Reports

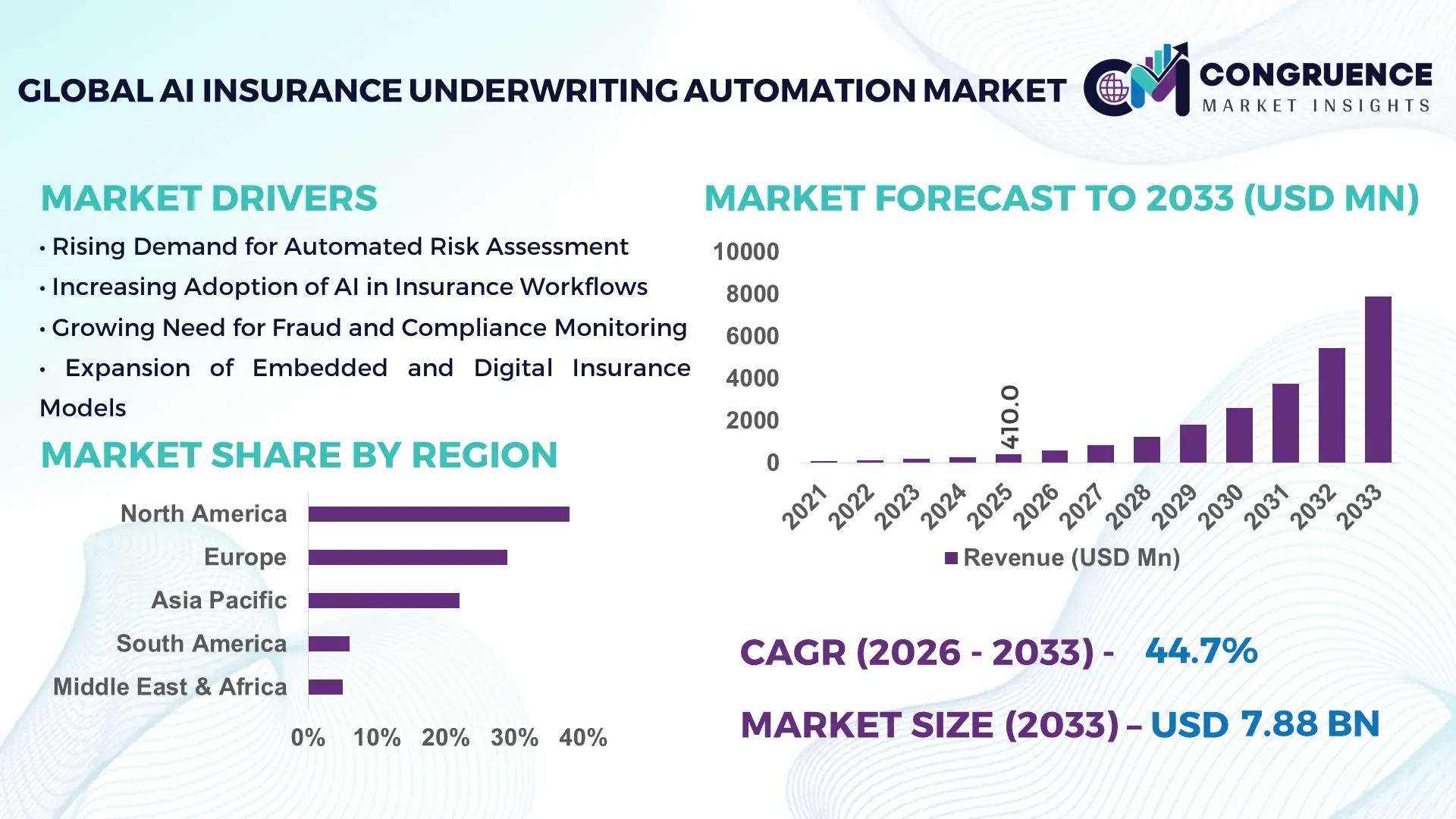

The Global AI Insurance Underwriting Automation Market was valued at USD 410.0 Million in 2025 and is anticipated to reach a value of USD 7,880.1 Million by 2033 expanding at a CAGR of 44.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding rapidly due to accelerating digital transformation across insurance carriers and the growing need to reduce underwriting cycle times while enhancing risk accuracy and regulatory compliance.

The United States dominates the AI Insurance Underwriting Automation Market in terms of technology deployment and investment scale. Over 68% of Tier-1 U.S. insurers have integrated AI-driven underwriting engines into at least one core product line, particularly in property & casualty and life insurance. Annual insurtech investment in the country exceeded USD 8.5 billion in recent funding cycles, with underwriting automation platforms representing a significant share. More than 75% of large U.S. carriers use machine learning–based risk scoring models, and over 60% deploy API-based integrations to connect third-party data providers, reflecting strong production capacity, advanced analytics infrastructure, and high enterprise adoption rates.

Market Size & Growth: Valued at USD 410.0 Million in 2025, projected to reach USD 7,880.1 Million by 2033, expanding at 44.7% CAGR, driven by demand for real-time risk assessment and digital underwriting transformation.

Top Growth Drivers: 70% faster underwriting cycle times, 40% operational cost reduction, 35% improvement in risk prediction accuracy.

Short-Term Forecast: By 2028, AI-driven underwriting platforms are expected to reduce policy issuance time by 50% and manual review dependency by 45%.

Emerging Technologies: Generative AI for automated policy drafting, predictive analytics engines, explainable AI (XAI) for regulatory compliance transparency.

Regional Leaders: North America projected at USD 3,200.0 Million by 2033 with enterprise-wide automation adoption; Europe at USD 2,100.0 Million driven by regulatory-tech integration; Asia-Pacific at USD 1,850.0 Million supported by digital-first insurers.

Consumer/End-User Trends: Over 62% of insurers prioritize straight-through processing; 58% of mid-sized insurers adopt AI to enhance SME underwriting accuracy.

Pilot or Case Example: In 2024, a U.S. Tier-1 insurer achieved 52% reduction in underwriting processing time using AI risk engines.

Competitive Landscape: IBM holds approximately 18% share, followed by Microsoft, Oracle, SAP, and Guidewire Software.

Regulatory & ESG Impact: 65% of insurers are aligning AI governance with responsible AI frameworks; 40% target paperless underwriting workflows by 2027.

Investment & Funding Patterns: Over USD 5.2 billion allocated to AI-focused insurtech funding in recent cycles, emphasizing underwriting automation and predictive analytics platforms.

Innovation & Future Outlook: Integration of real-time IoT data, blockchain-based policy validation, and cloud-native AI underwriting ecosystems is reshaping insurer operating models.

Property & casualty accounts for nearly 48% of AI Insurance Underwriting Automation deployments, followed by life insurance at 32% and health at 20%. Advanced risk-scoring algorithms and generative AI–based documentation tools are improving underwriting productivity by over 40%. Regulatory digitization initiatives across North America and Europe are accelerating AI validation standards, while Asia-Pacific insurers are expanding digital policy issuance capabilities, supporting long-term automation-driven efficiency and compliance optimization.

The AI Insurance Underwriting Automation Market has become strategically central to insurers aiming to enhance underwriting precision, operational agility, and regulatory resilience. AI-based underwriting engines now process structured and unstructured data—including telematics, credit scoring, health records, and IoT streams—reducing manual intervention by up to 60%. Compared to traditional rule-based underwriting systems, machine learning–driven predictive analytics delivers 35% higher risk classification accuracy and up to 50% faster decision-making turnaround.

North America dominates in deployment volume, while Europe leads in responsible AI adoption, with over 72% of large European insurers implementing explainable AI frameworks for compliance alignment. By 2028, generative AI integration into underwriting workflows is expected to cut document preparation and risk summarization time by 45%, enhancing productivity KPIs across mid-sized carriers.

Firms are committing to ESG-aligned digital transformation goals, targeting 40% reduction in paper-based processing and 30% lower operational carbon footprints by 2030 through cloud-native underwriting systems. In 2024, a leading U.S. insurer achieved a 52% efficiency improvement through AI-enabled straight-through processing and automated risk validation.

Strategically, insurers are investing in API ecosystems, cloud migration, and AI governance frameworks to future-proof underwriting models. The AI Insurance Underwriting Automation Market is increasingly positioned as a pillar of resilience, compliance optimization, fraud mitigation, and sustainable growth across global insurance ecosystems.

The AI Insurance Underwriting Automation Market is characterized by rapid digitization, regulatory evolution, and intensifying competition among insurers seeking operational efficiency. The integration of machine learning, natural language processing, and predictive modeling tools is transforming underwriting from manual, experience-based decision-making to data-driven, automated workflows. Insurers are leveraging alternative data sources, including telematics and IoT feeds, to enhance risk visibility. At the same time, regulatory frameworks are mandating explainability and bias mitigation in algorithmic decision systems. Cloud adoption rates exceeding 65% among major insurers are enabling scalable AI deployment, while partnerships with insurtech firms are accelerating innovation cycles. Competitive differentiation increasingly depends on underwriting speed, loss ratio optimization, and digital customer experience enhancement.

The insurance industry is undergoing large-scale digital transformation, with over 75% of global insurers prioritizing automation initiatives within underwriting departments. Manual underwriting processes historically required several days to weeks for policy approval; AI-driven automation reduces this timeframe by up to 70%. Straight-through processing rates have improved by nearly 60% in digitally mature insurers, significantly lowering human error rates. Additionally, predictive risk scoring models analyze thousands of data variables simultaneously, improving underwriting consistency by 35%. Insurers deploying AI-based automation report up to 40% reduction in administrative workload, enabling reallocation of workforce resources toward complex case assessments. Increasing integration of third-party data APIs and real-time analytics platforms further accelerates digital underwriting transformation across property, life, and specialty insurance segments.

Data governance challenges remain a significant restraint in the AI Insurance Underwriting Automation Market. More than 60% of insurers cite compliance complexity related to data protection regulations such as GDPR and regional privacy frameworks. AI models trained on historical datasets risk perpetuating bias, prompting regulatory scrutiny and mandatory explainability audits. Approximately 45% of insurers report delays in AI deployment due to model validation requirements and fairness testing procedures. Additionally, integrating legacy core systems with AI platforms can require extensive IT modernization, with system compatibility issues affecting nearly 38% of digital transformation projects. Concerns regarding cyber risks and sensitive customer data exposure further necessitate robust encryption and monitoring mechanisms, increasing operational complexity and governance oversight.

The rapid growth of embedded insurance within digital ecosystems presents strong opportunities for AI Insurance Underwriting Automation providers. Embedded insurance adoption has increased by over 30% annually in e-commerce and mobility platforms, requiring real-time underwriting decisions within seconds. AI-powered risk engines enable instant policy pricing and approval, supporting high-volume micro-insurance models. Small and medium-sized enterprises (SMEs), representing nearly 90% of global businesses, are increasingly targeted through automated underwriting platforms that simplify risk profiling. Additionally, the integration of IoT data in commercial insurance—covering fleet management and smart property monitoring—improves predictive loss prevention by up to 28%. These developments create scalable, API-driven underwriting ecosystems capable of supporting high-frequency digital transactions.

Integration of AI underwriting systems into legacy insurance infrastructures remains a major challenge. Nearly 50% of established insurers operate on core systems over 10 years old, complicating API-based interoperability and data standardization. Migration to cloud-native AI environments often requires phased deployment strategies, extending implementation timelines by 12–18 months. Furthermore, the shortage of skilled AI and actuarial data scientists affects approximately 42% of insurance firms attempting advanced automation projects. Model interpretability requirements and audit trails add technical layers that increase system design complexity. Operational resistance to change within underwriting departments also slows adoption, as retraining initiatives are necessary to transition from manual evaluation processes to AI-supervised decision frameworks.

60% Increase in Straight-Through Processing Adoption: Insurers adopting AI underwriting platforms report straight-through processing rates exceeding 65%, compared to 30% in traditional systems. Automated decision engines process over 80% of low-risk applications without manual review, reducing underwriting turnaround time by 50% and lowering error rates by 25%.

45% Growth in Generative AI-Based Documentation Automation: Generative AI tools now assist in drafting policy summaries and risk reports, cutting documentation preparation time by 45%. Over 58% of mid-to-large insurers are piloting AI copilots to support underwriting teams, improving productivity metrics by 35%.

30% Expansion in IoT-Integrated Risk Assessment Models: Integration of telematics and IoT sensor data has improved predictive loss accuracy by 28% in auto and commercial property segments. Approximately 40% of commercial insurers now incorporate real-time behavioral or environmental data streams into underwriting algorithms.

50% Reduction in Manual Compliance Reviews Through Explainable AI: Explainable AI frameworks are enabling 50% faster regulatory audit processes. Around 72% of European insurers have embedded model transparency dashboards, enhancing governance visibility and reducing compliance review cycles by 33%.

The AI Insurance Underwriting Automation Market is segmented by type, application, and end-user, reflecting the industry’s structured transformation toward data-driven underwriting models. By type, the market includes rule-based automation systems, machine learning–based underwriting engines, natural language processing (NLP) tools, predictive analytics platforms, and generative AI–enabled underwriting assistants. Machine learning–driven systems account for the highest deployment levels due to their superior risk modeling precision and scalability.

By application, the primary areas include risk assessment & scoring, policy issuance & processing automation, claims-linked underwriting validation, fraud detection, and regulatory compliance monitoring. Risk assessment platforms lead adoption due to insurers’ demand for real-time predictive modeling.

From an end-user perspective, large insurance enterprises dominate deployments, while small and mid-sized insurers increasingly adopt cloud-native AI underwriting solutions to enhance competitiveness. Digital-first insurers and insurtech firms are integrating embedded underwriting capabilities within API ecosystems, reflecting a shift toward scalable, automated, and compliance-driven underwriting frameworks.

The AI Insurance Underwriting Automation Market by type includes machine learning–based underwriting engines, rule-based automation systems, natural language processing (NLP) solutions, predictive analytics platforms, and generative AI underwriting assistants. Machine learning–based underwriting engines currently account for approximately 46% of total adoption due to their ability to process high-dimensional risk variables and improve classification accuracy by over 35%. Rule-based automation systems hold nearly 21%, primarily among traditional insurers modernizing legacy systems. However, generative AI underwriting assistants are the fastest-growing segment, expanding at an estimated CAGR of 48%, driven by demand for automated document drafting, risk summaries, and real-time decision explanations. NLP solutions represent around 18% of deployments, supporting extraction of unstructured data from medical reports and policy documents. Predictive analytics platforms and other niche automation tools collectively account for approximately 15%, serving specialty underwriting lines and commercial risk modeling.

By application, risk assessment & scoring leads the AI Insurance Underwriting Automation Market, accounting for approximately 44% of deployments, as insurers prioritize predictive modeling to improve loss ratio management. Policy issuance & processing automation represents around 27%, enhancing straight-through processing efficiency. Fraud detection & compliance monitoring contribute nearly 17%, leveraging AI anomaly detection capabilities. The remaining 12% includes claims-linked underwriting validation and cross-line risk optimization. While risk assessment remains dominant, policy issuance automation is the fastest-growing application segment, projected to expand at approximately 45% CAGR due to digital onboarding demand and embedded insurance expansion. In 2025, more than 41% of global insurers reported piloting AI-driven underwriting automation tools for customer-facing digital policy platforms. Additionally, over 63% of millennial policyholders indicated preference for insurers offering instant AI-based policy approvals.

Large insurance enterprises dominate the AI Insurance Underwriting Automation Market, representing approximately 58% of total adoption due to higher IT budgets and enterprise-wide digital transformation strategies. Mid-sized insurers account for nearly 26%, increasingly adopting cloud-native underwriting automation platforms to compete with larger incumbents. Digital-first insurers and insurtech firms contribute around 16%, integrating AI-driven underwriting directly into digital ecosystems. Although large enterprises lead adoption, mid-sized insurers represent the fastest-growing end-user segment, expanding at an estimated CAGR of 46%, driven by scalable SaaS-based AI underwriting platforms and API integrations. In 2025, over 39% of mid-sized insurers globally reported implementing AI-based underwriting for at least one major product line. Furthermore, 67% of digital insurers prioritize straight-through underwriting automation to improve customer acquisition rates.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of47% between 2026 and 2033.

Europe followed with a 29% share, while Asia-Pacific held approximately 22%, South America accounted for 6%, and the Middle East & Africa represented nearly 5% of total global adoption in 2025. Over 72% of Tier-1 insurers in North America have implemented AI-driven underwriting modules in at least one core insurance line. In Europe, more than 65% of insurers have adopted explainable AI frameworks to meet compliance mandates. Asia-Pacific has witnessed over 40% year-on-year increase in digital policy issuance volumes, reflecting expanding embedded insurance ecosystems. Across emerging regions, digital onboarding rates exceed 35%, indicating strong potential for automation expansion driven by cloud adoption levels surpassing 60% among insurers globally.

North America holds approximately 38% of the global AI Insurance Underwriting Automation Market share, supported by high enterprise technology spending and early adoption of AI-driven decision engines. Key industries driving demand include property & casualty, life insurance, and commercial risk underwriting, with over 70% of large insurers integrating machine learning into underwriting workflows. Regulatory modernization initiatives encourage algorithmic transparency and responsible AI governance frameworks. Digital transformation trends show more than 68% of insurers leveraging cloud-native underwriting platforms, while API-based integrations with third-party data providers exceed 60% adoption. A notable player, Guidewire Software, has expanded AI-enabled underwriting analytics modules to improve straight-through processing by over 50% for enterprise clients. Consumer behavior reflects strong preference for instant policy issuance, with nearly 64% of policyholders favoring digital-first underwriting experiences, particularly in finance and healthcare-related coverage segments.

Europe represents approximately 29% of the global AI Insurance Underwriting Automation Market. Major markets include Germany, the United Kingdom, and France, collectively contributing over 65% of regional deployments. Strong oversight from regulatory bodies and AI governance frameworks has accelerated demand for explainable AI tools, with nearly 72% of large insurers implementing algorithm transparency dashboards. Sustainability initiatives emphasize paperless underwriting and carbon footprint reduction, with over 45% of insurers targeting digital-only policy documentation by 2027. Adoption of predictive analytics platforms has increased by 33% across commercial insurance lines. A regional technology provider, SAP, has enhanced AI-based insurance modules integrated within enterprise resource planning systems to optimize underwriting data flows. Consumer behavior shows higher demand for compliant and transparent underwriting processes, as regulatory pressure drives insurers to adopt bias-mitigation and fairness-testing mechanisms.

Asia-Pacific accounts for approximately 22% of global market volume and ranks as the fastest-growing regional market. China, India, and Japan are the top consuming countries, collectively representing over 70% of regional demand. Digital-first insurance ecosystems and mobile policy distribution platforms contribute to underwriting automation adoption rates exceeding 48% among urban insurers. Infrastructure digitization and cloud migration initiatives have increased by 40% across insurance enterprises. Innovation hubs in Singapore and Tokyo are advancing AI underwriting pilots that reduce manual risk assessment time by 45%. A prominent regional insurer, Ping An Insurance, utilizes AI-powered risk engines to process millions of underwriting applications annually with significant reductions in manual intervention. Regional consumer behavior shows strong adoption of mobile-based insurance purchases, with over 58% of policyholders preferring app-based policy issuance supported by AI decision engines.

South America holds approximately 6% of the global AI Insurance Underwriting Automation Market share, with Brazil and Argentina serving as primary growth centers. Brazil accounts for nearly 55% of regional adoption, supported by financial sector digitalization initiatives. Infrastructure modernization in banking and insurance ecosystems has driven AI underwriting integration rates above 30% among mid-sized insurers. Government-backed digital transformation incentives encourage API-based financial services connectivity. A leading regional insurer, SulAmérica, has introduced AI-powered underwriting analytics to streamline policy issuance and improve fraud detection accuracy by over 25%. Consumer behavior reflects increasing preference for digital onboarding, with nearly 49% of new insurance buyers opting for automated underwriting channels. Localization and language-based AI processing tools are expanding to address diverse regional markets.

The Middle East & Africa region represents about 5% of the global AI Insurance Underwriting Automation Market. The UAE and South Africa are major growth contributors, collectively accounting for nearly 60% of regional demand. Insurance demand linked to oil & gas, construction, and infrastructure sectors drives automated commercial underwriting adoption. Technological modernization initiatives have increased cloud deployment among insurers to over 52%, enabling scalable AI integration. Regulatory authorities are introducing fintech-friendly policies to encourage digital insurance expansion. A regional insurer, Discovery Limited, has leveraged AI-based behavioral data analytics to enhance underwriting precision and risk segmentation. Consumer behavior indicates rising mobile adoption, with approximately 46% of policy applications submitted through digital platforms, supporting accelerated automation in underwriting workflows.

United States – 34% Market Share: It leads due to high enterprise AI investment, advanced analytics infrastructure, and widespread digital policy issuance adoption.

Germany – 11% Market Share: It is driven by strong regulatory compliance frameworks, enterprise digital transformation programs, and advanced industrial insurance underwriting capabilities.

The AI Insurance Underwriting Automation Market exhibits a moderately fragmented structure, with more than 45 active global and regional technology providers competing across underwriting analytics, machine learning engines, and SaaS-based automation platforms. The top five companies collectively account for approximately 52% of total market share, indicating moderate consolidation at the enterprise tier, while niche insurtech firms capture specialized segments such as embedded insurance underwriting and API-driven risk scoring.

Large enterprise technology vendors focus on end-to-end digital underwriting ecosystems, integrating AI engines with claims, policy administration, and CRM platforms. Over 60% of competitive differentiation is driven by proprietary predictive modeling accuracy and explainable AI capabilities. Strategic partnerships between insurers and AI vendors increased by 38% between 2023 and 2025, particularly for cloud-native deployments and data-sharing ecosystems.

Product innovation cycles have shortened to 12–18 months, with generative AI copilots, automated document extraction, and IoT-integrated underwriting becoming key differentiators. Mergers and acquisitions activity has intensified, with at least 15 insurtech-focused acquisitions recorded in 2024–2025 targeting analytics and underwriting automation specialists. Competitive positioning increasingly depends on scalability, API compatibility, compliance readiness, and enterprise-level cybersecurity resilience, as insurers demand platforms capable of processing over 1 million underwriting transactions per month with minimal latency.

SAP SE

Guidewire Software, Inc.

Salesforce, Inc.

Cognizant Technology Solutions

Accenture plc

Capgemini SE

Tata Consultancy Services (TCS)

Infosys Limited

DXC Technology

Zensar Technologies

Shift Technology

Earnix Ltd.

FICO (Fair Isaac Corporation)

The AI Insurance Underwriting Automation Market is driven by advancements in machine learning, natural language processing (NLP), predictive analytics, and generative AI frameworks. Machine learning algorithms now process more than 10,000 structured and unstructured data variables per policy application, improving underwriting precision by approximately 35% compared to traditional rule-based systems.

Natural language processing tools extract key risk indicators from medical reports, inspection documents, and claims histories with over 90% data extraction accuracy, reducing manual review time by nearly 45%. Generative AI copilots are increasingly deployed to auto-generate policy summaries and risk narratives, decreasing documentation preparation time by up to 50%.

Explainable AI (XAI) frameworks have become critical for regulatory compliance, with more than 70% of large insurers implementing transparency dashboards that visualize algorithmic decision pathways. Cloud-native AI platforms support horizontal scalability, enabling insurers to handle underwriting workloads exceeding 500,000 applications per month.

Emerging technologies such as federated learning allow insurers to train AI models across distributed datasets without compromising data privacy, improving cross-company predictive insights by approximately 20%. Additionally, IoT-driven underwriting integrates telematics and smart property sensors, improving real-time risk assessment accuracy by 28%. Blockchain-enabled smart contracts are being piloted to automate policy validation and audit trails, reducing compliance review times by 30%.

The convergence of API ecosystems, advanced analytics, and secure cloud infrastructure positions AI underwriting platforms as mission-critical digital assets for insurance enterprises.

• In October 2025, OpenText launched new cloud-ready AI content solutions for Guidewire platforms, embedding AI-powered assistance within PolicyCenter, ClaimCenter, and BillingCenter workflows to help insurers automate access to critical underwriting and claims content, reducing search time and improving service outcomes. Source: www.prnewswire.com

• In December 2025, Heritage Insurance Company deployed Guidewire’s Cloud-based PolicyCenter and BillingCenter, modernizing underwriting, policy admin, and billing processes across 13 U.S. states on a scalable cloud platform to streamline core insurance functions and adapt to evolving market conditions. Source: www.guidewire.com

• In September 2025, Guidewire was named a Leader in the 2025 Gartner Magic Quadrant for SaaS P&C Platforms, with its Mammoth release enhancing predictive analytics and underwriting decision support capabilities at the point of decision, reinforcing its leadership in AI-augmented insurance operations. Source: www.guidewire.com

• In October 2025, Earnix served as a Platinum Sponsor at Guidewire Connections 2025, showcasing its Intelligent Decisioning solutions that integrate AI-driven pricing, underwriting, and personalization tools and demonstrating case studies on transforming insurance analytics and decision workflows. Source: www.earnix.com

The AI Insurance Underwriting Automation Market Report provides a comprehensive assessment of technology-driven underwriting transformation across life, property & casualty, health, and specialty insurance segments. The scope includes detailed evaluation of automation types such as machine learning engines, NLP-based document processing systems, predictive analytics platforms, and generative AI underwriting assistants.

The report covers segmentation across applications including risk scoring, policy issuance automation, fraud detection, compliance monitoring, and embedded insurance enablement. It examines enterprise-scale deployments as well as SaaS-based solutions adopted by mid-sized and digital-first insurers. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating country-level insights for over 15 key insurance markets.

Additionally, the report analyzes regulatory technology integration, explainable AI adoption rates exceeding 70% among large insurers, cloud migration trends surpassing 65% enterprise penetration, and IoT-enabled underwriting use cases across commercial and motor insurance lines. Emerging niches such as federated learning, blockchain-enabled policy validation, and API-driven embedded insurance ecosystems are also evaluated.

The scope further includes competitive benchmarking of more than 40 market participants, assessment of digital transformation maturity levels, and evaluation of automation impact on underwriting cycle times, operational efficiency, and compliance optimization—providing strategic insights tailored for executives, insurers, technology providers, and institutional investors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 410.0 Million |

| Market Revenue (2033) | USD 7,880.1 Million |

| CAGR (2026–2033) | 44.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM Corporation; Microsoft Corporation; Oracle Corporation; SAP SE; Guidewire Software, Inc.; Salesforce, Inc.; Accenture plc; Capgemini SE; Tata Consultancy Services; Infosys Limited; DXC Technology; Shift Technology; Earnix Ltd.; FICO |

| Customization & Pricing | Available on Request (10% Customization Free) |