rack-density optimization, deployment speed, and energy efficiency, with AI-focused server performance improving nearly 35% over legacy enterprise systems. Companies are expanding through vertically integrated manufacturing, hyperscale partnerships, localized assembly operations, and custom AI infrastructure design. Current market disruption is driven by sovereign AI infrastructure investment and advanced chip supply control. High entry barriers stem from semiconductor dependency, cooling infrastructure complexity, and enterprise-scale deployment capability. Winning requires integrated AI compute ecosystems, resilient supply chains, and scalable high-density infrastructure execution.

Dell Technologies

Super Micro Computer, Inc.

Hewlett Packard Enterprise

Lenovo Group Limited

Inspur Electronic Information Industry Co., Ltd.

Cisco Systems, Inc.

Fujitsu Limited

IBM Corporation

Gigabyte Technology Co., Ltd.

ASUS

Quanta Computer Inc.

Wiwynn Corporation

Advantech Co., Ltd.

NEC Corporation

AI servers are rapidly transitioning toward GPU-accelerated architectures, liquid-cooled rack systems, and AI-specific networking frameworks optimized for large language model training and inference. In 2026, more than 57% of hyperscale AI deployments utilized GPU-dense servers integrated with high-bandwidth memory and advanced interconnect technologies. Modern Blackwell-based AI systems deliver nearly 3x higher inference throughput than previous Hopper-generation platforms while improving mixed-workload energy efficiency by approximately 42%. Enterprises deploying liquid-cooled AI infrastructure are also reducing cooling-related operational power consumption by nearly 30%, strengthening data center scalability and compute density advantages.

Emerging technologies between 2026 and 2028 include modular AI superclusters, photonic interconnect integration, and edge-optimized AI inference servers supporting distributed enterprise workloads. AI-optimized rack architectures now process up to 250 tokens per second per user in advanced inference environments, while edge AI server adoption increased nearly 34% across telecom and industrial automation applications. Compared with legacy CPU-centric systems, accelerator-driven AI servers reduce training-cycle completion time by approximately 36%, creating operational advantages for hyperscale cloud operators, telecom firms, and financial analytics providers managing real-time AI workloads.

Disruptive innovation is increasingly centered on unified CPU-GPU memory architectures, automated infrastructure orchestration, and sustainable cooling ecosystems. Companies investing early in integrated AI compute environments, semiconductor partnerships, and energy-efficient server designs are securing faster deployment cycles, lower operational overhead, and stronger long-term AI infrastructure competitiveness.

October 2024 – Supermicro: Launched liquid-cooled NVIDIA Blackwell AI SuperClusters and delivered over 2,000 liquid-cooled racks since June 2024, reducing data center power consumption by up to 40%. The deployment strengthened hyperscale AI infrastructure scalability and accelerated enterprise AI factory modernization.

March 2025 – NVIDIA: Introduced Blackwell-powered DGX systems achieving over 30,000 tokens per second throughput and nearly 3x higher inference performance versus prior-generation Hopper platforms. The advancement significantly improved enterprise generative AI processing efficiency and accelerated large-scale inference deployment capability.

October 2024 – Fujitsu and Supermicro: Announced a strategic partnership to develop Arm-based green AI server platforms and liquid-cooled infrastructure targeting next-generation data centers. The collaboration focused on high-performance energy-efficient AI computing architectures supporting future hyperscale and enterprise AI workloads.

May 2026 – Supermicro: Showcased Vera Rubin NVL72 AI racks featuring advanced coolant technology with 1,000x higher electrical impedance than conventional solutions. The innovation improved infrastructure reliability, reduced system shutdown risk, and strengthened competitive differentiation in high-density AI server deployments.

The AI Servers Market report provides comprehensive analysis across GPU Servers, CPU Servers, Edge AI Servers, Rack Servers, and Blade Servers, covering deployment trends, infrastructure modernization, and enterprise AI integration patterns between 2026 and 2033. The study evaluates operational demand across Machine Learning, Natural Language Processing, Cloud Computing, Data Analytics, and Computer Vision applications while assessing adoption intensity within IT and Telecom, Healthcare, BFSI, Manufacturing, Retail, and Government sectors. More than 55% of enterprise AI infrastructure expansion analyzed in the report is linked to hyperscale cloud and generative AI workloads.

The report further delivers region-wise assessment covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed insights into semiconductor supply dynamics, liquid-cooling adoption, edge AI deployment, and sovereign AI infrastructure investment trends. It analyzes competitive positioning, deployment scalability, infrastructure efficiency, partnership strategies, and evolving procurement priorities to support expansion planning, technology investment decisions, and long-term AI infrastructure optimization strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4560 Million |

|

Market Revenue in 2033 |

USD 18622.98 Million |

|

CAGR (2026 - 2033) |

19.23% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dell Technologies, Super Micro Computer, Inc., Hewlett Packard Enterprise, Lenovo Group Limited, Inspur Electronic Information Industry Co., Ltd., Cisco Systems, Inc., Fujitsu Limited, IBM Corporation, Gigabyte Technology Co., Ltd., ASUS, Quanta Computer Inc., Wiwynn Corporation, Advantech Co., Ltd., NEC Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |