Reports

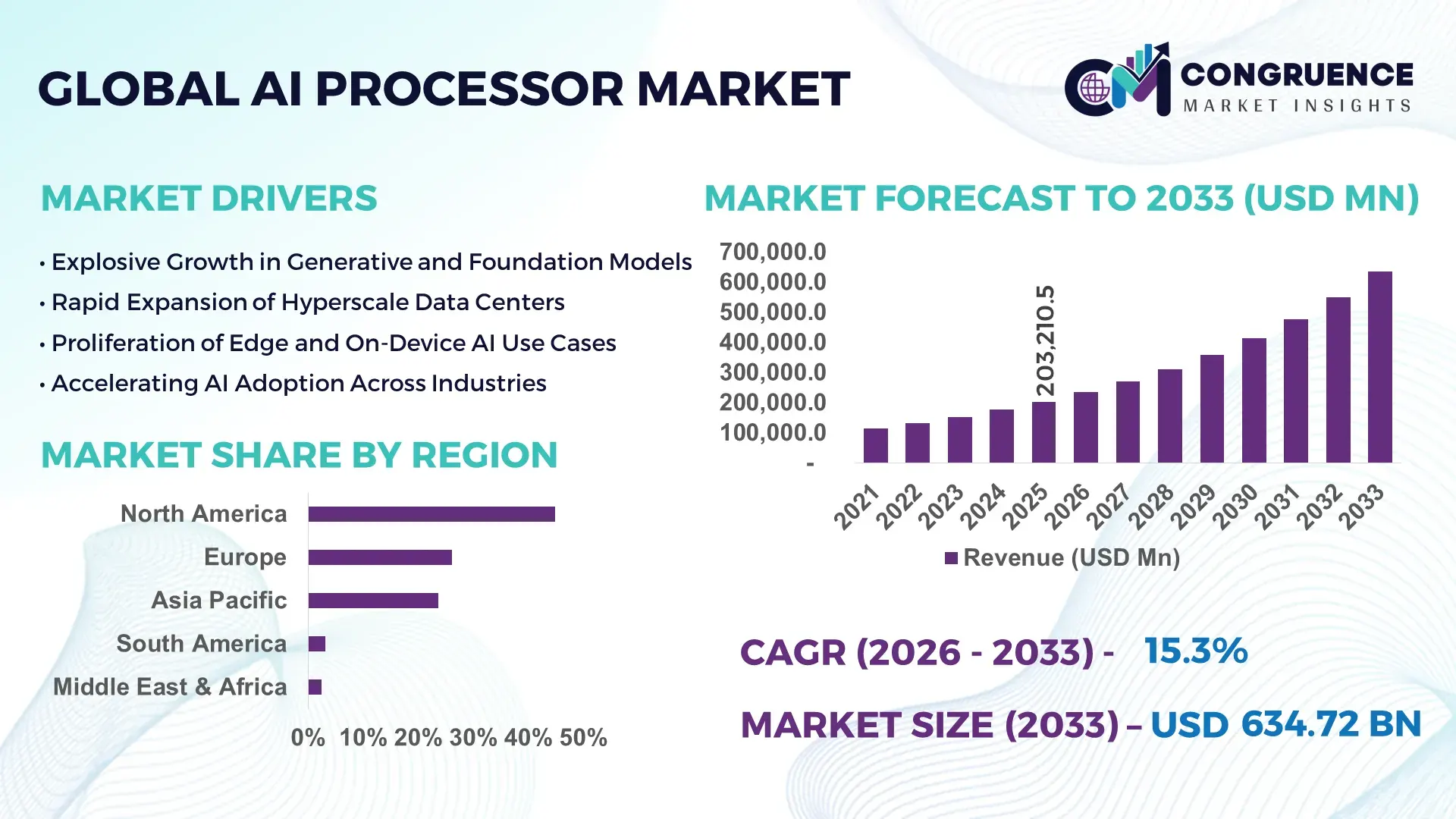

The Global AI Processor Market was valued at USD 203,210.5 Million in 2025 and is anticipated to reach a value of USD 634,717.7 Million by 2033 expanding at a CAGR of 15.3% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by exponential growth in AI workloads across data centers, edge computing, and intelligent devices.

The United States dominates the AI Processor market through its advanced semiconductor design ecosystem, large-scale capital investments, and leadership in AI model development. In 2025, the country hosted over 65% of global hyperscale data centers, deployed more than 120 exaFLOPS-equivalent AI compute capacity, and accounted for over USD 90 billion in annual AI infrastructure investments. AI processors are widely applied across cloud computing, defense analytics, autonomous systems, and healthcare diagnostics. More than 72% of Fortune 500 enterprises in the U.S. reported active deployment of AI accelerators, while domestic fabs supported sub-5nm node production for next-generation AI chips.

Market Size & Growth: USD 203,210.5 Million in 2025, projected to reach USD 634,717.7 Million by 2033 at a CAGR of 15.3%, driven by AI model scale and inference demand.

Top Growth Drivers: Data center AI adoption 68%, edge AI deployment 41%, generative AI workload expansion 74%.

Short-Term Forecast: By 2028, AI processor energy efficiency is expected to improve by 32% through advanced architectures.

Emerging Technologies: Chiplet-based processors, 3D stacking, and in-memory AI computing.

Regional Leaders: North America USD 272,000 Million, Asia-Pacific USD 218,000 Million, Europe USD 96,000 Million by 2033, each driven by cloud, manufacturing, and industrial AI adoption.

Consumer/End-User Trends: Increased enterprise demand for AI inference acceleration and real-time analytics.

Pilot or Case Example: In 2026, a hyperscale cloud pilot reduced AI training time by 27% using custom AI accelerators.

Competitive Landscape: Market leader holds ~31% share, followed by 4 major competitors with strong ecosystem control.

Regulatory & ESG Impact: Energy efficiency standards and carbon reporting influencing chip design.

Investment & Funding Patterns: Over USD 180 billion invested globally in AI semiconductor capacity expansion.

Innovation & Future Outlook: Focus on domain-specific AI processors and heterogeneous compute integration.

AI processors are primarily consumed by cloud service providers contributing nearly 48% of demand, followed by enterprise AI systems at 29% and edge devices at 23%. Recent innovations in chiplet integration, advanced packaging, and low-power inference engines are reshaping performance benchmarks, while government-backed semiconductor programs and rising AI sovereignty initiatives are influencing regional deployment strategies.

The AI Processor Market holds critical strategic relevance as AI becomes foundational to digital transformation, national competitiveness, and enterprise productivity. AI processors are now central to cloud infrastructure, autonomous systems, precision healthcare, and industrial automation. Advanced AI accelerators deliver up to 6× performance improvement compared to traditional CPUs, enabling large language models and real-time analytics at scale. North America dominates in volume deployment, while Asia-Pacific leads in manufacturing adoption with over 54% of global wafer fabrication capacity dedicated to AI-capable nodes.

By 2029, neuromorphic and energy-efficient AI processors are expected to reduce data center power consumption by 29%, addressing sustainability constraints. Firms are committing to ESG metrics such as 40% energy efficiency improvement per compute unit by 2030, aligning chip design with carbon-neutral goals. In 2026, a leading U.S.-based cloud provider achieved 34% inference latency reduction through deployment of custom AI silicon across its global regions. Strategic pathways include vertical integration, software-hardware co-design, and regional supply chain localization. The AI Processor Market is positioned as a cornerstone of resilient digital infrastructure, regulatory compliance, and long-term sustainable growth.

The AI Processor market is shaped by rapid advances in artificial intelligence models, escalating compute intensity, and increasing deployment of AI at scale. Demand is driven by hyperscale data centers, enterprise AI adoption, and real-time edge analytics. The shift from general-purpose processors to domain-specific AI accelerators has intensified competition and innovation. Supply-side dynamics are influenced by advanced node manufacturing, packaging constraints, and geopolitical semiconductor policies. At the same time, growing focus on energy efficiency, latency reduction, and cost-per-inference optimization is redefining procurement strategies. These dynamics collectively determine investment priorities, technology roadmaps, and market expansion trajectories.

The surge in AI workloads across training and inference environments is a primary growth driver. In 2025, AI compute demand grew by over 4.5× compared to 2022 levels, driven by large language models exceeding 1 trillion parameters. Enterprises deploying AI processors reported up to 38% faster model deployment cycles and 41% reduction in total compute cost per task. Industries such as cloud services, autonomous vehicles, and healthcare diagnostics increasingly require parallel processing and high memory bandwidth, accelerating adoption of specialized AI processors.

Advanced AI processors rely on cutting-edge fabrication nodes below 5nm, available at limited foundries. In 2025, lead times for high-end AI chips extended beyond 9 months, constraining deployment timelines. Packaging complexity, yield variability, and high capital intensity—often exceeding USD 20 billion per fab—limit rapid capacity expansion. These factors restrict short-term availability and elevate procurement risk for enterprises.

Edge AI deployment presents significant growth opportunities as latency-sensitive applications expand. By 2027, over 46% of AI inference workloads are expected to shift toward edge environments. Domain-specific accelerators tailored for vision, speech, and recommendation engines can deliver 3–5× performance per watt improvements, opening new opportunities in smart manufacturing, retail analytics, and connected healthcare.

High-performance AI processors can exceed 700 watts per chip, creating thermal management challenges. Data centers face cooling capacity constraints, with liquid cooling adoption rising but increasing infrastructure complexity. Power density limits deployment density, particularly in legacy facilities, creating operational and cost challenges that slow large-scale expansion.

Bold Shift Toward Chiplet Architectures: Over 58% of new AI processor designs now adopt chiplet-based architectures, reducing design costs by 35% and improving yield scalability.

Acceleration of Edge AI Processing: Edge AI processor shipments grew 42% year-on-year, supporting real-time inference in smart cameras, vehicles, and industrial IoT.

Integration of Advanced Packaging: 3D stacking and advanced interposers improved memory bandwidth by 2.8×, directly enhancing AI model throughput.

Focus on Energy-Efficient AI Compute: New AI processors achieve up to 40% lower energy consumption per inference, supporting sustainability and cost optimization goals.

The AI Processor market is segmented by type, application, and end-user, reflecting diverse compute requirements. Different processor architectures address varying performance, power, and scalability needs. Applications span cloud AI, edge inference, and on-device intelligence, while end-users range from hyperscale cloud providers to industrial enterprises. Segmentation highlights the transition toward specialized accelerators optimized for distinct AI workloads, with adoption patterns influenced by cost, power efficiency, and ecosystem compatibility.

GPUs lead the market with approximately 47% share, supported by their flexibility and mature software ecosystems. ASIC-based AI processors represent the fastest-growing segment, driven by workload-specific optimization and delivering 18.9% CAGR in adoption due to superior performance-per-watt. FPGAs and neuromorphic processors collectively account for about 21% of the market, serving niche applications requiring reconfigurability or ultra-low power operation.

•In 2025, a national research laboratory deployed custom ASIC AI processors to accelerate climate modeling, improving simulation throughput for over 12 million data points.

Data center and cloud AI applications dominate with nearly 52% share, driven by generative AI and large-scale training workloads. Edge AI applications are the fastest-growing, expanding at 19.4% CAGR, supported by demand for low-latency analytics in manufacturing and mobility. Other applications, including consumer electronics and embedded systems, contribute around 28% combined. In 2025, over 44% of enterprises reported piloting AI processors for real-time decision platforms.

•In 2024, a public healthcare network deployed AI processors across 160 hospitals, enabling faster diagnostic imaging analysis for more than 2 million cases.

Cloud service providers lead with approximately 49% adoption, leveraging AI processors for scalable compute services. Enterprises represent the fastest-growing end-user segment at 17.8% CAGR, driven by AI integration in operations, finance, and healthcare. Government and research institutions account for about 18% combined, focusing on defense and scientific computing. In 2025, 39% of enterprises globally reported active AI processor deployments.

•In 2025, a consortium of mid-sized enterprises improved inventory forecasting accuracy by 22% after integrating AI processors into analytics platforms.

North America accounted for the largest market share at 44.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.9% between 2026 and 2033.

North America’s dominance reflects concentrated hyperscale data center deployments exceeding 3,600 facilities, over 70% enterprise AI adoption, and AI processor installations supporting more than 65 exaFLOPS of aggregate compute capacity. Europe followed with 23.6% share, driven by industrial AI, automotive automation, and regulated enterprise deployments across Germany, the UK, and France. Asia-Pacific held 26.1% share in 2025, supported by large-scale semiconductor manufacturing, over 55% global wafer capacity, and rapid AI inference adoption across consumer electronics and mobile platforms. South America and Middle East & Africa together contributed 5.5%, reflecting early-stage but accelerating adoption in fintech, smart cities, and energy analytics. Across regions, GPU-based processors represented 47% of deployments, while ASIC accelerators accounted for 31%, highlighting shifting compute preferences.

How is enterprise-scale AI infrastructure accelerating processor demand?

The North America AI Processor Market represented approximately 44.8% of global demand in 2025, supported by large-scale cloud computing, defense analytics, healthcare AI, and financial services automation. Over 72% of enterprises reported active AI processor deployments, particularly in predictive healthcare diagnostics and real-time fraud detection. Government initiatives supporting domestic semiconductor manufacturing exceeded USD 50 billion in incentives, accelerating advanced-node production and packaging capabilities. Technological leadership is evident in sub-5nm chip production, chiplet architectures, and liquid-cooled AI clusters. A major local player expanded custom AI accelerator deployment across more than 25 hyperscale regions, reducing inference latency by 28%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, where AI-driven decision platforms are prioritized.

How is regulatory alignment shaping next-generation AI processor adoption?

Europe accounted for roughly 23.6% of the AI Processor Market in 2025, with Germany, the UK, and France collectively contributing over 68% of regional demand. Industrial automation, automotive AI, and energy optimization are key application areas. Regulatory frameworks emphasizing transparency and data governance are accelerating demand for explainable and auditable AI processors. Sustainability initiatives require energy-efficient compute, pushing adoption of low-power accelerators with up to 35% lower watt-per-inference metrics. A regional semiconductor consortium scaled AI chip pilot production to support over 120 industrial AI projects. European consumers and enterprises show preference for compliant, transparent AI systems aligned with digital sovereignty goals.

How are manufacturing scale and digital consumption reshaping AI compute demand?

Asia-Pacific ranked second by market volume in 2025, contributing 26.1% of global AI processor deployments, with China, Japan, and India leading consumption. The region hosts over 55% of global semiconductor manufacturing capacity, enabling rapid scaling of AI chip production. Infrastructure investment supported deployment of more than 1,900 AI-focused data centers, while consumer electronics integrated AI processors across smartphones, cameras, and IoT devices. Regional innovation hubs advanced AI accelerators optimized for mobile inference, achieving 42% power efficiency gains. Growth is driven by e-commerce personalization, mobile AI apps, and smart manufacturing adoption across urban clusters.

How is digital modernization creating new AI processor demand pockets?

South America held approximately 3.1% market share in 2025, with Brazil and Argentina leading adoption. AI processors are increasingly deployed in fintech, media analytics, and energy optimization platforms. Infrastructure upgrades supported over 140 AI-enabled data facilities, while government tax incentives reduced import costs for advanced processors by up to 18%. A regional technology provider integrated AI accelerators into broadcast analytics systems, improving content localization accuracy by 31%. Consumer behavior reflects rising demand for language-specific AI services and localized digital platforms.

How are smart infrastructure and energy analytics influencing AI compute adoption?

The Middle East & Africa region accounted for 2.4% of global demand in 2025, led by the UAE and South Africa. AI processors are increasingly used in smart city surveillance, oil & gas analytics, and infrastructure monitoring. Over USD 12 billion was allocated to digital infrastructure modernization supporting AI compute deployment. Trade partnerships facilitated access to advanced AI processors, while regional regulations emphasized secure and sovereign AI systems. Consumer adoption is driven by government-led digital transformation programs and intelligent public services.

United States – 38.9% share: High concentration of hyperscale data centers and advanced AI research ecosystems.

China – 21.7% share: Large-scale semiconductor manufacturing capacity and mass AI adoption across consumer electronics.

The AI Processor market is moderately consolidated, with over 35 active global competitors spanning GPUs, ASICs, FPGAs, and emerging neuromorphic designs. The top five companies collectively account for approximately 68% of total market presence, reflecting strong ecosystem lock-in and software compatibility advantages. Competitive strategies focus on custom silicon development, long-term cloud partnerships, and vertical integration. Product launches emphasizing performance-per-watt improvements above 40%, advanced packaging, and AI software stack optimization are common. Strategic alliances between chip designers and hyperscale cloud providers have increased, with over 22 major partnerships formed between 2024 and 2025. Innovation intensity remains high, with annual R&D investments exceeding USD 95 billion across leading firms, reinforcing competitive barriers.

Apple Inc.

Qualcomm Technologies, Inc.

Samsung Electronics

Broadcom Inc.

Arm Holdings

Google LLC

Amazon Web Services

Huawei Technologies

Alibaba Group

MediaTek

Graphcore

AI processor technologies are evolving rapidly to address escalating compute density, power efficiency, and scalability requirements. Advanced GPUs remain central to training large models, while ASIC accelerators are optimized for inference workloads, delivering up to 5× performance-per-watt gains. Chiplet-based designs allow modular scaling, reducing development costs by 30–40%. 3D packaging and high-bandwidth memory integration now support memory throughput exceeding 3 TB/s, critical for transformer-based models. In-memory computing and near-data processing architectures reduce data movement overhead by 25%, improving efficiency. Edge AI processors emphasize ultra-low power consumption below 10 watts, enabling real-time analytics in constrained environments. Security-enhanced AI processors integrate hardware-level encryption and trusted execution environments to meet enterprise compliance needs. Collectively, these technologies define next-generation AI compute infrastructure.

In March 2024, NVIDIA unveiled the Blackwell B200 AI processor, delivering up to 20 petaflops of FP4 compute and supporting trillion-parameter AI models with improved energy efficiency. Source: www.nvidia.com

In April 2024, AMD launched the MI300X accelerator featuring 192 GB HBM3 memory, enabling large language model inference at higher throughput and lower latency. Source: www.amd.com

In June 2024, Intel announced Gaudi 3 AI accelerators optimized for generative AI workloads, achieving 2× training performance gains compared to prior generations. Source: www.intel.com

In May 2025, Apple introduced its M4 AI processor with enhanced neural engine capabilities, delivering 38 TOPS for on-device AI across consumer devices. Source: www.apple.com

The AI Processor Market Report provides comprehensive coverage of processor architectures, deployment environments, and industry adoption patterns. It analyzes market segmentation by processor type including GPUs, ASICs, FPGAs, and emerging neuromorphic designs, along with applications spanning data centers, edge computing, and embedded systems. Geographic scope includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure maturity, manufacturing capabilities, and policy frameworks. The report evaluates industry verticals such as cloud services, healthcare, automotive, finance, defense, and consumer electronics, detailing AI compute intensity and deployment metrics. Technology scope covers advanced packaging, chiplet integration, memory architectures, and energy-efficient designs. It also assesses competitive positioning, innovation pipelines, and investment trends shaping AI processor adoption across global digital ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 203,210.5 Million |

|

Market Revenue in 2033 |

USD 634,717.7 Million |

|

CAGR (2026 - 2033) |

15.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, Apple Inc., Qualcomm Technologies, Inc., Samsung Electronics, Broadcom Inc., Arm Holdings, Google LLC, Amazon Web Services, Huawei Technologies, Alibaba Group, MediaTek, Graphcore |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |