Reports

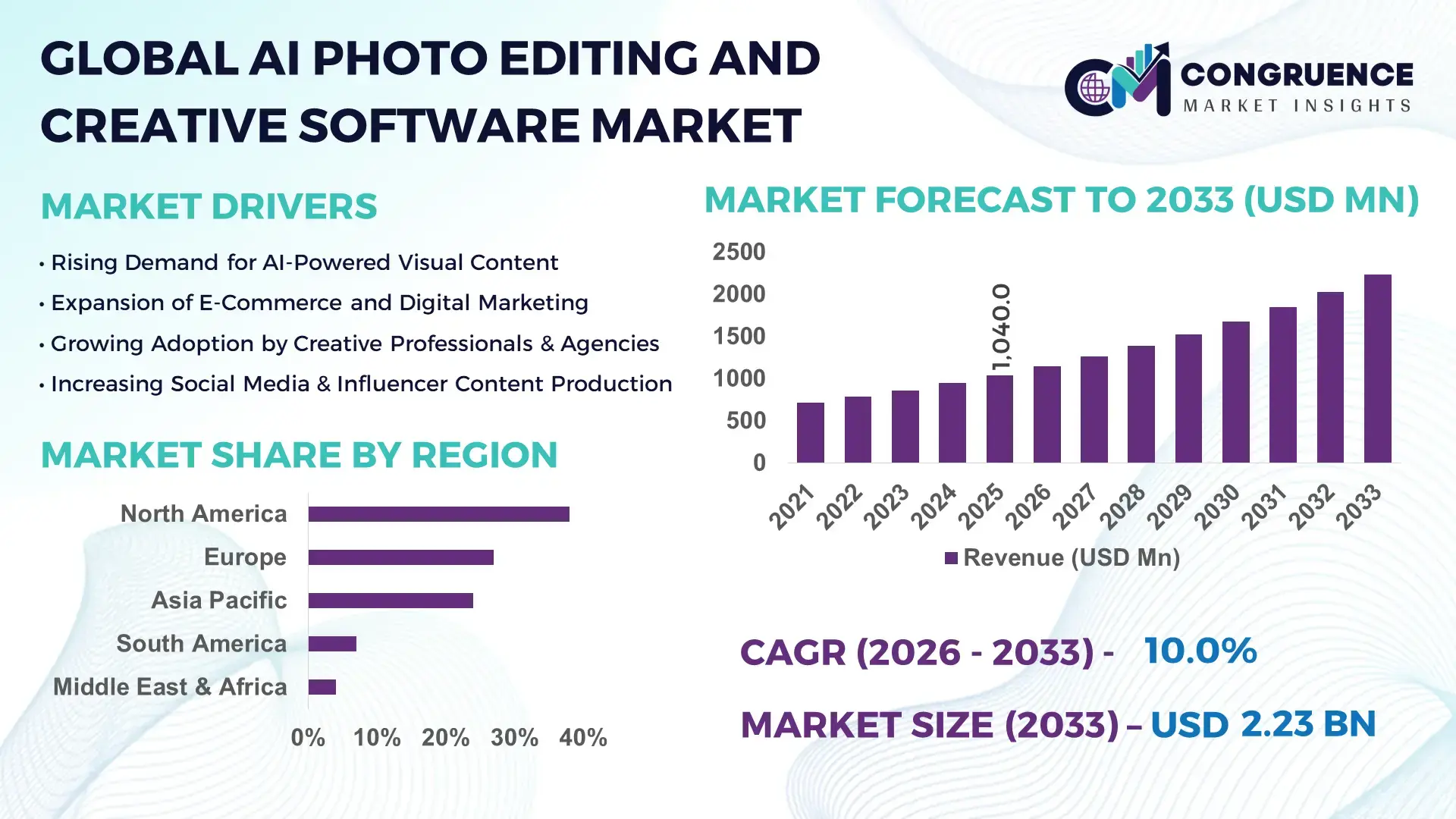

The Global AI Photo Editing and Creative Software Market was valued at USD 1,040.0 Million in 2025 and is anticipated to reach a value of USD 2,229.3 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the rapid integration of generative AI, automation, and cloud-based creative workflows across professional, enterprise, and consumer digital content ecosystems.

The United States dominates the AI Photo Editing and Creative Software Market in terms of technological leadership and commercial deployment. The country hosts over 65% of global AI creative software R&D centers, with major platforms operating large-scale cloud infrastructure supporting millions of daily image-processing tasks. In 2024, U.S.-based companies processed more than 18 billion AI-assisted image edits annually, spanning media, advertising, e-commerce, and entertainment applications. Enterprise adoption is strong, with nearly 72% of U.S. design and marketing firms using AI-driven photo enhancement or generative tools in production workflows. Investment levels remain high, with over USD 3.8 billion allocated to AI creative software development and infrastructure upgrades between 2022 and 2024. Advanced diffusion models, multimodal AI engines, and GPU-accelerated rendering pipelines developed in the U.S. continue to set global benchmarks for speed, accuracy, and creative scalability.

Market Size & Growth: Valued at USD 1,040.0 Million in 2025, projected to reach USD 2,229.3 Million by 2033, expanding at a CAGR of 10%, driven by automation of creative workflows and generative AI adoption.

Top Growth Drivers: AI-assisted editing adoption at 68%, workflow efficiency improvement of 45%, and cloud-based collaboration penetration at 52%.

Short-Term Forecast: By 2028, AI-driven automation is expected to reduce manual editing time by 40% across professional studios.

Emerging Technologies: Diffusion-based image generation, multimodal AI editing engines, real-time cloud rendering.

Regional Leaders: North America USD 840 Million, Europe USD 610 Million, Asia Pacific USD 520 Million by 2033, with APAC showing fastest mobile-creator adoption.

Consumer/End-User Trends: Over 60% of individual users prefer AI-powered one-click enhancements over manual tools.

Pilot or Case Example: In 2024, an enterprise media pilot reduced post-production turnaround time by 35% using AI retouching.

Competitive Landscape: Adobe (~32%), followed by Canva, Corel, CyberLink, and Skylum.

Regulatory & ESG Impact: AI transparency rules influencing model explainability and dataset governance standards.

Investment & Funding Patterns: More than USD 4.5 Billion invested globally in AI creative software startups since 2021.

Innovation & Future Outlook: Deep AI-human co-creation, API-driven platforms, and real-time generative design ecosystems shaping future growth.

The AI Photo Editing and Creative Software Market serves media and entertainment (~34%), advertising and marketing (~27%), e-commerce (~18%), and individual creators (~21%). Recent innovations include text-to-image workflows, automated background replacement, and AI-powered style transfer. Regulatory focus on ethical AI, rising digital content demand, and strong adoption in North America and Asia Pacific continue to define consumption patterns, while real-time generative creativity shapes long-term outlook.

The AI Photo Editing and Creative Software Market holds strong strategic relevance as digital content becomes central to brand communication, commerce, and user engagement. Enterprises are increasingly embedding AI creative tools into marketing, product visualization, and customer experience platforms to reduce cycle times and improve output consistency. Advanced diffusion-based generative AI delivers 55% productivity improvement compared to traditional manual raster-editing standards, enabling faster ideation and scalable content production.

From a regional perspective, North America dominates in volume, while Asia Pacific leads in adoption with nearly 58% of creators and SMEs actively using AI-powered photo editing tools. Short-term projections indicate that by 2028, automated generative editing is expected to cut creative production costs by 30%, particularly in e-commerce and digital advertising workflows.

Compliance and ESG considerations are shaping platform strategies, with firms committing to 20% reduction in compute-related carbon intensity by 2030 through optimized model training and energy-efficient data centers. A micro-scenario illustrates this impact: in 2024, a U.S.-based media technology firm achieved a 38% reduction in post-production time by deploying AI-assisted retouching and automated color grading pipelines.

Looking ahead, the AI Photo Editing and Creative Software Market is positioned as a pillar of operational resilience, regulatory alignment, and sustainable digital growth, enabling organizations to balance creativity, efficiency, and responsible AI deployment.

The AI Photo Editing and Creative Software Market is characterized by rapid technological evolution, increasing cloud penetration, and expanding creator economies. Demand is influenced by the surge in digital media consumption, rising e-commerce visual standards, and enterprise-level automation of creative processes. Continuous improvements in neural rendering, generative models, and multimodal AI have significantly lowered skill barriers, enabling non-professional users to access advanced editing capabilities. At the same time, enterprises are integrating AI creative tools into broader digital experience platforms, increasing interoperability and data-driven design optimization. Regional dynamics vary, with mature markets focusing on workflow efficiency and emerging markets prioritizing accessibility and mobile-first creativity solutions.

The growing need for high-volume, visually rich digital content is a key driver of the AI Photo Editing and Creative Software Market. Businesses now produce 3–4× more visual assets than five years ago across marketing, social media, and e-commerce channels. AI-powered photo editing tools enable automation of repetitive tasks such as retouching, resizing, and background replacement, reducing production timelines by up to 45%. This efficiency is particularly valuable for e-commerce platforms managing catalogs with millions of images and advertising agencies operating under tight campaign schedules. The shift toward omnichannel digital engagement continues to reinforce demand for scalable AI creative solutions.

Data privacy, copyright, and AI model transparency issues present notable restraints. Many AI photo editing tools rely on large training datasets, raising concerns over unauthorized use of copyrighted images. Regulatory scrutiny has increased, with over 40% of enterprises delaying full-scale deployment until compliance frameworks are clarified. Additionally, lack of explainability in generative outputs can limit adoption in regulated industries such as media publishing and corporate communications. These factors can slow enterprise procurement cycles and increase compliance costs.

The rapid growth of global creator economies offers substantial opportunities. More than 200 million individuals worldwide now earn income through digital content platforms, many relying on AI-powered editing tools to scale output. Affordable subscription models, mobile-first AI editors, and integrated monetization features are expanding adoption among freelancers, influencers, and small businesses. As creators demand faster, more personalized tools, vendors can differentiate through adaptive AI models, localized features, and seamless platform integrations.

High computational requirements for training and deploying advanced generative models remain a challenge. GPU-intensive workloads can increase operating costs by 25–35%, particularly for real-time rendering and high-resolution image generation. Smaller vendors may struggle to balance performance with affordability, while enterprises face rising cloud infrastructure expenses. Managing compute efficiency without compromising output quality is a critical challenge for sustained market expansion.

Expansion of Generative AI Editing Pipelines: Over 62% of new creative software releases in 2024 incorporated generative AI features, enabling users to create, edit, and enhance images in under 50% of traditional processing time. Enterprises report 35% faster campaign deployment using generative workflows.

Cloud-Based Collaborative Editing Adoption: Cloud-native AI editing platforms now support 70% of enterprise creative teams, enabling real-time collaboration and reducing version-control errors by 42%. Cross-region collaboration has increased productivity by 28%.

Mobile-First AI Creative Tools Growth: Mobile AI photo editing applications recorded 48% year-on-year user growth, with smartphones accounting for 55% of total AI-edited images globally. Lightweight models reduced processing latency by 30%.

Ethical AI and Responsible Design Integration: Nearly 46% of vendors have implemented AI transparency dashboards and consent-based training controls, while optimized models reduced energy consumption per image edit by 18%, aligning innovation with sustainability goals.

The AI Photo Editing and Creative Software Market is segmented by type, application, and end-user, reflecting the diverse ways artificial intelligence is embedded across creative value chains. By type, the market ranges from AI-powered photo enhancement tools to generative image creation and automated design platforms, each addressing different complexity and workflow needs. Application-wise, adoption spans advertising, media production, e-commerce visualization, social media content creation, and enterprise branding, with demand closely linked to digital engagement intensity and content volume. End-user segmentation highlights strong uptake among creative professionals and enterprises, while individual creators and small businesses represent a rapidly expanding user base due to accessible subscription models and mobile-first tools. Across all segments, automation depth, ease of integration, and scalability remain decisive factors shaping purchasing and deployment decisions.

AI-powered photo enhancement and retouching tools represent the leading type, accounting for approximately 38% of overall adoption, driven by their widespread use in advertising, e-commerce, and professional photography workflows. These tools automate color correction, object removal, and resolution enhancement, reducing manual editing time by up to 45% in commercial settings. Generative image creation platforms follow closely, holding around 31% adoption, enabling text-to-image and style-transfer capabilities increasingly used in marketing and concept design. However, AI-driven video and multimodal creative tools are the fastest-growing type, expanding at an estimated 14% CAGR, fueled by rising short-form video content and demand for dynamic visual storytelling. Supporting growth is the integration of image, text, and layout generation in a single interface. Other types, including AI-assisted layout design and background synthesis tools, collectively contribute about 31%, serving niche but essential roles in specialized creative workflows.

A 2025 industry technology review highlighted that a major global media platform deployed generative image tools to automate thumbnail creation, improving visual consistency across more than 12 million digital assets.

Advertising and marketing remain the leading application area, representing nearly 35% of market usage, as brands increasingly rely on AI tools to generate, localize, and personalize visual campaigns at scale. E-commerce visualization is another major application at 27%, where AI photo editing improves product imagery quality and conversion performance through automated background removal and lighting optimization. Social media and influencer content creation is the fastest-growing application, advancing at an estimated 15% CAGR, supported by the rapid rise of short-form visual platforms and creator economies. Other applications, including media production, education, and enterprise branding, together account for roughly 38%, providing stable demand across professional and institutional use cases. In 2025, over 41% of global enterprises reported piloting AI-powered creative tools for customer engagement initiatives, while 62% of Gen Z users preferred AI-enhanced visuals over manually edited content for social platforms.

A 2025 global industry assessment noted that AI-driven image optimization tools were deployed across hundreds of online retail platforms, enhancing visual load performance and user engagement for millions of shoppers.

Creative professionals and enterprises form the leading end-user segment, accounting for approximately 44% of total adoption, as agencies, media houses, and large brands integrate AI photo editing into standardized production pipelines. These users prioritize scalability, integration with existing software ecosystems, and collaborative cloud workflows. Individual creators and freelancers represent the fastest-growing end-user group, expanding at an estimated 16% CAGR, driven by affordable subscriptions, mobile accessibility, and the ability to produce high-quality visuals without advanced technical skills. Small and medium-sized businesses, educational institutions, and non-profit organizations collectively contribute around 56%, reflecting broad-based adoption across sectors. In 2025, more than 39% of SMEs globally reported using AI creative tools for digital marketing, while 58% of independent creators relied on AI-assisted photo editing as their primary production method.

A 2025 enterprise technology survey observed that thousands of small creative agencies adopted AI-powered editing platforms, achieving measurable improvements in turnaround time and project throughput across client portfolios.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.6% between 2026 and 2033.

North America continues to lead due to high enterprise penetration, with over 72% of large creative agencies integrating AI-based photo editing tools into daily workflows. Europe followed with a 27% share, supported by strong regulatory alignment and adoption of explainable AI in creative applications. Asia-Pacific held approximately 24%, driven by rapid mobile creator growth and e-commerce-led demand, while South America and the Middle East & Africa collectively accounted for nearly 11%, reflecting emerging adoption across media localization and digital infrastructure expansion. Regional variation is strongly influenced by cloud readiness, creator economy maturity, and regulatory frameworks governing AI deployment.

The market holds a dominant position with an estimated 38% share in 2025, supported by strong demand from advertising, media & entertainment, e-commerce, and enterprise marketing sectors. Over 68% of Fortune 1000 companies deploy AI-powered creative tools to automate campaign production and asset optimization. Government-backed AI innovation programs and updated digital copyright frameworks have increased enterprise confidence in AI-generated content. Technological advancements such as GPU-accelerated cloud rendering and multimodal generative models are widely adopted. A leading local player has expanded AI-powered background generation and brand-consistent design automation, processing billions of images annually. Consumer behavior shows higher enterprise-led adoption, particularly in healthcare, finance, and retail, where compliance-ready AI tools are preferred over standalone consumer apps.

Europe represents approximately 27% of the global market, with Germany, the UK, and France accounting for more than 60% of regional demand. Regulatory frameworks emphasizing data privacy and AI explainability have accelerated demand for transparent and auditable creative AI tools. Sustainability initiatives have also encouraged energy-efficient AI model deployment, reducing compute intensity by nearly 18% across several platforms. Adoption of generative design and automated localization tools is increasing among publishers and multinational brands. A prominent European creative software provider has integrated consent-based AI training controls to align with regional regulations. Consumer behavior reflects strong preference for explainable and controllable AI outputs, particularly among enterprise and public-sector users.

Asia-Pacific ranks as the fastest-growing regional market, holding close to 24% share in 2025. China, India, and Japan together contribute over 70% of regional usage, driven by massive e-commerce ecosystems and mobile content creation. Infrastructure investments in cloud data centers and AI accelerators support high-volume image processing at scale. Regional innovation hubs focus on lightweight AI models optimized for smartphones, reducing processing latency by 30–35%. A major regional platform has deployed AI-powered image enhancement tools across social commerce apps used by hundreds of millions of users. Consumer behavior is strongly influenced by mobile-first adoption, with creators prioritizing speed, affordability, and social media compatibility.

South America accounts for roughly 7% of the global market, led by Brazil and Argentina, which together represent nearly 65% of regional demand. Growth is supported by expanding digital media consumption, localized advertising, and multilingual content needs. Infrastructure upgrades in cloud connectivity and broadband access have improved AI software accessibility. Government-backed digital transformation initiatives have encouraged adoption among SMEs and media startups. A regional creative software firm has focused on AI-driven language-specific visual customization for advertising campaigns. Consumer behavior shows demand closely tied to media production, social platforms, and localized branding rather than large enterprise automation.

The region contributes approximately 4% of the global market, with the UAE and South Africa emerging as primary growth centers. Demand is driven by media, tourism, construction marketing, and government digital identity projects. Investments in smart city initiatives and cloud infrastructure have increased AI software adoption across creative and communication use cases. Regional regulations increasingly support AI innovation while emphasizing ethical deployment. A local technology firm has introduced AI-powered visual content tools for tourism promotion and public-sector campaigns. Consumer behavior varies widely, with enterprise-led adoption in the Gulf states and creator-driven usage in parts of Africa.

United States – 31% Market Share: Strong enterprise demand, advanced cloud infrastructure, and large-scale AI R&D investments support leadership in the AI Photo Editing and Creative Software Market.

China – 18% Market Share: High-volume mobile content creation, e-commerce-driven visual demand, and rapid deployment of AI-powered creative platforms underpin its strong position in the AI Photo Editing and Creative Software Market.

The AI Photo Editing and Creative Software Market exhibits a moderately consolidated competitive environment, with an estimated 40 + active competitors ranging from established software giants to agile AI-focused startups. The top 5 companies—Adobe, Canva, Picsart, Skylum, and Pixlr—together hold a combined share of approximately 62 %, reflecting significant influence but leaving ample space for specialized and emerging players. Adobe maintains a leading position, continually expanding its AI portfolio across Photoshop, Creative Cloud, Firefly, and Express, and developing strategic partnerships with Hollywood studios, talent agencies, and production companies to embed generative AI deeper into media production workflows. Other major players such as Canva have broadened offerings through all-in-one creative platforms that integrate AI editing, vector design, and layout features under a freemium model. Picsart supports a vast user base of over 150 million monthly active users, reinforcing its competitive strength in mobile and web environments. Meanwhile, Skylum and Pixlr continue to innovate with advanced AI tools for sky replacement, style transfer, and background removal. Competitive dynamics are also shaped by acquisitions (e.g., Figma’s integration of AI creative tools), product launches, cross-platform integrations, and funding rounds—such as FLORA’s $42 million Series A. Innovation trends influencing competition include multimodal AI models, mobile-first creative workflows, real-time cloud rendering, and low-friction user interfaces. This dynamic landscape demands ongoing investment in R&D, ecosystem partnerships, and user experience enhancements to sustain differentiation and growth.

Skylum

Pixlr

Fotor

Corel Corporation

InPixio

BeFunky

Lightricks

GIMP

Photopea

ImagineArt (Vyro.ai)

VSCO

The technological landscape of the AI Photo Editing and Creative Software Market is evolving rapidly, driven by innovations in generative AI, deep learning, multimodal engines, and cloud-based workflows. Generative AI systems such as transformer-based and diffusion models now form the backbone of advanced photo editing, enabling features like text-to-image generation, intelligent background removal, style transfer, and automated enhancements. Tools powered by multilayer contextual awareness can now interpret complex prompts and apply nuanced visual adjustments without manual intervention, improving creative efficiency for both professionals and individual users. The integration of AI into traditional workflows has expanded beyond standalone applications into conversational interfaces, allowing creators to perform editing tasks directly through natural language inputs across platforms. Mobile AI technologies support on-device enhancements, delivering higher resolution outputs with minimal latency and enabling creators to produce professional-grade visual content on smartphones. Cloud infrastructures further support collaborative editing, real-time version control, and scalable rendering, streamlining creative workflows for distributed teams.

Emerging technical trends include multimodal creative pipelines that unify image, video, and audio editing under a single intelligent framework, and edge-AI optimization that enhances performance on low-power devices. Advancements in neural upscaling and semantic segmentation enable tools to preserve image integrity while performing complex tasks like object replacement and scene relighting. Open-source and community-driven models contribute to broader experimentation, fostering innovation in layered generative control and human-AI co-creation paradigms. As hardware acceleration improves and AI models become more efficient, the market will likely see greater integration of specialized APIs, plugin ecosystems, and adaptive interfaces tailored to specific professional domains such as advertising, entertainment, and fashion.

• In 2025, Adobe integrated additional AI models from industry leaders such as OpenAI and Google into its Firefly app, expanding photo generation capabilities with multiple third-party models and broadening creative options for users across platforms. Source: www.reuters.com

• In late 2025, Adobe expanded its strategic partnership with Google Cloud, integrating advanced AI photo and video models like Gemini, Veo, and Imagen into its creative suite, and collaborating with YouTube to enhance short-form content creation workflows. Source: www.timesofindia.indiatimes.com

• In 2025, Canva relaunched the Affinity Creative Suite as a unified, subscription-free application for photo editing, illustration, and layout design, with integrated AI-powered features for image generation and cleanup, targeting broader adoption across professional and mobile users. Source: www.theverge.com

• In December 2025, VSCO introduced a new AI-powered “AI Upscale” tool within its AI Lab, enabling up to 4× resolution enhancement for images while preserving detail, aimed at revitalizing low-resolution photos on mobile platforms. Source: www.digitalcameraworld.com

The AI Photo Editing and Creative Software Market Report offers a comprehensive evaluation of the market’s breadth, covering multiple product types, application areas, and end-user segments that define the current and emerging landscape. It systematically analyzes types including traditional AI-assisted photo editors, generative image creation tools, integrated creative suites, and multimodal editing platforms, highlighting their role in professional creative workflows, enterprise automation, and consumer-driven content production. On the application front, the report examines usage patterns across advertising, media production, e-commerce visualization, social media content creation, and digital branding, providing numerical and functional insights into how AI capabilities are deployed for image enhancement, background manipulation, concept generation, and collaborative editing.

Geographically, the report evaluates key market regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—detailing market presence, technological adoption, infrastructure readiness, and regional behavioral trends that influence the uptake of AI photo editing solutions. End-user insights include segmentation by creative professionals, enterprises, SMEs, individual creators, educators, and digital agencies, illustrating differentiated adoption dynamics and platform preferences. The technology section explores generative AI models, deep learning frameworks, transformer and diffusion architectures, cloud-native rendering, and AI-enhanced mobile workflows that underpin innovation and competitive advantage. Emerging or niche segments such as AI-driven mobile editing apps, conversational creative interfaces, and interactive co-creation frameworks are also examined, reflecting early adoption signals and growth potential. Tailored for decision-makers and analysts, the report synthesizes numerical insights, platform differentiation, competitive positioning, and user-centric trends to support strategic planning and investment decisions across this rapidly evolving market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,040.0 Million |

| Market Revenue (2033) | USD 2,229.3 Million |

| CAGR (2026–2033) | 10% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Adobe Inc., Canva Ltd., Picsart, Skylum, Pixlr, Fotor, Corel Corporation, InPixio, BeFunky, Lightricks, GIMP, Photopea, ImagineArt (Vyro.ai), VSCO |

| Customization & Pricing | Available on Request (10% Customization Free) |