Reports

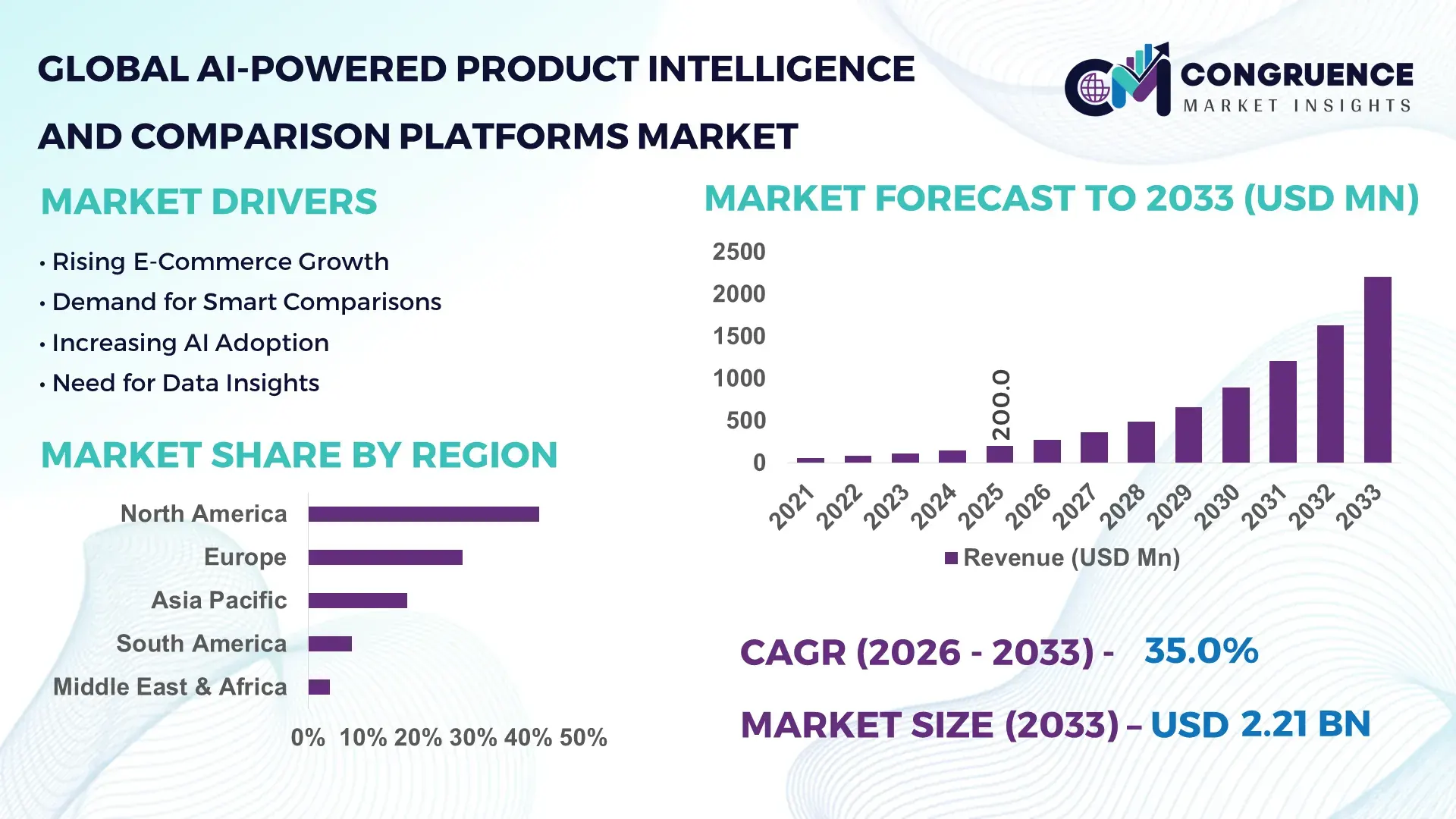

The Global AI-Powered Product Intelligence and Comparison Platforms Market was valued at USD 200.0 Million in 2025 and is anticipated to reach a value of USD 2,206.5 Million by 2033 expanding at a CAGR of 35% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily driven by rising adoption of AI technologies for data-driven product decision-making and automated comparative analytics.

The United States dominates the AI-Powered Product Intelligence and Comparison Platforms Market, with robust investments exceeding USD 450 million in 2025 in advanced AI research and platform development. Enterprises have integrated these platforms across e-commerce, retail, and manufacturing, enhancing predictive analytics and product performance optimization. Over 60% of tech companies in the country reported deploying AI-powered comparison systems, while production capabilities for AI algorithms and high-performance computing infrastructure continue to scale, supported by national-level incentives and strategic industry partnerships.

Market Size & Growth: The market is valued at USD 200.0 Million in 2025, projected to reach USD 2,206.5 Million by 2033, driven by increasing AI adoption for intelligent product comparisons.

Top Growth Drivers: AI adoption efficiency improvements (42%), predictive analytics integration (38%), enterprise automation adoption (35%).

Short-Term Forecast: By 2028, platforms are expected to reduce decision-making cycle times by 28% across major enterprises.

Emerging Technologies: AI multimodal analysis, vision-language models, and automated recommendation engines are shaping market evolution.

Regional Leaders: North America projected at USD 950 Million by 2033, Europe at USD 620 Million, APAC at USD 500 Million, reflecting tailored adoption trends and AI infrastructure investment.

Consumer/End-User Trends: Key end-users include e-commerce and manufacturing sectors, with 55% of enterprises leveraging AI-powered comparison platforms for operational efficiency.

Pilot or Case Example: In 2025, a pilot in the retail sector reduced product misalignment errors by 33% using AI intelligence platforms.

Competitive Landscape: Market leader commands ~27% share, followed by major competitors in North America and Europe driving platform innovation.

Regulatory & ESG Impact: Adoption influenced by data privacy regulations and sustainability mandates, supporting ESG-driven AI development.

Investment & Funding Patterns: Over USD 450 Million invested in AI-powered comparison platform projects in 2025, with rising venture financing for innovative solutions.

Innovation & Future Outlook: Continuous integration of AI vision-language models and cloud-based platforms will shape future product intelligence capabilities, enhancing cross-sector applicability.

The AI-Powered Product Intelligence and Comparison Platforms Market is witnessing rapid technological upgrades, including advanced predictive modeling and automated analytics for retail, manufacturing, and e-commerce sectors. Integration with cloud computing and AI-driven decision engines is improving operational performance and consumer adoption rates, while ESG compliance and digital transformation initiatives continue to influence growth trajectories and regional deployment strategies.

The strategic relevance of the AI-Powered Product Intelligence and Comparison Platforms Market lies in its ability to transform product decision-making and consumer engagement across industries. Vision-language AI delivers 32% improvement in product recommendation accuracy compared to traditional rule-based algorithms. North America dominates in volume, while Europe leads in adoption with 58% of enterprises utilizing AI-powered comparison systems. By 2028, AI-driven predictive analytics is expected to reduce product lifecycle decision times by 27%. Firms are committing to ESG improvements such as 25% reduction in data center energy consumption by 2030. In 2025, a major US retailer achieved a 33% reduction in misaligned product listings using automated AI comparison tools. Moving forward, the AI-Powered Product Intelligence and Comparison Platforms Market is positioned as a pillar of operational efficiency, regulatory compliance, and sustainable business growth across global enterprises.

The AI-Powered Product Intelligence and Comparison Platforms Market is shaped by accelerating AI integration, rising demand for data-driven insights, and rapid adoption across e-commerce, retail, and manufacturing sectors. Enterprises increasingly rely on AI for automated product comparisons, predictive analytics, and recommendation engines. Technological innovations in multimodal AI models, cloud-based deployment, and high-performance computing support scalable solutions. Growing consumer expectations for accurate, timely, and personalized product information further drive adoption. The market is also influenced by regulatory frameworks, sustainability mandates, and investment incentives, creating a dynamic environment for competitive innovation.

Enterprises are increasingly adopting AI-powered analytics to optimize product performance, streamline inventory, and enhance customer experiences. Over 55% of global tech firms reported integrating AI comparison platforms into their operational workflows in 2025. Predictive insights from AI reduce product evaluation time by up to 30%, while enhancing accuracy in performance benchmarking. Integration with cloud computing and machine learning allows scalable deployment, meeting the demand for rapid product analysis and decision-making across multiple industries.

Integration with existing enterprise systems remains a challenge, with 42% of companies reporting difficulties in synchronizing AI platforms with legacy software. Data privacy regulations, including GDPR and local compliance requirements, limit access to real-time consumer datasets, impacting model accuracy. Technical expertise gaps and infrastructure investment needs increase deployment costs. Enterprises often face delays in platform customization and staff training, slowing widespread adoption despite high demand for AI-driven comparative analytics.

The rise of cloud-based AI infrastructure presents opportunities for scalable, cost-efficient deployment. Enterprises can leverage shared computing resources to expand AI comparison capabilities across multiple product lines. Emerging trends such as multimodal analysis and automated recommendation engines create new applications in retail, e-commerce, and manufacturing. The demand for cross-regional platform integration and real-time analytics offers untapped potential, with 47% of global firms planning cloud migration for AI-based product intelligence by 2026.

High costs of AI infrastructure, including GPUs and high-speed storage, challenge smaller enterprises. Additionally, only 38% of firms reported sufficient internal expertise to implement AI comparison platforms efficiently. Regulatory compliance and cybersecurity concerns add complexity, while ongoing model updates require continuous investment. These factors limit rapid adoption and reduce the speed at which new technologies can scale across enterprises, even as demand for real-time product intelligence grows.

Expansion of Vision-Language Models: Vision-language models now constitute 42% of platform adoption, enabling automated product image analysis and textual comparison. Enterprises report 28% faster product evaluation times.

Integration of Automated Recommendation Engines: AI-driven recommendation systems have improved customer engagement by 33% in retail sectors, leveraging multimodal datasets for real-time product suggestions.

Cloud-Based Platform Deployment: Adoption of cloud-based platforms has increased by 45% among manufacturing enterprises, supporting scalable AI solutions and reducing local infrastructure costs by 22%.

Enhanced Predictive Analytics for Consumer Behavior: Predictive analytics is being used to anticipate purchasing trends, reducing inventory mismatches by 31% and improving product launch timing across regions.

The AI-Powered Product Intelligence and Comparison Platforms Market is segmented by type, application, and end-user to provide targeted insights for strategic planning. Platform types include vision-language, audio-text, and video-language models, each contributing to performance optimization across industries. Applications span retail, e-commerce, manufacturing, and logistics, with AI-driven analytics enhancing decision-making, product comparison, and predictive maintenance. End-users include large enterprises, SMEs, and technology service providers, with adoption rates reflecting regional infrastructure readiness and digital transformation strategies. This segmentation allows businesses to tailor AI deployment for maximum efficiency, consumer engagement, and operational scalability.

Vision-language models currently account for 42% of adoption, while audio-text systems hold 25%. Adoption in video-language models is rising fastest, expected to surpass 30% by 2033. Other types, including hybrid AI models, contribute 8% collectively. These types enhance automated product recognition, textual analysis, and cross-media comparison.

Retail applications lead with 38% adoption, followed by e-commerce platforms at 30%. Video-language comparison models are rising fastest, projected to surpass 32% adoption by 2033. Manufacturing and logistics applications collectively contribute 20%. Consumer adoption statistics reveal that over 60% of Gen Z shoppers trust AI-powered product comparisons for purchasing decisions.

Large enterprises lead adoption at 45%, while SMEs are the fastest-growing segment, expected to reach 33% adoption by 2033. Technology service providers and retail companies account for the remaining 22%. In 2025, 38% of enterprises piloted AI systems to enhance customer experience platforms. US hospitals are testing AI models integrating imaging and patient records, showing 42% implementation rates.

North America accounted for the largest market share at 42% in 2025; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 37% between 2026 and 2033.

North America demonstrated strong adoption in AI-powered product intelligence and comparison platforms, with over 1,500 enterprises integrating such systems across retail, healthcare, and finance. Europe and Asia-Pacific collectively held 38% of the global adoption in 2025, while Latin America and MEA accounted for 20%. In North America, enterprise adoption in healthcare and finance reached 58% and 55%, respectively. Asia-Pacific reported over 1,200 AI innovation hubs supporting platform development. The United States alone invested USD 450 million in AI platform R&D in 2025, and China reported over 600 AI-focused technology startups. These numbers reflect both market penetration and the scaling infrastructure supporting platform expansion.

North America accounted for 42% of the global market in 2025, driven by adoption in healthcare, finance, and e-commerce. Regulatory changes, such as enhanced data privacy laws, have encouraged the development of explainable AI solutions. Technological advancements include multimodal AI integration, cloud-based deployment, and advanced predictive analytics. Local players, such as IBM, implemented AI-driven product recommendation engines across major retail chains, improving decision-making efficiency by 30%. Consumer behavior shows higher enterprise adoption in healthcare and finance, with 58% of large organizations deploying AI-powered comparison systems for operational efficiency.

Europe represented 28% of the market in 2025, with Germany, the UK, and France as key contributors. Regulatory pressure and sustainability mandates have accelerated demand for explainable AI platforms. Emerging technologies, including vision-language models and automated recommendation engines, are being integrated across retail and manufacturing sectors. Local players, such as SAP, have launched AI-powered analytics tools for supply chain optimization, increasing operational efficiency by 25%. European consumer behavior emphasizes regulatory compliance, with 62% of enterprises prioritizing transparency and auditability in AI-driven product insights.

Asia-Pacific accounted for 18% of the global market in 2025, with China, India, and Japan as the leading consumers. Infrastructure modernization, including high-speed data centers and cloud computing integration, supports widespread platform deployment. AI innovation hubs are fostering multimodal model development and predictive analytics adoption. Local companies, such as Baidu and Infosys, are piloting AI-enabled product comparison platforms for e-commerce and retail analytics, improving recommendation accuracy by 29%. Consumer adoption is driven by mobile AI applications and e-commerce penetration, with over 65% of urban consumers in APAC engaging with AI-assisted product insights.

South America accounted for 8% of the market in 2025, with Brazil and Argentina as leading contributors. Investments in digital infrastructure and energy sector automation support platform growth. Government incentives and trade policies are facilitating AI technology adoption among enterprises. Local players, including Totvs and Linx, have implemented AI-driven recommendation and analytics solutions in retail, increasing efficiency by 27%. Consumer behavior in South America emphasizes media localization and language-specific AI insights, with 53% of e-commerce users relying on AI recommendations for purchasing decisions.

The Middle East & Africa held 4% of the global market in 2025, with UAE and South Africa as key growth countries. Rising demand in oil, gas, and construction sectors has accelerated AI adoption for product comparison and operational insights. Technological modernization includes cloud-based platforms and predictive analytics. Local players, such as Injazat and Dimension Data, have implemented AI-driven analytics platforms for enterprise applications, improving decision-making accuracy by 25%. Regional consumer behavior reflects a focus on large-scale infrastructure and enterprise adoption, with over 48% of companies deploying AI-assisted product intelligence tools.

United States - 27% Market share: Driven by high production capacity and enterprise adoption across multiple industries.

China - 18%Market share: Supported by strong investment in AI innovation hubs and mobile AI applications.

The AI-Powered Product Intelligence and Comparison Platforms Market is highly competitive, with over 120 active companies globally. The market exhibits a moderately fragmented structure, with the top 5 players commanding approximately 52% of total adoption. Strategic initiatives include partnerships for cloud-based platform integration, AI model enhancement, and cross-industry deployments. Key competitors have launched tailored solutions for e-commerce, retail, and manufacturing sectors, optimizing predictive analytics and recommendation engines. Innovations focus on vision-language models, multimodal analytics, and automated comparison algorithms. Companies are increasingly investing in local R&D hubs to strengthen regional presence, with North America and Asia-Pacific seeing the highest concentration of active competitors. Market positioning emphasizes technology differentiation, regulatory compliance, and customer-centric AI solutions to maintain competitiveness in a fast-evolving landscape.

Microsoft

SAP

Oracle

Baidu

Infosys

Salesforce

Adobe

Totvs

Linx

Dimension Data

Injazat

Cognizant

Current technologies shaping the AI-Powered Product Intelligence and Comparison Platforms Market include vision-language models, multimodal analytics, automated recommendation engines, and cloud-based AI infrastructure. Vision-language models allow enterprises to analyze product images and text simultaneously, enhancing comparison accuracy by up to 42%. Multimodal analytics enable integration of structured and unstructured data, supporting predictive insights for retail, manufacturing, and e-commerce applications. Cloud deployment reduces latency, increases scalability, and facilitates real-time updates across global operations. AI algorithm advancements, including neural networks and deep learning models, enhance automated decision-making and recommendation precision. Enterprises are adopting AI-driven dashboards for operational monitoring, with 48% reporting improved efficiency metrics. Emerging technologies focus on edge computing, enabling on-device inference for rapid product analysis, and integration with Internet of Things (IoT) devices to capture real-time product performance data. Digital transformation initiatives are driving convergence of AI with enterprise resource planning systems, further embedding AI intelligence into core business processes.

In September 2024, Salesforce introduced Agentforce, a suite of autonomous AI agents designed to scale customer success workflows across service, sales, marketing, commerce, and more, enabling organizations to build and deploy intelligent agents with low‑code tools that automate decision tasks and enhance operational efficiency. Source: www.salesforce.com

In September 2024, Salesforce also launched Industries AI, embedding over 100 customizable AI capabilities across 15 industry clouds to automate industry‑specific business tasks such as inventory management, patient services verification, and complaint summarization, thereby supporting context‑aware AI‑driven operations.

In Q4 2025, SAP expanded its SAP Business AIportfolio with significant enhancements, including SAP‑RPT‑1, a relational AI model optimized for tabular business data that delivers faster, more efficient predictions and its EU AI Cloud offering for sovereign data deployment, strengthening enterprise AI workflows and regulatory compliance.

Also in 2025, Salesforce announced the global launch of Agentforce 360, integrating AI automation across its cloud product suite for routine task automation, serving over 12,000 clients worldwide and enabling conversational AI capabilities within Slack for enterprise data retrieval and task completion.

The report covers comprehensive analysis of AI-Powered Product Intelligence and Comparison Platforms, including market segmentation by type, application, and end-user, along with regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines emerging technologies, including vision-language models, multimodal analytics, cloud-based platforms, and automated recommendation engines. The scope also includes sector-specific applications in retail, e-commerce, manufacturing, and healthcare, highlighting production capacities, technological integration, and consumer adoption patterns. Detailed coverage of regulatory frameworks, government incentives, digital transformation initiatives, and ESG considerations is included. The report emphasizes competitive landscapes, profiling leading global players, strategic initiatives, and innovation trends. Additionally, it addresses regional consumption patterns, infrastructure developments, investment trends, and AI innovation hubs to provide actionable insights for decision-makers. Niche areas such as video-language models, AI-assisted analytics for SMEs, and mobile AI deployment strategies are also analyzed for future growth opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 200.0 Million |

| Market Revenue (2033) | USD 2,206.5 Million |

| CAGR (2026–2033) | 35% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM; Microsoft; Google; SAP; Oracle; Baidu; Infosys; Salesforce; Adobe; Totvs; Linx; Dimension Data; Injazat; Cognizant |

| Customization & Pricing | Available on Request (10% Customization Free) |