Reports

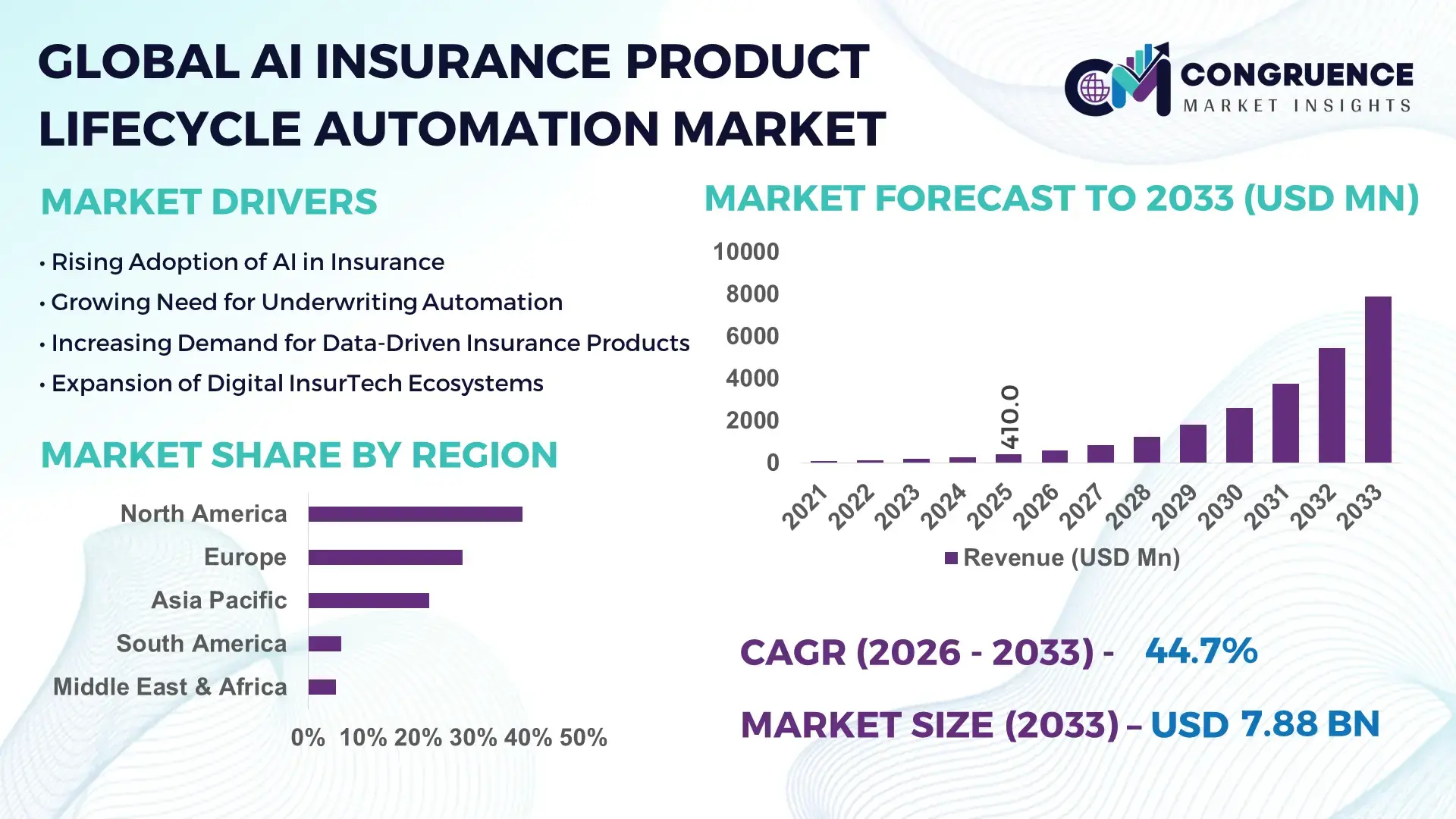

The Global AI Insurance Product Lifecycle Automation Market was valued at USD 410.0 Million in 2025 and is anticipated to reach a value of USD 7,880.1 Million by 2033 expanding at a CAGR of 44.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is largely attributed to the rising adoption of artificial intelligence to accelerate insurance product design, automate underwriting workflows, and reduce policy administration costs across digital insurance ecosystems.

The United States currently leads the AI Insurance Product Lifecycle Automation ecosystem through strong investment flows, digital insurance infrastructure, and advanced enterprise AI deployment across the insurance sector. The U.S. hosts more than 2,800 InsurTech startups, many specializing in AI-driven policy lifecycle management, underwriting automation, and product analytics. In 2025, over 68% of large U.S. insurers reported using AI-based automation tools for product development and lifecycle management processes. Major insurers such as Allstate, Progressive, and MetLife have expanded AI-driven underwriting and policy design frameworks capable of processing over 500,000 automated policy evaluations daily. Additionally, U.S. InsurTech venture funding exceeded USD 7.5 billion in 2024, with nearly 35% allocated to AI-enabled automation platforms supporting insurance product design, regulatory compliance automation, and lifecycle analytics tools used across life, health, and property insurance sectors.

Market Size & Growth: The market reached USD 410.0 million in 2025 and is projected to reach USD 7,880.1 million by 2033, expanding at a 44.7% CAGR as insurers deploy AI to accelerate product design cycles and reduce manual policy management tasks.

Top Growth Drivers: Automation adoption across insurers exceeds 63%, AI-enabled underwriting improves risk assessment accuracy by 35%, and product development cycle time is reduced by 40% through AI-driven analytics platforms.

Short-Term Forecast: By 2028, AI insurance lifecycle automation tools are expected to reduce policy administration costs by 30% while improving product launch timelines by 25% across global insurers.

Emerging Technologies: Generative AI for policy design, explainable AI underwriting engines, and low-code AI insurance workflow platforms are becoming core technological trends supporting insurance product lifecycle automation.

Regional Leaders: North America is projected to exceed USD 3.2 billion by 2033 driven by InsurTech innovation; Europe may reach USD 2.1 billion with strong regulatory AI adoption; Asia-Pacific is expected to surpass USD 1.9 billion due to rapid digital insurance penetration.

Consumer/End-User Trends: More than 55% of insurers globally are integrating AI-powered lifecycle tools to automate underwriting, product testing, and compliance workflows, particularly across life and property insurance segments.

Pilot or Case Example: In 2024, a European digital insurer deployed an AI lifecycle automation platform that reduced policy product launch time by 42% and improved underwriting accuracy by 28%.

Competitive Landscape: The market remains moderately concentrated, with IBM holding approximately 18% share, followed by major technology providers including Microsoft, Oracle, Accenture, and SAP.

Regulatory & ESG Impact: Over 40% of global insurers are integrating responsible AI governance frameworks to comply with emerging AI regulations and ensure transparent underwriting decisions.

Investment & Funding Patterns: Global InsurTech and AI insurance automation platforms attracted over USD 10 billion in investments between 2023–2025, with growing venture capital support for AI underwriting and product lifecycle management platforms.

Innovation & Future Outlook: AI-driven digital insurance platforms, predictive product design engines, and autonomous underwriting systems are expected to reshape insurance product development pipelines over the next decade.

AI Insurance Product Lifecycle Automation platforms are increasingly used across life insurance, health insurance, and property & casualty segments, which collectively account for nearly 70% of enterprise deployments. Emerging innovations such as generative AI policy modeling, automated regulatory compliance engines, and predictive underwriting analytics are reshaping product lifecycle workflows. Rising regulatory digitalization across Europe and North America, combined with strong insurance digitization across Asia-Pacific, is accelerating adoption among global insurers seeking faster product innovation cycles and improved operational efficiency.

The AI Insurance Product Lifecycle Automation Market is becoming strategically critical for insurers seeking operational efficiency, faster product innovation, and regulatory compliance across increasingly complex digital insurance ecosystems. Traditional insurance product development processes often require 12–18 months for product launch, while AI-driven lifecycle automation platforms are reducing this timeline by integrating predictive analytics, automated underwriting models, and AI-powered compliance monitoring tools across policy design, pricing, distribution, and lifecycle management stages.

Advanced technologies such as generative AI and machine learning underwriting engines are enabling insurers to process large-scale risk datasets and automate product testing cycles. For instance, generative AI-driven product design frameworks deliver nearly 35% faster product modeling compared to traditional actuarial analysis methods, significantly improving speed-to-market for insurers launching new insurance products. These systems can analyze millions of policyholder data points, enabling insurers to dynamically adjust policy pricing and features based on evolving customer behavior and risk models.

Regional dynamics further highlight strategic positioning within the market. North America dominates in deployment volume, driven by its strong InsurTech ecosystem and enterprise AI adoption. Meanwhile, Europe leads in regulatory-driven adoption with nearly 52% of insurance enterprises integrating AI governance frameworks to ensure transparent underwriting and compliance with emerging digital regulations. Asia-Pacific markets, particularly Japan, South Korea, and Singapore, are rapidly implementing AI-driven lifecycle automation to support digital insurance platforms.

Short-term projections indicate strong technological integration. By 2028, AI-driven lifecycle automation platforms are expected to improve underwriting efficiency by nearly 40% and reduce operational costs by approximately 25% through automated product lifecycle management workflows. Additionally, insurers are aligning AI strategies with environmental, social, and governance (ESG) commitments. Many insurance firms are committing to reducing operational data processing energy consumption by 20% by 2030 through optimized AI infrastructure and cloud-based automation systems.

A practical example illustrates the impact of this technology. In 2024, a major U.S. insurer implemented AI-powered lifecycle automation for product development, achieving a 33% reduction in underwriting processing time and a 27% improvement in policy lifecycle analytics accuracy through integrated AI decision-support systems.

Looking ahead, the AI Insurance Product Lifecycle Automation Market is expected to become a central pillar of digital insurance transformation. As insurers continue integrating AI-driven analytics, automated product design, and intelligent regulatory compliance frameworks, the market will play a crucial role in enabling resilient, compliant, and sustainable insurance ecosystems worldwide.

The AI Insurance Product Lifecycle Automation Market is experiencing rapid evolution as insurers adopt advanced automation technologies to improve operational efficiency, accelerate product development cycles, and enhance customer experience across digital insurance platforms. AI-powered lifecycle automation platforms integrate data analytics, predictive modeling, natural language processing, and machine learning to streamline the complete insurance product lifecycle—from product ideation and underwriting to policy management and renewal optimization.

Digital transformation across the insurance sector is significantly influencing market dynamics. Global insurers are increasingly prioritizing automation to reduce manual underwriting processes and improve data-driven decision-making. AI-enabled lifecycle platforms can analyze large volumes of structured and unstructured data, enabling insurers to design more personalized insurance products while maintaining compliance with evolving regulatory frameworks. Additionally, increasing investments in InsurTech ecosystems, cloud-based AI platforms, and digital insurance distribution channels are further strengthening the market landscape.

The growing complexity of risk modeling and regulatory compliance requirements is also driving adoption. AI-based automation tools enable insurers to integrate compliance validation within product lifecycle workflows, improving operational transparency and reducing policy development risks. As digital insurance platforms expand globally, lifecycle automation technologies are becoming essential for insurers seeking scalable product development, faster policy approvals, and advanced analytics-driven market insights.

Insurance companies worldwide are under increasing pressure to accelerate product innovation while managing complex underwriting processes. AI-powered lifecycle automation systems are enabling insurers to automate risk assessment, product testing, and policy approval processes with significantly higher efficiency. Traditional underwriting methods often require extensive manual evaluation of risk factors, whereas AI-driven systems can analyze thousands of customer profiles and historical claims datasets in seconds. More than 60% of global insurers have already integrated some form of AI-powered underwriting automation, enabling faster product development and improved risk modeling accuracy. These technologies allow insurers to create highly customized insurance products for different customer segments, including usage-based insurance and micro-insurance solutions. AI lifecycle automation also reduces operational bottlenecks by automating repetitive tasks such as compliance verification, documentation validation, and pricing model simulations. As insurance companies continue expanding digital channels and customer-centric products, demand for AI-based lifecycle automation platforms is expected to intensify across the industry.

Despite strong adoption momentum, data privacy and regulatory compliance challenges remain major restraints for the AI Insurance Product Lifecycle Automation Market. Insurance companies process highly sensitive personal and financial data, including health records, income details, and risk assessment information. The integration of AI-driven lifecycle platforms requires secure data pipelines and strict compliance with regional data protection laws. Across major markets such as Europe and North America, regulatory frameworks impose strict guidelines on automated decision-making and data transparency. Many insurers must implement explainable AI systems to ensure that automated underwriting decisions can be audited and justified. Additionally, legacy insurance IT infrastructure in many companies makes it difficult to integrate modern AI automation platforms without extensive system upgrades. Concerns about algorithmic bias in underwriting models and compliance risks associated with automated policy decisions further slow adoption among conservative insurance institutions.

The global shift toward digital insurance ecosystems presents substantial opportunities for AI lifecycle automation platforms. Increasing adoption of online insurance marketplaces, mobile-based insurance services, and embedded insurance solutions is creating demand for automation tools capable of managing dynamic product lifecycles. AI-powered automation enables insurers to rapidly design and launch new insurance products tailored to emerging risks such as cyber threats, climate-related events, and gig economy employment models. In addition, insurers are leveraging AI lifecycle platforms to analyze behavioral and transactional data, enabling personalized policy pricing and dynamic risk assessment models. The rise of InsurTech partnerships is further accelerating innovation in this space. Technology providers and insurance companies are collaborating to build AI-driven product design platforms capable of integrating predictive analytics, compliance automation, and real-time risk modeling. As digital insurance distribution continues expanding globally, these platforms will play a critical role in supporting scalable product innovation strategies.

One of the major challenges affecting the AI Insurance Product Lifecycle Automation Market is the complexity of integrating AI-driven automation platforms into existing insurance technology ecosystems. Many insurers continue to operate legacy core systems designed decades ago, which lack compatibility with modern AI-based analytics and automation frameworks. Upgrading these systems often requires significant investment, system restructuring, and operational disruption. Another challenge is the shortage of skilled professionals capable of managing advanced AI insurance automation systems. Successful deployment requires expertise in data science, actuarial modeling, AI ethics, regulatory compliance, and digital product development. Many insurance companies face difficulties recruiting and retaining professionals with these specialized skill sets. Furthermore, organizational resistance to automation and concerns regarding workforce displacement may slow adoption in some traditional insurance markets.

Rapid Growth of AI-Driven Underwriting Automation: AI-powered underwriting systems are increasingly integrated into insurance product lifecycle automation platforms. More than 62% of global insurers now deploy automated underwriting tools, enabling risk assessments to be completed in less than 5 minutes compared to traditional processing times of 24–48 hours. These systems process thousands of variables simultaneously, improving risk evaluation accuracy by nearly 30% while reducing manual underwriting workloads across insurance operations.

Expansion of Generative AI in Insurance Product Design: Generative AI is transforming the way insurers design new insurance products and pricing models. Nearly 48% of large insurance companies are experimenting with generative AI tools to simulate product features, pricing structures, and regulatory compliance checks. Early adopters report 35% faster product development cycles and the ability to analyze over 1 million risk scenarios simultaneously, improving policy innovation and customer targeting capabilities.

Integration of Cloud-Based Lifecycle Automation Platforms: Cloud-native AI platforms are becoming the backbone of insurance lifecycle automation systems. Approximately 58% of insurers have migrated key product lifecycle management processes to cloud environments, enabling real-time data analytics and cross-department collaboration. Cloud automation tools can process over 2 million policy lifecycle transactions per day, enabling insurers to scale product operations across global markets while maintaining regulatory oversight.

Growth of Embedded Insurance and Digital Distribution Channels: The emergence of embedded insurance ecosystems is increasing demand for automated lifecycle management solutions. Digital commerce platforms and fintech ecosystems now integrate insurance products directly into consumer transactions, with embedded insurance adoption rising by over 40% in the last three years. AI lifecycle automation platforms support this model by enabling insurers to create and launch customized insurance products within weeks rather than months, supporting rapid expansion across digital distribution channels.

The AI Insurance Product Lifecycle Automation Market is segmented based on type, application, and end-user categories, reflecting the diverse operational requirements across insurance ecosystems. Different automation technologies address specific stages of the insurance product lifecycle including product design, underwriting, pricing, compliance management, and policy administration. AI-driven platforms are increasingly designed as modular solutions, allowing insurers to integrate automation capabilities within existing IT infrastructures while maintaining regulatory compliance and operational scalability.

Across the market, adoption varies depending on operational priorities. Large insurers tend to deploy end-to-end lifecycle automation platforms covering product design, underwriting, and policy management, while smaller insurance firms focus on specific automation modules such as underwriting analytics or regulatory compliance monitoring. Applications range from product development and risk modeling to automated policy servicing and customer analytics. End-user adoption is led by large insurance carriers, though digital insurers and InsurTech startups are rapidly expanding deployment across cloud-based AI lifecycle automation ecosystems.

AI Insurance Product Lifecycle Automation platforms are categorized into several technology types including underwriting automation platforms, product design and pricing automation tools, policy lifecycle management platforms, regulatory compliance automation systems, and AI analytics platforms. Among these, underwriting automation platforms dominate the segment with approximately 36% adoption share, largely because risk evaluation and policy approval processes represent some of the most resource-intensive operations in insurance companies. These platforms utilize machine learning models to analyze large risk datasets, enabling insurers to automate underwriting decisions with improved accuracy and speed. Product design and pricing automation tools represent the fastest-growing segment with an estimated growth rate of about 46%, as insurers increasingly deploy predictive analytics to design customized insurance products and pricing strategies. These solutions allow insurers to simulate thousands of risk scenarios, improving product innovation and reducing time required for regulatory approval processes. Policy lifecycle management systems and regulatory compliance automation platforms together account for nearly 39% of the remaining market, providing automated documentation management, compliance tracking, and policy administration capabilities. AI analytics platforms also support insurers by delivering predictive insights for product lifecycle performance and customer engagement.

• In 2025, several major insurers implemented AI underwriting automation capable of processing more than 300,000 policy risk assessments daily, significantly improving underwriting efficiency and reducing manual review workloads.

AI Insurance Product Lifecycle Automation technologies are widely applied across insurance product development, underwriting and risk assessment, regulatory compliance management, policy administration, and customer analytics. Among these applications, underwriting and risk assessment currently account for nearly 34% of total adoption, as insurers prioritize automating complex risk evaluation workflows. AI-driven underwriting models analyze large volumes of historical claims data and customer information, enabling insurers to produce highly accurate policy risk profiles while reducing human intervention. Insurance product development is the fastest-growing application segment with an estimated growth rate of approximately 45%, supported by the increasing use of predictive analytics and generative AI models in product design and pricing optimization. These technologies allow insurers to rapidly prototype new insurance offerings tailored to emerging risks such as cyber threats and climate-related events. Policy administration and regulatory compliance automation collectively represent around 41% of the remaining market, ensuring efficient policy management and compliance verification across insurance operations. In 2025, nearly 38% of global insurers reported piloting AI-driven lifecycle automation platforms to enhance customer experience and digital policy servicing capabilities. Additionally, more than 52% of insurance enterprises are integrating AI analytics into underwriting workflows to improve operational decision-making and risk forecasting.

• In 2024, a national insurance regulator implemented AI-based compliance monitoring tools across multiple insurers, enabling automated verification of policy design and regulatory standards for over 5 million insurance policies.

The primary end-users of AI Insurance Product Lifecycle Automation solutions include large insurance carriers, small and medium-sized insurers, digital insurers, InsurTech companies, and insurance brokers or intermediaries. Large insurance carriers dominate the segment with approximately 44% adoption share, primarily due to their extensive product portfolios and complex operational structures requiring automated lifecycle management solutions. These organizations deploy AI-driven automation tools to streamline underwriting, accelerate product development cycles, and improve policy management efficiency across global operations. Digital insurers represent the fastest-growing end-user segment with an estimated growth rate of about 48%, driven by their cloud-native technology infrastructure and reliance on AI-driven automation for real-time product design and customer engagement. These companies leverage AI lifecycle platforms to develop highly personalized insurance offerings and optimize digital policy servicing operations. InsurTech startups and small-to-medium insurance firms collectively contribute nearly 39% of the remaining market, focusing primarily on modular automation tools for underwriting, pricing analytics, and compliance management. In 2025, over 42% of insurance enterprises globally reported testing AI lifecycle automation platforms to improve product innovation and regulatory compliance capabilities. Furthermore, nearly 60% of digital insurers rely on AI-driven analytics tools for automated policy lifecycle management and customer behavior analysis.

• In 2025, an international insurance technology consortium launched a collaborative AI automation platform enabling over 120 insurers to automate product lifecycle management workflows and share anonymized risk analytics data.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 47.2% between 2026 and 2033.

The global AI Insurance Product Lifecycle Automation Market shows clear regional variations in adoption, technology investment, and regulatory readiness. North America remains the largest market due to high enterprise AI adoption, strong InsurTech ecosystems, and large-scale digital insurance infrastructure. The region hosts over 1,200 InsurTech companies, with approximately 70% of large insurers deploying AI-driven underwriting automation tools. Europe represents around 28% of the market, driven by regulatory initiatives requiring transparent and explainable AI models in insurance underwriting and policy development. Asia-Pacific currently holds nearly 22% of the market but is witnessing rapid digital insurance expansion across China, Japan, and India. More than 400 digital insurers operate across Asia-Pacific, supporting the adoption of AI lifecycle automation platforms. South America accounts for approximately 6% of global deployments, with Brazil leading adoption across digital insurance platforms. The Middle East & Africa collectively contribute about 5% of the market, supported by government-led digital transformation initiatives and the rapid modernization of financial services infrastructure.

North America dominates the AI Insurance Product Lifecycle Automation Market with approximately 39% global market share, driven by rapid digital transformation in the insurance sector and strong InsurTech innovation ecosystems. The United States and Canada host more than 2,800 InsurTech companies, with nearly 65% of large insurance carriers implementing AI-based lifecycle automation tools to accelerate product development, underwriting, and policy management operations. Key industries driving demand include life insurance, property & casualty insurance, and digital insurance platforms. Regulatory developments such as AI governance frameworks and responsible AI standards are influencing adoption, requiring insurers to integrate explainable AI systems in underwriting workflows. Technological advancements such as generative AI for policy design, predictive risk modeling, and cloud-based lifecycle automation platforms are reshaping operational efficiency. One example is IBM, which has expanded AI-driven insurance automation platforms capable of processing millions of underwriting decisions annually through integrated analytics and workflow automation systems. Regional consumer behavior also supports adoption, with enterprises in finance and healthcare sectors demonstrating high AI automation usage, enabling insurers to develop highly customized policy products for digital consumers.

Europe represents approximately 28% of the global AI Insurance Product Lifecycle Automation Market, supported by strong regulatory frameworks and a mature insurance industry. Key European markets include Germany, the United Kingdom, and France, which collectively account for nearly 65% of regional insurance technology investments. Regulatory institutions across the region are promoting responsible AI adoption through strict governance frameworks that require transparent underwriting algorithms and ethical AI practices. Insurance companies across Europe are increasingly integrating advanced analytics and explainable AI models to comply with these regulations. Technological adoption includes predictive risk analytics, digital policy lifecycle management systems, and automated regulatory compliance platforms. Local players such as SAP are actively developing AI-enabled insurance workflow automation platforms designed to streamline underwriting and product lifecycle processes for European insurers. Regional consumer behavior also plays a role in adoption trends, as regulatory pressure and data protection laws encourage insurers to implement transparent AI models, driving demand for explainable AI solutions within insurance product lifecycle automation platforms.

Asia-Pacific ranks as the fastest-growing region in the AI Insurance Product Lifecycle Automation Market, with strong expansion across digital insurance ecosystems and mobile-first insurance platforms. The region accounts for nearly 22% of global adoption volume, with leading markets including China, Japan, and India. China alone hosts more than 300 InsurTech startups, many developing AI-driven underwriting and policy lifecycle automation tools for digital insurers. Infrastructure development across financial technology sectors and rapid expansion of mobile insurance platforms are fueling demand for automation technologies. Innovation hubs such as Singapore, Shenzhen, and Bangalore are supporting the development of AI-powered insurance technologies through government-backed fintech initiatives and technology accelerators. Companies such as Ping An Technology have implemented AI-driven insurance automation systems capable of processing over 200 million insurance service requests annually. Regional consumer behavior further supports growth, as Asia-Pacific consumers increasingly rely on mobile applications and digital financial services, accelerating demand for automated insurance product lifecycle platforms.

South America represents roughly 6% of the global AI Insurance Product Lifecycle Automation Market, with key markets including Brazil and Argentina driving adoption. Brazil accounts for nearly 60% of the regional insurance technology ecosystem, supported by digital financial infrastructure expansion and growing InsurTech startup activity. Governments across the region are introducing fintech-friendly regulations and digital banking initiatives that encourage automation within financial services, including insurance. Key industries driving adoption include life insurance, agricultural insurance, and property insurance sectors, which require advanced analytics for risk assessment and policy lifecycle management. Local InsurTech players such as Thinkseg are developing AI-based insurance platforms designed to automate product development and underwriting workflows for digital insurers. Consumer behavior in South America is increasingly influenced by mobile-first financial services, with over 65% of insurance customers using digital platforms to access policy services, accelerating the demand for automated lifecycle management technologies.

The Middle East & Africa region accounts for approximately 5% of global adoption in the AI Insurance Product Lifecycle Automation Market, with significant growth observed in the United Arab Emirates and South Africa. Regional demand is largely driven by digital transformation programs within financial services and the modernization of insurance infrastructure across emerging markets. The insurance sector in the UAE is increasingly adopting AI-based automation platforms to improve underwriting efficiency and accelerate product development. Industries such as energy, construction, and logistics insurance are driving demand for advanced risk modeling and automated lifecycle management systems. Technology modernization initiatives are supported by government-backed digital economy programs and fintech innovation hubs across the region. For example, Dubai International Financial Centre has launched several InsurTech accelerators supporting AI-driven insurance automation startups. Regional consumer behavior shows increasing reliance on digital insurance services, with over 50% of urban consumers preferring online policy management platforms, encouraging insurers to implement automated lifecycle management technologies.

United States – 34% market share: Lt leads due to its large InsurTech ecosystem, strong enterprise AI adoption across insurance carriers, and high digital insurance penetration.

China – 17% market share: It holds a major position, driven by rapid digital insurance growth, strong fintech innovation hubs, and large-scale deployment of AI-driven insurance service platforms.

The AI Insurance Product Lifecycle Automation Market features a competitive landscape characterized by both established technology providers and specialized InsurTech innovators. The market currently includes over 120 active solution providers globally, offering a wide range of AI-powered automation platforms covering underwriting, policy lifecycle management, compliance monitoring, and predictive analytics for insurance product development. The market structure is considered moderately fragmented, with the top five companies accounting for approximately 42% of global market presence through enterprise AI solutions and large-scale digital insurance platform integrations.

Major technology firms such as IBM, Microsoft, Oracle, and SAP have developed integrated AI platforms capable of automating multiple stages of the insurance product lifecycle. These platforms combine machine learning algorithms, cloud computing infrastructure, and advanced analytics to support underwriting automation and product development workflows. Strategic collaborations between technology vendors and insurance companies are also increasing. Over 60% of global insurers are currently partnering with InsurTech startups to integrate AI automation solutions into their operational systems.

Innovation remains a central competitive factor within the market. Companies are focusing on developing generative AI-powered product design systems, automated compliance engines, and predictive analytics platforms capable of analyzing millions of policy data points in real time. Mergers, acquisitions, and technology partnerships are also shaping the competitive environment, with several large technology firms acquiring specialized AI startups to expand their insurance automation capabilities. As insurers accelerate digital transformation initiatives, competition is expected to intensify around scalable AI platforms, regulatory compliance capabilities, and advanced risk analytics technologies.

Microsoft

Oracle

SAP

Accenture

Pegasystems

Guidewire Software

Cognizant

TCS (Tata Consultancy Services)

Infosys

Capgemini

Salesforce

FICO

SAS Institute

Wipro

DXC Technology

Technology innovation plays a central role in shaping the AI Insurance Product Lifecycle Automation Market, as insurers increasingly rely on advanced analytics and intelligent automation systems to streamline policy development, underwriting, and lifecycle management processes. AI-driven platforms combine multiple technologies including machine learning, natural language processing, generative AI, robotic process automation (RPA), and predictive analytics to automate various stages of the insurance product lifecycle.

Machine learning algorithms are widely used for risk modeling and underwriting automation. These systems analyze vast volumes of historical claims data, behavioral datasets, and financial information to generate highly accurate risk predictions. Advanced underwriting automation engines can evaluate over 10,000 data variables within seconds, significantly improving underwriting accuracy and operational efficiency. Natural language processing technologies are also being integrated into insurance automation platforms to analyze policy documents, regulatory requirements, and customer communications, enabling insurers to automate compliance verification and document processing workflows.

Generative AI represents one of the most transformative technological trends within the market. Generative AI models are capable of simulating insurance product designs, pricing strategies, and risk scenarios based on large-scale actuarial and customer datasets. Early deployments demonstrate that generative AI tools can generate thousands of policy configuration models within minutes, accelerating insurance product development cycles and enabling insurers to launch highly customized products tailored to specific customer segments.

Cloud computing infrastructure further enhances the scalability of AI lifecycle automation platforms. More than 55% of insurers are migrating insurance product lifecycle management systems to cloud-based platforms, allowing real-time analytics and cross-department collaboration across global insurance operations. Robotic process automation is also widely used to automate repetitive tasks such as policy documentation, compliance checks, and underwriting verification processes. Many AI-enabled automation platforms can now process over 2 million policy lifecycle transactions daily, supporting the growing demand for digital insurance services worldwide.

• In December 2025, Guidewire introduced new AI-driven capabilities within its cloud platform, including an Underwriting Assistant that helps insurers convert complex submissions into underwriting decisions by automatically extracting information, enriching risk data, and performing clearance checks. The feature is designed to accelerate underwriting workflows and reduce manual intake processing across insurance operations. Source: www.guidewire.com

• In July 2025, Microsoft highlighted multiple enterprise deployments of its AI platforms where organizations used Azure AI and generative AI capabilities to automate business processes and accelerate product innovation, enabling insurers and financial institutions to streamline operations, reduce manual workflows, and enhance decision-making across digital insurance systems.

• In September 2024, Accenture announced a collaboration with F&G Annuities & Life to enhance its technology architecture using Accenture Life Insurance Platform (ALIP)—a cloud-native digital insurance platform designed to support underwriting, policy administration, and product lifecycle management with advanced data analytics capabilities.

• In March 2024, Accenture partnered with Amazon Web Services and Anthropic to help enterprises—including companies in highly regulated industries such as insurance—deploy custom generative AI solutions using Anthropic models through Amazon Bedrock, enabling organizations to accelerate AI adoption for analytics, document generation, and operational automation.

The AI Insurance Product Lifecycle Automation Market Report provides a comprehensive analysis of the technologies, industry participants, and operational trends shaping the adoption of AI-driven automation platforms across the global insurance industry. The report evaluates the full lifecycle of insurance product development and management, covering stages such as product ideation, risk modeling, underwriting automation, regulatory compliance verification, policy administration, and renewal optimization.

The scope of the report includes detailed segmentation across technology types, application areas, and end-user categories. Technology segments include underwriting automation platforms, AI-powered product design systems, compliance automation solutions, predictive analytics tools, and policy lifecycle management platforms. Application analysis covers major operational areas such as insurance product development, risk assessment, compliance management, policy administration, and customer analytics, highlighting how automation technologies are transforming traditional insurance workflows.

The report also evaluates adoption patterns across key end-user segments including large insurance carriers, digital insurers, InsurTech companies, and insurance intermediaries. Regional analysis covers major markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with insights into regional adoption patterns, digital transformation initiatives, and insurance technology infrastructure development.

Additionally, the report analyzes emerging technological innovations shaping the market, including generative AI, explainable AI underwriting models, cloud-based lifecycle automation platforms, and robotic process automation tools. More than 120 technology vendors and InsurTech companies are actively developing solutions within this market ecosystem, supporting digital insurance transformation initiatives worldwide. The report also explores evolving regulatory frameworks, enterprise AI governance standards, and strategic partnerships between insurers and technology providers that are accelerating adoption of automation platforms across global insurance operations.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 410.0 Million |

| Market Revenue (2033) | USD 7,880.1 Million |

| CAGR (2026–2033) | 44.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM Corporation; Microsoft Corporation; Oracle Corporation; SAP SE; Accenture Plc; Pegasystems Inc.; Guidewire Software Inc.; Cognizant Technology Solutions; Tata Consultancy Services (TCS); Infosys Limited; Capgemini SE; Salesforce Inc.; FICO; SAS Institute Inc.; Wipro Limited; DXC Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |