Reports

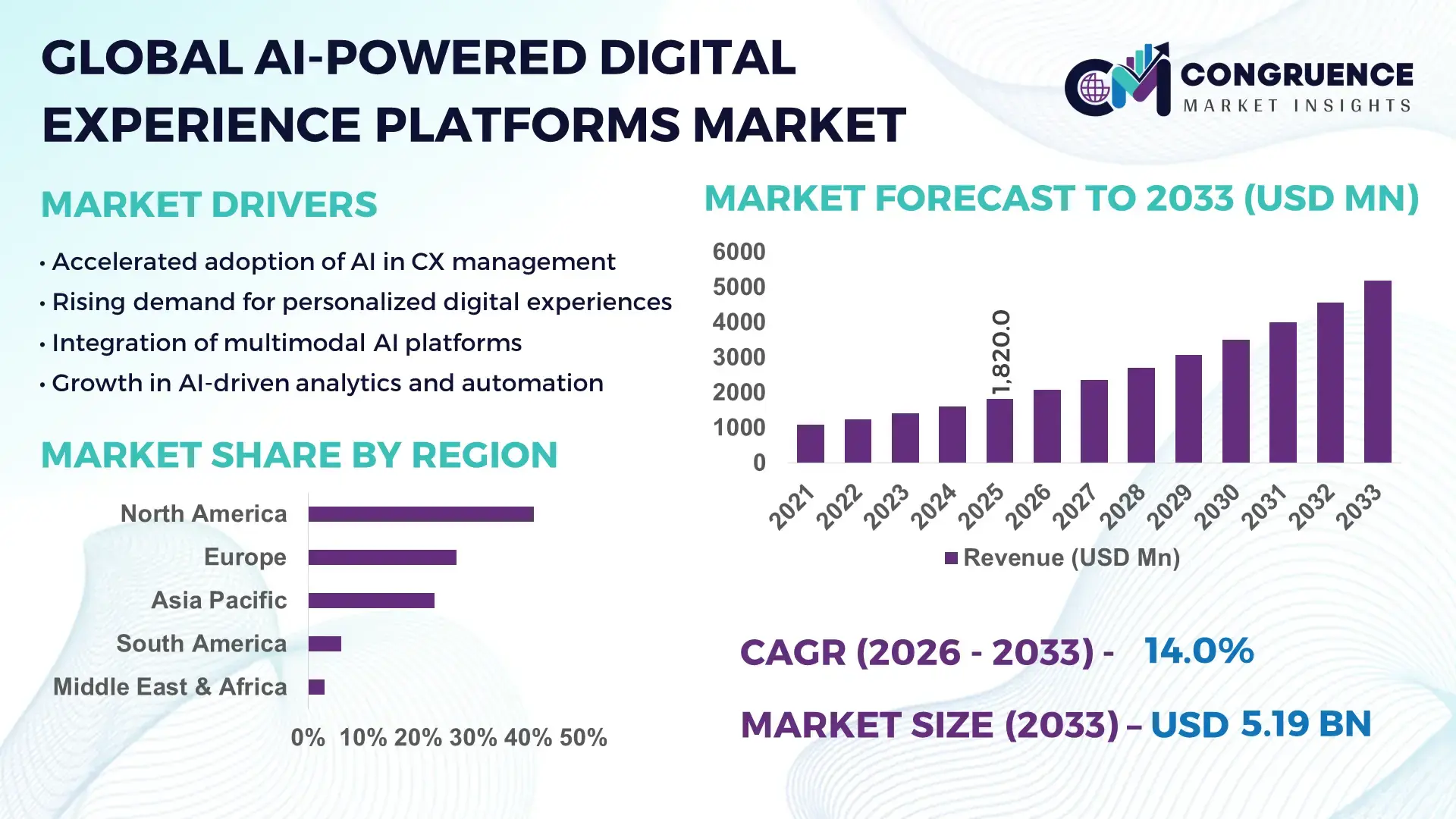

The Global AI-Powered Digital Experience Platforms Market was valued at USD 1,820.0 Million in 2025 and is anticipated to reach USD 5,191.7 Million by 2033, expanding at a CAGR of 14% between 2026 and 2033, according to an analysis by Congruence Market Insights. This acceleration is largely driven by enterprises embedding generative AI and real-time analytics into customer journeys to reduce churn and increase lifetime value.

The United States hosts over 5,300 enterprise-grade data centers, more than 40% of global hyperscale cloud capacity, and consistently attracts USD 35–45 billion annually in AI and cloud infrastructure investment. Large-scale deployment of AI-powered DX platforms spans retail, fintech, healthcare, and government services, with 60%+ of Fortune 500 firms running AI-enabled personalization engines in 2024–2025. More than 1,200 active AI patents per year are filed in experience analytics, recommendation systems, and automated content orchestration. The country also leads in enterprise SaaS adoption—72% of mid-to-large firms use composable or headless digital stacks—supported by high-speed 5G coverage in 95% of urban zones and widespread use of edge computing for low-latency experiences.

Market Size & Growth: USD 1,820.0 Mn in 2025 to USD 5,191.7 Mn by 2033 at 14% CAGR, propelled by AI-driven personalization at scale.

Top Growth Drivers: 68% faster campaign deployment; 32% lift in conversion rates; 27% reduction in support tickets.

Short-Term Forecast: By 2028, real-time AI orchestration will cut customer friction scores by 25% across omnichannel journeys.

Emerging Technologies: Generative AI content engines, composable/headless DXP architectures, and edge-AI analytics.

Regional Leaders (2033): North America ~USD 2.1 Bn (enterprise automation); Europe ~USD 1.6 Bn (privacy-first design); Asia-Pacific ~USD 1.3 Bn (super-app ecosystems).

End-User Trends: Retail, BFSI, and healthcare lead adoption; rising use of AI assistants and self-serve portals.

Pilot Example (2024): A global retailer used AI journey mapping to reduce checkout drop-off by 18%.

Competitive Landscape: Market leader ~22% share; key players include Adobe, Salesforce, SAP, Acquia, and Bloomreach.

Regulatory & ESG Impact: Strong alignment with GDPR/CPRA; privacy-by-design becoming default architecture.

Investment Patterns: ~USD 8–10 Bn invested recently in AI-DXP startups, data orchestration, and vertical platforms.

Future Outlook: Deeper AI-agent integration and industry-specific DX platforms will standardize hyper-personalization.

The market is shaped by strong contributions from retail (~28%), BFSI (~24%), and healthcare (~16%), while media, telecom, and public services make up the remainder. Recent innovations include autonomous content creation, AI experimentation sandboxes, and real-time consent management tools. Stricter data-privacy rules in Europe, rising digital commerce in Asia, and cloud-native modernization in North America are steering adoption. Enterprises are moving toward composable architectures and agentic AI workflows that promise greater interoperability and resilience over the next five years.

AI-powered Digital Experience Platforms (DXPs) are becoming core digital infrastructure rather than peripheral marketing tools. Strategically, they enable organizations to unify data, content, commerce, and customer engagement into a single intelligent layer that continuously learns from behavior in real time. This shift is critical as businesses move from campaign-led marketing to always-on experience orchestration. Modern AI-native DXPs reduce operational silos, automate experimentation, and allow rapid scaling across channels without proportional cost increases.

From a performance perspective, AI-driven personalization typically delivers 30–40% higher engagement compared to rules-based legacy CMS systems, demonstrating a clear benchmark advantage over older standards. Cloud-native, composable DXPs also shorten deployment cycles by 35–50%, allowing firms to launch new digital products in weeks instead of months.

Regionally, North America dominates in deployment volume, while Europe leads in adoption intensity, with roughly 65% of large enterprises embedding privacy-first AI workflows into their DX stacks. Asia-Pacific is rapidly scaling through super-app ecosystems that blend payments, commerce, and services into unified digital experiences.

In the short term, by 2028, agentic AI orchestration is expected to reduce customer service handling time by 28% and cut digital operating costs by 20% through automation. On the ESG front, firms are committing to measurable improvements such as a 25% reduction in cloud energy intensity per transaction by 2030, supported by optimized AI workloads and greener data centers.

A concrete micro-scenario illustrates this trajectory: in 2024, a multinational bank deployed AI journey orchestration across mobile and web, achieving a 22% reduction in customer drop-offs and a 15% increase in digital self-service usage.

Looking ahead, the AI-Powered Digital Experience Platforms Market is positioned as a pillar of resilient, compliant, and sustainable digital growth—integrating intelligence, trust, and efficiency into every customer interaction.

The AI-Powered Digital Experience Platforms market is being reshaped by converging forces of cloud migration, data interoperability, and generative AI. Enterprises are prioritizing unified customer data platforms, real-time analytics, and automated content workflows to compete in increasingly digital-first environments. Rising expectations for seamless omnichannel experiences, tighter data-privacy regulations, and rapid innovation cycles are compelling firms to modernize legacy systems. At the same time, vendor ecosystems are shifting toward composable architectures that allow modular upgrades rather than monolithic replacements. Integration with CRM, ERP, and commerce platforms is deepening, while edge computing is enabling faster decision-making. Talent shortages in AI and engineering, cybersecurity risks, and infrastructure costs are moderating adoption pace, but strategic investments and partnerships continue to expand the market footprint.

Large-scale digital transformation programs are pushing organizations to replace fragmented tech stacks with intelligent, integrated DX platforms. More than 70% of global enterprises are modernizing legacy CMS and CRM systems to support real-time personalization and analytics. AI-powered automation is reducing manual content operations by 30–45%, freeing teams to focus on strategy and creativity. Retailers are embedding predictive recommendations into storefronts, while banks use AI to personalize financial insights across mobile channels. The rise of cloud-native architecture allows rapid experimentation, with A/B testing cycles shrinking from weeks to days. Meanwhile, the expansion of 5G and edge computing has enabled millisecond-level response times for interactive experiences. Together, these trends are driving higher adoption of AI-powered DXPs across industries seeking efficiency, agility, and deeper customer engagement.

Stricter global privacy frameworks—such as GDPR in Europe and CPRA in California—are increasing compliance costs and slowing deployment timelines for AI-driven DX platforms. Nearly 58% of enterprises report delays in AI projects due to consent management, data localization, and governance requirements. Organizations must invest heavily in data anonymization, encryption, and auditability, which can raise implementation expenses by 15–25%. Cross-border data transfer restrictions complicate cloud-based architectures, particularly for multinational firms. In addition, cybersecurity risks associated with large data lakes and AI models are prompting more cautious rollouts. Shortages of skilled data governance professionals further constrain adoption, as many firms struggle to balance innovation with regulatory compliance and consumer trust.

Verticalized AI solutions represent a major growth opportunity for the market. Healthcare providers are adopting specialized DX platforms that integrate patient portals, AI triage tools, and personalized care pathways, with digital appointment usage rising above 65% in many regions. In retail, sector-specific recommendation engines are boosting basket sizes by 12–18% on average. Financial services firms are deploying tailored AI for risk-aware personalization, fraud detection, and advisory services. Meanwhile, government agencies are using secure DX platforms to improve citizen services and reduce processing times by up to 30%. As vendors build preconfigured industry modules, deployment cycles shorten and total cost of ownership declines, creating fertile ground for faster and broader adoption.

Many organizations operate with fragmented legacy systems, making integration with modern AI-powered DX platforms technically complex and expensive. Large enterprises often manage 10–20 disparate data sources, requiring significant middleware and migration efforts. Integration projects can take 9–18 months, delaying time-to-value. Additionally, a global shortage of AI engineers, data architects, and experience designers limits implementation capacity. Salaries for specialized talent have risen by 20–30%, increasing project costs. Cybersecurity concerns, vendor lock-in risks, and the need for continuous model monitoring further complicate adoption. Without clear governance frameworks and interoperable standards, scaling AI-powered DX initiatives remains a persistent challenge for many firms.

Modular, prefabricated digital stacks gaining traction: Enterprises are increasingly assembling DX platforms from pre-built modules rather than monolithic suites. Around 55% of new digital programs report lower project costs using modular, pre-configured components that mirror the efficiency logic of prefabrication. Off-site “pre-baked” experience templates, APIs, and microservices reduce deployment timelines by 20–35%, while automated testing cuts rework rates by 18%. Adoption is strongest in Europe and North America, where CIOs prioritize speed and operational consistency.

Generative AI content factories scaling personalization: Brands are deploying AI studios that automatically generate text, images, and offers in real time. Early adopters report 40% faster content production and 22% higher click-through rates versus manual workflows. By 2026, over 1,000 large brands are expected to run always-on generative engines tied to customer data. Guardrails for brand safety and copyright are becoming embedded features in leading platforms.

Edge analytics reducing latency for experiences: To support real-time interactions, companies are shifting workloads closer to users. Edge-enabled DX systems are cutting response times from ~200 ms to under 50 ms, improving video, AR/VR, and conversational interfaces. Approximately 35% of new deployments now include edge components, particularly in telecom and retail environments with high mobile traffic.

Automated privacy-by-design becoming default: Modern AI-powered DX platforms increasingly embed consent, minimization, and retention controls into core architecture. Firms adopting automated governance report 28% fewer compliance incidents and 15% lower audit costs. By 2027, roughly 70% of regulated enterprises are expected to rely on built-in privacy automation rather than manual controls, accelerating safer innovation.

The AI-Powered Digital Experience Platforms Market is structured around technology types, application domains, and end-user industries that shape adoption patterns and investment priorities. On the type axis, platforms are differentiated by the underlying multimodal AI architectures they employ—ranging from vision-language and audio-text systems to emerging video-language and generative reasoning engines—each serving distinct performance needs such as real-time personalization, content automation, and contextual decisioning. Application segmentation reflects how these capabilities are operationalized across customer engagement, commerce, analytics, content operations, and service automation, with usage intensity varying by data maturity and regulatory environment. End-user segmentation reveals uneven but accelerating uptake across retail, BFSI, healthcare, media, telecom, and public services, driven by industry-specific digital modernization, data availability, and tolerance for AI experimentation. Overall, segmentation demonstrates a shift from generic platforms to domain-tailored, modular solutions that align technology depth with business outcomes and compliance requirements.

Vision-language models currently represent the leading type with ~42% share, reflecting their central role in product discovery, visual merchandising, and multimodal search within commerce and media workflows. Enterprises favor these systems because they reliably connect images, text, and customer intent at scale, reducing manual tagging by 30–45% and improving recommendation relevance.

The fastest-growing type is video-language models (≈18% CAGR), driven by exploding video volumes, creator-led marketing, and demand for automated scene indexing, highlights generation, and real-time accessibility features. Adoption is expected to exceed 30% of total platform usage by 2033, as brands shift budgets from static content to short-form and interactive video experiences.

Audio-text systems account for about 25% share, supporting conversational AI, call analytics, and voice commerce with rising use in contact centers and smart devices. Emerging categories—such as reasoning agents, retrieval-augmented generation (RAG) engines, and synthetic data simulators—together represent roughly 33% combined share, serving niche but strategically important roles in experimentation, compliance testing, and autonomous workflow orchestration.

Customer experience orchestration is the leading application (~38% share) as enterprises prioritize unified journey management across web, mobile, and in-store touchpoints. Real-time personalization, predictive offers, and cross-channel attribution have made this use case mission-critical for retention and lifetime value.

The fastest-growing application is AI-driven content operations (≈17% CAGR), fueled by generative tools that automate copy, imagery, and localization while maintaining brand guardrails. Marketing teams are moving from campaign factories to continuous content flows integrated directly into DX platforms.

Commerce enablement (~22% share) spans product discovery, pricing intelligence, and checkout optimization; analytics and experimentation (~18% share) support rapid A/B testing and behavioral insights; service automation and virtual agents (~22% combined share) are expanding in support centers and self-serve portals. In 2025, over 38% of enterprises globally reported piloting AI-powered systems within their customer experience platforms. More than 60% of Gen Z consumers indicate greater trust in brands that use AI-powered multimodal chatbots for support and discovery.

Retail & e-commerce lead end-user adoption with ~34% share, reflecting heavy reliance on visual search, recommendation engines, and personalized storefronts that lift conversion rates and reduce returns. High data richness and rapid experimentation cycles make retail the most advanced deployer of AI-powered DX platforms.

The fastest-growing end-user segment is healthcare (≈16% CAGR), driven by digital front doors, patient engagement portals, and AI-assisted triage that integrate clinical and experience data while complying with strict privacy rules.

BFSI (~22% share) leverages AI-DX for risk-aware personalization, onboarding automation, and fraud prevention. Media & entertainment (~12% share) uses video-language systems for content tagging and discovery, while telecom and public services together contribute about 32% combined share, focusing on service modernization and citizen engagement. In 2025, 42% of U.S. hospitals were testing AI models that combine imaging with structured patient records. Roughly 36% of large enterprises reported running pilot AI-DX programs in at least two business units.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2026 and 2033.

North America’s leadership is supported by high enterprise AI adoption, with over 70% of large organizations deploying AI-driven experience platforms. Europe held approximately 27% share, driven by compliance-led digital transformation. Asia-Pacific accounted for nearly 23%, supported by rapid mobile-first adoption and large digital consumer bases exceeding 2.5 billion users. South America and the Middle East & Africa together contributed around 9%, reflecting early-stage but accelerating adoption.

North America represents about 41% market share, driven by strong demand from BFSI, healthcare, retail, and media sectors. Over 65% of enterprises use AI-enabled personalization engines across digital channels. Regulatory clarity around data governance and cloud adoption has supported enterprise-scale deployments. The region leads in composable DX architecture adoption, with 60%+ organizations shifting away from monolithic CMS. A major local player has expanded generative AI modules for real-time journey orchestration across finance and retail. Consumer behavior reflects higher adoption in healthcare portals and digital banking experiences.

Europe holds nearly 27% of the market, led by Germany, the UK, and France. Strict data protection and AI governance frameworks have driven demand for explainable and auditable AI-DX platforms. Over 55% of enterprises prioritize privacy-by-design features in digital experience tools. Adoption of headless and modular platforms is growing, especially in manufacturing and public services. A regional vendor has focused on consent-aware personalization engines for cross-border operations. European consumers show higher trust in transparent AI-powered interactions.

Asia-Pacific ranks third by share at 23% but leads in volume expansion, with China, India, and Japan as top adopters. The region supports over 60% of global mobile internet users, accelerating AI-powered commerce and service platforms. Cloud infrastructure expansion and AI innovation hubs in India and Southeast Asia are strengthening deployment capacity. Local platforms integrate payments, content, and commerce into unified experiences. Consumer behavior is strongly driven by e-commerce, super-apps, and mobile AI assistants.

South America contributes roughly 6% market share, led by Brazil and Argentina. Growth is supported by rising digital media consumption and multilingual experience requirements. Governments are investing in digital infrastructure, with over 70% urban internet penetration in major economies. A regional technology firm has expanded AI-driven content localization tools for streaming and retail. Consumers show strong engagement with AI-powered media and mobile-first service platforms.

Middle East & Africa accounts for about 3% share, with UAE and South Africa leading adoption. Government-led smart city and e-government programs are driving AI-DX demand. Over 50% of large enterprises in the Gulf are upgrading digital experience stacks. Investments in cloud zones and data centers are improving deployment readiness. Consumer behavior reflects growing use of AI-driven government, telecom, and banking platforms.

United States – 29% Market Share: Strong enterprise AI adoption, advanced cloud infrastructure, and large-scale digital transformation programs.

China – 14% Market Share: High digital consumer density, integrated super-app ecosystems, and rapid AI commercialization across commerce and services.

The competitive environment in the AI-Powered Digital Experience Platforms Market is dynamic and moderately consolidated with 20+ active competitors globally. The top 5 companies collectively represent an estimated ~58–63% of installed enterprise deployments, reflecting strong positioning among leaders while mid-tier and emerging players continue to innovate. A range of strategic initiatives—such as deep AI integration, partner ecosystems, and modular architecture rollouts—is shaping vendor differentiation. In 2025, several major platform providers introduced significant AI enhancements, including agent-based automation, real-time personalization, and integrated journey orchestration that handle structured and unstructured data. Competitive actions include expanded partnerships with cloud hyperscalers and AI model developers, as well as ecosystem alliances that enable seamless embedding of generative AI services across CRM, analytics, and commerce stacks. Innovation trends reveal heavy investment in composable DXP frameworks, AI copilots, and brand-aware automation, enabling faster time-to-value for enterprise customers. The market features a mix of traditional enterprise software vendors, cloud-native challengers, and specialist AI platform developers, creating an environment where strategic alliances and differentiated technology stacks are crucial to leadership positioning.

SAP Customer Experience AI Suite

Oracle Digital Experience Platform

Microsoft Copilot & Azure AI

IBM Watson Experience Platform

Uniphore Business AI Cloud

Anthropic Claude Platform

AWS Bedrock & Partner AI Tools

Klaviyo B2C AI CRM

Mitel CX

Avaya Experience Platform (AXP)

Zendesk AI / AI-enhanced CX

The AI-Powered Digital Experience Platforms Market is characterized by technologies that enable real-time, context-aware digital engagement at scale. Core advancements include generative AI integration, which automates content creation, personalization, and campaign orchestration across channels. Agent-based frameworks and AI copilots are emerging as differentiators, offering autonomous workflows that help users define intent, automate decision logic, and execute complex, multi-step processes without manual intervention. Composable and headless architectures are standard, allowing enterprises to replace rigid monoliths with modular services that plug into existing data infrastructures and support rapid experimentation. Interaction-centric innovations include multimodal AI, which blends text, visual, and audio signals for richer customer insights and improved classification accuracy. Edge intelligence and distributed inference pipelines are gaining traction, especially where ultra-low latency or privacy-preserving processing is required. Data orchestration layers unify disparate repositories—first- and third-party—enabling predictive analytics and customer journey optimization. AI governance and explainability tools embed audit trails to support compliance and trust. Furthermore, partnerships between infrastructure providers and AI model developers are optimizing platforms for enterprise workloads, enabling secure model deployment, monitoring, and lifecycle management across cloud environments. Collectively, these technologies are transforming static digital experience platforms into intelligent systems capable of automating personalization, analytics, and operational workflows for decision-makers across sectors.

• In February 2025, Sitecore announced a major intelligent digital experience release featuring over 250 AI-driven enhancements—including brand-aware AI and agentic workflows—to help marketers rapidly create and scale personalized content across channels. Source: www.sitecore.com

• In October 2025, Salesforce deepened collaborations with AI leaders to embed advanced GPT-5 and Claude models into its Agentforce 360 platform, enabling natural language analytics, visualizations, and commerce features integrated with Slack and enterprise data. Source: www.reuters.com

• In mid-2025, Kapture CX announced profitability and 100% year-over-year growth, with net revenue retention above 140%, driven by expanded enterprise adoption in banking, fintech, and online retail. Source: www.economictimes.indiatimes.com

• In December 2025, Tata Communications acquired a 51% stake in Commotion Inc., boosting AI capabilities in personalized customer engagement and omnichannel automation across enterprise platforms. Source: www.timesofindia.indiatimes.com

The AI-Powered Digital Experience Platforms Market Report encompasses comprehensive analysis across technology types, enterprise applications, geographic regions, and end-user industries. Coverage includes platform components such as customer journey orchestration, personalization engines, analytics dashboards, AI agents, and content automation modules. It evaluates deployment models—including cloud, hybrid, and edge architectures—alongside organizational segmentation spanning SMBs to large enterprises. The report also addresses horizontal use cases (customer engagement, commerce enablement, analytics, and service automation) and vertical insights across retail, BFSI, healthcare, telecom, media, and public services. Geographic focus spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, examining regional technology adoption, regulatory influences, digital maturity, and infrastructure readiness. Technology dimensions include multimodal AI, composable headless stacks, AI governance tooling, and data orchestration layers, providing decision-makers with actionable insights on adoption patterns and integration strategies. The analysis further explores market dynamics such as competitive positioning, partnerships, and innovation trends, alongside practical considerations like platform interoperability, integration complexity, and evolving digital standards. Overall, the report delivers a detailed, business-oriented view of how AI-driven digital experience platforms are shaping enterprise digital transformation across ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,820.0 Million |

| Market Revenue (2033) | USD 5,191.7 Million |

| CAGR (2026–2033) | 14.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Adobe Experience Cloud, Salesforce Agentforce 360, Sitecore Intelligent Digital Experience Platform, SAP Customer Experience AI Suite, Oracle Digital Experience Platform, Microsoft Copilot & Azure AI, IBM Watson Experience Platform, Uniphore Business AI Cloud, Anthropic Claude Platform, AWS Bedrock & Partner AI Tools, Klaviyo B2C AI CRM, Mitel CX, Avaya Experience Platform (AXP), Zendesk AI / AI-enhanced CX |

| Customization & Pricing | Available on Request (10% Customization Free) |