Reports

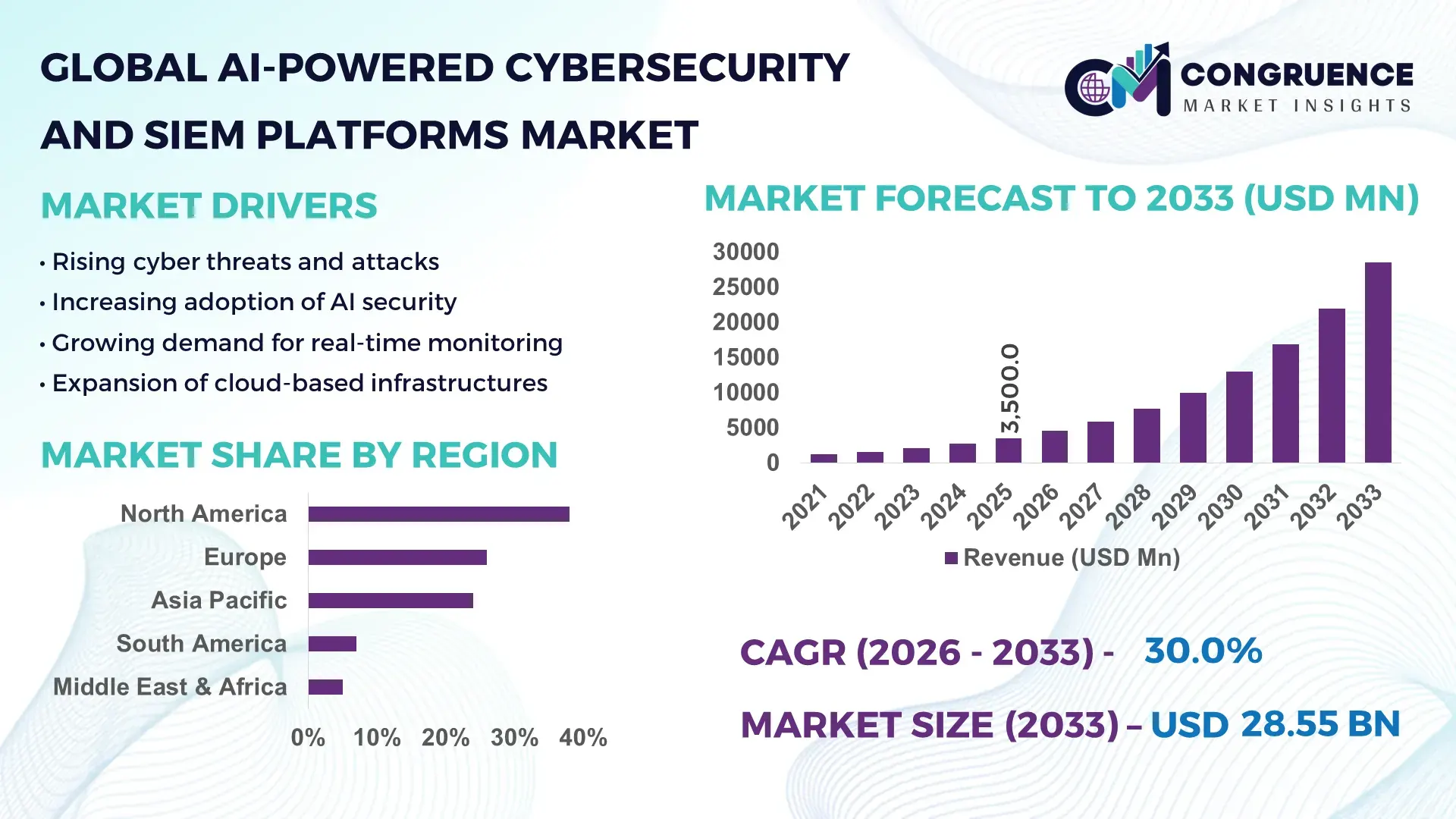

The Global AI-Powered Cybersecurity and SIEM Platforms Market was valued at USD 3,500.0 Million in 2025 and is anticipated to reach a value of USD 28,550.6 Million by 2033 expanding at a CAGR of 30% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the increasing frequency of cyberattacks and rapid enterprise adoption of AI-driven threat detection systems.

The United States leads the AI-Powered Cybersecurity and SIEM Platforms Market with over 42% enterprise adoption across large-scale organizations and more than 65% deployment in financial and healthcare sectors. The country hosts over 3,500 cybersecurity firms and accounts for nearly 48% of global cybersecurity investments. AI-enabled SIEM platforms are implemented in over 70% of Fortune 500 companies, supporting real-time threat intelligence processing exceeding 5 petabytes daily. Federal cybersecurity budgets surpassed USD 18 billion in 2025, with significant allocation toward AI-based threat analytics, while over 60% of enterprises report automated incident response integration, demonstrating strong technological maturity and operational scale.

Market Size & Growth: USD 3,500.0 Million in 2025, projected to reach USD 28,550.6 Million by 2033, expanding at 30% CAGR due to rising AI-driven threat detection adoption.

Top Growth Drivers: 68% increase in AI adoption for threat detection, 55% improvement in incident response efficiency, 47% rise in cloud-based SIEM deployment.

Short-Term Forecast: By 2028, AI-powered platforms are expected to reduce cybersecurity operational costs by 32% and improve detection accuracy by 40%.

Emerging Technologies: Adoption of XDR platforms, behavioral analytics AI, and automated SOC orchestration tools is accelerating.

Regional Leaders: North America (USD 12,500 Million by 2033) leads with enterprise-scale deployments; Europe (USD 7,800 Million) shows strong compliance-driven adoption; Asia-Pacific (USD 6,900 Million) driven by rapid digitalization.

Consumer/End-User Trends: Over 62% of enterprises prioritize AI-based SIEM for real-time analytics, especially in BFSI and healthcare sectors.

Pilot or Case Example: In 2025, a global bank deployed AI-SIEM reducing incident response time by 45% and false positives by 38%.

Competitive Landscape: Market leader holds ~18% share, followed by IBM, Splunk, Palo Alto Networks, and Microsoft.

Regulatory & ESG Impact: Over 58% of firms comply with AI-driven cybersecurity mandates aligned with GDPR and zero-trust frameworks.

Investment & Funding Patterns: Over USD 9.5 Billion invested in AI cybersecurity startups globally, with rising venture capital inflows.

Innovation & Future Outlook: Integration of generative AI and predictive threat intelligence is expected to redefine automated cybersecurity ecosystems.

AI-powered cybersecurity and SIEM platforms are increasingly utilized across BFSI (32%), healthcare (18%), and IT sectors (25%), driven by data protection regulations and cyber risk mitigation. Innovations such as generative AI threat modeling and cloud-native SIEM solutions are reshaping operations. North America and Asia-Pacific lead consumption, while automation and zero-trust security frameworks are emerging as key future trends enhancing enterprise resilience.

The AI-Powered Cybersecurity and SIEM Platforms Market holds strategic relevance as enterprises transition toward automated, intelligence-driven security infrastructures. Organizations are increasingly prioritizing AI integration to enhance threat detection accuracy and reduce response times, with studies indicating up to 45% faster incident resolution compared to traditional SIEM systems. Machine learning-based anomaly detection delivers 35% improvement compared to rule-based systems, enabling real-time identification of complex cyber threats across distributed environments.

From a regional perspective, North America dominates in volume, while Asia-Pacific leads in adoption with over 58% of enterprises integrating AI-based cybersecurity solutions into digital transformation strategies. By 2028, autonomous SOC platforms are expected to reduce manual intervention in security operations by nearly 40%, improving operational efficiency and reducing labor dependency.

Compliance and ESG factors are becoming central to cybersecurity investments. Firms are committing to reducing cyber risk exposure by 50% and achieving 30% improvement in data governance frameworks by 2030, aligning with global regulatory standards. AI-driven compliance monitoring tools are being widely deployed to meet stringent regulatory requirements, particularly in financial services and healthcare sectors.

In 2025, a leading technology firm in the United States achieved a 42% reduction in breach response time through AI-enabled SIEM integration combined with predictive analytics. Such initiatives highlight the growing importance of intelligent automation in cybersecurity.

Looking ahead, the AI-Powered Cybersecurity and SIEM Platforms Market is positioned as a critical pillar for organizational resilience, regulatory compliance, and sustainable digital transformation, enabling enterprises to proactively mitigate risks and safeguard digital assets in an increasingly complex threat landscape.

The AI-Powered Cybersecurity and SIEM Platforms Market is evolving rapidly, driven by increasing cyber threat complexity, regulatory requirements, and digital transformation initiatives across industries. Organizations are shifting from traditional security systems toward AI-enabled platforms capable of processing large-scale data streams exceeding terabytes per day. Approximately 67% of enterprises now prioritize real-time threat intelligence integration, while over 52% have adopted automated incident response systems.

Cloud adoption is significantly influencing market dynamics, with more than 60% of organizations deploying cloud-native SIEM solutions to enhance scalability and operational flexibility. Additionally, integration of advanced analytics, behavioral monitoring, and predictive threat detection has improved detection rates by nearly 40% compared to legacy systems. However, concerns related to data privacy, integration complexity, and skill shortages continue to impact adoption rates.

The market is also shaped by increasing investments in cybersecurity infrastructure, with enterprises allocating up to 12% of their IT budgets toward advanced security solutions. Emerging technologies such as XDR and zero-trust architectures are further redefining market dynamics, enabling organizations to build resilient and adaptive cybersecurity frameworks.

The increasing frequency and sophistication of cyberattacks are a primary driver of the AI-Powered Cybersecurity and SIEM Platforms Market. Over 72% of organizations reported experiencing at least one major cyber incident in 2025, with ransomware attacks rising by 38% year-over-year. AI-powered platforms enable real-time detection of anomalies across millions of data points, improving threat identification accuracy by over 40%. Enterprises are leveraging AI-driven SIEM solutions to analyze network traffic, user behavior, and endpoint activities simultaneously, processing over 10 million events per second in large-scale environments. Financial institutions and healthcare providers, which account for over 50% of cyberattack targets, are increasingly deploying AI-based solutions to enhance data protection and regulatory compliance. Additionally, automation capabilities reduce incident response times by up to 45%, enabling faster mitigation of potential threats and minimizing operational disruptions.

Despite strong growth potential, integration challenges and workforce limitations act as key restraints in the AI-Powered Cybersecurity and SIEM Platforms Market. Nearly 48% of enterprises report difficulties integrating AI-driven SIEM solutions with legacy IT infrastructure, leading to operational inefficiencies. Compatibility issues with existing security tools and data silos further complicate implementation processes. Additionally, the shortage of skilled cybersecurity professionals remains a critical concern, with over 3.4 million unfilled cybersecurity roles globally. Organizations face challenges in managing AI-based systems due to the need for specialized expertise in machine learning and data analytics. Training costs have increased by approximately 25%, further limiting adoption among small and medium enterprises. These factors collectively hinder seamless deployment and scalability of advanced cybersecurity solutions.

The rapid adoption of cloud computing and zero-trust architectures presents significant opportunities for the AI-Powered Cybersecurity and SIEM Platforms Market. Over 65% of enterprises have migrated critical workloads to cloud environments, creating demand for advanced security solutions capable of protecting distributed infrastructures. AI-powered SIEM platforms enable continuous monitoring and risk assessment across multi-cloud ecosystems, improving visibility by over 50%. Zero-trust frameworks, adopted by nearly 58% of large enterprises, require continuous authentication and real-time threat analysis, driving demand for AI-based analytics. Furthermore, integration of AI with cloud-native security tools allows organizations to automate threat detection and response, reducing false positives by 35%. These advancements open new avenues for solution providers to develop scalable, intelligent security platforms tailored to evolving enterprise needs.

Data privacy regulations and compliance requirements pose significant challenges for the AI-Powered Cybersecurity and SIEM Platforms Market. Over 62% of organizations cite regulatory complexity as a barrier to implementing AI-driven security solutions, particularly in regions with strict data protection laws. Managing sensitive data across multiple jurisdictions requires robust encryption and governance frameworks, increasing operational complexity. Additionally, AI models require large datasets for training, raising concerns about data misuse and privacy breaches. Approximately 45% of enterprises express concerns regarding transparency and explainability of AI algorithms, limiting trust in automated systems. Compliance with evolving regulations such as GDPR and industry-specific standards demands continuous updates and monitoring, increasing costs and resource allocation for organizations adopting AI-powered cybersecurity solutions.

Rise in Autonomous SOC Platforms: Over 48% of enterprises are transitioning toward autonomous Security Operations Centers powered by AI, reducing manual intervention by 35%. These systems process over 2 million alerts daily, improving incident prioritization accuracy by 42% and enabling faster threat containment across enterprise networks.

Expansion of Cloud-Native SIEM Solutions: More than 62% of organizations are adopting cloud-native SIEM platforms, with data ingestion capabilities exceeding 10 terabytes per day. This shift enhances scalability by 50% and reduces infrastructure costs by approximately 28%, particularly in large enterprises managing distributed workloads.

Growth in Behavioral Analytics Integration: Behavioral analytics adoption has increased by 55%, enabling detection of insider threats and anomalies with 38% higher precision. These systems analyze over 500 user activity parameters, improving early threat detection rates and reducing false positives significantly.

Increasing Adoption of Zero-Trust Security Models: Nearly 58% of enterprises have implemented zero-trust frameworks, with AI-based continuous authentication improving access control efficiency by 40%. This approach reduces unauthorized access incidents by 33%, particularly in sectors handling sensitive financial and healthcare data.

The AI-Powered Cybersecurity and SIEM Platforms Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across industries. Solution-based platforms dominate due to their comprehensive threat detection and analytics capabilities, while services are gaining traction as organizations seek managed security expertise. Applications are widely distributed across threat detection, compliance management, and incident response, with threat detection accounting for a significant portion of deployments. End-user segmentation highlights strong adoption in BFSI, healthcare, and IT sectors, where data protection and regulatory compliance are critical. Increasing cloud adoption and digital transformation initiatives are further influencing segmentation dynamics, driving demand for scalable and AI-integrated cybersecurity solutions across global markets.

The market is segmented into Solutions and Services. Solutions dominate the segment, accounting for approximately 64% of adoption due to their ability to provide integrated threat intelligence, real-time monitoring, and automated incident response capabilities. Organizations prefer unified platforms that consolidate security operations, reducing complexity and improving operational efficiency. Services, including managed security and professional services, represent a growing segment, contributing nearly 36% of the market. These services are gaining traction as enterprises seek external expertise to manage complex AI-driven cybersecurity infrastructures. Managed services, in particular, are witnessing rapid adoption with an estimated growth rate exceeding 28%, driven by increasing outsourcing of security operations. Cloud-based solutions and hybrid deployment models are also emerging as critical subcategories, enabling scalability and flexibility.

• A 2025 industry report highlighted that over 70% of large enterprises adopted integrated AI-driven SIEM solutions to enhance real-time threat detection capabilities.

Threat Detection & Monitoring leads the application segment with approximately 46% share, driven by the need for real-time identification of cyber threats across enterprise networks. Compliance Management and Incident Response follow, collectively accounting for nearly 38% of applications, reflecting increasing regulatory requirements and demand for rapid threat mitigation. Incident response is the fastest-growing application, supported by automation trends and increasing cyberattack frequency, with adoption rates expected to exceed 30% in the coming years. Other applications, including risk assessment and log management, contribute around 16% of the market. In 2025, over 41% of enterprises globally reported implementing AI-powered cybersecurity solutions specifically for real-time monitoring and analytics, while 58% of organizations prioritized compliance-focused deployments.

• A 2025 global cybersecurity assessment indicated that AI-based threat detection systems were deployed across more than 2,000 large enterprises, significantly improving breach detection rates.

The BFSI sector dominates the end-user segment with approximately 32% share, driven by high exposure to cyber threats and stringent regulatory requirements. Healthcare follows with around 18%, leveraging AI-powered SIEM platforms to protect sensitive patient data and ensure compliance with data protection regulations. IT & Telecom is the fastest-growing end-user segment, with adoption rates increasing rapidly due to expanding digital infrastructure and cloud adoption, expected to grow above 29%. Other sectors, including retail, government, and manufacturing, collectively account for nearly 50% of the market, reflecting widespread adoption across industries. In 2025, more than 44% of enterprises globally reported deploying AI-powered cybersecurity platforms to enhance operational security, while 60% of large organizations integrated automated threat response systems.

• A 2025 industry analysis revealed that over 500 financial institutions implemented AI-driven SIEM platforms to strengthen fraud detection and risk management capabilities.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 32% between 2026 and 2033.

The global market shows strong regional variation, with Europe accounting for approximately 26% share driven by regulatory compliance, while Asia-Pacific contributes around 24% due to rapid digital transformation. South America holds nearly 7% share, supported by increasing enterprise cybersecurity investments, and the Middle East & Africa accounts for about 5% with growing adoption in oil & gas and government sectors. Over 65% of global enterprises in North America and Europe have implemented AI-based cybersecurity solutions, compared to 48% in Asia-Pacific, indicating strong growth potential in emerging economies.

North America holds approximately 38% market share, driven by strong demand across BFSI, healthcare, and government sectors. Over 70% of large enterprises have deployed AI-powered SIEM platforms, reflecting high digital maturity. Regulatory frameworks such as zero-trust mandates and data protection laws are accelerating adoption. Technological advancements include integration of predictive analytics and automated SOC systems, improving threat detection efficiency by over 40%. A leading player, IBM, has implemented AI-driven security solutions across multiple industries, processing billions of security events daily. Consumer behavior indicates higher enterprise adoption in healthcare and finance, where data protection is critical.

Europe accounts for approximately 26% market share, with key markets including Germany, the UK, and France. Strict regulatory frameworks such as GDPR drive demand for AI-powered cybersecurity solutions. Over 60% of enterprises have adopted advanced SIEM platforms to ensure compliance and data protection. Emerging technologies such as explainable AI and privacy-preserving analytics are gaining traction. A regional player, SAP, is enhancing cybersecurity solutions through AI integration. Consumer behavior shows strong demand for transparent and compliant AI systems, particularly in financial services and healthcare sectors.

Asia-Pacific contributes around 24% of the global market, with China, India, and Japan leading adoption. Over 55% of enterprises in the region are investing in AI-driven cybersecurity platforms to support rapid digitalization. Infrastructure growth and cloud adoption are key drivers, with data volumes increasing by over 45% annually. Technology hubs in India and China are fostering innovation in AI-based security solutions. A local player, Tata Consultancy Services, is expanding AI cybersecurity offerings. Consumer behavior highlights growth driven by e-commerce and mobile-based applications.

South America holds approximately 7% market share, with Brazil and Argentina leading adoption. Increasing investments in digital infrastructure and cloud technologies are driving demand for AI-powered SIEM platforms. Government initiatives promoting cybersecurity awareness and data protection are supporting market growth. Over 40% of enterprises are adopting AI-based security solutions to mitigate cyber risks. Regional players are focusing on managed security services to address skill gaps. Consumer behavior indicates rising demand for localized cybersecurity solutions, particularly in media and financial sectors.

The Middle East & Africa region accounts for approximately 5% market share, with UAE and South Africa leading adoption. Demand is driven by sectors such as oil & gas, construction, and government. Over 35% of enterprises are investing in AI-powered cybersecurity platforms to enhance infrastructure security. Technological modernization initiatives, including smart city projects, are accelerating adoption. Local players are focusing on cloud-based security solutions to address scalability needs. Consumer behavior shows increasing adoption driven by digital transformation and regulatory compliance requirements.

United States – 38% Market share: driven by high enterprise adoption and strong cybersecurity infrastructure

China – 18% Market share: supported by rapid digital transformation and large-scale data ecosystem

The AI-Powered Cybersecurity and SIEM Platforms Market is moderately consolidated, with the top five companies accounting for approximately 52% of the global market share. The competitive landscape includes over 150 active players ranging from global technology firms to specialized cybersecurity vendors. Key companies are focusing on product innovation, strategic partnerships, and mergers to strengthen their market position.

Major players are investing heavily in AI and machine learning capabilities, with over 65% of leading firms integrating advanced analytics into their cybersecurity platforms. Strategic collaborations between cloud service providers and cybersecurity firms are increasing, enabling seamless integration of AI-powered SIEM solutions into enterprise ecosystems. Product launches focusing on autonomous SOC platforms and XDR solutions are reshaping competition.

Additionally, companies are expanding geographically, particularly in Asia-Pacific and the Middle East, where adoption rates are rising. Innovation in generative AI and predictive threat intelligence is becoming a key differentiator, with over 40% of vendors incorporating these technologies into their offerings. The market also sees increasing investment in startup ecosystems, intensifying competition and accelerating technological advancements.

Microsoft

Splunk

Palo Alto Networks

Cisco Systems

Fortinet

Check Point Software Technologies

CrowdStrike

FireEye

McAfee

Rapid7

LogRhythm

Sumo Logic

AT&T Cybersecurity

AI and machine learning technologies are at the core of advancements in the AI-Powered Cybersecurity and SIEM Platforms Market. Over 68% of modern SIEM platforms now incorporate machine learning algorithms to analyze large-scale datasets, enabling detection of anomalies across billions of network events. Natural language processing is increasingly used to interpret threat intelligence reports, improving response accuracy by approximately 35%.

Extended Detection and Response (XDR) platforms are gaining traction, integrating endpoint, network, and cloud security into unified systems. Over 52% of enterprises have adopted XDR solutions to enhance visibility across digital infrastructures. Behavioral analytics is another key innovation, analyzing over 500 user attributes to detect insider threats and unusual patterns.

Cloud-native architectures are transforming SIEM platforms, with over 60% of deployments leveraging scalable cloud infrastructure. Automation technologies, including robotic process automation, are reducing manual workloads by nearly 40%. Generative AI is emerging as a transformative technology, enabling predictive threat modeling and automated response strategies.

Blockchain is also being explored for secure data sharing and tamper-proof logging, enhancing trust and transparency in cybersecurity operations. These technologies collectively enable organizations to build resilient, adaptive, and intelligent security ecosystems.

• In September 2024, Palo Alto Networks completed the acquisition of IBM’s QRadar SaaS assets, integrating them into its Cortex XSIAM platform. This enables unified AI-driven security operations combining SIEM, SOAR, and XDR, while offering no-cost migration services for enterprise customers transitioning from QRadar. Source: www.paloaltonetworks.com

• In May 2024, IBM and Palo Alto Networks announced a strategic partnership to deliver AI-powered cybersecurity solutions, including integration of IBM watsonx AI with Cortex XSIAM. The collaboration supports over 3,000 pre-built threat detectors and aims to accelerate enterprise adoption of AI-driven SOC platforms.

• In March 2024, Cisco completed its $28 billion acquisition of Splunk, strengthening its AI-driven security analytics and SIEM capabilities. The integration enables enhanced data-scale threat detection and deeper connectivity with Cisco’s XDR platform, improving enterprise-level security automation and analytics performance.

• In May 2024, CrowdStrike announced the general availability of its Falcon Next-Gen SIEM platform, incorporating generative AI capabilities and expanded third-party integrations. The platform enhances real-time threat detection and automates security workflows, supporting large-scale enterprise deployments across cloud and hybrid environments.

The AI-Powered Cybersecurity and SIEM Platforms Market Report provides a comprehensive analysis of market segments, technologies, applications, and regional dynamics shaping the industry. The report covers key segments including solutions and services, with detailed insights into deployment models such as cloud-based and on-premise systems. It also evaluates applications such as threat detection, compliance management, and incident response, highlighting their adoption across industries.

Geographically, the report analyzes major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering over 20 key countries. It examines industry-specific adoption across BFSI, healthcare, IT & telecom, retail, and government sectors, providing insights into usage patterns and technological integration.

The report further explores emerging technologies such as machine learning, XDR, behavioral analytics, and generative AI, which are transforming cybersecurity operations. It includes analysis of enterprise adoption trends, with over 60% of large organizations implementing AI-driven security solutions. Additionally, the report highlights regulatory frameworks, compliance requirements, and ESG considerations influencing market growth.

Overall, the scope encompasses a detailed evaluation of market structure, competitive landscape, innovation trends, and strategic developments, offering actionable insights for decision-makers and stakeholders aiming to capitalize on opportunities in the evolving cybersecurity ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,500.0 Million |

| Market Revenue (2033) | USD 28,550.6 Million |

| CAGR (2026–2033) | 30% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM; Microsoft; Splunk; Palo Alto Networks; Cisco Systems; Fortinet; Check Point Software Technologies; CrowdStrike; FireEye; McAfee; Rapid7; LogRhythm; Sumo Logic; AT&T Cybersecurity |

| Customization & Pricing | Available on Request (10% Customization Free) |