Reports

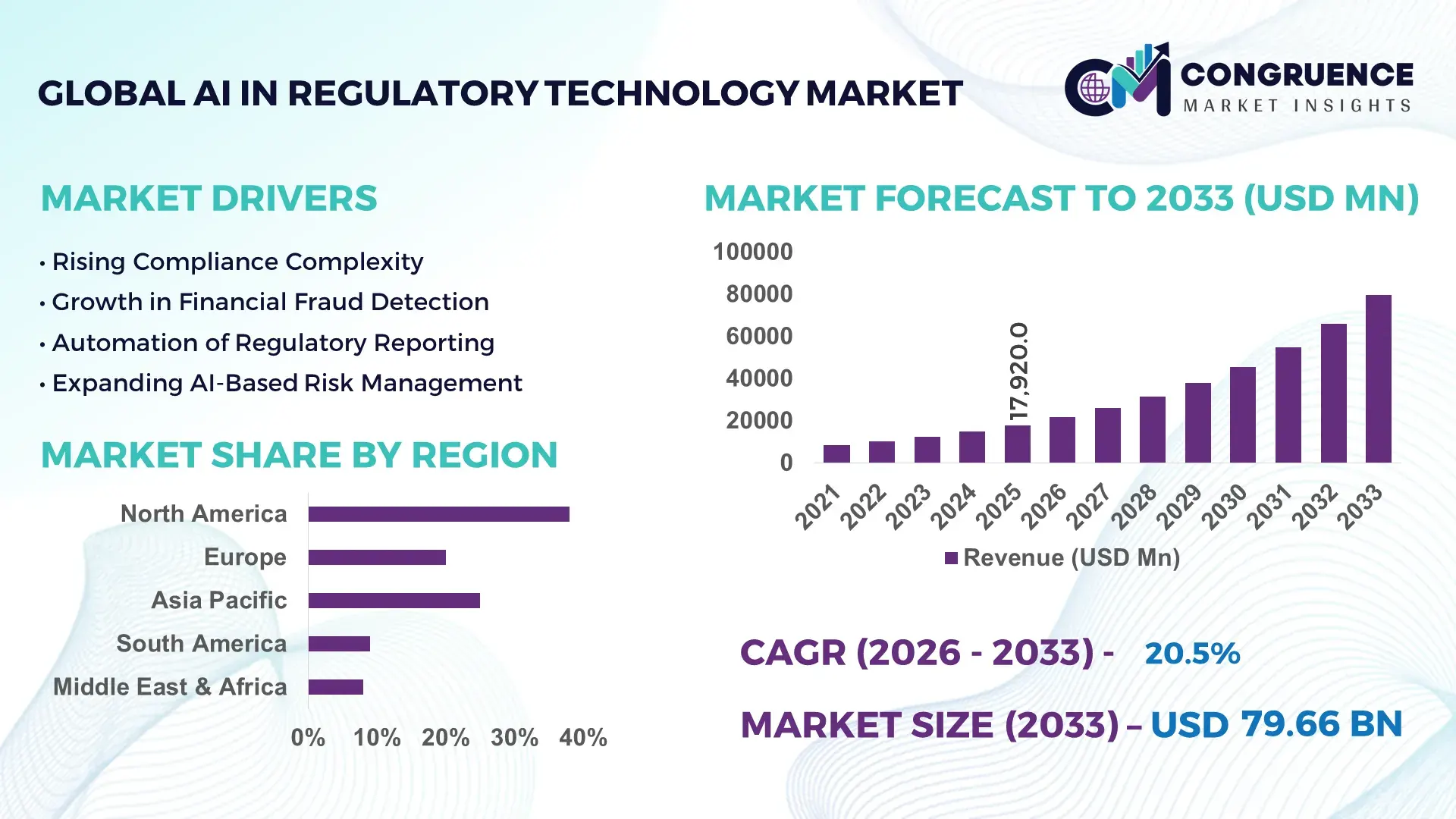

The Global AI in Regulatory Technology Market was valued at USD 17920 Million in 2025 and is anticipated to reach a value of USD 79658.91 Million by 2033 expanding at a CAGR of 20.5% between 2026 and 2033.

Accelerated adoption is driven by AI-enabled compliance automation, which reduces regulatory processing time by nearly 42% across banking and insurance workflows while improving audit accuracy and risk detection capabilities. Increasing regulatory complexity across cross-border financial operations, especially under tightening data governance and anti-money laundering frameworks in North America and Europe, is pushing enterprises toward scalable RegTech AI platforms.

In the 2024–2026 period, global digital compliance transformation has intensified due to stricter financial oversight and rising penalties for reporting delays, with enterprises shifting from manual compliance systems to predictive AI-driven monitoring models. The United States dominates the ecosystem with nearly 38% market share, supported by over USD 6.8 billion in RegTech-focused AI investments and strong deployment across banking, fintech, and insurance sectors. U.S. institutions report up to 55% faster regulatory reporting cycles compared to legacy systems, while cloud-native compliance adoption exceeds 62% in large financial enterprises. By contrast, emerging Asian markets collectively hold around 29% share, driven by rapid fintech expansion and regulatory digitization programs.

This concentration of technological and capital leadership in North America is reshaping global compliance standards and accelerating cross-border RegTech integration strategies for multinational enterprises.

Market Size & Growth: USD 17920M (2025) to USD 79658.91M (2033), driven by AI-based compliance automation reducing regulatory workload by 40%+ in financial systems.

Top Growth Drivers: 24% increase in compliance digitization, 31% rise in financial fraud detection demand, 27% expansion in AI governance tools adoption.

Short-Term Forecast: By 2028, regulatory processing costs decline by 35% with AI-enabled workflow automation across banking and insurance sectors.

Emerging Technologies: AI-driven risk analytics, NLP-based compliance monitoring, and blockchain-integrated audit trails improving transparency by 45%.

Regional Leaders: North America (~USD 28500M), Europe (~USD 19600M), Asia-Pacific (~USD 23200M) with cloud-first compliance adoption exceeding 60% in advanced economies.

Consumer/End-User Trends: Nearly 58% of financial institutions now use AI compliance dashboards for real-time regulatory reporting and fraud prevention.

Pilot/Case Example: 2026 fintech deployment reduced AML screening time by 52% and improved false-positive detection accuracy by 38%.

Competitive Landscape: Top leader holds ~18% share; key players include IBM, Thomson Reuters, NICE Actimize, Oracle, and Workiva shaping enterprise RegTech ecosystems.

Regulatory & ESG Impact: 44% improvement in ESG reporting accuracy due to AI-assisted compliance verification and automated disclosure tracking systems.

Investment & Funding: Over USD 9.2 billion invested in 2025 with strong VC-backed expansion into AI compliance SaaS platforms and cross-border RegTech partnerships.

Innovation & Future Outlook: Shift toward autonomous compliance systems and predictive regulatory intelligence expected to reduce manual audits by 50%+ across global enterprises.

Financial services and banking lead adoption with about 46% share, followed by insurance at 22% and fintech at 18%, driven by increasing automation in compliance-heavy operations. Recent innovation includes generative AI-based regulatory mapping tools improving classification accuracy by 41% and reducing reporting delays by 36%. Regionally, North America remains dominant, while Asia-Pacific shows rapid expansion supported by digital banking penetration above 65% in major economies. A key shift is emerging toward real-time AI-led regulatory monitoring as global data governance rules tighten. The market is steadily moving toward autonomous compliance systems integrated into cloud ecosystems.

The AI in Regulatory Technology market is becoming a critical investment frontier as compliance complexity intensifies across global financial ecosystems, forcing institutions to prioritize automated governance over manual oversight. A major structural shift is underway as regulatory fragmentation across jurisdictions is increasing operational pressure, with compliance processing costs rising by nearly 28% in multi-market enterprises. In response, AI-enabled RegTech platforms are accelerating decision automation, with next-generation NLP systems improving regulatory interpretation speed by 47% compared to legacy rule-based engines while reducing compliance infrastructure costs by 32%.

North America leads in deployment volume, contributing nearly 38% of global adoption, while Europe leads in innovation intensity with 44% of advanced AI compliance pilots focused on explainable AI and audit transparency frameworks. Over the next 2–3 years, enterprise adoption of predictive compliance systems is expected to reduce regulatory breach incidents by around 35%, significantly reshaping enterprise risk management strategies. ESG-linked compliance automation is also emerging as a competitive differentiator, improving reporting efficiency by 29% while enhancing regulatory alignment across sustainability disclosures. A 2026 fintech deployment demonstrated a 51% reduction in fraud flagging errors using adaptive AI monitoring systems, reinforcing measurable efficiency gains. Strategic investments are increasingly shifting toward cloud-native RegTech ecosystems, with financial institutions reallocating nearly 22% of compliance IT budgets toward AI-first architectures, signaling a decisive transformation in governance infrastructure and competitive positioning.

The expansion of cross-border financial regulation is accelerating demand for AI-driven compliance automation, with regulatory reporting volumes increasing by nearly 33% in global banking networks. Financial institutions are responding to stricter AML and data governance frameworks by integrating AI systems that reduce compliance processing time by 42% and improve anomaly detection accuracy by 37%. A major global shift toward digital-first regulatory frameworks is pushing enterprises to replace fragmented legacy systems with unified AI compliance platforms. Companies are scaling investments in predictive analytics and automated reporting tools, with enterprise adoption of AI governance solutions growing by 31% in highly regulated industries. This structural pressure is driving partnerships between banks and RegTech providers, alongside accelerated deployment of cloud-based compliance infrastructures to ensure real-time regulatory alignment and reduce operational risk exposure.

Despite rapid growth, regulatory fragmentation across jurisdictions is constraining scalability, with compliance discrepancies increasing operational costs by nearly 26% for multinational firms. Around 41% of financial institutions report integration delays due to legacy system incompatibility with AI-driven platforms. Data silos across banking and insurance ecosystems further reduce processing efficiency by 28%, limiting real-time regulatory visibility. Additionally, infrastructure gaps in emerging markets slow deployment cycles by nearly 34%, especially where digital compliance frameworks are still evolving. Companies are responding by investing in interoperable compliance architectures, forming cross-border regulatory alliances, and adopting hybrid AI models that combine rule-based and predictive systems to reduce transition risk and ensure smoother integration across fragmented regulatory environments.

A significant opportunity is emerging in predictive regulatory intelligence, where AI systems forecast compliance risks with up to 45% higher accuracy compared to static monitoring tools. Adoption in emerging markets is expanding rapidly, with digital banking ecosystems growing by nearly 39%, creating new demand for scalable RegTech platforms. Cloud-native compliance solutions are enabling up to 33% cost reduction in regulatory operations, unlocking strong ROI for mid-sized financial institutions. A notable innovation shift is the integration of generative AI into regulatory mapping, improving document processing speed by 41% and enabling real-time policy adaptation. Companies are positioning aggressively through R&D investment expansion, ecosystem partnerships, and localized compliance solutions to capture underserved markets and establish early dominance in AI-first regulatory infrastructure.

Scalability remains a critical challenge as nearly 36% of enterprises struggle with integrating AI compliance tools into fragmented legacy IT infrastructures. High data security requirements increase implementation complexity, raising deployment costs by approximately 29% for large financial institutions. Additionally, regulatory uncertainty across emerging digital governance frameworks creates adoption delays of up to 27% in cross-border operations. Infrastructure limitations in certain regions further restrict real-time compliance capabilities, reducing system responsiveness by nearly 22%. These constraints are forcing companies to prioritize phased deployment strategies, increase cybersecurity investments, and build resilient hybrid compliance ecosystems that balance automation with regulatory control. Long-term competitiveness will depend on solving integration complexity while maintaining accuracy, scalability, and regulatory trust in AI-driven systems.

38% surge in real-time compliance automation reshaping enterprise workflows: Financial institutions are shifting from periodic compliance checks to continuous AI-driven monitoring, with real-time regulatory processing adoption rising by 38% and manual audit dependency dropping by 29%. Deployment of event-driven compliance engines is improving reporting speed by 44% while reducing operational bottlenecks by 31%. Banks and fintech firms are restructuring compliance teams and integrating AI copilots into workflows to manage increasing regulatory volume triggered by stricter cross-border financial oversight and digital taxation frameworks. This shift is forcing enterprises to replace legacy batch systems with streaming compliance architectures that optimize decision cycles and reduce escalation delays.

41% expansion in NLP-based regulatory intelligence systems optimizing document processing: AI-powered natural language processing tools are now handling up to 41% more regulatory documents compared to traditional rule-based engines, improving classification accuracy by 36%. Organizations are deploying automated legal interpretation models to reduce manual review workloads by 33%, especially in banking and insurance compliance units. This is significantly lowering cost per compliance case by 27% while improving audit traceability. Companies are increasingly partnering with RegTech vendors to integrate domain-specific language models, particularly in response to rising documentation complexity across multi-jurisdictional reporting frameworks and evolving ESG disclosure requirements.

35% shift toward cloud-native RegTech platforms accelerating deployment scalability: Cloud-based regulatory solutions are expanding rapidly, with adoption increasing by 35% as enterprises move away from on-premise compliance infrastructure. Processing latency has dropped by 32% while system scalability has improved by 40%, enabling faster regulatory updates across distributed operations. Supply chain digitization in financial data processing is reinforcing this transition, with institutions optimizing infrastructure costs and improving cross-border compliance synchronization. Vendors are responding by launching modular SaaS compliance suites and forming hyperscaler partnerships to support real-time regulatory adaptability across global markets.

29% rise in AI-driven fraud and anomaly detection redefining risk prevention models: Advanced machine learning-based monitoring systems are increasing fraud detection accuracy by 29% while reducing false positives by 34%, significantly improving compliance efficiency. Transaction monitoring systems are now processing up to 48% more data streams in real time, enabling faster regulatory escalation response. Financial institutions are restructuring risk management frameworks and investing in hybrid AI models to balance precision with explainability, particularly under tightening global financial crime regulations. This is pushing vendors to integrate adaptive learning models into compliance ecosystems, improving resilience against evolving digital fraud patterns.

The AI in Regulatory Technology Market is segmented by type, application, and end-users, with demand distribution heavily concentrated in compliance-intensive financial ecosystems. Type-based segmentation shows dominance of risk and compliance management solutions due to high regulatory dependency, while application segmentation is led by AML monitoring and regulatory reporting because of real-time enforcement requirements. End-user demand is primarily concentrated in BFSI, driven by high transaction volumes and strict governance frameworks. Around 44% of demand is concentrated in BFSI alone, while healthcare and government collectively account for nearly 31%, reflecting increasing digitization of compliance systems. Demand is gradually shifting toward fraud detection and identity verification solutions as institutions prioritize security automation and cross-border compliance efficiency, forcing vendors to expand AI-driven modular offerings across all segments.

Compliance Management dominates the AI in Regulatory Technology market with nearly 36% share due to its deep integration into mandatory regulatory workflows and high scalability across banking and insurance systems. Risk Management follows with around 27% share, supported by rising demand for predictive analytics and enterprise-wide governance frameworks. Fraud Detection, holding approximately 21%, is the fastest-growing type as institutions face a 33% rise in digital fraud incidents and increasingly rely on AI-based anomaly detection systems. Identity Verification accounts for the remaining 16%, playing a niche but expanding role in onboarding and KYC digitization. The shift is clearly moving from static compliance tools toward intelligent, predictive systems, with fraud detection and identity verification gaining momentum over traditional compliance modules. Companies are prioritizing AI-first product expansion in high-risk segments while optimizing compliance platforms for cross-functional integration.

AML Monitoring leads the application segment with nearly 34% share due to rising global financial crime enforcement and stricter cross-border transaction surveillance requirements. Regulatory Reporting follows at 26%, driven by increasing automation of mandatory disclosures and a 39% reduction in reporting cycle times through AI integration. Transaction Monitoring, at 20%, is the fastest-growing application as real-time payment ecosystems expand and digital transactions surge. KYC Verification holds 12% share, reflecting steady adoption in onboarding processes, while Audit Management accounts for 8%, primarily used for internal governance optimization. The shift is moving from periodic compliance functions to continuous monitoring systems, with transaction monitoring and AML platforms gaining stronger traction than traditional audit-heavy workflows. Companies are investing in API-based compliance infrastructure and cloud integration to scale real-time regulatory visibility across applications.

BFSI dominates the end-user landscape with nearly 52% share due to high transaction density, regulatory exposure, and heavy reliance on compliance automation systems. Insurance follows with 21% share, driven by fraud prevention and claims validation requirements. Government accounts for 17%, increasingly adopting AI-driven regulatory oversight for taxation and policy enforcement, while healthcare holds 10%, focusing on compliance in patient data governance and billing transparency. Healthcare is emerging as the fastest-growing segment due to a 28% increase in digital health record compliance requirements and rising regulatory digitization. BFSI remains the most mature adopter, while government and healthcare are accelerating adoption through digital transformation initiatives. Companies are tailoring solutions through sector-specific compliance platforms, subscription-based pricing models, and strategic partnerships with public institutions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.4% between 2026 and 2033.

North America leads in scale due to dense financial infrastructure and early AI compliance adoption, while Europe holds around 27% share driven by strict regulatory frameworks and explainable AI deployment requirements. Asia-Pacific contributes nearly 29% share, accelerating due to rapid digital banking expansion and fintech penetration above 65% in major economies. Europe is emerging as the innovation hub with 44% of advanced RegTech pilots focused on transparency and audit automation. A structural shift is visible as regulatory digitization and cross-border compliance tightening force enterprises to diversify AI compliance investments across regions. Companies are strategically expanding in Asia-Pacific for scale and in Europe for regulatory sophistication while maintaining operational hubs in North America for execution stability.

North America holds nearly 38% share of the AI in Regulatory Technology market, driven by strong financial digitization and early adoption of AI-based compliance automation across BFSI institutions. Regulatory pressure from evolving AML and data governance frameworks has increased automation deployment by 41%, while cloud-based compliance systems now cover over 62% of large enterprises. A structural shift toward real-time regulatory reporting has reduced compliance processing time by 45%, improving operational efficiency. The U.S. alone accounts for nearly 70% of regional AI RegTech investment flow, supported by rapid fintech expansion and enterprise modernization programs. Institutions are prioritizing predictive compliance tools and automated risk detection systems to reduce audit delays by 33%. Companies are aggressively scaling AI-first compliance infrastructure, making North America a strategic hub for high-value regulatory innovation and enterprise-grade deployment decisions.

Europe accounts for nearly 27% share of the AI in Regulatory Technology market, with Germany, the UK, and France leading adoption due to stringent compliance and ESG mandates. GDPR-driven governance frameworks and MiCA regulations are forcing enterprises to integrate AI compliance systems, improving reporting accuracy by 39% and reducing manual audit workloads by 31%. ESG compliance automation is a major driver, with 44% of financial institutions deploying AI-based sustainability reporting tools. A key operational shift is the move toward explainable AI, with 36% of RegTech deployments focused on audit transparency and regulatory traceability. Enterprises are prioritizing quality-first compliance systems, investing in cross-border reporting automation and risk analytics platforms. Strategic investment in AI governance tools is increasing as companies adapt to strict regulatory scrutiny, making Europe a policy-driven innovation hub for advanced compliance transformation.

Asia-Pacific holds around 29% share of the AI in Regulatory Technology market, driven by rapid fintech expansion and digital banking penetration exceeding 65% in key economies such as China, India, and Singapore. Regulatory digitization programs are accelerating adoption, improving compliance processing speed by 42% and reducing operational costs by 28%. The region benefits from strong infrastructure scaling and cloud-first financial ecosystems, enabling 33% faster deployment of AI compliance systems compared to traditional markets. Transaction volumes are rising sharply, forcing institutions to adopt real-time regulatory monitoring tools. Companies are prioritizing scalable SaaS-based compliance models to support mass adoption across SMEs and large banks. Asia-Pacific is becoming critical for volume expansion and cost-efficient scaling, with enterprises focusing on speed-driven deployment strategies to capture high-growth financial digitization demand.

South America represents nearly 4% of the AI in Regulatory Technology market, with Brazil and Chile leading adoption due to increasing financial digitization. Banking modernization programs are improving compliance automation efficiency by 26%, while digital transaction growth has risen by 31%, driving RegTech demand. However, infrastructure gaps and limited cloud penetration constrain large-scale deployment, delaying adoption cycles by nearly 22%. Despite this, financial institutions are increasingly shifting toward cloud-based compliance tools to reduce operational costs by 19% and improve reporting efficiency. Enterprises are adopting modular AI compliance systems to overcome cost sensitivity and scalability issues. The region presents a mixed opportunity-risk profile, where growing digital banking demand is balanced by regulatory and infrastructure limitations, making it attractive for selective but cautious RegTech expansion strategies.

Middle East & Africa accounts for nearly 2% share of the AI in Regulatory Technology market, with the UAE, Saudi Arabia, and South Africa leading adoption. Financial sector modernization and government-led digital transformation programs are driving compliance automation growth, improving regulatory efficiency by 34%. Oil & gas-linked financial ecosystems and infrastructure megaprojects are increasing demand for transparent compliance systems. Cloud adoption in regulatory workflows has grown by 29%, enabling faster audit processing and cross-border reporting integration. However, uneven infrastructure development remains a constraint, slowing uniform adoption across the region. Companies are investing in partnerships with local financial institutions and government agencies to deploy scalable AI compliance platforms. The region is emerging as a strategic transformation zone where regulatory modernization and investment-led digitalization are creating new RegTech opportunities.

United States – 34% share in AI in Regulatory Technology market – Strong fintech ecosystem and early AI compliance adoption across BFSI sector

China – 18% share in AI in Regulatory Technology market – Rapid digital banking expansion and large-scale regulatory digitization programs

The AI in Regulatory Technology market is shaped by global technology leaders, RegTech specialists, and enterprise software providers competing on AI capability, compliance automation depth, and integration speed. Key players such as IBM, Oracle, Thomson Reuters, NICE Actimize, and Workiva collectively hold around 46% share, driven by strong enterprise penetration and advanced AI compliance platforms. Competition is intensifying around predictive analytics accuracy (improving by 33%), real-time monitoring speed (enhanced by 41%), and automation depth (cost reduction of 29%). Firms are expanding through cloud partnerships, API-driven ecosystems, and acquisitions of niche RegTech startups to strengthen domain expertise. A clear shift is visible toward platform consolidation as enterprises prefer unified compliance ecosystems over fragmented tools. Entry barriers remain high due to regulatory complexity and data security requirements. Winning requires deep AI specialization, regulatory adaptability, and scalable cloud-native architecture.

IBM

Oracle

Thomson Reuters

NICE Actimize

Workiva

SAS Institute

Fenergo

ComplyAdvantage

Ascent RegTech

Clausematch

Trulioo

Napier AI

Ayasdi

Suade Labs

Current technologies in the AI in Regulatory Technology market are centered on AI-driven compliance automation, NLP-based regulatory interpretation, and cloud-native monitoring systems. These tools are improving compliance processing efficiency by nearly 42% and reducing manual review costs by 31% across BFSI operations. Around 58% of large financial institutions now deploy AI-enabled compliance dashboards, integrating real-time reporting with risk analytics for faster decision-making and audit readiness.

Emerging technologies include generative AI for regulatory mapping, explainable AI for audit transparency, and predictive risk engines integrated with blockchain-based audit trails. Generative AI systems are improving document classification speed by 39% while cutting compliance validation errors by 27%. These technologies are being embedded into enterprise workflows through API-first architectures, enabling seamless integration with legacy banking systems and reducing system migration friction by 33%.

Disruptive innovation is led by autonomous compliance agents that continuously monitor transactions and adapt regulatory rules in real time. These systems are delivering up to 48% improvement in fraud detection accuracy compared to rule-based models while reducing compliance escalation delays by 35%. A clear shift is visible where AI replaces static compliance workflows, creating a 52% performance gap versus legacy systems. Between 2026 and 2028, enterprises adopting fully integrated AI compliance ecosystems are expected to gain stronger regulatory agility and faster audit closure cycles, giving early adopters a sustained competitive advantage in high-risk financial environments.

Jan 2025 – IBM launched an upgraded AI compliance engine integrated with Watson X, improving regulatory document processing speed by 44% and reducing false compliance alerts by 28% across banking clients. The enhancement strengthened enterprise risk automation and improved audit readiness across global financial institutions. [RegTech Upgrade] Source: https://www.ibm.com

Sep 2024 – Thomson Reuters expanded its CLEAR regulatory intelligence platform with generative AI features, increasing identity verification accuracy by 36% and processing over 1.2 million compliance checks daily. This improved real-time regulatory screening efficiency for legal and financial sectors. [AI Compliance Scale] Source: https://www.thomsonreuters.com

Mar 2026 – NICE Actimize partnered with a major European bank to deploy AI-driven fraud detection systems, reducing transaction monitoring false positives by 41% and improving AML detection speed by 33%, significantly strengthening cross-border financial security operations. [Fraud Shield Expansion] Source: https://www.niceactimize.com

Jul 2025 – Oracle upgraded its cloud RegTech suite with embedded AI governance tools, enabling 38% faster regulatory reporting cycles and supporting compliance workloads across 900+ enterprise clients globally, enhancing scalability and operational resilience. [Cloud Compliance Shift] Source: https://www.oracle.com

The AI in Regulatory Technology Market report covers comprehensive segmentation across compliance management, risk management, fraud detection, and identity verification, alongside applications such as AML monitoring, KYC verification, regulatory reporting, transaction monitoring, and audit management. It further analyzes end-user industries including BFSI, healthcare, government, and insurance, where BFSI alone contributes nearly 52% of total demand, highlighting concentrated adoption in high-regulation sectors.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing regional adoption patterns, infrastructure maturity, and regulatory digitization trends. It also examines key technologies such as NLP-based compliance systems, generative AI, cloud-native RegTech platforms, and predictive risk analytics, with over 58% adoption observed in advanced financial institutions for AI-driven compliance workflows.

Strategically, the report provides decision-makers with insights into emerging automation trends, cross-border regulatory alignment, and enterprise-scale AI deployment strategies. It supports investment planning, market expansion, and competitive positioning by analyzing more than 15 key companies and tracking adoption shifts where AI-based compliance systems improve operational efficiency by up to 42%. Covering forward-looking dynamics for 2026–2033, the report highlights niche growth areas like autonomous compliance agents and explainable AI systems, enabling stakeholders to identify high-impact opportunities in a rapidly transforming regulatory landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 17920 Million |

|

Market Revenue in 2033 |

USD 79658.91 Million |

|

CAGR (2026 - 2033) |

20.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Oracle, Thomson Reuters, NICE Actimize, Workiva, SAS Institute, Fenergo, ComplyAdvantage, Ascent RegTech, Clausematch, Trulioo, Napier AI, Ayasdi, Suade Labs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |