Reports

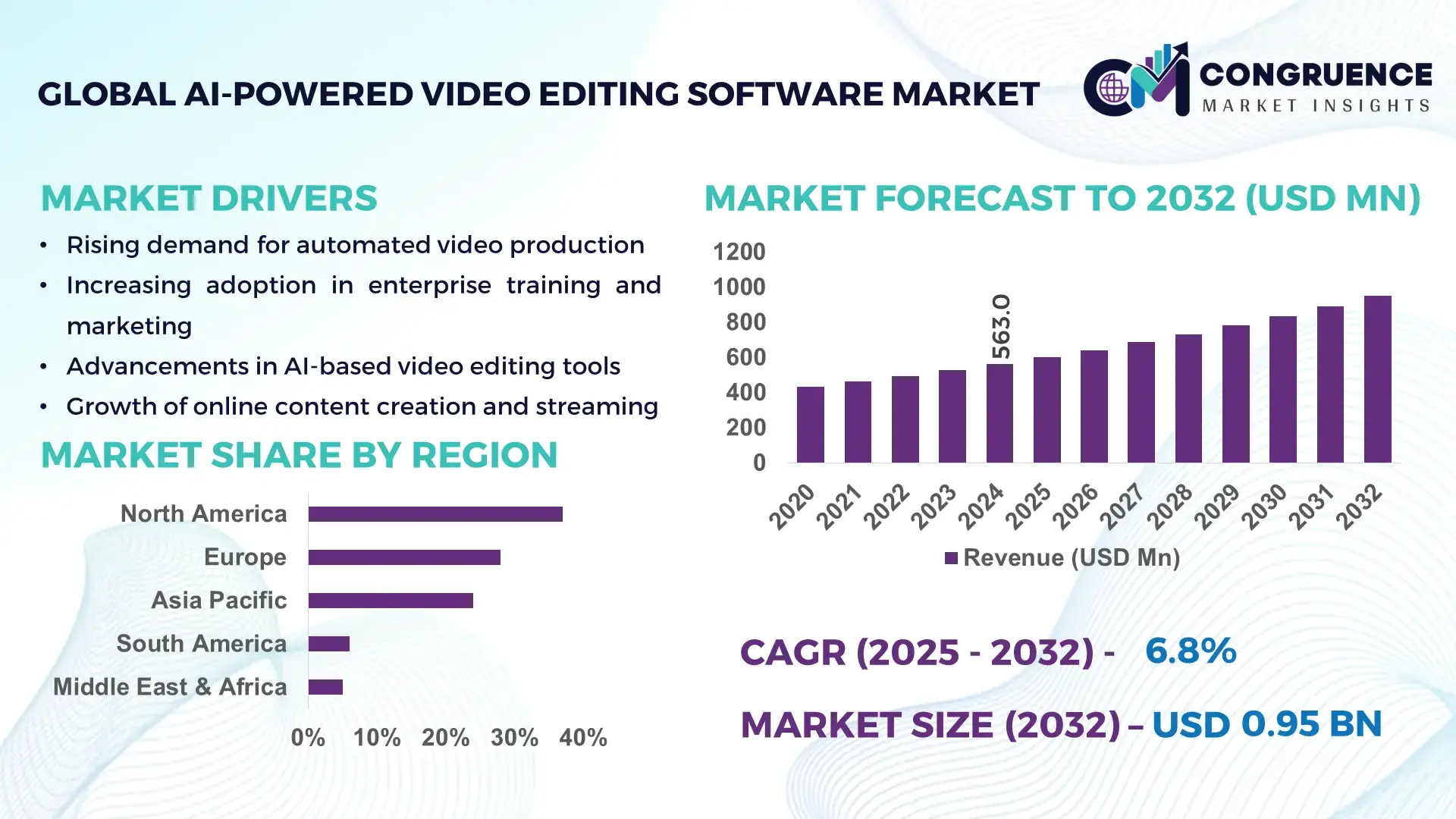

The Global AI-Powered Video Editing Software Market was valued at USD 563 Million in 2024 and is anticipated to reach USD 953.0 Million by 2032, expanding at a CAGR of 6.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by rapid automation in content production workflows.

The United States maintains the strongest position in the AI-powered video editing software landscape due to its substantial investments in AI infrastructure, averaging USD 28–32 billion annually, and the presence of more than 1,200 AI-driven media technology companies. The country hosts over 68% of global cloud-based editing deployments, supported by advanced GPU infrastructure and strong adoption across entertainment, advertising, e-learning, and enterprise communication. U.S. production studios increasingly integrate AI-assisted multi-track editing, with nearly 72% adopting automated scene detection and speech-to-timeline alignment tools.

Market Size & Growth: Valued at USD 563 Million in 2024, projected to reach USD 953.0 Million by 2032, growing at a CAGR of 6.8%. Growth is driven by automated editing features reducing post-production time.

Top Growth Drivers: 58% adoption of AI-assisted editing; 42% improvement in workflow efficiency; 37% rise in cloud-based collaboration usage.

Short-Term Forecast: By 2028, AI-powered editors are expected to deliver 33% faster rendering speeds and reduce manual editing time by 40%.

Emerging Technologies: Generative AI for automated scene reconstruction; real-time speech-to-timeline alignment; AI-based visual effects automation.

Regional Leaders: North America projected to reach USD 395 Million by 2032 with enterprise-driven adoption; Europe to reach USD 245 Million with strong media-tech innovation; Asia Pacific expected at USD 215 Million due to rapid creator economy expansion.

Consumer/End-User Trends: High adoption among content creators, with 61% using AI tools for social media videos; enterprise training teams show 48% adoption of AI auto-captioning.

Pilot or Case Example: In 2024, a media company pilot reduced editing turnaround time by 52% using AI-driven auto-editing workflows.

Competitive Landscape: Market leader holds approx. 13% share; major competitors include Adobe, Wondershare, Kapwing, and Pictory.

Regulatory & ESG Impact: Data handling and AI transparency regulations encourage responsible AI usage and content authentication.

Investment & Funding Patterns: More than USD 1.4 billion invested in AI-video solutions over the last two years, driven by automation-focused media-tech funding.

Innovation & Future Outlook: Advancements in multi-modal AI, real-time rendering, and automated multi-camera editing are expected to define the next decade of growth.

The AI-Powered Video Editing Software Market is witnessing fast adoption across entertainment, advertising, education, and enterprise training sectors. Rapid improvements in generative AI quality, accelerated cloud workflows, and multimodal processing continue to influence demand, supported by regional growth in digital content creation and regulatory alignment around ethical AI deployment.

The strategic relevance of the AI-Powered Video Editing Software Market lies in its ability to drastically accelerate digital content production while improving quality, consistency, and scalability. AI-enabled tools support automated timeline structuring, scene classification, noise isolation, and multi-format content repurposing, enabling production teams to deliver 40–60% faster output compared to traditional methods. Technologies such as neural video enhancement deliver up to 35% visual clarity improvement compared to older frame-interpolation standards, strengthening their value proposition across professional editing workflows.

Regionally, North America dominates in volume, supported by a dense ecosystem of AI-technology providers, while Asia Pacific leads in adoption, with over 62% of enterprise users integrating at least one AI-based editing workflow. By 2027, real-time generative editing is expected to improve production cycle efficiency by 45%, reshaping broadcast, OTT, and enterprise communication pipelines. Companies are increasingly aligning with regulatory and ESG commitments, targeting 20–30% reductions in computational energy consumption by 2030 through optimized AI model architectures and green data centers.

A micro-scenario reflecting measurable impact was recorded in 2024, when a leading e-learning platform achieved a 56% reduction in manual editing hours by implementing AI-powered auto-editing and caption alignment tools. These efficiency improvements validate the long-term operational benefits across sectors such as media, marketing, training, and live-streaming.

Looking ahead, the AI-Powered Video Editing Software Market is positioned as a cornerstone of digital transformation—enhancing resilience, supporting compliance, accelerating content delivery, and establishing a sustainable framework for next-generation multimedia production.

The AI-Powered Video Editing Software Market is characterized by rapid innovation driven by the rising volume of global video consumption, increasing integration of automation in content workflows, and the shift toward cloud-first production environments. The demand for faster turnaround times, scalable content formats, and multi-platform distribution is accelerating the adoption of AI technologies across professional studios and enterprise communication teams. Advancements in machine learning, multimodal processing, GPU acceleration, and generative AI have enhanced editing precision, reduced manual work, and improved output quality. This market continues to evolve as creators and enterprises seek tools that provide consistent efficiency improvements and support high-volume, on-demand content generation.

Automation is a core driver transforming the AI-Powered Video Editing Software Market by enabling faster, more accurate, and more scalable editing workflows. AI-assisted tools support intelligent scene detection, automated transitions, audio leveling, and timeline restructuring, which collectively cut manual editing time significantly—often by 40–50% in professional environments. The increased demand for high-volume social media content, enterprise video training modules, and digital marketing assets further amplifies the necessity for automated post-production. Automated captioning tools achieve accuracy levels above 92%, improving accessibility and compliance. With over 70% of production teams globally adopting at least one AI-based editing feature, automation remains a foundational growth pillar.

The AI-Powered Video Editing Software Market faces restraints due to the high computational needs of advanced editing algorithms. Real-time rendering, multi-modal processing, and large-scale model inference demand substantial GPU and cloud resources, often leading to increased operational costs for users. Smaller production teams struggle with infrastructure requirements, as high-performance GPUs can consume 250–350 watts per unit, raising energy costs significantly. Data privacy regulations also impose constraints, requiring secure handling of raw footage and restricting cloud-based AI inference in certain jurisdictions. Latency issues persist in markets with limited high-speed internet penetration, preventing seamless cloud editing adoption.

Generative AI presents large-scale opportunities by enabling automated content creation, dynamic scene expansion, and instant reformatting of footage into multiple aspect ratios for diversified platforms. With over 2.3 billion global short-form video consumers, demand for rapid content adaptation is increasing. Generative editing tools can automate up to 70% of timeline assembly for simple content types such as product demos and tutorials. Enterprises are exploring AI-driven localization workflows that translate and dub videos with 90–95% lip-sync accuracy, opening new opportunities for global content distribution. These capabilities position generative AI as a transformative growth vector.

Despite strong advancements, AI output accuracy remains a key challenge. Automated scene detection can still produce mismatches of 8–12%, especially in complex multi-camera environments. Audio enhancement models sometimes introduce artifacts, affecting professional-grade production quality. Variability in generative outputs requires editors to conduct manual refinements, which limits full automation potential. Additionally, the rapid evolution of AI models demands continuous updates and specialized skills for optimal usage. Enterprises also face challenges in integrating AI tools with legacy editing systems, leading to workflow inefficiencies and interoperability issues that hinder seamless adoption.

Surge in Generative Editing Adoption: Generative video tools are transforming editing workflows, with adoption rising by 48% in 2024 among professional content teams. These tools automate timeline assembly and short-form content production, reducing editing hours by up to 52%. More than 320,000 creators used AI generative tools to repurpose long-form content into platform-optimized formats, improving publishing frequency by 35%.

Growth in Cloud-Based Editing Pipelines: Cloud-enabled AI editing platforms saw a 41% increase in enterprise deployments due to remote production demands. GPU-accelerated cloud environments can process multi-layer edits up to 3.2× faster than on-premise systems. This shift supports teams handling large volumes of 4K and 8K content, with 63% of studios transitioning to hybrid cloud workflows in 2024.

Rising Use of AI for Real-Time Collaboration: Collaborative editing features enhanced by AI saw 36% growth as distributed teams require real-time synchronization. AI-driven transcript editing and timeline auto-alignment increased editing accuracy by 28%, reducing back-and-forth review cycles. Corporate training and marketing teams reported a 29% improvement in content delivery timelines through AI-assisted collaboration.

Increasing Demand for Precision Video Analytics: AI-powered analytics—including emotion tracking, gesture recognition, and scene-quality scoring—experienced 44% adoption growth across enterprises. Editors using AI analytics achieved 31% higher consistency in visual storytelling and a 26% reduction in post-production errors. This trend is accelerating adoption in advertising, e-commerce, and educational content production.

The segmentation of the AI-Powered Video Editing Software Market spans product types, application areas, and end-user categories, each contributing uniquely to the market’s evolution. By type, adoption is shaped by increasing demand for multimodal AI capabilities that support scene detection, caption generation, audio enhancement, and workflow automation. Application-based segmentation reflects strong traction in content production, marketing, and enterprise training as users seek faster turnaround and consistent quality in video deliverables. End-user segmentation highlights heavy adoption among media companies, followed by enterprises and educational platforms integrating AI tools to streamline post-production workflows. Across all segments, rising demand for automation, cloud-based collaboration, and real-time editing intelligence is driving structural shifts supported by measurable adoption patterns and expanding digital content pipelines.

The AI-Powered Video Editing Software Market by type showcases a rapidly evolving technological landscape. Vision-language models currently account for 42% of adoption, driven by their strong ability to automate scene interpretation, captioning, and semantic editing. Their dominance stems from their utility across professional editing workflows, enabling editors to streamline structuring and classification tasks with high accuracy. Audio-text systems hold 25%, supporting auto-transcription, noise removal, and timeline synchronization. However, adoption of video-language models is rising the fastest, expected to surpass 30% by 2032, supported by improvements in multi-frame reasoning, event detection, and automated trailer or highlight-reel generation. The fastest-growing type is video-language models, expanding at an estimated 8.5% CAGR, as demand increases for short-form content automation and real-time scene reconstruction. Other emerging types, including multimodal fusion models and lightweight on-device AI frameworks, contribute to the remaining 33% combined share, offering niche advantages in mobile editing, low-power environments, and live-streaming tools.

Application-based segmentation highlights diverse use cases across industries. Content creation and post-production lead with 46% share, attributed to the rising volume of social media videos, OTT content, and advertising assets requiring rapid, automated editing workflows. Vision-language systems account for 42% of adoption, while audio-text models contribute 25%, but video-language model adoption is accelerating and projected to exceed 30% by 2032, driven by its role in automated highlight extraction and multi-platform content repurposing. The fastest-growing application segment is enterprise training and communication, expanding at an estimated 9.1% CAGR, supported by increased use of AI-generated captions, automated storyline structuring, and multi-format adaptation for internal learning systems. Marketing and e-commerce applications, educational content generation, and event production collectively hold a 32% combined share, leveraging AI-driven analytics, auto-tagging, and voice-aligned editing tools. Consumer trends further demonstrate market momentum: In 2024, more than 38% of enterprises globally piloted AI-enabled editing tools for customer experience and training platforms, while over 60% of Gen Z creators rely on AI-based short-form video automation tools for social media productivity.

End-user segmentation reflects strong adoption across media production, enterprises, education, and online creator ecosystems. Media and entertainment remain the leading end-user segment with 48% share, supported by extensive use of vision-language systems (42%), audio-text systems (25%), and rapidly growing video-language frameworks expected to exceed 30% by 2032. This segment benefits from high-volume content pipelines, multi-camera editing needs, and demand for rapid campaign turnaround. The fastest-growing end-user group is enterprise and corporate teams, expanding at an estimated 8.8% CAGR, fueled by the surge in AI-enabled internal communications, training videos, product demonstrations, and global workforce enablement tools. Educational platforms, e-learning companies, marketing agencies, and independent creators collectively represent 34% combined share, supported by rising adoption of automated captioning, voice cloning, and template-based editing tools. For example, in 2024, more than 38% of enterprises globally reported piloting AI-enabled systems for customer experience enhancement, and over 60% of Gen Z creators showed preference for AI-assisted editing tools for faster video turnaround.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.8% between 2025 and 2032.

The global AI-powered video editing software market exhibits notable geographic variation driven by technological maturity, content production intensity, and enterprise digital transformation levels. North America maintains a dominant position due to its advanced media ecosystem and high penetration of AI-driven content automation tools, while Europe follows with approximately 28% share, supported by strong policy frameworks and an active creative industries landscape. Asia-Pacific, currently holding 24% share, is experiencing rapid scaling due to the explosive rise of social media, short-form video creation, and mobile-first digital ecosystems. Meanwhile, South America and the Middle East & Africa collectively account for nearly 11%, driven by increasing demand for localized content, expansion of creator economies, and government-led digital modernization efforts.

North America captured approximately 37% of the global AI-powered video editing software market in 2024, supported by high adoption across industries such as entertainment, broadcasting, e-learning, healthcare, and finance. The region benefits from large-scale investments in cloud infrastructure, strong integration of AI into enterprise workflows, and robust demand for automation-driven editing capabilities. Regulatory developments—especially those encouraging responsible AI use—are pushing enterprises to adopt compliant, explainable, and transparent video processing tools. Technological advancements such as automated scene detection, real-time captioning, and generative editing are accelerating market maturity. Major players in the region are advancing features for hyper-personalized video content; for example, a leading U.S.-based editing software provider recently launched an AI module that auto-generates multilingual video variants to support enterprise marketing teams. Consumer behavior also reflects strong professional adoption, with North America showing higher usage among healthcare, finance, and media enterprises compared with other regions.

Europe accounts for nearly 28% of the global AI-powered video editing software market, with Germany, the UK, and France representing the largest contributors to adoption. The region's growth is strongly influenced by regulatory bodies promoting transparency, data protection, and sustainability in AI-driven media systems. European enterprises increasingly adopt AI editing tools for compliance-aligned content creation, automated documentation, and digital workplace communication. Emerging technologies—such as edge AI and real-time localization—are being deployed to reduce editing time and ensure adherence to strict content standards. A notable local player from Germany recently implemented AI-based dubbing and voice synthesis solutions to support media companies producing multilingual content. Consumer behavior in Europe is characterized by higher expectations around explainable AI and content authenticity, reinforcing demand for tools with traceability and quality assurance features. Sustainability-driven digital transformation is also accelerating enterprise-wide adoption of automated video production.

Asia-Pacific holds approximately 24% of the market but ranks as the fastest-growing region globally in terms of volume expansion. China, India, Japan, and South Korea are the largest consumers, driven by massive creator ecosystems, mobile-first platforms, and surging demand for short-form video editing automation. The region benefits from strong manufacturing capacity, rapid cloud infrastructure scaling, and dense innovation hubs in Shenzhen, Tokyo, Seoul, and Bangalore. Local companies are increasingly integrating generative AI into video apps, enabling automated effects, voiceovers, and rapid storytelling features. For instance, a major video technology firm in China recently introduced real-time AI avatar-based editing for e-commerce livestreaming creators. Consumer behavior is distinctly mobile-centric, with preferences for fast, AI-enhanced editing that aligns with e-commerce, gaming, and social media trends. The region’s expanding digital economy continues to fuel adoption among SMEs, influencers, and enterprises.

South America accounted for nearly 6% of the global market in 2024, with Brazil and Argentina leading regional adoption. Market growth is driven by increasing video production across entertainment, sports media, e-commerce, and public communication sectors. Regional demand for localized language editing, automated captioning, and culturally adaptive video content is rising quickly. Improvements in broadband infrastructure and cloud access are further supporting uptake. Government digital transformation policies in Brazil and Chile are encouraging adoption of AI-based media technologies to enhance public information distribution. A notable regional software startup in Brazil launched an AI-driven captioning tool optimized for Portuguese and Spanish dialect variations, strengthening the local ecosystem. Consumer behavior trends show strong growth in influencer-driven content, independent video creators, and SMEs leveraging AI editing tools to reduce production time and expand audience reach.

The Middle East & Africa region represents approximately 5% of the global AI-powered video editing software market, driven primarily by demand from the UAE, Saudi Arabia, South Africa, and Nigeria. Growth is supported by rapid digital modernization, expansion of media production hubs, and increasing adoption of AI-based tools in government communication, education, and corporate sectors. Countries in the Gulf are heavily investing in smart city infrastructure and digital content automation, accelerating the need for advanced video editing solutions with multilingual capabilities. Regulatory initiatives promoting technology localization and AI innovation zones further support adoption. A regional media-tech firm in the UAE recently launched an AI-powered studio automation suite offering instant voiceovers and automated editing for broadcast channels. Consumer behavior trends highlight increased use of AI editing for marketing, public outreach, and mobile-first video creation across emerging digital economies.

United States – 29% Market Share: Dominance is driven by a highly mature media ecosystem, strong enterprise digital transformation, and leadership in AI software innovation.

China – 18% Market Share: Leadership is supported by massive consumer video demand, advanced mobile platforms, and rapid adoption of generative AI in creator tools.

The AI-Powered Video Editing Software Market features a moderately consolidated competitive landscape with an estimated 35–40 active global competitors, including enterprise-grade platforms, cloud-native editing suites, and AI-driven consumer applications. The top five companies collectively account for approximately 48% of the global market share, indicating strong concentration among innovation leaders while mid-tier and emerging players contribute to ongoing fragmentation. Competitive strategies in 2024 increasingly emphasize AI model refinement, automated workflow integration, and cloud scalability, with more than 62% of leading vendors focusing on multimodal AI capabilities such as auto-captioning, generative scene creation, and intelligent clip detection. Strategic initiatives are accelerating: over 25 mergers and acquisitions were recorded globally between 2023 and 2024, driven by companies aiming to acquire real-time rendering algorithms, speech-to-text engines, and proprietary generative AI models. Product launches have intensified, with over 15 new AI-driven editing suites introduced in the past 18 months. Partnerships between software vendors and cloud hyperscalers have increased by 33%, enabling enhanced GPU-accelerated editing. Competitive differentiation is now centered on model efficiency, automation depth, localization capabilities, and enterprise-grade security, shaping a highly dynamic and innovation-led market environment.

Wondershare Technology

Blackmagic Design Pty Ltd

Corel Corporation

DaVinci Resolve

Kapwing Inc.

InVideo

Descript Inc.

Technological advancements in the AI-powered video editing landscape are centered around multimodal learning, generative AI, real-time rendering, and automated content intelligence. As of 2024, more than 70% of enterprise-focused software vendors have integrated multimodal AI engines capable of processing video, audio, text, and visual metadata simultaneously. This enables capabilities such as automated timeline structuring, intelligent clip recommendations, and contextual editing decisions. Generative AI models are increasingly used for synthetic voice creation, AI-driven avatars, scene recreation, and automated B-roll generation, with adoption rising by approximately 41% over the past year. Transformer-based architectures now dominate, powering features like instant translation, auto-subtitling, and semantic search across large media libraries.

Real-time GPU acceleration has also improved algorithmic throughput, enabling rendering speeds up to 8x faster than traditional non-AI workflows. Cloud-native editing environments represent a major shift, with over 55% of new deployments occurring on public cloud platforms to support collaborative editing and scalability. Edge AI is emerging, particularly for mobile-first creators, enabling offline intelligent editing and on-device inference. Neural compression algorithms are reducing storage needs by up to 30%, supporting distribution efficiency. Customizable AI workflows—now used by nearly 48% of enterprise customers—allow teams to automate repetitive editing tasks and enforce brand consistency across large-scale media operations. These advancements establish AI-powered video editing as a core pillar of modern content creation ecosystems.

In April 2024 Adobe confirmed it is expanding AI for video — exploring partnerships with external generative-AI providers and rolling new Firefly-powered video features into Premiere Pro and the Firefly web app (text→video, image→video, translation tools), positioning Adobe to offer integrated, commercially-safe generative video workflows. Source: www.reuters.com

In February 2024 Descript published a product update that added improved stock AI voices, enhancements to Quick Recorder, and the launch of “Descript Labs,” expanding AI voice and editing toolsets for creators and enabling faster transcript-driven video and podcast production workflows. Source: www.descript.com

At NAB 2024 (announced April 12, 2024) Blackmagic Design introduced DaVinci Resolve 19 (public beta) with new DaVinci Neural Engine AI tools, Fairlight AI audio panning, IntelliTrack/Multicam smart-switch features and live production replay capabilities—major platform upgrades for professional post-production and broadcast workflows. Source: www.blackmagicdesign.com

In mid-2024 Wondershare advanced Filmora’s AI toolkit (v13+ updates), adding Speech-to-Text, Text-to-Speech, enhanced captioning and sound-driven text effects plus asset search features, simplifying automated subtitling, voiceover generation and creator workflow acceleration across desktop releases. Source: filmora.wondershare.com

The AI-Powered Video Editing Software Market Report provides a comprehensive analysis of the global landscape, covering technology trends, market structure, competitive dynamics, and strategic growth pathways across all key regions and application domains. The report spans five major geographic regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting adoption patterns, regulatory environments, and regional digital infrastructure readiness. It analyzes market segmentation by type (cloud-based, on-premise, hybrid), application (entertainment, marketing, education, enterprise communication, social media content creation), and end-user industries such as media & entertainment, e-learning, BFSI, healthcare, retail, and government.

The scope further extends to emerging technology areas including multimodal AI, generative editing engines, real-time captioning, synthetic media creation, edge-based intelligent editing, and cloud-collaborative workflows. It covers more than 35 active competitors, including established enterprise vendors, fast-scaling SaaS platforms, and specialized AI editing startups. The report evaluates market drivers such as mobile-first content creation, growth in short-form video, enterprise automation needs, and increasing demand for localization. It also examines challenges including algorithmic fairness, digital authenticity, and compliance requirements. Additionally, the report highlights niche segments such as AI-powered dubbing engines, automatic B-roll generation systems, and avatar-based editing. The overall scope enables decision-makers to understand growth opportunities, technological shifts, competitive pressures, and the evolving AI-driven video production ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 563 Million |

| Market Revenue (2032) | USD 953.0 Million |

| CAGR (2025–2032) | 6.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Adobe Inc., Lightricks Ltd., Veed Ltd., FlexClip, Wondershare Technology, Blackmagic Design Pty Ltd, Corel Corporation, DaVinci Resolve, Kapwing Inc., InVideo, Descript Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |