Reports

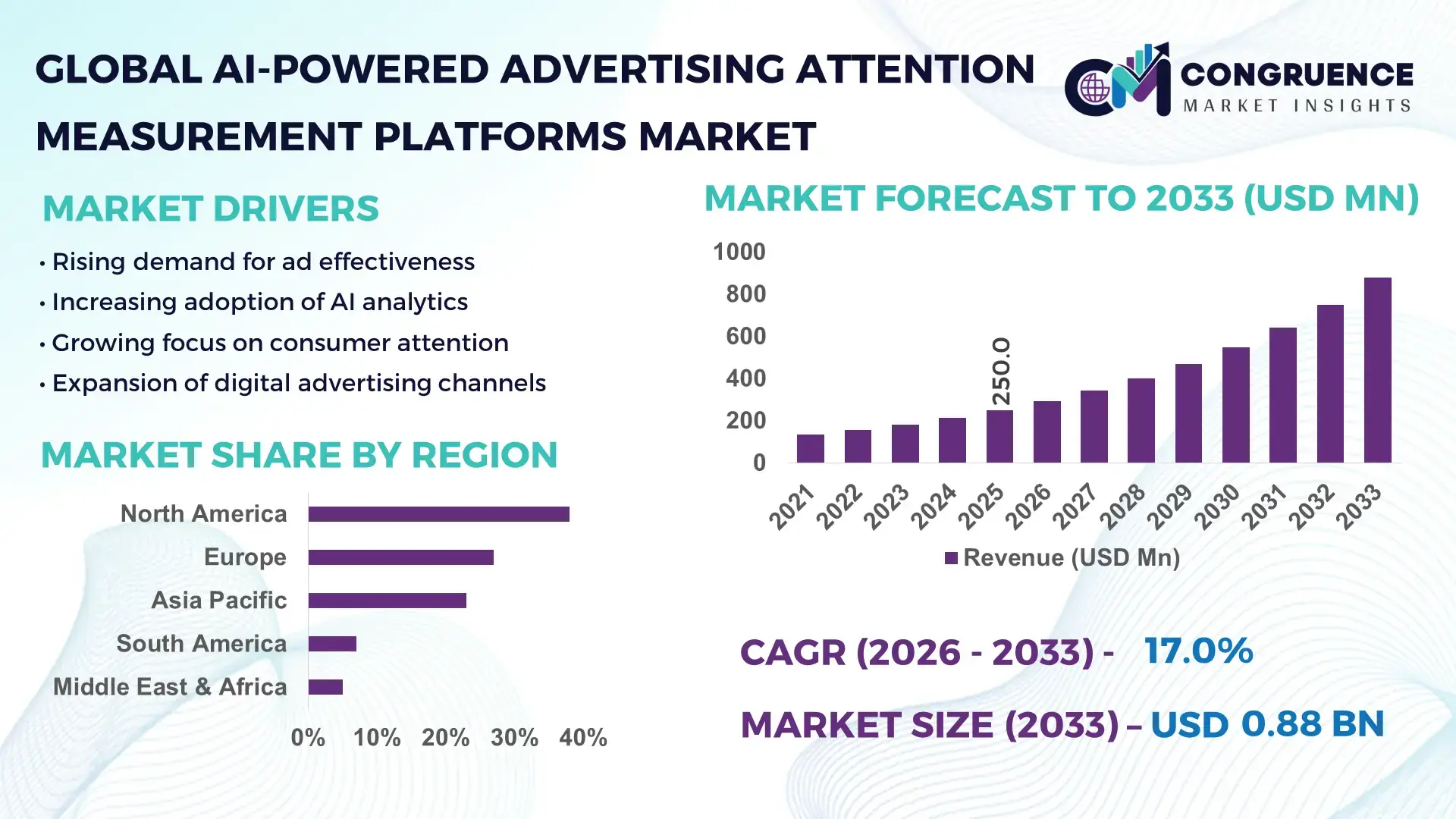

The Global AI-Powered Advertising Attention Measurement Platforms Market was valued at USD 250.0 Million in 2025 and is anticipated to reach a value of USD 877.9 Million by 2033 expanding at a CAGR of 17% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by the rapid shift from impression-based metrics to attention-based performance analytics in digital advertising ecosystems.

The United States demonstrates strong industrial maturity in this market, with over 65% of Fortune 500 advertisers integrating AI-based attention analytics into campaign workflows. More than 70% of large-scale digital campaigns utilize real-time eye-tracking or gaze prediction models to optimize engagement. Investments in ad-tech AI exceeded USD 12 billion in 2025, with over 120 active startups focusing on attention scoring algorithms. The country also leads in enterprise-level adoption, where over 58% of marketing teams deploy attention metrics across omnichannel platforms including connected TV, social media, and programmatic advertising networks.

Market Size & Growth: USD 250.0 Million in 2025, projected to reach USD 877.9 Million by 2033, growing at 17% CAGR driven by rising demand for real-time engagement analytics.

Top Growth Drivers: AI adoption in marketing (68%), engagement-based targeting improvement (52%), shift from impression to attention metrics (47%).

Short-Term Forecast: By 2028, attention-based optimization is expected to improve ad performance efficiency by 35%.

Emerging Technologies: Eye-tracking AI, computer vision-based gaze detection, multimodal attention analytics platforms.

Regional Leaders: North America (USD 320 Million by 2033, enterprise-driven adoption), Europe (USD 240 Million, compliance-focused AI), Asia-Pacific (USD 210 Million, mobile-first engagement growth).

Consumer/End-User Trends: Over 60% of brands prioritize attention metrics over click-through rates in campaign evaluation.

Pilot or Case Example: In 2025, a global retail brand achieved 28% higher ad recall using AI-driven attention optimization tools.

Competitive Landscape: Market leader holds ~22% share; key players include multiple AI ad-tech firms driving innovation.

Regulatory & ESG Impact: Over 45% of firms align with AI transparency and data privacy frameworks in advertising.

Investment & Funding Patterns: Over USD 3.5 billion invested in AI advertising analytics startups between 2023–2025.

Innovation & Future Outlook: Integration of generative AI with attention scoring is expected to redefine ad personalization strategies.

AI-powered advertising attention measurement platforms are increasingly adopted across retail (34%), media (27%), and BFSI (18%) sectors. Innovations such as predictive gaze modeling and real-time engagement heatmaps are enhancing campaign effectiveness. Regulatory frameworks emphasizing data privacy and ethical AI usage are shaping deployment strategies. North America leads in enterprise adoption, while Asia-Pacific shows rapid growth driven by mobile-first consumption and AI-enabled advertising ecosystems.

The AI-Powered Advertising Attention Measurement Platforms Market is strategically positioned at the intersection of digital advertising transformation and advanced analytics. As advertisers move away from traditional impression-based KPIs, attention metrics have become critical for evaluating true engagement and optimizing ROI. AI-driven gaze tracking and cognitive engagement models deliver up to 40% improvement compared to traditional click-through rate analysis, enabling more precise targeting and campaign optimization.

North America dominates in volume due to large-scale enterprise deployments, while Europe leads in adoption with over 62% of enterprises integrating AI-driven compliance-focused attention analytics solutions. The market is also benefiting from rapid adoption in Asia-Pacific, where mobile-first advertising ecosystems are accelerating AI integration across digital platforms.

By 2028, AI-powered attention analytics is expected to reduce wasted ad spend by nearly 30% through real-time optimization and predictive modeling. Firms are committing to ESG metrics, including reducing data processing energy consumption by 20% through efficient AI algorithms by 2030. In 2025, a leading advertising technology firm in the United States achieved a 33% improvement in campaign engagement by deploying multimodal attention analytics integrating video, audio, and behavioral data.

Looking ahead, the AI-Powered Advertising Attention Measurement Platforms Market will play a pivotal role in enabling data-driven, compliant, and sustainable advertising strategies, positioning itself as a cornerstone of next-generation digital marketing ecosystems.

The AI-Powered Advertising Attention Measurement Platforms Market is evolving rapidly as enterprises prioritize measurable engagement over traditional advertising metrics. The integration of artificial intelligence with computer vision and behavioral analytics has transformed how advertisers assess campaign effectiveness. Over 72% of digital campaigns now incorporate some form of AI-driven analytics, with attention measurement emerging as a key differentiator. The growing adoption of omnichannel marketing strategies has further increased demand for platforms capable of delivering real-time, cross-device attention insights. Additionally, the expansion of connected TV, short-form video platforms, and immersive digital formats has intensified the need for advanced attention tracking solutions. Regulatory developments around data privacy and AI transparency are also influencing platform design, pushing companies to adopt privacy-preserving technologies. Overall, the market is shaped by technological innovation, increasing enterprise demand for actionable insights, and the shift toward performance-based advertising models.

The increasing inadequacy of traditional metrics such as impressions and click-through rates is driving the adoption of attention-based analytics. Studies indicate that nearly 65% of digital ads are not viewed for more than two seconds, highlighting inefficiencies in conventional measurement systems. AI-powered attention platforms address this gap by analyzing gaze duration, screen visibility, and user engagement patterns in real time. Over 58% of advertisers have reported improved campaign effectiveness after integrating attention metrics into their strategies. Additionally, the rise of video-centric platforms, where over 80% of content consumption occurs, has accelerated demand for precise engagement tracking. These platforms enable brands to optimize ad placements and creative elements dynamically, leading to measurable improvements in recall and conversion rates.

Data privacy regulations and consumer concerns are significant barriers to market growth. More than 70% of global consumers express concerns about how their behavioral data is tracked and used in digital advertising. Regulations such as GDPR and evolving AI governance frameworks require companies to implement strict data handling and transparency measures. Compliance costs have increased by approximately 25% for firms deploying AI-based analytics solutions. Furthermore, limitations on third-party cookies and tracking technologies restrict data availability, impacting the accuracy of attention measurement models. Organizations must invest in privacy-preserving AI techniques, such as federated learning and anonymization, which can increase operational complexity and delay deployment timelines.

The expansion of omnichannel advertising presents significant growth opportunities for attention measurement platforms. With over 75% of consumers interacting with brands across multiple digital touchpoints, there is a growing need for unified attention analytics. AI-powered platforms can integrate data from mobile, desktop, connected TV, and social media channels, providing comprehensive insights into user engagement. Retail and e-commerce sectors, accounting for over 40% of digital ad spending, are increasingly adopting these solutions to optimize cross-channel campaigns. Additionally, advancements in multimodal AI enable simultaneous analysis of visual, auditory, and behavioral signals, enhancing accuracy and scalability. These capabilities open new avenues for personalized advertising and real-time campaign optimization.

Integration with existing marketing technology stacks remains a major challenge for market participants. Enterprises typically use multiple platforms for data management, customer relationship management, and ad delivery, making seamless integration difficult. Over 55% of organizations report challenges in aligning attention measurement tools with legacy systems. Additionally, the need for high computational power to process real-time engagement data increases infrastructure costs by approximately 30%. Compatibility issues with various digital channels and formats further complicate deployment. Companies must also ensure interoperability across platforms while maintaining data accuracy and compliance, which requires significant technical expertise and investment.

Surge in AI-Based Eye-Tracking Without Hardware: Over 68% of platforms now use camera-free gaze prediction models, reducing deployment costs by nearly 40% while maintaining accuracy levels above 85%. This shift is enabling large-scale adoption across mobile and web-based advertising environments.

Expansion of Multimodal Attention Analytics: Around 57% of advanced platforms integrate visual, audio, and behavioral signals simultaneously, improving engagement prediction accuracy by 32%. This trend is particularly strong in video advertising, where multimodal data enhances campaign performance insights.

Growing Adoption in Connected TV Advertising: Connected TV campaigns now account for over 35% of attention measurement use cases, with attention scores improving ad recall rates by up to 28%. Advertisers are prioritizing large-screen engagement analytics to optimize premium content placements.

Integration of Generative AI in Ad Optimization: Nearly 45% of platforms are incorporating generative AI to dynamically adjust ad creatives based on real-time attention data, resulting in up to 30% improvement in viewer retention and engagement rates across digital campaigns.

The AI-Powered Advertising Attention Measurement Platforms Market is segmented based on type, application, and end-user, reflecting diverse adoption patterns across industries. The market is characterized by increasing demand for advanced analytics solutions that provide real-time engagement insights. Different platform types cater to varying levels of complexity, from basic gaze tracking to sophisticated multimodal attention analytics. Applications span across digital advertising channels, including social media, video streaming, and programmatic advertising. End-users range from large enterprises to SMEs, with varying degrees of adoption depending on digital maturity and marketing budgets. The segmentation highlights the growing importance of tailored solutions to meet specific industry requirements and optimize advertising performance.

AI-powered attention measurement platforms are categorized into eye-tracking-based systems, computer vision-based attention analytics, and multimodal AI platforms. Computer vision-based platforms lead the market, accounting for approximately 48% of adoption due to their scalability and ability to analyze engagement without specialized hardware. Eye-tracking systems hold around 28%, primarily used in high-precision research and premium advertising campaigns. Multimodal AI platforms, currently at 24%, are the fastest-growing segment with an expected growth rate of 19%, driven by their ability to integrate visual, auditory, and behavioral data for comprehensive analysis. Other niche solutions, including biometric and EEG-based systems, collectively contribute to a smaller share but are gaining traction in specialized applications.

• In 2025, a major global streaming platform implemented computer vision-based attention analytics to optimize video ad placements, improving viewer engagement by over 25%.

Key applications include digital display advertising, video advertising, social media advertising, and programmatic advertising. Video advertising dominates with approximately 42% share due to its high engagement potential and increasing consumption of video content across platforms. Social media advertising accounts for 26%, while programmatic advertising is the fastest-growing segment, driven by automation and real-time bidding capabilities, with an expected growth rate of 18%. Other applications, including display advertising, collectively hold around 32%. In 2025, more than 38% of enterprises globally reported piloting attention measurement systems for customer experience platforms, while over 60% of Gen Z consumers showed higher engagement with AI-optimized ads.

• In 2025, AI-driven attention analytics were deployed across over 200 digital campaigns globally, improving ad recall rates by an average of 22%.

Major end-users include retail & e-commerce, media & entertainment, BFSI, and healthcare. Retail & e-commerce leads with approximately 34% share, driven by high digital advertising expenditure and the need for performance optimization. Media & entertainment follows with 27%, leveraging attention analytics for content monetization. BFSI is the fastest-growing segment, with an expected growth rate of 18%, as financial institutions adopt AI-driven marketing strategies to enhance customer engagement. Other sectors, including healthcare and telecom, collectively account for around 39%. In 2025, over 45% of enterprises reported integrating AI-based attention analytics into marketing workflows, with adoption particularly high among large enterprises.

• In 2025, over 500 retail companies implemented AI-powered attention measurement tools, achieving an average 20% improvement in campaign effectiveness.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19% between 2026 and 2033.

North America benefits from high enterprise adoption, with over 60% of large organizations deploying AI-based attention analytics. Europe holds approximately 27% share, driven by strong regulatory frameworks and demand for privacy-compliant AI solutions. Asia-Pacific accounts for around 23%, supported by rapid digital transformation and mobile-first advertising ecosystems. South America and the Middle East & Africa collectively contribute about 12%, with increasing investments in digital advertising infrastructure. The global market is witnessing strong regional diversification, with emerging economies playing a critical role in future growth.

North America holds approximately 38% of the global market, driven by strong demand from retail, media, and technology sectors. Over 62% of enterprises in the region have integrated AI-driven attention analytics into their marketing strategies. Regulatory frameworks emphasizing data transparency have encouraged adoption of privacy-focused AI solutions. Technological advancements, including real-time analytics and multimodal AI, are widely implemented. A leading regional player has developed advanced gaze prediction algorithms, improving campaign efficiency by 30%. Consumer behavior indicates higher adoption among large enterprises, particularly in finance and healthcare sectors.

Europe accounts for around 27% of the market, with key countries including Germany, the UK, and France leading adoption. Regulatory bodies enforce strict data privacy standards, driving demand for explainable AI solutions. Approximately 58% of enterprises prioritize compliance when selecting attention measurement platforms. The region is witnessing increased adoption of privacy-preserving technologies such as federated learning. A regional AI firm has introduced compliant attention analytics tools, enhancing transparency and user trust. Consumer behavior reflects a strong preference for ethical AI applications in advertising.

Asia-Pacific represents about 23% of the market, with China, India, and Japan as key contributors. The region is experiencing rapid growth due to expanding digital infrastructure and high mobile penetration. Over 70% of digital advertising in the region occurs on mobile devices, driving demand for scalable attention analytics solutions. Innovation hubs are emerging in major cities, supporting AI development. A regional technology firm has implemented AI-based attention tracking in mobile advertising, improving engagement rates by 25%. Consumer behavior is driven by e-commerce and social media platforms.

South America holds approximately 7% of the market, with Brazil and Argentina leading adoption. The region is witnessing growth in digital media consumption, with over 65% of internet users engaging with online advertising content. Government initiatives supporting digital transformation are encouraging adoption of AI technologies. A local ad-tech company has introduced AI-driven attention measurement tools tailored for regional languages, improving campaign effectiveness. Consumer behavior indicates strong demand for localized advertising solutions.

The Middle East & Africa region accounts for around 5% of the market, with the UAE and South Africa as key contributors. Rapid digital transformation and increasing internet penetration are driving demand for AI-powered analytics solutions. Over 50% of enterprises are investing in digital advertising technologies. Government initiatives supporting AI adoption are accelerating market growth. A regional player has developed AI-based attention analytics platforms for digital campaigns, improving engagement rates. Consumer behavior reflects growing adoption of digital media platforms.

United States – 32% Market share: strong enterprise adoption and high investment in AI-driven advertising technologies

United Kingdom – 11% Market share: advanced regulatory frameworks and high demand for privacy-compliant analytics solutions

The AI-Powered Advertising Attention Measurement Platforms Market is moderately fragmented, with over 80 active players globally competing across technology innovation, analytics accuracy, and platform scalability. The top five companies collectively account for approximately 48% of the market, indicating a competitive yet innovation-driven environment. Market leaders focus on developing advanced AI algorithms, including computer vision and multimodal analytics, to enhance attention measurement capabilities. Strategic partnerships between ad-tech firms and digital media platforms are increasing, enabling integrated solutions for advertisers. Mergers and acquisitions have also intensified, with companies aiming to expand technological capabilities and geographic reach. Product innovation remains a key differentiator, with over 60% of companies investing in real-time analytics and generative AI integration. Additionally, startups are entering the market with specialized solutions, particularly in privacy-preserving AI and mobile-first analytics. The competitive landscape is shaped by continuous technological advancements, evolving customer requirements, and increasing emphasis on data privacy and compliance.

Realeyes

Amplified Intelligence

Adelaide Metrics

Attention Economy Analytics

Neurons Inc

TVision Insights

iMotions

EyeSee

Kantar

Nielsen

Oracle Advertising

Meta Platforms

The technological landscape of the AI-Powered Advertising Attention Measurement Platforms Market is evolving rapidly, driven by advancements in artificial intelligence, machine learning, and computer vision. Modern platforms leverage deep learning algorithms to analyze gaze patterns, facial expressions, and user interactions in real time. Approximately 72% of platforms now incorporate computer vision techniques, enabling accurate attention tracking without requiring specialized hardware. This shift has significantly reduced deployment costs and expanded accessibility across digital channels.

Multimodal AI is emerging as a key innovation, integrating visual, auditory, and behavioral data to provide comprehensive insights into user engagement. Around 57% of advanced solutions utilize multimodal analytics, improving prediction accuracy by over 30%. Generative AI is also playing a transformative role, with nearly 45% of platforms adopting it to dynamically optimize ad creatives based on real-time attention data. This enables personalized advertising experiences and enhances campaign effectiveness.

Privacy-preserving technologies, such as federated learning and differential privacy, are gaining traction, with over 50% of companies implementing these methods to comply with regulatory requirements. Additionally, cloud-based deployment models dominate the market, accounting for more than 65% of implementations, providing scalability and real-time processing capabilities. Edge computing is also emerging, enabling faster data processing and reduced latency. These technological advancements are reshaping the market, enabling more accurate, efficient, and compliant attention measurement solutions.

• In February 2026, Lumen Researchpartnered with SeenThis to launch a new AI-powered attention measurement model integrating adaptive video streaming. Campaign testing showed a +37% improvement in attention per thousand impressions (APM)and +22% increase in viewability, validating real-time attention optimization in programmatic advertising.

• In March 2026, Lumen Researchannounced a collaboration with Netflix to deliver cross-device attention measurement across CTV, mobile, and desktop environments. The solution leverages one of the largest consented eye-tracking datasets, enabling advertisers to optimize media allocation and improve campaign effectiveness across streaming platforms.

• In late 2025, Lumen Researchpublished findings showing that high-attention media plans deliver 12% higher market share growthand 40% greater attention on trusted news platforms, reinforcing the measurable impact of attention metrics on campaign performance and brand outcomes.

• In 2025 (industry framework release), Adelaide Metrics, alongside major ad-tech players, contributed to the development of standardized attention measurement frameworks under industry bodies, enabling cross-platform comparability of attention signals across digital campaignsand improving transparency in media buying ecosystems. Source: www.insurads.com

The AI-Powered Advertising Attention Measurement Platforms Market Report provides a comprehensive analysis of industry dynamics, covering key segments, technologies, applications, and regional markets. The report evaluates multiple platform types, including eye-tracking systems, computer vision-based analytics, and multimodal AI solutions, offering insights into their adoption across industries. Applications analyzed include digital display advertising, video advertising, social media campaigns, and programmatic advertising, reflecting the diverse use cases of attention measurement technologies.

Geographically, the report covers major regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into country-level trends and adoption patterns. The report also examines end-user industries, including retail & e-commerce, media & entertainment, BFSI, healthcare, and telecom, highlighting their contribution to market development.

Additionally, the report explores technological advancements, including AI algorithms, cloud computing, edge processing, and privacy-preserving technologies, which are shaping the future of the market. It also provides insights into competitive dynamics, profiling key players and their strategic initiatives. Emerging trends such as generative AI integration, multimodal analytics, and real-time optimization are analyzed to provide a forward-looking perspective. Overall, the report serves as a strategic tool for decision-makers, offering actionable insights into market opportunities, challenges, and future growth pathways.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 250.0 Million |

| Market Revenue (2033) | USD 877.9 Million |

| CAGR (2026–2033) | 17.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Lumen Research; Realeyes; Amplified Intelligence; Adelaide Metrics; Attention Economy Analytics; Neurons Inc.; TVision Insights; iMotions; EyeSee; Kantar; Nielsen; Oracle Advertising; Google; Meta Platforms |

| Customization & Pricing | Available on Request (10% Customization Free) |