Reports

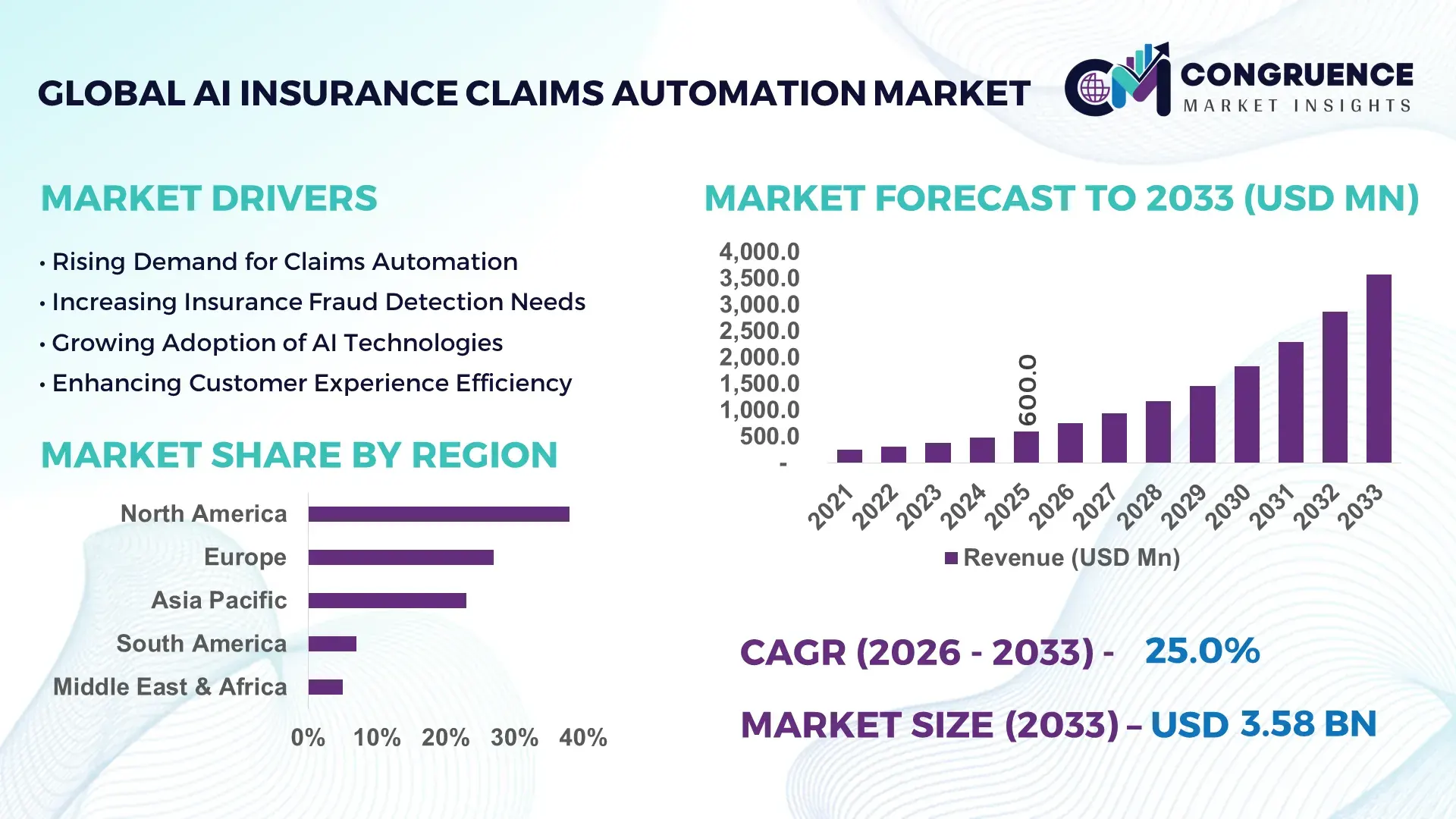

The Global AI Insurance Claims Automation Market was valued at USD 600.0 Million in 2025 and is anticipated to reach a value of USD 3,576.3 Million by 2033 expanding at a CAGR of 25.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. Increasing demand for faster claims settlement and fraud detection is accelerating market adoption.

The United States leads the AI Insurance Claims Automation Market with strong deployment across large insurers and digital-first platforms. Over 72% of tier-1 insurers in the U.S. have integrated AI-based claims processing systems, with automated claims handling reducing processing time by up to 60%. Annual investments in insurance AI technologies exceeded USD 4.5 billion in 2025, driven by use cases in fraud detection, document processing, and predictive analytics. AI-driven claims automation is widely adopted across health, property, and auto insurance segments, with auto insurance alone accounting for nearly 38% of AI-driven claims implementations. Additionally, over 65% of consumers in the U.S. prefer digital-first claim submissions, reinforcing enterprise investments in intelligent claims platforms and cloud-based automation systems.

Market Size & Growth: USD 600.0 Million in 2025, projected USD 3,576.3 Million by 2033, CAGR of 25.0%, driven by automation in claims lifecycle and fraud detection.

Top Growth Drivers: AI adoption rate at 68%, claims processing efficiency improved by 55%, fraud detection accuracy increased by 47%.

Short-Term Forecast: By 2028, claims processing costs expected to decline by 35% with AI integration.

Emerging Technologies: NLP-based document processing, computer vision for damage assessment, predictive analytics for risk scoring.

Regional Leaders: North America USD 1,420 Million by 2033 (high enterprise AI adoption), Europe USD 980 Million (regulatory-driven AI adoption), Asia-Pacific USD 820 Million (rapid digital insurance growth).

Consumer/End-User Trends: Over 62% of policyholders prefer automated claims with real-time updates and digital interfaces.

Pilot or Case Example: In 2025, a leading insurer implemented AI automation achieving 50% faster claims resolution and 30% cost savings.

Competitive Landscape: Market leader holds ~18% share followed by IBM, Accenture, Cognizant, Capgemini, and Pegasystems.

Regulatory & ESG Impact: Over 40% of insurers are aligning AI deployments with data privacy regulations and ESG transparency standards.

Investment & Funding Patterns: AI insurance tech investments crossed USD 6.2 billion globally in 2024–2025 with increased venture funding.

Innovation & Future Outlook: Integration of generative AI and real-time analytics expected to transform claims decision-making and automation workflows.

AI Insurance Claims Automation Market is shaped by strong contributions from auto (38%), health (29%), and property insurance (21%) segments. AI-powered fraud detection tools now identify up to 45% more suspicious claims. Regulatory frameworks such as data privacy compliance are influencing adoption across Europe and North America. Cloud-based deployment accounts for over 58% of implementations, while emerging trends include real-time claims adjudication and conversational AI-driven claims interfaces.

The AI Insurance Claims Automation Market is strategically positioned as a core enabler of operational efficiency, risk mitigation, and enhanced customer experience across the global insurance industry. Insurers are increasingly leveraging artificial intelligence to streamline end-to-end claims processing, reduce manual intervention, and improve decision accuracy. AI-driven claims systems have demonstrated up to 55% improvement in operational efficiency compared to traditional rule-based processing systems, making them a critical investment area for insurers aiming to scale operations while controlling costs.

From a comparative benchmark perspective, AI-powered claims automation platforms deliver nearly 60% faster claim resolution compared to legacy manual workflows, significantly improving customer satisfaction and retention rates. North America dominates in volume due to the presence of large insurers and high technology investments, while Europe leads in adoption with over 70% of insurance enterprises implementing AI-driven compliance and claims automation solutions.

In the short term, by 2028, the integration of generative AI and advanced analytics is expected to reduce claims processing errors by approximately 40%, enhancing accuracy and reducing fraud-related losses. Additionally, ESG considerations are influencing strategic priorities, with insurers committing to reducing paper-based processes by over 50% by 2030 through digital claims ecosystems.

A micro-scenario highlights that in 2025, a U.S.-based insurer achieved a 48% reduction in claims processing time through AI-powered document recognition and predictive analytics integration. This demonstrates the tangible benefits of AI adoption in real-world settings.

Looking ahead, the AI Insurance Claims Automation Market is expected to evolve as a critical pillar supporting resilience, regulatory compliance, and sustainable growth, driven by continuous innovation in AI technologies and increasing demand for digital-first insurance services.

The AI Insurance Claims Automation Market is witnessing rapid transformation driven by digitalization across the insurance value chain and increasing pressure to enhance operational efficiency. Insurers are adopting AI-driven solutions to automate claims intake, assessment, fraud detection, and settlement processes, reducing reliance on manual workflows. Approximately 65% of insurers globally have initiated AI-based claims automation projects to improve turnaround time and reduce operational costs. The market is also influenced by the rising complexity of insurance claims, particularly in health and property segments, requiring advanced analytics and real-time data processing capabilities. Integration of AI with cloud computing and IoT data sources is further enabling insurers to process high volumes of claims with improved accuracy. Additionally, regulatory compliance requirements related to data privacy and transparency are shaping AI adoption strategies, particularly in developed markets. Overall, the market dynamics reflect a shift toward intelligent automation, enhanced customer experience, and scalable digital insurance operations.

The increasing demand for faster and more efficient claims settlement is a primary driver of the AI Insurance Claims Automation Market. Traditional claims processing methods often involve multiple manual steps, leading to delays and inefficiencies. AI-based automation solutions have reduced claims processing time by up to 60%, enabling insurers to handle higher claim volumes without increasing workforce size. Over 70% of policyholders now expect claims to be processed within 24–48 hours, pushing insurers to adopt automated systems. Additionally, AI-driven fraud detection tools improve accuracy by nearly 45%, reducing financial losses and enhancing trust among customers. The ability to process claims in real-time using AI algorithms and predictive analytics is transforming operational workflows and improving customer satisfaction.

Data privacy concerns and integration challenges are significant restraints affecting the AI Insurance Claims Automation Market. Insurance claims processing involves sensitive customer data, including personal, financial, and medical information, making compliance with regulations such as GDPR and similar frameworks essential. Approximately 48% of insurers report difficulties in integrating AI systems with legacy infrastructure, leading to delays in implementation. Additionally, concerns around data security breaches and algorithm transparency are limiting adoption among smaller insurers. The need for high-quality structured data also poses a challenge, as nearly 35% of claims data remains unstructured, requiring extensive preprocessing before AI models can be applied effectively. These factors collectively slow down large-scale adoption despite strong demand.

The ongoing digital transformation across the insurance industry presents significant opportunities for the AI Insurance Claims Automation Market. Increasing adoption of cloud-based platforms and digital insurance ecosystems enables insurers to deploy scalable AI solutions. Over 58% of insurers have shifted to cloud-based claims systems, facilitating faster AI integration. Emerging markets in Asia-Pacific and Latin America are witnessing rapid growth in digital insurance adoption, with mobile-based claims submissions increasing by over 50%. Additionally, advancements in technologies such as computer vision and natural language processing are opening new opportunities for automated damage assessment and document processing. These innovations allow insurers to enhance accuracy, reduce costs, and improve customer engagement, creating new growth avenues.

High implementation costs and a shortage of skilled professionals pose major challenges for the AI Insurance Claims Automation Market. Deploying AI-driven systems requires significant investment in infrastructure, data management, and integration with existing platforms. Approximately 42% of insurers cite high initial costs as a barrier to adoption. Additionally, there is a growing demand for AI specialists, data scientists, and domain experts, with a global talent gap of nearly 30% in AI-related roles. Training existing workforce and ensuring seamless system integration further adds to operational complexity. These challenges limit adoption among small and medium-sized insurers, despite the long-term benefits of automation.

Surge in AI-powered fraud detection systems: AI-driven fraud detection tools are now used in over 68% of insurance claims processes, improving detection rates by nearly 45%. Advanced machine learning models analyze claim patterns and behavioral data, enabling insurers to identify suspicious claims with higher accuracy and reduce fraudulent payouts significantly.

Expansion of computer vision for damage assessment: More than 52% of insurers have adopted computer vision technologies for assessing vehicle and property damage. Automated image analysis reduces inspection time by up to 70% and improves estimation accuracy by 40%, especially in auto insurance claims processing.

Growth in conversational AI and chatbot integration: Around 60% of insurers have deployed AI-powered chatbots for claims initiation and customer support. These systems handle over 65% of initial customer queries, reducing call center workloads and improving response times by 50%.

Increasing adoption of cloud-based AI platforms: Cloud deployment accounts for over 58% of AI claims automation implementations. Insurers leveraging cloud-based AI solutions report a 35% improvement in scalability and a 30% reduction in infrastructure costs, enabling faster deployment and integration of advanced analytics tools.

The AI Insurance Claims Automation Market is segmented based on type, application, and end-user, each contributing uniquely to market expansion. Different AI technologies such as machine learning, natural language processing, and computer vision are integrated to streamline claims processing. Applications vary across claims management, fraud detection, and customer interaction, with increasing reliance on automated systems to enhance efficiency. End-users include insurance companies, third-party administrators, and insurtech firms, each leveraging AI to improve operational workflows and reduce manual intervention. Approximately 60% of adoption is concentrated among large insurers, while small and mid-sized enterprises are gradually increasing investments in AI-driven claims automation. The segmentation reflects a growing emphasis on digital transformation and intelligent automation across the insurance ecosystem.

The AI Insurance Claims Automation Market by type includes Machine Learning, Natural Language Processing (NLP), Computer Vision, and Other AI Technologies. Machine Learning leads the segment with approximately 42% share due to its ability to analyze large datasets and predict claim outcomes efficiently. NLP accounts for nearly 28% of adoption, primarily used for document processing and claims communication. However, Computer Vision is the fastest-growing segment, expanding at an estimated 27% CAGR, driven by its ability to automate damage assessment in auto and property insurance claims. Other AI technologies collectively contribute around 30% share, supporting niche applications such as predictive analytics and anomaly detection.

• In 2025, a major insurer deployed computer vision technology to assess over 2 million auto claims annually, reducing manual inspection time by 65%.

The market by application includes Claims Processing Automation, Fraud Detection, Customer Support, and Others. Claims Processing Automation dominates with a 46% share, driven by the need to streamline end-to-end claims workflows. Fraud Detection accounts for approximately 26% of adoption, leveraging AI algorithms to identify suspicious activities. Customer Support applications, including chatbots, are growing rapidly and are expected to expand at a CAGR of 26%, supported by increasing demand for real-time customer interaction. Other applications contribute around 28% share, including risk assessment and underwriting support. In 2025, over 40% of insurers globally reported piloting AI-based claims automation systems for customer experience enhancement, while 62% of policyholders preferred digital claims processing solutions.

• In 2025, AI-powered claims automation systems were deployed across more than 150 insurance platforms globally, improving claims turnaround time for millions of users.

The end-user segment includes Insurance Companies, Third-Party Administrators (TPAs), and Insurtech Firms. Insurance Companies lead with a 58% share due to large-scale adoption of AI technologies for claims automation. TPAs account for approximately 22% of the market, focusing on outsourced claims management services. Insurtech Firms represent the fastest-growing segment, expanding at an estimated 29% CAGR, driven by innovation and digital-first business models. Other end-users contribute around 20% share, including brokers and service providers. In 2025, more than 45% of large insurance enterprises reported full-scale AI deployment in claims operations, while 38% of mid-sized firms were in pilot stages.

• In 2025, over 500 insurtech companies globally integrated AI-driven claims automation tools to enhance efficiency and customer experience.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27% between 2026 and 2033.

North America’s dominance is driven by advanced digital infrastructure and high adoption of AI technologies among insurers. Europe follows with a 27% share, supported by strong regulatory frameworks and increasing adoption of explainable AI solutions. Asia-Pacific holds approximately 23% share, driven by rapid digitalization and increasing insurance penetration in countries such as China and India. South America accounts for around 7%, while the Middle East & Africa region contributes nearly 5% share. Increasing investments in digital insurance platforms, rising demand for automated claims processing, and growing consumer preference for digital-first services are key factors shaping regional market dynamics.

North America holds approximately 38% of the global AI Insurance Claims Automation Market, driven by strong presence of large insurance providers and advanced IT infrastructure. Key industries include health, auto, and property insurance, with auto insurance accounting for nearly 40% of AI-based claims implementations. Regulatory frameworks supporting data security and digital transformation are accelerating adoption. Companies such as Guidewire are actively developing AI-powered claims platforms to improve efficiency. Consumer behavior indicates that over 65% of users prefer digital claims submission, reflecting high adoption of automated systems.

Europe accounts for around 27% of the market, with key countries including Germany, the UK, and France leading adoption. Regulatory bodies emphasize transparency and explainable AI, influencing technology deployment strategies. Over 60% of insurers in Europe have implemented AI solutions for compliance and claims automation. Companies like SAP are investing in AI-driven insurance platforms. Consumer behavior shows strong preference for secure and compliant digital services, driving demand for AI-enabled claims systems.

Asia-Pacific represents approximately 23% of the market and is the fastest-growing region. Countries such as China, India, and Japan are leading adoption due to increasing digital insurance penetration. Mobile-based claims submissions account for over 55% of total claims in the region. Insurtech startups are driving innovation, with companies like ZhongAn leveraging AI for automated claims processing. Consumer behavior is heavily influenced by mobile-first platforms, accelerating adoption of AI-based solutions.

South America holds around 7% of the global market, with Brazil and Argentina as key contributors. Increasing adoption of digital insurance platforms is driving demand for AI-based claims automation. Government initiatives supporting fintech growth are encouraging innovation. Local insurers are investing in AI technologies to improve operational efficiency. Consumer behavior reflects growing preference for digital claims processing, particularly among younger demographics.

The Middle East & Africa region accounts for approximately 5% of the market, with UAE and South Africa leading adoption. Growth is driven by increasing investments in digital infrastructure and insurance sector modernization. AI adoption is rising in health and property insurance segments. Local insurers are partnering with technology providers to implement automated claims systems. Consumer behavior indicates growing acceptance of digital insurance services, supporting market growth.

United States – 34% Market share: Strong investment in AI technologies and high adoption among large insurers

China – 18% Market share: Rapid digital insurance growth and increasing use of AI-driven claims platforms

The AI Insurance Claims Automation Market is moderately fragmented, with over 120 active players globally competing across technology development, platform integration, and service delivery. The top five companies collectively account for approximately 48% of the market share, indicating a mix of established technology providers and emerging insurtech firms. Key players are focusing on strategic partnerships, mergers, and acquisitions to expand their capabilities and market presence. For instance, collaborations between insurers and AI technology firms have increased by over 35% in the past two years.

Innovation remains a key competitive factor, with companies investing heavily in machine learning, natural language processing, and computer vision technologies. Product differentiation is driven by features such as real-time claims processing, fraud detection accuracy, and customer engagement tools. Additionally, cloud-based solutions are becoming a standard offering, with over 60% of vendors providing SaaS-based platforms. The competitive landscape is expected to evolve further with increasing entry of startups and continuous technological advancements.

Accenture

Cognizant

Capgemini

Pegasystems

Guidewire Software

SAP

DXC Technology

Infosys

Wipro

TCS (Tata Consultancy Services)

Genpact

HCLTech

Shift Technology

The AI Insurance Claims Automation Market is driven by rapid advancements in artificial intelligence technologies, including machine learning, natural language processing (NLP), and computer vision. Machine learning algorithms are widely used to analyze historical claims data, enabling predictive analytics and improving decision accuracy by up to 45%. NLP technologies are transforming document processing, with over 70% of claims-related documents now processed automatically, reducing manual workload significantly. Computer vision is gaining traction in auto and property insurance, where image recognition systems can assess damage with up to 90% accuracy.

Cloud computing plays a critical role in enabling scalable AI deployments, with more than 58% of insurers adopting cloud-based platforms for claims automation. Integration with IoT devices is further enhancing data collection and real-time analysis, particularly in health and auto insurance segments. Additionally, generative AI is emerging as a transformative technology, enabling automated report generation and decision support systems. Robotic process automation (RPA) is also widely used to handle repetitive tasks, improving efficiency and reducing operational costs. These technological advancements are collectively driving innovation and enabling insurers to deliver faster, more accurate, and customer-centric claims processing solutions.

• In May 2025, IBM announced new hybrid AI capabilities at its THINK event, enabling enterprises to deploy AI agents integrated across 80+ business applications, supporting automated workflows such as claims processing and decision orchestration at scale. Source: www.ibm.com

• In 2025, IBM highlighted the growing role of agentic AI in insurance claims operations, with 77% of insurers expecting autonomous execution of transactional processes within two years, significantly enhancing claims automation efficiency and real-time decision-making.

• In 2024–2025, IBM expanded its watsonx-based generative AI initiatives for insurance clients, enabling automated claims document analysis, summarization, and decision support, improving productivity for insurance agents by up to 42% in operational workflows.

• In 2024, IBM continued deployment of AI-powered intelligent workflows through IBM Cloud Paks, allowing insurers to modernize claims processing systems by automating manual tasks and improving claims handling efficiency across automotive insurance use cases.

The AI Insurance Claims Automation Market Report provides a comprehensive analysis of key market segments, including type, application, and end-user categories. It covers technologies such as machine learning, natural language processing, computer vision, and robotic process automation, which are widely used in claims automation processes. The report evaluates applications across claims processing, fraud detection, customer support, and risk assessment, offering insights into how these functions contribute to operational efficiency and customer satisfaction.

Geographically, the report includes detailed analysis of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional adoption patterns, infrastructure development, and technological advancements. It also examines industry-specific use cases across health, auto, and property insurance sectors, which collectively account for over 80% of AI-based claims automation deployments.

Additionally, the report explores emerging trends such as cloud-based AI platforms, generative AI integration, and real-time analytics, which are shaping the future of the market. It provides insights into competitive dynamics, innovation strategies, and investment patterns, offering valuable information for stakeholders, including insurers, technology providers, and investors. The scope is designed to support strategic decision-making and identify growth opportunities in the evolving AI-driven insurance landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 600.0 Million |

| Market Revenue (2033) | USD 3,576.3 Million |

| CAGR (2026–2033) | 25.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM; Accenture; Cognizant; Capgemini; Pegasystems; Guidewire Software; SAP; DXC Technology; Infosys; Wipro; TCS (Tata Consultancy Services); Genpact; HCLTech; Shift Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |