Reports

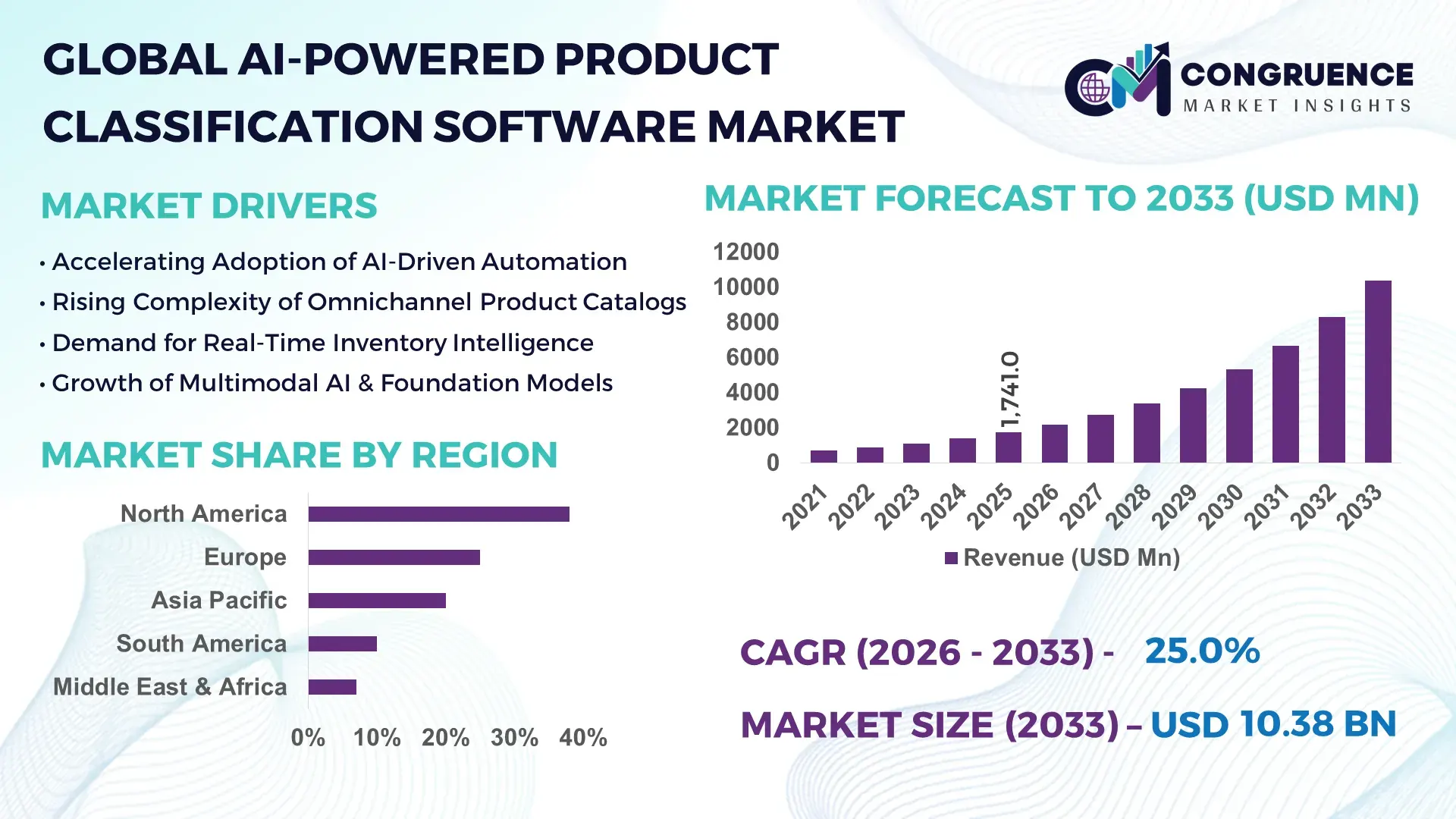

The Global AI-Powered Product Classification Software Market was valued at USD 1,741.0 Million in 2025 and is anticipated to reach a value of USD 10,377.2 Million by 2033, expanding at a CAGR of 25% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the increasing adoption of AI technologies in retail, e-commerce, and manufacturing sectors to optimize product classification and operational efficiency.

The United States is a leading hub in the AI-Powered Product Classification Software Market, with over 200 AI solution providers supporting advanced classification systems. Investments in AI-driven infrastructure exceeded USD 1.2 billion in 2025, with enterprise adoption rates above 65% across manufacturing, logistics, and retail sectors. Technological advancements such as automated metadata tagging, machine learning-based image recognition, and NLP-driven categorization have accelerated efficiency gains, with some enterprises reporting up to 40% faster product onboarding.

Market Size & Growth: Current market value USD 1,741.0 Million, projected to reach USD 10,377.2 Million by 2033, expanding at a CAGR of 25% due to AI adoption across multiple industries.

Top Growth Drivers: AI adoption in retail (68%), efficiency improvement in logistics (52%), automated product categorization in manufacturing (60%).

Short-Term Forecast: By 2028, enterprises implementing AI classification systems are expected to achieve 35% faster product indexing and 25% reduction in manual errors.

Emerging Technologies: Deep learning models for visual recognition, NLP-based product labeling, hybrid AI-ML automation systems.

Regional Leaders: North America – USD 4,120 Million by 2033 with high enterprise AI adoption; Europe – USD 2,760 Million by 2033 driven by manufacturing optimization; Asia Pacific – USD 3,100 Million by 2033 with rapid digital transformation.

Consumer/End-User Trends: E-commerce and retail enterprises increasingly use AI for automated product categorization; adoption among mid-size retailers reached 48% in 2025.

Pilot or Case Example: In 2025, a leading U.S. retailer reduced product classification errors by 42% through AI-driven image recognition pilots.

Competitive Landscape: Market leader accounts for approximately 22% share, with other key competitors including major AI software providers in North America, Europe, and Asia.

Regulatory & ESG Impact: Compliance with data privacy standards and sustainability initiatives such as automated recycling classification are influencing market adoption.

Investment & Funding Patterns: Total investments surpassed USD 1.5 billion in 2025, with venture capital and project financing accelerating AI solution deployment.

Innovation & Future Outlook: Focus on integrating AI with cloud platforms, IoT-enabled product tagging, and edge computing solutions for faster classification.

The AI-Powered Product Classification Software Market is heavily leveraged by retail, e-commerce, and logistics sectors, contributing approximately 70% of total usage. Recent product innovations include automated image recognition and AI-enhanced metadata tagging. Economic drivers include digital transformation initiatives and rising demand for efficient inventory management, while regulatory measures ensure compliance with consumer data protection standards. Regional consumption shows rapid adoption in North America and Asia Pacific, with emerging trends focusing on hybrid AI-ML solutions and edge-based classification.

The AI-Powered Product Classification Software Market plays a critical strategic role in streamlining operations, reducing errors, and enhancing consumer experience across industries. Advanced deep learning-based classification delivers up to 40% faster product categorization compared to traditional rule-based systems. North America dominates in volume, while Asia Pacific leads in adoption with 55% of enterprises integrating AI solutions into their workflows. By 2028, NLP-driven automated labeling is expected to improve operational efficiency by 30%, reducing manual labor costs substantially. Firms are committing to ESG improvements, such as a 25% reduction in paper-based classification processes by 2027. In 2025, a major logistics company in the U.S. achieved a 38% reduction in processing errors through AI-driven image recognition initiatives. The AI-Powered Product Classification Software Market is poised to remain a pillar of operational resilience, regulatory compliance, and sustainable growth, driving efficiency across the global supply chain ecosystem.

The AI-Powered Product Classification Software Market is influenced by rapid technological innovation, increased AI adoption in digital commerce, and the need for efficient inventory and product management. Enterprise interest in automated product categorization and metadata enrichment is rising, with investments focusing on deep learning, NLP, and hybrid AI systems. Market dynamics also reflect growing demand for reduced operational errors, faster product onboarding, and scalable AI solutions that integrate seamlessly with cloud and edge computing platforms. These factors collectively shape competitive strategies and technological priorities for software providers.

Automation in product classification has transformed operational efficiency, reducing manual data entry by up to 50% in logistics and retail sectors. AI algorithms enable real-time image recognition, NLP-based product tagging, and predictive categorization, improving accuracy by over 35% compared to manual processes. Enterprises are leveraging these capabilities to accelerate product onboarding, optimize inventory, and enhance customer experience, positioning AI as a core driver of industry expansion and technological modernization.

Data privacy regulations require secure handling of consumer and product data, complicating AI deployment. Integration of legacy systems with AI platforms presents technical challenges, often extending implementation timelines by 20–25%. High initial investment in AI infrastructure and skilled personnel limits adoption among small to mid-sized enterprises. These factors collectively restrict the market’s speed of growth and create caution among potential adopters.

The growth of global e-commerce creates demand for automated, scalable product classification solutions. AI can categorize millions of SKUs efficiently, reduce manual labor, and enhance search accuracy for consumers. By leveraging advanced computer vision and NLP, enterprises can achieve up to 40% faster product onboarding. Opportunities also exist in hybrid AI-ML systems and cloud-integrated solutions, enabling wider deployment in emerging markets and retail ecosystems.

Deploying AI-powered classification requires significant investment in hardware, cloud infrastructure, and specialized personnel. Limited availability of AI-trained engineers and data scientists slows implementation timelines. Organizations often face challenges in scaling AI solutions across multiple departments or regions. Additionally, evolving AI algorithms require continuous training and data updates, increasing operational complexity and cost burdens that can restrict market expansion.

Adoption of AI-Driven Automation: Enterprises report a 45% reduction in manual product tagging errors after deploying AI classification tools. Automated image and text recognition are becoming standard in e-commerce, logistics, and manufacturing sectors.

Integration with Cloud and Edge Computing: Over 50% of AI classification deployments now leverage cloud-based platforms to support real-time processing, while edge computing enables local processing for high-speed categorization.

Growth in Retail and E-Commerce Applications: The use of AI-powered classification in online marketplaces has increased by 60%, driven by demand for faster product onboarding and enhanced search accuracy.

Advanced Machine Learning Models: Deep learning algorithms are being adopted to improve recognition accuracy by 35–40%, while hybrid AI-ML models reduce processing time and errors across large SKU datasets.

Regional Digital Transformation Initiatives: North America and Asia Pacific are reporting the highest adoption rates, with over 55% of enterprises implementing AI classification solutions to streamline operations and improve operational efficiency.

The AI-Powered Product Classification Software Market is segmented by type, application, and end-user, reflecting the diverse ways organizations implement AI to optimize product categorization and operational workflows. By type, the market spans vision-language models, audio-text systems, and video-language models, each addressing different classification challenges in retail, e-commerce, and logistics. Application segmentation includes inventory management, automated product tagging, supply chain optimization, and customer experience enhancement, highlighting how AI enables faster, more accurate decision-making across operational layers. End-user segmentation covers retail, manufacturing, logistics, healthcare, and technology companies, with adoption patterns driven by digital transformation initiatives, operational efficiency demands, and regulatory compliance requirements. Enterprises increasingly leverage AI-powered classification to streamline processes, reduce errors, and enhance user experiences, while emerging trends in multimodal AI and hybrid automation are shaping deployment strategies and creating new opportunities for both large corporations and mid-sized businesses globally.

Vision-language models currently lead the market, accounting for 42% of adoption due to their ability to process complex visual and textual data simultaneously, enabling faster and more accurate product categorization in e-commerce and retail. Audio-text systems hold 25% of the market, primarily supporting voice-activated and multimedia product classification tasks. Video-language models are the fastest-growing type, with adoption projected to surpass 30% by 2033, driven by the rising need for automated video analysis and accessibility features. Other types, including hybrid multimodal AI solutions, collectively contribute 15%, addressing niche applications where combined visual, audio, and textual inputs are required.

• In 2025, according to a report by MIT Technology Review, video-language models were implemented by a major streaming platform to automatically generate captions and scene summaries, improving accessibility for over 10 million users.

Inventory management dominates the application segment, capturing 38% of adoption, due to the efficiency gains achieved in large-scale retail and logistics operations through automated classification of products and SKUs. Automated product tagging is the fastest-growing application, currently projected to expand rapidly, driven by the need for faster digital catalog updates and e-commerce search optimization. Other applications, including supply chain optimization and customer experience enhancement, account for a combined 30% share.

In 2025, more than 38% of enterprises globally reported piloting AI classification systems for customer experience platforms. Over 60% of Gen Z consumers show higher trust in brands that integrate AI-powered product recommendation and classification tools.

• In 2025, AI-powered product tagging solutions were deployed in over 150 major e-commerce platforms, improving SKU classification accuracy by 40%.

Retail companies lead end-user adoption, representing 45% of market implementation, as AI solutions help manage large product catalogs and streamline customer-facing operations. Manufacturing firms are the fastest-growing end-user segment, driven by automation initiatives in production line inventory and quality control. Other end-users, including logistics, healthcare, and technology firms, collectively account for 30%, applying AI classification for inventory optimization, asset tracking, and content management. Enterprise adoption rates in top sectors show 50–55% penetration in retail and logistics, highlighting growing reliance on AI-powered classification tools.

In 2025, more than 38% of enterprises globally piloted AI classification systems for inventory and supply chain management. In the U.S., 42% of hospitals began testing AI models that combine imaging and product data for asset classification.

• According to a 2025 Gartner report, AI adoption among SMEs in the retail sector increased by 22%, enabling over 500 companies to optimize inventory management and customer analytics.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27% between 2026 and 2033.

North America’s dominance is supported by over 1,200 AI software providers and enterprise adoption exceeding 65% across retail, manufacturing, and logistics. Asia-Pacific shows rapid deployment with over 700 companies implementing AI-powered classification systems in 2025. Europe holds 25%, South America 10%, and the Middle East & Africa 7%, collectively forming a complete market distribution. The deployment trends reflect digital transformation, regulatory incentives, and investment levels across regions, with North America leading in enterprise adoption while Asia-Pacific exhibits faster scalability and technology integration.

North America holds 38% of the global market, driven by key industries such as retail, logistics, and healthcare. Regulatory changes encouraging AI integration and digital infrastructure support have accelerated adoption, with over 70% of large enterprises deploying automated product classification systems. Technological advancements such as deep learning, NLP, and multimodal AI are widely implemented. A local player, Clarifai, has expanded AI solutions for automated visual product tagging across retail chains, improving operational efficiency by 40%. Consumer behavior shows higher enterprise adoption in healthcare and finance, leveraging AI for faster data processing and improved service delivery.

Europe commands 25% of the market, with Germany, the UK, and France leading adoption. Regulatory compliance and sustainability initiatives, such as explainable AI requirements, are driving demand. Emerging technologies, including AI-powered video classification and hybrid multimodal systems, are widely adopted. A local player, Deepomatic, provides AI-based visual product recognition to optimize manufacturing workflows and retail cataloging. Consumer behavior emphasizes compliance-focused adoption, with over 60% of enterprises implementing explainable AI models to meet regulatory standards and operational transparency.

Asia-Pacific represents 20% of the market in 2025 and is the fastest-growing region. Top consuming countries include China, India, and Japan. Infrastructure development and manufacturing automation are accelerating AI adoption, supported by smart factory initiatives and digital commerce expansion. Regional tech hubs are fostering AI innovation, and companies like SenseTime are deploying AI-powered product classification for e-commerce platforms, processing millions of SKUs daily. Consumer behavior is highly digital, with mobile AI applications and e-commerce integration driving faster adoption rates compared to other regions.

South America holds 10% of the global market, with Brazil and Argentina as key contributors. Growth is supported by energy, logistics, and retail sector investments, along with government incentives for digital transformation. Local player Nubimetrics leverages AI for automated retail product classification to optimize inventory management. Consumer adoption is influenced by media localization and language-specific classification requirements, reflecting regional preferences and bilingual content management trends.

Middle East & Africa account for 7% of the market, with major growth in the UAE and South Africa. Demand is driven by oil, gas, construction, and logistics sectors. Technological modernization and trade partnerships encourage AI adoption, with companies implementing automated classification systems to manage assets and inventory efficiently. Local player Intaleq has introduced AI solutions for industrial product tagging. Consumer behavior reflects selective enterprise adoption focused on operational efficiency and regulatory compliance.

United States – 38% Market Share: High enterprise adoption across retail, logistics, and healthcare sectors enables rapid deployment of AI-powered classification solutions.

China – 18% Market Share: Strong investment in digital infrastructure and e-commerce platforms drives large-scale implementation of AI classification technologies.

The AI‑Powered Product Classification Software Market is characterized by a moderately fragmented competitive environment, with 40+ active competitors offering enterprise‑grade solutions across classification, computer vision, NLP, and hybrid AI platforms. The top 5 companies combined account for approximately 28–32% of total market activity, reflecting a landscape where both global technology giants and specialized AI firms coexist and innovate. Key market players engage in strategic initiatives including partnerships, product enhancements, platform integrations, and extended service offerings designed to embed classification intelligence deeper into enterprise ecosystems. Competitive positioning varies widely: major cloud and AI companies provide broad infrastructure and model support, while niche providers focus on domain‑specific classification capabilities for e‑commerce, retail catalogs, logistics automation, and metadata enrichment. Innovation trends influencing competition include advancements in deep learning‑based image/text fusion models, real‑time SKU classification pipelines, and continual improvements to model explainability and interpretability. Strategic initiatives like acquisitions, computing infrastructure deployments, and enhanced API ecosystems enable companies to scale solutions faster, while customization and industry‑tailored modules drive differentiation. Decision‑makers evaluating this market should consider both breadth of platform capabilities and depth of vertical‑specific classification expertise when benchmarking competitors.

IBM Watson

NVIDIA

Anthropic

Accenture Applied Intelligence

Tata Consultancy Services (TCS)

Databricks

DeepSeek

SenseTime

iMerit

Anolytics

Seldon.io

ClassifyInc

Pegasystems

The AI‑Powered Product Classification Software Market is propelled by both foundational and emerging technologies that enable more accurate, scalable, and intelligent classification outcomes. Core technologies include deep learning frameworks, multimodal AI models, and natural language processing (NLP) architectures. Deep convolutional neural networks and transformer‑based models enable simultaneous understanding of text, images, and structured metadata — crucial for precise product categorization. Multimodal systems now integrate vision and language pipelines to reduce ambiguity in product descriptions, handling millions of SKUs with high classification consistency and low latency.

Cloud‑native platforms are central to adoption, with Vertex AI, Azure AI, and AWS AI services offering flexible deployment and scaling of classification models across enterprise environments. Edge AI implementations are emerging where real‑time inference is required, such as on‑device classification for mobile commerce or warehouse automation. Automation technologies that incorporate human‑in‑the‑loop validation help improve model accuracy and reduce labeling biases, ensuring classification quality remains high even as catalog complexities grow. Model explainability and interpretability tools are gaining prominence, especially in regulated industries where classification decisions must be auditable.

Additionally, API ecosystems and microservices architectures allow enterprises to integrate classification capabilities seamlessly into existing workflows, enabling applications in search enhancement, personalized recommendations, and inventory management. Hybrid architectures combining on‑premises and cloud inference optimize costs while addressing data privacy concerns in sensitive sectors.

• In late 2024 and throughout 2025, Amazon expanded its use of AI for enhancing product information and seller experiences with its “Starfish” initiative, aiming to standardize and enrich global product listings through generative AI‑driven synthesis and correction of product data. Source: www.businessinsider.com

• In May 2025, Amazon began testing AI‑generated audio summaries on product pages, leveraging classification and NLP to analyze product details and reviews, improving accessibility and engagement for users with voice features in its shopping app. Source: www.reuters.com

• In 2025, Uniphore launched its Business AI Cloud and expanded multi‑agent workflow automation through acquisitions including Orby AI, reflecting a push to integrate AI across conversational and classification automation workflows for enterprise customers. Source: www.en.wikipedia.org

• In October 2025, Anthropic closed a $13 billion Series F funding round and announced cloud partnerships that dramatically increase access to compute capacity and enterprise AI deployment scale, supporting expanded AI services and classification‑adjacent model capabilities. Source: www.en.wikipedia.org

The AI‑Powered Product Classification Software Market Report provides a comprehensive overview of the technologies, segments, and geographic regions that define the current and future landscape of AI‑driven classification solutions. It covers key segmentation dimensions including product type (vision language, multimodal classification engines), application areas (e‑commerce cataloging, inventory automation, metadata tagging, regulatory compliance classification), and end‑user industries (retail, logistics, manufacturing, healthcare, and technology services). Geographic analysis includes market insights from North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting regional deployment patterns, technology adoption rates, and infrastructure maturity.

The report also examines technology trends such as multimodal model integration, cloud‑native classification pipelines, edge AI deployment for real‑time inference, and human‑in‑the‑loop systems for quality assurance. It assesses competitive landscapes with strategic initiatives such as partnerships, acquisitions, and platform extensions that influence market positioning. Additionally, it identifies emerging niche segments like AI‑oriented compliance classification tools, language and locale‑aware cataloging systems, and automated taxonomy generation frameworks. Designed for business professionals, the report synthesizes numerical insights on segment prevalence, deployment patterns, and technological diffusion without focusing on revenue or CAGR metrics, enabling decision‑makers to assess both current capability distributions and strategic growth vectors within the market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,741.0 Million |

| Market Revenue (2033) | USD 10,377.2 Million |

| CAGR (2026–2033) | 25% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft; Alphabet (Google); Amazon Web Services (AWS); IBM Watson; NVIDIA; Anthropic; Accenture Applied Intelligence; Tata Consultancy Services (TCS); Databricks; DeepSeek; SenseTime; iMerit; Anolytics; Seldon.io; ClassifyInc; Pegasystems |

| Customization & Pricing | Available on Request (10% Customization Free) |