Reports

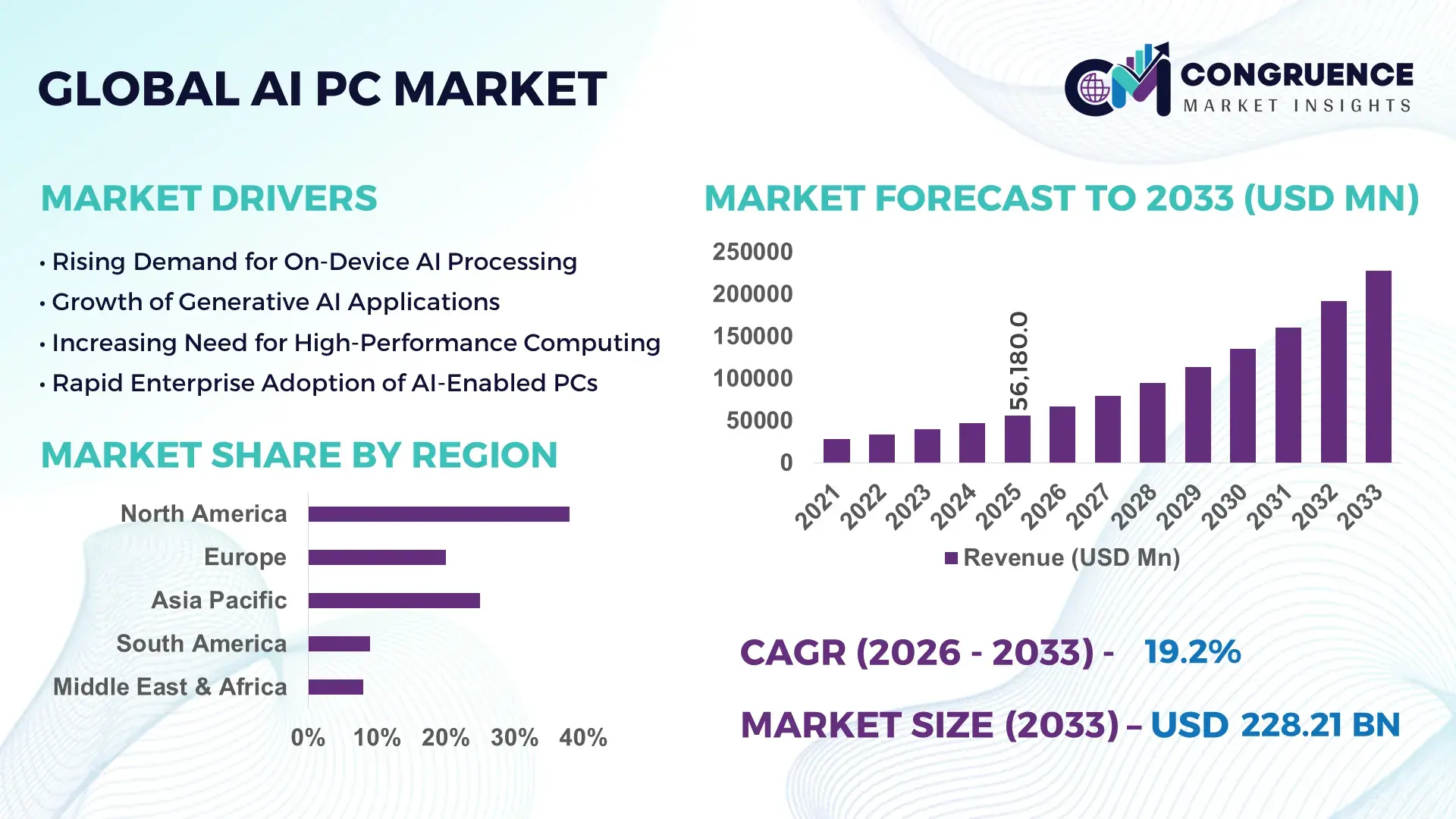

The Global AI PC Market was valued at USD 56180 Million in 2025 and is anticipated to reach a value of USD 228209.7 Million by 2033 expanding at a CAGR of 19.15% between 2026 and 2033. The rapid integration of on-device artificial intelligence capabilities in personal computing systems is accelerating enterprise productivity and consumer adoption.

The United States remains a major production and innovation hub within the AI PC market ecosystem, supported by large-scale semiconductor manufacturing capacity, advanced processor design, and extensive enterprise deployment of AI-enabled computing platforms. U.S.-based technology companies collectively invested more than USD 40 billion in AI hardware and software ecosystem development between 2023 and 2025. AI-enabled laptops and workstations already account for over 35% of enterprise PC refresh cycles in large American organizations. In sectors such as financial services, healthcare diagnostics, and software engineering, more than 42% of high-performance computing endpoints now incorporate neural processing units (NPUs) capable of executing over 40 trillion operations per second. The country also hosts several large-scale AI research labs and cloud infrastructure providers that actively optimize operating systems, chipsets, and edge-AI frameworks specifically for AI PCs.

• Market Size & Growth: Valued at USD 56180 Million in 2025 and projected to reach USD 228209.7 Million by 2033 at a CAGR of 19.15%, driven by rapid enterprise demand for on-device AI processing and high-performance computing devices.

• Top Growth Drivers: Enterprise AI workload adoption (48%), productivity gains from local AI acceleration (35%), and demand for privacy-focused edge computing (27%).

• Short-Term Forecast: By 2028, AI-enabled PCs are expected to improve local computing efficiency by 30% while reducing cloud dependency for AI inference workloads by 22%.

• Emerging Technologies: Integration of neural processing units (NPUs), generative AI copilots embedded in operating systems, and hybrid edge-cloud AI frameworks.

• Regional Leaders: North America projected to reach USD 85 billion by 2033, Asia-Pacific USD 92 billion, and Europe USD 36 billion, with strong enterprise device refresh cycles and AI productivity tool adoption.

• Consumer/End-User Trends: Software developers, enterprise analysts, digital designers, and data scientists increasingly adopt AI PCs for offline model execution and accelerated workflow automation.

• Pilot or Case Example: In 2024, a multinational technology firm deployed AI-powered PCs across 25,000 employees and reported a 28% productivity improvement in coding and document generation tasks.

• Competitive Landscape: Market leader holds roughly 32% share, followed by major competitors across semiconductor, PC manufacturing, and AI accelerator segments.

• Regulatory & ESG Impact: Governments promoting energy-efficient computing standards targeting 20% power efficiency improvement in AI-enabled processors by 2030.

• Investment & Funding Patterns: More than USD 18 billion in AI hardware ecosystem funding has been directed toward processor design, edge AI frameworks, and advanced device architectures since 2023.

• Innovation & Future Outlook: Integration of multimodal AI assistants, edge inference engines, and secure on-device machine learning pipelines will shape next-generation AI PC architecture.

Enterprise computing currently represents nearly 55% of AI PC deployments, followed by creative professionals and software development environments accounting for around 25% of installations. Recent innovations include dedicated neural engines integrated within CPUs capable of handling over 45 TOPS (trillion operations per second), enabling local generative AI inference and advanced image processing without continuous cloud connectivity. Regulatory frameworks promoting secure data processing are also encouraging enterprises to shift toward on-device AI computing models. Asia-Pacific shows strong consumer adoption growth, particularly in education technology and content creation sectors. Over the next several years, improvements in processor efficiency, operating system AI integration, and hybrid computing architectures are expected to accelerate AI PC deployment across corporate, academic, and consumer environments.

The AI PC market is emerging as a strategic foundation for enterprise productivity, edge computing security, and decentralized artificial intelligence deployment. Devices equipped with neural processing units capable of executing AI workloads locally are enabling faster analytics, improved data privacy, and reduced cloud infrastructure dependency. For instance, on-device AI inference delivers nearly 40% faster response times compared to traditional cloud-based processing architectures.

North America dominates in production volume and enterprise device deployments, while Asia-Pacific leads in consumer adoption with over 46% of technology-focused users actively utilizing AI-powered computing tools in productivity and creative workflows. By 2028, embedded generative AI copilots and local machine learning accelerators are expected to improve enterprise workflow efficiency by approximately 32%.

Environmental compliance is also shaping product design. Manufacturers are committing to sustainability targets such as 25% reductions in device energy consumption and expanded recyclable component usage by 2030. In 2024, a major laptop manufacturer deployed AI-powered device management software across corporate fleets, reducing IT maintenance workload by nearly 21%. As enterprise digital transformation accelerates, the AI PC Market is positioned to become a critical pillar supporting resilient computing infrastructure, regulatory compliance, and long-term sustainable technological growth.

Organizations across finance, healthcare, engineering, and software development are increasingly deploying AI PCs to run machine learning models locally for faster insights and improved data security. Modern AI PCs integrate neural processing units capable of processing over 40 trillion operations per second, enabling real-time generative AI functions such as document summarization, coding assistance, and predictive analytics. Surveys among enterprise IT departments indicate that nearly 44% of organizations plan to transition to AI-enabled PCs within their next hardware refresh cycle. The shift toward hybrid work environments and data privacy regulations is also driving demand for on-device AI computing. By processing sensitive workloads locally rather than relying entirely on cloud services, enterprises reduce latency while strengthening cybersecurity and regulatory compliance.

Despite strong technological momentum, the AI PC market faces adoption barriers related to hardware costs and evolving software ecosystems. AI-enabled laptops equipped with dedicated neural processors often cost 20–30% more than conventional enterprise PCs due to specialized chipsets and advanced cooling architectures. In addition, many enterprise applications are still optimized for cloud-based AI execution rather than on-device inference, limiting the immediate benefits of local AI acceleration. Industry assessments suggest that fewer than 35% of enterprise productivity tools currently support dedicated NPU optimization. This mismatch between hardware capability and software compatibility slows deployment across small and mid-sized organizations that require clear productivity gains before upgrading entire device fleets.

The rapid expansion of edge computing infrastructure presents a significant opportunity for AI PC deployment. Businesses increasingly require localized processing capabilities for data-intensive workloads such as real-time video analytics, cybersecurity monitoring, and intelligent automation. AI PCs equipped with powerful neural engines enable edge AI processing directly on workstations and laptops, reducing latency and network bandwidth consumption. In sectors like healthcare diagnostics and smart manufacturing, on-device AI systems can analyze large datasets instantly without transmitting sensitive information to external servers. Analysts estimate that more than 60% of enterprise AI workloads could shift partially toward edge devices by the end of the decade, creating substantial demand for AI-enabled computing platforms designed for local inference and secure data processing.

One of the primary challenges facing the AI PC market is the fast pace of processor innovation combined with semiconductor supply volatility. Manufacturers must continually redesign hardware architectures to accommodate increasingly powerful neural processing units, advanced graphics processors, and AI-optimized operating systems. These rapid development cycles increase research and manufacturing costs while shortening product lifecycles. Additionally, global semiconductor supply disruptions have periodically affected availability of advanced AI chips used in laptops and workstations. Industry supply chain reports indicate that high-performance AI processor demand has increased by more than 50% since 2023, creating procurement pressure for device manufacturers. Balancing innovation speed, supply stability, and device affordability remains a critical challenge for long-term AI PC market expansion.

• Rapid Integration of Dedicated Neural Processing Units (NPUs) in Consumer PCs:

AI PC hardware architecture is rapidly evolving with the integration of high-performance neural processing units capable of handling complex AI inference workloads locally. In 2024, over 38% of newly released premium laptops incorporated NPUs capable of processing more than 40 trillion operations per second. This shift enables on-device execution of generative AI models, real-time language translation, and advanced image processing without continuous cloud connectivity. Corporate IT surveys indicate that nearly 46% of large enterprises plan to prioritize AI-enabled PCs in their next device refresh cycle to support advanced productivity tools such as AI-assisted coding and data analysis. The trend is particularly strong in North America and East Asia, where enterprise device upgrade programs are expanding rapidly.

• Expansion of Generative AI Workflows Driving Enterprise Device Upgrades:

The rapid adoption of generative AI productivity tools is accelerating demand for AI PCs capable of handling local AI workloads. In enterprise environments, more than 52% of knowledge workers now regularly interact with AI-assisted tools for document drafting, coding assistance, and analytics automation. AI PCs equipped with high-performance GPUs and AI accelerators can improve generative AI inference speed by nearly 35% compared with conventional computing devices. Technology adoption studies show that organizations deploying AI-enabled PCs experienced a 27% improvement in workflow automation efficiency across departments such as marketing, finance, and software development. As generative AI continues to expand across business applications, device manufacturers are prioritizing AI-optimized chipsets and software ecosystems.

• Growth in Edge AI Processing Across Enterprise and Professional Workflows:

Edge computing capabilities embedded in AI PCs are transforming how organizations manage sensitive data and real-time analytics workloads. Approximately 41% of AI workloads within enterprise environments are expected to shift partially toward edge devices to reduce latency and improve data privacy compliance. AI PCs with integrated AI accelerators enable rapid execution of tasks such as cybersecurity monitoring, predictive maintenance modeling, and intelligent video analysis. In sectors such as manufacturing and healthcare diagnostics, local AI processing has reduced data processing delays by nearly 28% while lowering cloud dependency by 22%. The expansion of edge AI infrastructure is therefore strengthening the role of AI PCs as intelligent computing hubs in distributed enterprise networks.

• Operating System-Level AI Assistants Reshaping User Productivity Models:

Operating systems are increasingly embedding AI copilots and machine learning frameworks directly into personal computing platforms. More than 33% of newly released business laptops now support integrated AI assistants capable of automating routine tasks such as scheduling, document summarization, and real-time collaboration analysis. Early enterprise deployments show that integrated AI assistants can reduce repetitive administrative workload by nearly 24% for office professionals. In addition, developers using AI-assisted programming tools on AI PCs have reported productivity gains exceeding 29% when compared with traditional development environments. As AI integration at the operating system level expands, AI PCs are becoming central platforms for intelligent workplace productivity and advanced human–machine collaboration.

The AI PC market is segmented by type, application, and end-user categories, reflecting the growing diversity of AI-enabled computing platforms. Laptop-based AI PCs currently account for the largest share due to strong enterprise demand for mobile productivity devices with integrated AI acceleration. Desktop AI workstations remain essential for high-performance tasks such as software development, AI model training, and advanced design workloads. From an application perspective, enterprise productivity and software development represent major adoption areas, followed by creative content generation and data analytics workloads. In terms of end users, large enterprises dominate device deployments due to large-scale digital transformation initiatives, while small and medium-sized businesses are rapidly increasing adoption as AI-powered productivity tools become more accessible and cost-efficient.

AI PC product types primarily include AI laptops, AI desktops, AI workstations, and hybrid edge AI devices designed for specialized computing tasks. AI laptops currently represent the leading segment, accounting for approximately 48% of total AI PC deployments. Their dominance is driven by strong enterprise demand for portable AI-enabled devices capable of running generative AI tools, machine learning applications, and data analytics workloads. Integrated neural processing units and AI-accelerated GPUs enable these devices to perform real-time inference tasks such as natural language processing and automated document generation directly on the device. AI workstations represent the fastest-growing segment with an estimated growth rate of around 22% annually, supported by increasing demand for high-performance computing environments used in software development, engineering simulations, and AI model training. These systems typically include advanced GPUs, large memory configurations exceeding 64 GB, and specialized AI processors capable of supporting large-scale machine learning workloads.

AI desktops also play a significant role in enterprise IT infrastructure, particularly in corporate environments requiring powerful fixed computing systems for analytics and development. Meanwhile, hybrid edge AI devices and specialized AI mini PCs together contribute nearly 18% of deployments, serving niche use cases such as industrial automation, smart surveillance systems, and localized AI inference.

AI PCs are widely used across several applications including enterprise productivity, software development, creative content generation, data analytics, and advanced research computing. Enterprise productivity currently represents the largest application segment, accounting for approximately 44% of AI PC usage. Organizations are increasingly adopting AI-enabled PCs to run generative AI assistants, automate business workflows, and analyze enterprise datasets locally without relying entirely on cloud infrastructure. AI-assisted office tools have improved employee productivity in areas such as document processing and reporting automation. Software development represents the fastest-growing application segment with an estimated growth rate of approximately 24%, supported by rising adoption of AI-powered coding assistants, automated debugging tools, and machine learning development environments. Developers using AI-enabled PCs can accelerate code generation and testing processes while running large language models locally for improved security and lower latency.

Creative content production, including graphic design, video editing, and digital media generation, accounts for around 21% of AI PC applications. Data analytics, scientific research, and simulation workloads collectively contribute roughly 15% of total adoption, particularly within engineering and academic institutions.

The AI PC market serves multiple end-user groups including large enterprises, small and medium-sized businesses (SMEs), educational institutions, and individual professional users. Large enterprises currently represent the leading end-user segment, accounting for approximately 51% of AI PC deployments. These organizations are integrating AI-enabled computing systems into enterprise IT infrastructure to support generative AI productivity tools, cybersecurity analytics, and advanced data processing tasks. Large corporate device refresh programs have accelerated adoption as companies seek to modernize digital workplaces. Small and medium-sized businesses represent the fastest-growing end-user category with an estimated growth rate of approximately 23%, driven by increasing availability of affordable AI-enabled laptops and cloud-integrated productivity software. SMEs are adopting AI PCs to automate customer service tasks, manage data analytics, and enhance operational efficiency without requiring large-scale IT infrastructure.

Educational institutions and research organizations together account for approximately 17% of AI PC deployments, using these systems for AI research, programming education, and data science training. Individual professionals including software developers, digital designers, and content creators contribute nearly 12% of the market as they adopt AI-enabled devices for high-performance creative workflows.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2026 and 2033.

North America’s leadership is supported by strong enterprise device refresh cycles, where more than 52% of corporate IT departments upgraded to AI-enabled laptops during 2024–2025. Europe represents approximately 26% of global demand, driven by rising adoption of AI-powered productivity tools across manufacturing and financial services sectors. Asia-Pacific holds nearly 30% of global AI PC shipments, with China contributing over 40% of regional production capacity and India witnessing more than 33% growth in enterprise PC deployments in 2025. South America accounts for about 4% of the global market, while the Middle East & Africa collectively contribute nearly 2%, with increasing adoption in government digitalization initiatives and smart infrastructure projects.

How Are Enterprise AI Workflows Accelerating Advanced Personal Computing Adoption?

North America represents approximately 38% of global AI PC deployments, supported by strong demand from sectors such as financial services, healthcare technology, software development, and cybersecurity analytics. Corporate organizations across the United States and Canada have integrated AI-enabled laptops into more than 50% of enterprise workstation refresh programs. Government initiatives promoting advanced semiconductor manufacturing and AI innovation are strengthening regional supply chains. Digital transformation strategies in healthcare and financial institutions are accelerating demand for devices capable of running machine learning inference locally. A major regional technology manufacturer launched AI-enabled laptops equipped with neural processing units exceeding 45 TOPS processing capability in 2024. Consumer behavior also reflects higher enterprise adoption, particularly within healthcare diagnostics, finance analytics, and large-scale software development environments.

How Are Data Governance and Sustainable Computing Initiatives Transforming Intelligent PC Adoption?

Europe accounts for roughly 26% of the global AI PC market, with strong demand across Germany, the United Kingdom, and France where enterprise automation and advanced manufacturing systems drive technology upgrades. The region’s regulatory focus on secure data processing and explainable AI is encouraging organizations to deploy AI PCs capable of local data inference. Sustainability initiatives targeting energy-efficient computing have pushed manufacturers to design devices that reduce power consumption by nearly 20%. Industrial sectors such as automotive engineering, robotics development, and financial analytics represent major adoption areas. A European technology hardware manufacturer introduced AI-powered workstations optimized for engineering simulation workloads in 2024. Consumer behavior in the region reflects growing interest in privacy-focused computing solutions as organizations prioritize regulatory compliance and secure AI deployment.

What Factors Are Driving the Rapid Expansion of Intelligent Personal Computing Across High-Growth Technology Ecosystems?

Asia-Pacific represents nearly 30% of global AI PC shipments and ranks among the fastest expanding markets due to strong electronics manufacturing capacity and rapid enterprise digitalization. China, Japan, and India are the leading consuming countries, collectively accounting for over 70% of regional device shipments. China alone produces more than 45% of the region’s AI-capable computing hardware through advanced semiconductor fabrication and large-scale PC assembly plants. Technology innovation hubs in cities such as Shenzhen, Tokyo, and Bengaluru are accelerating development of AI-powered productivity tools and edge computing devices. A major regional PC manufacturer introduced AI laptops capable of processing 40+ TOPS AI workloads locally. Consumer behavior across the region is strongly influenced by e-commerce growth, mobile application ecosystems, and expanding AI-powered digital services.

How Is Digital Infrastructure Development Influencing Intelligent Computing Adoption?

South America accounts for approximately 4% of the global AI PC market, with Brazil and Argentina representing the largest technology consumption hubs. Rapid expansion of digital infrastructure and data center investments is encouraging businesses to adopt AI-enabled computing platforms for analytics and automation tasks. Brazil alone contributes nearly 48% of regional enterprise PC demand, supported by technology modernization initiatives in banking, telecommunications, and digital media sectors. Governments across the region are promoting digital transformation policies and tax incentives designed to expand local technology manufacturing. A regional technology distributor partnered with international hardware manufacturers in 2024 to deploy more than 120,000 AI-capable laptops for corporate IT upgrades. Consumer behavior indicates growing demand for localized language processing tools and AI-driven media production applications.

How Are Smart Infrastructure Projects and Technology Modernization Programs Driving Advanced Computing Demand?

The Middle East & Africa region represents nearly 2% of global AI PC adoption but is witnessing steady growth driven by digital transformation initiatives in the United Arab Emirates, Saudi Arabia, and South Africa. Smart city projects, oil and gas analytics platforms, and infrastructure monitoring systems are increasing demand for AI-capable computing devices capable of running advanced data analysis workloads. Government-led digital economy programs have accelerated enterprise technology adoption across finance, logistics, and public administration sectors. Regional trade partnerships supporting technology imports have improved access to advanced computing hardware. A major technology distributor in the United Arab Emirates deployed over 60,000 AI-enabled enterprise laptops in 2025 to support government digitalization programs. Consumer demand increasingly focuses on AI-powered productivity and multilingual communication tools.

United States – 34% share in the AI PC market: Strong semiconductor innovation, high enterprise adoption of AI productivity tools, and advanced technology infrastructure drive demand.

China – 27% share in the AI PC market: Large-scale electronics manufacturing capacity and strong consumer technology adoption support widespread AI PC production and deployment.

The AI PC market features a moderately consolidated competitive structure characterized by strong technology leadership from a group of global semiconductor manufacturers, personal computer vendors, and AI hardware innovators. More than 45 active technology companies currently compete across AI processor design, PC manufacturing, and AI software integration ecosystems. The top five companies collectively control approximately 58% of global AI PC shipments, supported by large-scale investments in processor development, AI accelerator chips, and next-generation computing architectures.

Competition is increasingly driven by innovation in neural processing units, integrated AI software frameworks, and high-performance graphics technologies capable of supporting advanced generative AI workloads. Major industry players are focusing on strategic partnerships with operating system developers and AI software companies to integrate generative AI assistants directly into computing platforms. Between 2023 and 2025, over 120 new AI-enabled PC models were introduced globally featuring neural processors exceeding 40 trillion operations per second. Mergers, joint research programs, and supply chain alliances are also shaping the competitive landscape as companies aim to strengthen semiconductor availability and accelerate innovation cycles. Additionally, manufacturers are investing heavily in energy-efficient chip architectures capable of improving computing performance by more than 30% while reducing power consumption.

Intel Corporation

Advanced Micro Devices Inc.

NVIDIA Corporation

Apple Inc.

Lenovo Group Ltd.

HP Inc.

Dell Technologies Inc.

Acer Inc.

ASUS Corporation

Samsung Electronics Co. Ltd.

Microsoft Corporation

Qualcomm Technologies Inc.

The AI PC market is being shaped by rapid advances in processor architecture, AI acceleration hardware, and software ecosystems designed to support on-device machine learning workloads. One of the most influential innovations is the integration of dedicated neural processing units (NPUs) capable of delivering over 40–50 trillion operations per second (TOPS), enabling efficient execution of generative AI tasks such as image creation, real-time language translation, and predictive analytics directly on personal computing devices. Modern AI PC chipsets now combine CPUs, GPUs, and NPUs into heterogeneous computing architectures, allowing optimized workload distribution that can improve AI inference performance by nearly 35% while reducing system power consumption by approximately 20%.

Operating systems are also evolving to support integrated AI assistants and developer frameworks that enable seamless deployment of local AI models. AI-enabled development environments now allow developers to run large language models with parameters exceeding 7 billion directly on high-end AI laptops. In addition, memory technologies such as LPDDR5X and high-bandwidth GDDR6 are improving data throughput speeds above 7,500 Mbps, enabling faster model processing. Emerging technologies such as edge AI orchestration platforms, secure on-device model training, and AI-optimized operating system kernels are further strengthening the AI PC ecosystem, allowing enterprises to deploy privacy-focused AI solutions without relying entirely on centralized cloud infrastructure.

• In May 2024, Microsoft introduced Copilot+ PCs, a new category of AI-powered personal computers designed to run advanced AI workloads locally. These devices integrate neural processing units capable of exceeding 40 trillion operations per second, enabling features such as real-time translation, AI image generation, and advanced productivity assistance. Source: www.microsoft.com

• In June 2024, Apple unveiled its new MacBook lineup powered by the M4 chip, featuring a neural engine capable of performing up to 38 trillion operations per second. The chip improves on-device AI processing for tasks such as image editing, speech recognition, and generative AI applications within creative software environments. Source: www.apple.com

• In January 2025, Lenovo expanded its AI PC portfolio by launching new ThinkPad and Yoga models equipped with advanced AI processors and dedicated neural engines. These systems are optimized for enterprise productivity workloads and AI-assisted collaboration tools, targeting large-scale corporate device refresh cycles. Source: www.lenovo.com

• In January 2024, Intel announced its Core Ultra processors featuring integrated AI acceleration engines designed specifically for next-generation AI PCs. The architecture combines CPU, GPU, and NPU cores to support local AI inference tasks while improving energy efficiency and enabling advanced AI productivity applications. Source: www.intel.com

The AI PC Market Report provides a comprehensive analysis of the global ecosystem surrounding artificial intelligence–enabled personal computing platforms. The report evaluates multiple product categories including AI laptops, AI desktops, high-performance AI workstations, and specialized edge AI computing devices equipped with neural processing accelerators capable of exceeding 40 trillion operations per second. It covers key technology components such as AI processors, GPUs, NPUs, high-speed memory architectures, and integrated operating system frameworks designed to support on-device machine learning workloads.

The analysis spans major application areas including enterprise productivity automation, software development, generative AI content creation, data analytics, and advanced research computing environments. More than 10 major end-user sectors are assessed, including finance, healthcare technology, manufacturing, education, and digital media industries that increasingly rely on local AI inference capabilities.

Geographically, the report examines market trends across five primary regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, including insights from over 25 key technology markets worldwide. Additional focus areas include supply chain developments, semiconductor innovation trends, enterprise adoption patterns, and emerging edge computing use cases. The report also evaluates the strategic positioning of over 40 major technology companies participating in the AI PC ecosystem, providing industry professionals with actionable insights for investment planning, technology deployment, and competitive strategy development.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

19.15% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Intel Corporation, Advanced Micro Devices Inc., NVIDIA Corporation, Apple Inc., Lenovo Group Ltd., HP Inc., Dell Technologies Inc., Acer Inc., ASUS Corporation, Samsung Electronics Co. Ltd., Microsoft Corporation, Qualcomm Technologies Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |