Reports

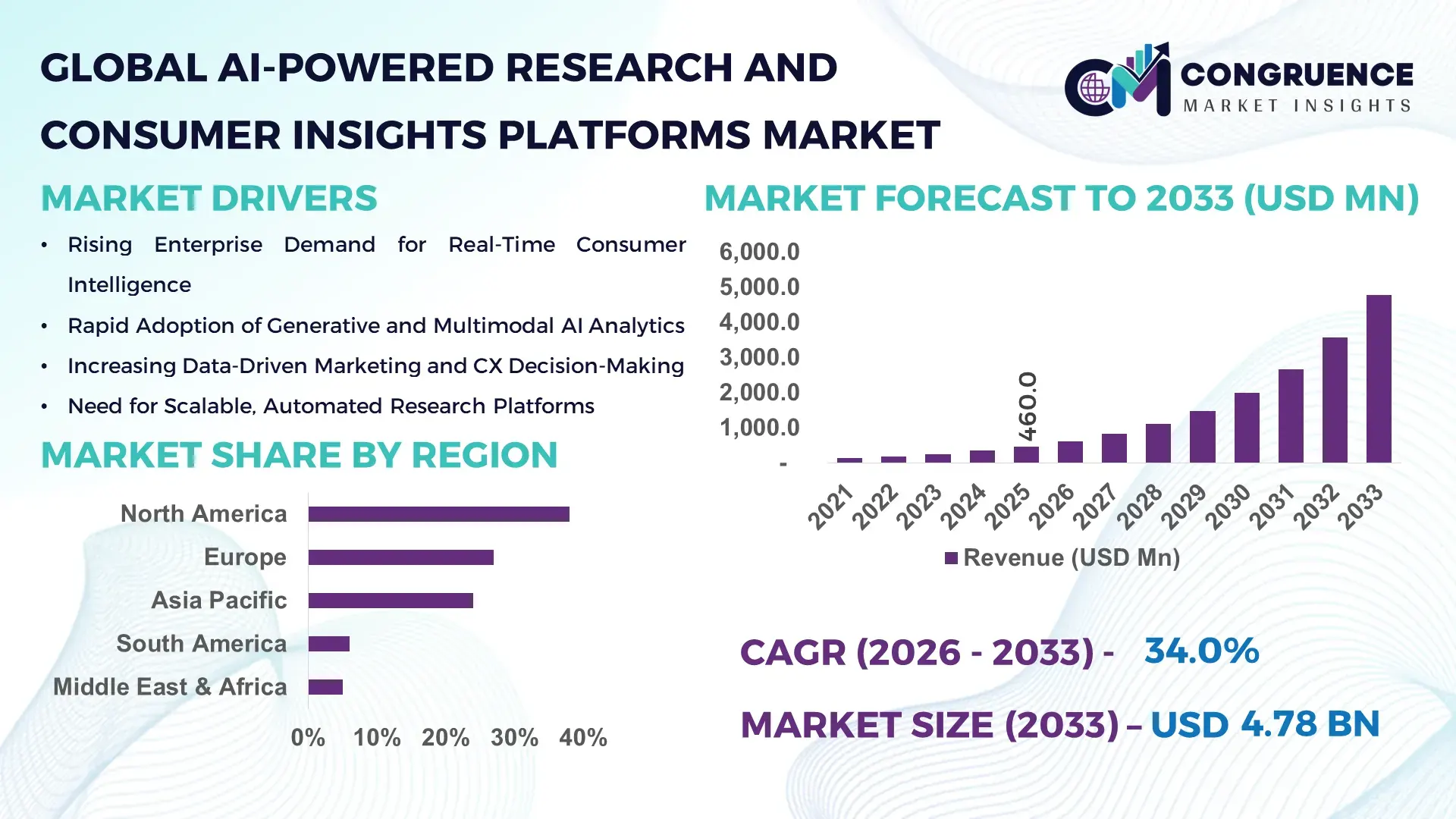

The Global AI-Powered Research and Consumer Insights Platforms Market was valued at USD 460.0 Million in 2025 and is anticipated to reach a value of USD 4,781.9 Million by 2033, expanding at a CAGR of 34% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by rapid enterprise adoption of AI-driven analytics to accelerate decision-making, improve consumer understanding, and reduce research cycle times across industries.

The United States dominates the global AI-Powered Research and Consumer Insights Platforms marketplace in terms of technology deployment and ecosystem depth. In 2025, the U.S. hosts over 45% of global AI analytics platform development centers, supported by annual private and public AI investments exceeding USD 65 billion. More than 72% of Fortune 500 companies operating in the U.S. integrate AI-powered consumer insight tools across marketing, retail analytics, product innovation, and financial services research. The country leads in advanced capabilities such as large language model (LLM)-driven qualitative analysis, real-time sentiment tracking, and predictive consumer modeling. Cloud-based AI research platforms account for nearly 68% of enterprise deployments in the U.S., while adoption among mid-sized enterprises has grown by over 40% since 2022, reflecting broad-based commercialization and scalability of AI-driven insights solutions.

Market Size & Growth: Valued at USD 460.0 Million in 2025, projected to reach USD 4,781.9 Million by 2033, growing at 34% CAGR, driven by enterprise-wide automation of market research workflows.

Top Growth Drivers: AI adoption in market research (62%), reduction in manual data processing time (55%), improvement in insight accuracy through machine learning (48%).

Short-Term Forecast: By 2028, AI-powered platforms are expected to reduce primary research costs by approximately 35% while improving data turnaround speed by 45%.

Emerging Technologies: Generative AI for qualitative insights, multimodal analytics combining text–audio–video data, and real-time consumer sentiment modeling.

Regional Leaders: North America (USD 1,950 Million by 2033; strong enterprise SaaS adoption), Europe (USD 1,320 Million; GDPR-compliant AI analytics), Asia Pacific (USD 1,080 Million; mobile-first consumer intelligence).

Consumer/End-User Trends: Marketing, retail, and FMCG enterprises account for over 50% of platform usage, with growing penetration in healthcare and BFSI research.

Pilot or Case Example: In 2024, a U.S.-based retail analytics pilot reduced campaign testing cycles by 38% using AI-driven consumer insight platforms.

Competitive Landscape: Market leader holds ~18% share, followed by Qualtrics, Talkwalker, Brandwatch, and Sprinklr.

Regulatory & ESG Impact: Increased focus on data privacy compliance and ethical AI, with over 60% platforms embedding explainable AI features.

Investment & Funding Patterns: More than USD 9.5 Billion invested globally since 2022, dominated by venture funding and strategic enterprise partnerships.

Innovation & Future Outlook: Integration of AI insights with enterprise ERP and CRM systems is shaping next-generation decision intelligence platforms.

The AI-Powered Research and Consumer Insights Platforms Market is driven by retail (32%), marketing and advertising (28%), BFSI (16%), and healthcare (12%) applications. Recent innovations in generative AI-driven qualitative analysis, stricter data privacy regulations, and increased regional demand from Asia Pacific are reshaping consumption patterns, while predictive analytics and real-time insight delivery define future growth trajectories.

The AI-Powered Research and Consumer Insights Platforms Market has become strategically critical as organizations shift from retrospective analysis toward predictive and prescriptive decision-making. Enterprises increasingly rely on AI-driven platforms to synthesize vast volumes of structured and unstructured consumer data, enabling faster go-to-market strategies and more precise demand forecasting. Advanced natural language processing now delivers 45% improvement in insight extraction accuracy compared to traditional survey analytics, while generative AI-based platforms deliver 30% faster reporting cycles than legacy business intelligence tools.

From a technology benchmark perspective, LLM-powered qualitative analysis delivers 40% higher contextual accuracy compared to rule-based text analytics, making it a preferred standard across global enterprises. Regionally, North America dominates in deployment volume, while Asia Pacific leads in adoption intensity, with over 58% of large enterprises integrating AI-powered consumer insight tools into core business operations. By 2028, real-time sentiment analytics is expected to improve campaign optimization efficiency by 42%, directly impacting customer acquisition and retention metrics.

Compliance and ESG considerations are increasingly shaping platform strategies. Firms are committing to data minimization and privacy-by-design frameworks, targeting 25% reductions in redundant data storage by 2027. In 2024, a European consumer goods company achieved a 33% reduction in research waste and rework through AI-driven automated insight validation. Looking forward, the AI-Powered Research and Consumer Insights Platforms Market is positioned as a foundational pillar supporting organizational resilience, regulatory compliance, and sustainable, data-driven growth across industries.

The AI-Powered Research and Consumer Insights Platforms Market dynamics are shaped by rapid digital transformation, rising data complexity, and the need for real-time decision intelligence. Enterprises are moving away from traditional manual research methodologies toward AI-enabled platforms capable of processing high-frequency consumer data streams. Increasing cloud adoption, integration with CRM and marketing automation systems, and demand for scalable analytics are influencing purchasing decisions. At the same time, regulatory scrutiny around data privacy and AI ethics is redefining platform architectures. The market reflects a balance between accelerated innovation cycles and the need for governance, security, and transparency, particularly across consumer-facing industries.

Enterprises now process consumer data generated across digital touchpoints at unprecedented volumes, with over 80% of customer interactions occurring through digital channels. AI-powered research platforms enable real-time sentiment analysis, reducing insight latency from weeks to hours. Marketing teams using AI-driven insights report up to 47% improvement in campaign responsiveness, while product teams achieve 35% faster concept validation. This demand for immediacy and precision is accelerating platform adoption across retail, e-commerce, and BFSI sectors.

Strict data protection regulations such as GDPR and emerging AI governance frameworks increase compliance complexity. Over 52% of enterprises cite data governance integration challenges as a barrier to AI analytics adoption. Ensuring anonymization, consent management, and explainability adds implementation time and cost. Smaller firms, in particular, face skill and infrastructure gaps, slowing platform deployment despite strong demand.

Integration of AI-powered insights with enterprise systems such as ERP, CRM, and marketing automation platforms presents a major growth opportunity. Unified analytics environments enable up to 41% improvement in cross-functional decision alignment. Expanding use cases in healthcare research, financial risk analysis, and smart retail personalization create new demand streams, especially in emerging digital economies.

Advanced AI platforms require skilled data scientists, ML engineers, and domain experts. However, over 38% of enterprises report shortages in AI analytics talent, leading to underutilization of platform capabilities. Model customization, bias mitigation, and continuous training add operational complexity, increasing total cost of ownership and slowing ROI realization.

Expansion of Generative AI in Qualitative Research: Over 60% of new platform deployments in 2025 incorporate generative AI for interview analysis, focus group synthesis, and open-ended survey interpretation, reducing manual qualitative analysis time by 50%.

Shift Toward Real-Time Consumer Sentiment Analytics: Real-time dashboards now process social, transactional, and behavioral data with latency reductions of 45%, enabling brands to adjust campaigns within 24 hours instead of traditional multi-week cycles.

Growing Adoption of Multimodal Data Analytics: Platforms combining text, voice, image, and video analytics account for 42% of enterprise upgrades, improving consumer behavior prediction accuracy by 37% across retail and media sectors.

Increased Emphasis on Ethical and Explainable AI: More than 58% of enterprises now require explainable AI features, with platforms embedding bias detection tools that reduce algorithmic risk exposure by 29%, supporting regulatory compliance and brand trust.

The AI-Powered Research and Consumer Insights Platforms Market is segmented based on type, application, and end-user, reflecting how enterprises deploy AI to transform data into actionable intelligence. By type, the market spans text-based analytics, multimodal AI systems, and emerging video- and audio-integrated models, with growing emphasis on platforms capable of handling unstructured data at scale. Application-wise, demand is concentrated in marketing intelligence, customer experience analytics, and product innovation, while newer use cases such as real-time sentiment tracking and predictive consumer behavior modeling are gaining momentum. From an end-user perspective, large enterprises dominate deployments due to scale and data availability, but adoption among SMEs and sector-specific users such as healthcare and BFSI organizations is expanding rapidly. This segmentation highlights a shift toward integrated, cross-functional insight platforms that support faster decision-making, personalization, and compliance across global markets.

The market by type includes text-based AI analytics platforms, vision-language models, audio-text analytics systems, and video-language or multimodal platforms. Text-based AI analytics currently represent the leading type, accounting for approximately 38% of overall adoption, driven by widespread use in survey analysis, social listening, and customer feedback interpretation. Vision-language models follow closely, holding around 42% of adoption, as enterprises increasingly combine image recognition with contextual understanding for retail analytics, brand monitoring, and digital ethnography. Audio-text systems account for about 25%, supporting call center analytics and voice-of-customer insights.

Video-language and fully multimodal platforms represent the fastest-growing type, with adoption expanding at an estimated 36% CAGR, driven by rising video content consumption, live-stream analytics, and AI-powered usability testing. These platforms are expected to surpass 30% adoption by 2033 as enterprises seek richer behavioral insights. Other niche types, including biometric sentiment analysis and behavioral AI engines, together contribute a combined share of roughly 15%, supporting specialized research use cases.

• In 2025, a large global streaming service deployed video-language AI systems to automatically analyze viewer reactions and content engagement patterns, improving accessibility features and personalized recommendations for over 10 million users worldwide.

By application, marketing and brand intelligence is the leading segment, accounting for approximately 34% of total platform usage, as organizations rely on AI to monitor consumer sentiment, brand perception, and campaign effectiveness across digital channels. Customer experience and journey analytics follow with around 28%, driven by real-time personalization and churn prediction initiatives. Product research and innovation analytics account for about 18%, enabling faster concept testing and feature optimization.

The fastest-growing application is real-time consumer sentiment and predictive behavior analytics, expanding at an estimated 35% CAGR, supported by increasing demand for instant insights from social media, e-commerce, and mobile platforms. Other applications, including competitive intelligence, pricing analytics, and policy research, collectively represent a combined share of roughly 20%.

Consumer adoption trends reinforce this growth. In 2025, more than 40% of global enterprises reported piloting AI-powered insight platforms for customer experience optimization, while over 60% of Gen Z consumers showed higher engagement with brands using AI-driven personalization tools.

• In 2025, AI-powered consumer insight platforms were deployed across more than 150 large retail and FMCG organizations globally, enabling faster detection of shifting consumer preferences and improving campaign response accuracy for millions of end users.

From an end-user perspective, large enterprises represent the dominant segment, accounting for approximately 46% of total adoption, due to their extensive data ecosystems, global operations, and higher investment capacity. These organizations primarily use AI-powered research platforms for omnichannel analytics, strategic planning, and global brand management. Mid-sized enterprises account for around 32%, leveraging cloud-based platforms to improve marketing efficiency and customer targeting.

The fastest-growing end-user segment is small and medium-sized enterprises (SMEs), with adoption rising at an estimated 33% CAGR, driven by affordable SaaS-based AI platforms and increasing digital commerce penetration. Other end-users, including academic institutions, public sector bodies, and non-profit research organizations, together contribute a combined share of about 22%, supporting policy analysis, social research, and public engagement studies.

Adoption indicators highlight momentum. In 2025, over 38% of enterprises globally reported piloting AI-powered research systems for customer experience platforms, while nearly 45% of digitally native brands integrated AI insights directly into decision workflows.

• In 2025, hundreds of retail and service-sector SMEs implemented AI-powered consumer insight platforms to optimize inventory planning and localized marketing strategies, achieving measurable improvements in demand forecasting accuracy and customer engagement.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 36% between 2026 and 2033.

Region-wise performance in the AI-Powered Research and Consumer Insights Platforms Market reflects varying levels of digital maturity, enterprise AI readiness, and regulatory environments. Europe held approximately 27% market share in 2025, supported by strong adoption in consumer goods, BFSI, and public-sector analytics, while Asia-Pacific accounted for nearly 24%, driven by large-scale digital consumer bases and mobile-first data ecosystems. South America and the Middle East & Africa together represented around 11%, with accelerating investments in digital marketing intelligence, media analytics, and government-led digital transformation initiatives. Regional demand is increasingly shaped by data privacy compliance, cloud infrastructure penetration, and sector-specific AI use cases, resulting in differentiated growth trajectories and adoption patterns across global markets.

The region accounted for approximately 38% of global market share in 2025, making it the largest contributor to the AI-Powered Research and Consumer Insights Platforms Market. Demand is primarily driven by technology, retail, healthcare, BFSI, and media industries, where AI-powered analytics are embedded into strategic planning and customer engagement workflows. Regulatory clarity around AI governance, combined with strong government support for innovation and cloud infrastructure, continues to accelerate adoption. Digital transformation trends include large-scale deployment of generative AI for qualitative research and real-time consumer sentiment tracking. A leading regional player has expanded its platform to integrate LLM-driven survey analysis and CRM-linked insight dashboards, enabling enterprises to reduce research turnaround time by over 40%. Regional consumer behavior shows higher enterprise adoption in healthcare and financial services, with over 65% of large organizations actively using AI-powered research platforms.

Europe held around 27% market share in 2025, with key markets including Germany, the United Kingdom, and France. Adoption is shaped by strong regulatory frameworks emphasizing data protection, ethical AI, and explainability, increasing demand for compliant and auditable research platforms. Sustainability initiatives and digital sovereignty goals further support local AI innovation. European enterprises are early adopters of explainable AI, privacy-preserving analytics, and federated learning within consumer insights platforms. A prominent regional analytics firm has focused on GDPR-aligned AI models that anonymize consumer data while maintaining analytical accuracy. Regional consumer behavior reflects that regulatory pressure directly translates into higher demand for explainable and compliant AI-powered research systems, particularly across public-sector research and regulated industries.

Asia-Pacific ranked as the third-largest region by volume in 2025, contributing approximately 24% of global demand, with China, India, and Japan as top-consuming countries. Rapid expansion of digital commerce, super-app ecosystems, and social media usage fuels demand for AI-powered consumer insight platforms. Infrastructure investments in cloud data centers and AI innovation hubs across major cities support scalability. Regional tech trends include mobile-native analytics, real-time language processing, and AI-driven personalization engines. A regional platform provider has focused on multilingual sentiment analysis across over 20 regional languages, enabling brands to localize insights at scale. Consumer behavior shows that growth is strongly driven by e-commerce and mobile AI applications, with more than 55% of enterprises prioritizing mobile-generated data in research workflows.

South America accounted for approximately 6% of global market share in 2025, led by Brazil and Argentina. Growth is supported by expanding digital media consumption, improving broadband infrastructure, and increasing adoption of AI-driven marketing analytics. Government incentives promoting digital transformation and regional trade agreements supporting cloud services have improved access to advanced analytics platforms. A local analytics provider has specialized in AI-powered language localization and sentiment analysis for Spanish and Portuguese markets, supporting regional brands in media and advertising sectors. Consumer behavior in this region shows that demand is closely tied to media analytics and language localization, with over 45% of platform usage linked to brand monitoring and social listening.

The Middle East & Africa region represented about 5% of global demand in 2025, with strong growth momentum in the UAE and South Africa. Demand is driven by digital modernization across oil & gas, construction, retail, and government services. National AI strategies, smart city initiatives, and cross-border digital trade partnerships are accelerating platform adoption. Regional enterprises increasingly deploy AI-powered insights to understand consumer behavior in rapidly urbanizing markets. A regional technology firm has launched AI-driven consumer analytics tailored for smart retail and tourism sectors, supporting data-driven urban planning. Consumer behavior varies widely, with enterprise-led adoption dominating, particularly in government-backed digital projects.

United States – 32% Market Share: Strong enterprise AI infrastructure, high digital data volumes, and early adoption across healthcare, retail, and finance drive dominance.

China – 18% Market Share: Large consumer data ecosystems, widespread mobile commerce adoption, and rapid deployment of AI analytics platforms support leadership in the AI-Powered Research and Consumer Insights Platforms Market.

The AI-Powered Research and Consumer Insights Platforms Market is characterized by a moderately fragmented competitive environment with a diverse mix of established analytics giants, specialized AI-driven insight providers, and innovative niche entrants. There are over 120 active competitors globally, ranging from full-service market research firms to SaaS platforms focused on generative AI and consumer analytics. Market positioning varies, with major players leveraging deep data repositories, proprietary AI models, and global client bases to differentiate offerings. The top 5 companies collectively hold an estimated 42–48% combined market share, indicating a competitive landscape where no single entity fully dominates, and multiple players maintain strong regional or sectoral influence.

Strategic initiatives across the market include product launches integrating advanced AI capabilities, partnerships for technology and data expansion, acquisitions to enhance research automation, and alliances aimed at embedding consumer insights tools into broader enterprise ecosystems. Innovation trends emphasize LLM-based qualitative analysis, automated trend discovery, multimodal data integration, and real-time consumer sentiment analytics. Competitors are increasingly emphasizing AI explainability, platform interoperability, and compliance with evolving data privacy regulations, as enterprises prioritize trustworthy and scalable insights. Market entrants are also forming alliances with cloud infrastructure providers to accelerate deployment and customization. This environment compels both incumbents and challengers to continuously innovate to capture evolving enterprise demand across industries such as retail, healthcare, finance, and media.

Brandwatch

YouScan

AlphaSense

Attest

Ipsos

Kantar

Forrester Research

Gartner

GfK

Material (formerly LRW)

Infotools Harmoni

Nexxt Intelligence inca

Resonate

Yabble

The technology landscape underpinning the AI-Powered Research and Consumer Insights Platforms Market is rapidly evolving, driven by innovations in machine learning, natural language processing (NLP), generative AI, and multimodal analytics tailored for complex consumer data environments. AI architectures capable of synthesizing structured and unstructured datasets are increasingly central to platform capabilities, enabling organizations to derive deeper insights from surveys, social media, CRM systems, transactional logs, and real-time behavioral signals.

Key technology trends include large language models (LLMs) optimized for consumer insight extraction, which automate the categorization, sentiment detection, and theme discovery across massive text corpora. Platforms are integrating multimodal analytics—combining text, voice, image, and video data—to enrich understanding of consumer preferences and engagement patterns, with real-time processing capabilities reducing insight latency. Neuro-symbolic AI frameworks and hybrid reasoning engines are emerging to enhance predictive accuracy and contextual understanding, allowing platforms to simulate synthetic panels and forecast consumer responses with reduced manual intervention. Tools that support privacy-preserving analytics and federated learning are growing due to increasing data protection mandates, allowing enterprises to leverage AI without compromising compliance or security.

Technological differentiation also comes from agentic AI and workflow automation tools that create bespoke analytic agents capable of navigating internal enterprise data environments and third-party sources. These agents improve workflow efficiency by automating repetitive insight generation tasks and enabling non-technical users to interact with complex datasets via conversational interfaces. Infrastructure advancements, including cloud-native deployment models, enhanced GPU acceleration, and API-first ecosystems, support scalable performance and seamless integration with enterprise systems such as CRM, ERP, and marketing automation suites. Together, these technologies are reshaping how organizations achieve actionable insights, operationalize consumer data, and maintain strategic agility in a data-driven marketplace.

• In December 2025, SaaS firm Wingify acquired AI-driven user insights platform Blitzllama to enhance its experience optimization capabilities with real-time customer feedback analysis and improve automated user research workflows. Source: www.economictimes.com

• In 2025, AWS launched Quick Suite, a new agentic AI platform enabling businesses to build and deploy AI agents that extract insights from internal repositories and third-party data, simplifying enterprise analytics workflows. Source: www.techradar.com

• In 2025, MoEngage secured $100 million in funding to expand its AI-driven consumer engagement and insights platform, accelerating international growth particularly in North America and enhancing its Merlin AI suite for marketing optimization. Source: www.timesofindia.indiatimes.com

• In 2025, Alibaba launched a new AI chatbot service within its Quark app, boosting real-time conversational consumer insights and positioning its Qwen3 model to improve reasoning and task performance for enhanced user interaction. Source: www.reuters.com

The scope of the AI-Powered Research and Consumer Insights Platforms Market Report encompasses a comprehensive examination of platform types, application domains, end-user industries, geographic regions, technologies, and competitive landscapes that define this evolving intelligence ecosystem. The report analyzes segmentation across text-based analytics, NLP-driven dashboards, multimodal AI systems, and specialized insight engines tailored for consumer behavior mapping, sentiment analysis, trend prediction, and strategic reporting. It covers key application areas including marketing and brand intelligence, customer experience optimization, product innovation research, and competitive benchmarking, detailing how platforms meet specific enterprise needs in sectors such as retail, healthcare, finance, media, and telecommunications.

Geographically, the report profiles performance dynamics in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering volume-based insight into regional technology maturity, data infrastructure investments, regulatory influences, and enterprise adoption patterns. Special focus is given to consumer behavior analytics frameworks, real-time sentiment engines, and privacy-compliant insight architectures that drive decision-making in digital-first markets. In addition, the report assesses the impact of emerging technologies such as AI agents, federated learning, synthetic data simulation, and multimodal reasoning frameworks on platform capabilities and scalability.

The competitive analysis section evaluates market positioning, strategic initiatives, innovation pipelines, and collaboration models among leading global providers, offering stakeholders actionable intelligence for vendor selection, partnership opportunities, and investment decisions. Niche segments such as voice analytics, synthetic panel generation, and real-time trend discovery are also explored, showcasing future growth avenues and technology adoption scenarios tailored to enterprise research needs. Overall, the report caters to decision-makers, data leaders, and innovation strategists seeking a multifaceted view of how AI-powered research and consumer insights platforms transform business intelligence, strategy formulation, and competitive differentiation in an increasingly data-driven world.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 460.0 Million |

| Market Revenue (2033) | USD 4,781.9 Million |

| CAGR (2026–2033) | 34.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Qualtrics, NielsenIQ, Sprinklr Insights, Brandwatch, YouScan, AlphaSense, Attest, Ipsos, Kantar, Forrester Research, Gartner, GfK, Material (formerly LRW), Infotools Harmoni, Nexxt Intelligence inca, Resonate, Yabble |

| Customization & Pricing | Available on Request (10% Customization Free) |