Reports

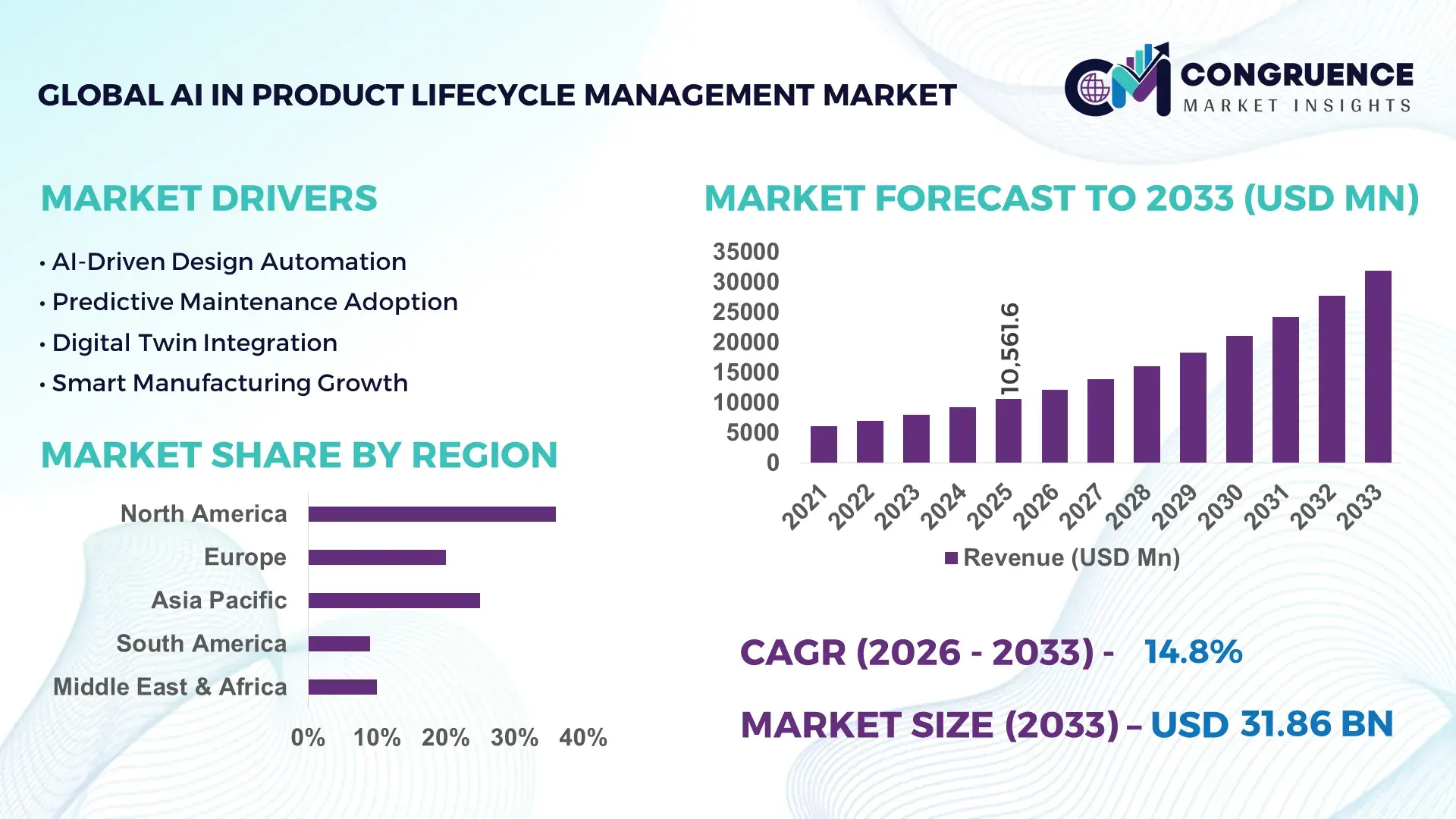

The Global AI in Product Lifecycle Management Market was valued at USD 10561.6 Million in 2025 and is anticipated to reach a value of USD 31861.39 Million by 2033 expanding at a CAGR of 14.8% between 2026 and 2033. Growth is accelerating through AI-driven digital thread integration, predictive engineering analytics, automated compliance management, and real-time product simulation adoption across automotive, aerospace, industrial manufacturing, and electronics sectors responding to post-Red Sea supply chain disruptions and shorter product development cycles.

The United States dominates the global AI in Product Lifecycle Management Market with approximately 34% market share, supported by over USD 4.2 billion in industrial AI deployment investments across aerospace, EV, semiconductor, and defense manufacturing ecosystems in 2026. Germany follows with nearly 18% share, driven by Industry 4.0 adoption where over 61% of automotive manufacturers integrate AI-enabled PLM platforms for digital twin and predictive maintenance functions. China continues expanding production-linked AI engineering infrastructure, increasing smart factory integration capacity by 22% year-over-year within electronics and industrial equipment manufacturing.

Enterprises prioritizing scalable AI-enabled PLM ecosystems gain faster engineering validation, lower redesign costs, and stronger supply-chain resilience across globally distributed production environments.

Market Size & Growth: USD 10.5 billion market in 2025 advancing toward USD 31.8 billion by 2033, supported by AI-driven engineering automation and accelerated digital manufacturing transformation.

Top Growth Drivers: Predictive maintenance adoption increased 41%, digital twin deployment expanded 38%, and automated design validation integration rose 35% across industrial sectors.

Short-Term Forecast: By 2028, AI-enabled PLM platforms are reducing product development timelines by 27% while improving engineering productivity by 31%.

Emerging Technologies: Generative AI, digital thread orchestration, and industrial digital twins improved design accuracy by 29% and reduced prototyping cycles by 24%.

Regional Leaders: North America exceeds USD 11.4 billion through aerospace AI integration, Europe approaches USD 8.2 billion via Industry 4.0 manufacturing, and Asia-Pacific surpasses USD 9.6 billion with electronics production expansion.

Consumer/End-User Trends: Nearly 58% of manufacturers shifted toward cloud-native PLM platforms supporting real-time collaboration and AI-assisted product lifecycle analytics.

Pilot/Case Example: In 2026, an automotive AI-PLM deployment reduced engineering change orders by 32% and lowered validation costs by 19% across EV production lines.

Competitive Landscape: Leading vendors collectively control nearly 46% market share, with enterprise competition intensifying among Siemens, PTC, Dassault Systèmes, Autodesk, and SAP.

Regulatory & ESG Impact: Automated lifecycle compliance tools improved carbon tracking efficiency by 28% as manufacturers aligned with stricter European digital product passport regulations.

Investment & Funding: Global industrial AI and PLM-focused investments exceeded USD 7.3 billion in 2026, fueled by strategic partnerships, semiconductor expansion, and smart factory modernization.

Innovation & Future Outlook: Autonomous engineering workflows, AI copilots, and simulation-driven product optimization are accelerating next-generation manufacturing scalability and supply-chain responsiveness.

AI in Product Lifecycle Management Market expansion is strengthening across automotive engineering, semiconductor design, aerospace manufacturing, and industrial equipment optimization where AI-assisted lifecycle analytics reduce design iteration cycles by nearly 30%. Enterprises increasingly deploy generative engineering tools, cloud-native digital twins, and automated compliance systems amid tighter sustainability regulations and ongoing global component sourcing realignments, creating a stronger foundation for long-term operational intelligence and strategic manufacturing resilience.

AI in Product Lifecycle Management is becoming strategically critical as manufacturers prioritize resilient product development ecosystems, accelerated engineering decisions, and digitally connected supply networks. Automotive, aerospace, semiconductor, and industrial equipment companies are restructuring lifecycle operations after persistent component shortages and rising compliance complexity across Europe and Asia. More than 57% of large manufacturers now integrate AI-assisted PLM functions into engineering and procurement workflows to shorten design-to-production timelines and improve cross-functional coordination.

Modern AI-enabled PLM platforms deliver nearly 35% faster design validation and reduce engineering change orders by approximately 28% compared with legacy rule-based lifecycle systems dependent on fragmented data environments. The United States leads in enterprise-scale deployment through semiconductor and defense manufacturing digitization, while Japan and Germany focus on precision engineering optimization and factory-level digital twin integration. In 2026, several EV manufacturers deployed AI-driven simulation platforms capable of reducing physical prototyping cycles by 22%, lowering material waste and improving launch consistency across multi-country production networks.

Over the next two to three years, enterprises are expected to prioritize cloud-native lifecycle orchestration, AI copilots for engineering teams, and supplier-integrated digital threads. Companies are increasing partnerships with industrial software providers and expanding localized engineering hubs to strengthen operational agility, accelerate compliance readiness, and secure long-term manufacturing competitiveness.

Industrial manufacturers are accelerating AI-enabled PLM adoption to improve engineering efficiency, reduce redesign costs, and stabilize globally distributed production operations. More than 61% of automotive and aerospace firms now use AI-supported simulation and lifecycle analytics platforms, while predictive engineering tools have reduced product development delays by nearly 26%. Germany and the United States continue expanding smart manufacturing investments following stricter digital compliance and traceability requirements affecting industrial exports. The transition toward software-defined vehicles and connected industrial equipment is increasing demand for real-time lifecycle intelligence across design, testing, and procurement functions. In response, technology vendors are expanding cloud engineering partnerships, integrating generative AI modules, and strengthening digital twin capabilities to improve collaboration speed, reduce validation bottlenecks, and support high-frequency product iteration strategies.

Fragmented enterprise systems and incompatible engineering architectures continue limiting scalable AI in Product Lifecycle Management deployment. Nearly 48% of manufacturers still operate on legacy PLM environments lacking standardized data interoperability, while integration expenses account for approximately 20% of total implementation budgets. Japanese industrial suppliers and mid-sized European manufacturers face operational disruptions when connecting AI-driven analytics with older CAD, ERP, and manufacturing execution systems. Semiconductor shortages and rising edge-computing hardware costs further pressure infrastructure modernization timelines across advanced manufacturing hubs. Companies are responding through phased cloud migration strategies, localized software customization, and multi-vendor interoperability frameworks to reduce deployment friction. A key operational challenge remains the synchronization of engineering, procurement, and compliance datasets without compromising production continuity or cybersecurity performance.

Generative AI integration is creating new operational opportunities across engineering automation, digital prototyping, and lifecycle optimization. AI-assisted design environments have improved component modeling efficiency by nearly 33% while reducing material consumption during prototyping by approximately 18%. China and South Korea are accelerating industrial AI infrastructure deployment through smart factory expansion and semiconductor manufacturing modernization initiatives. The emergence of AI copilots for engineering teams is enabling faster requirement validation, automated compliance documentation, and adaptive supply-chain coordination across multi-site production environments. Companies are increasing investments in digital thread ecosystems, industrial metaverse simulation, and supplier-connected lifecycle platforms to capture faster iteration cycles and lower operational waste. An emerging strategic opportunity involves combining AI-driven sustainability analytics with lifecycle management systems to improve product traceability and carbon reporting efficiency.

Long-term scalability depends on resolving workforce capability gaps, AI governance inconsistencies, and enterprise cybersecurity risks across connected lifecycle environments. Nearly 44% of manufacturers report shortages of engineers skilled in AI-driven simulation and digital thread management, while cybersecurity incidents targeting industrial software environments increased by over 30% during the past two years. United States defense contractors and European industrial manufacturers face rising pressure to secure sensitive design data within cloud-based collaboration platforms. Inconsistent AI model governance across supplier ecosystems also creates operational risks involving validation accuracy, compliance auditing, and engineering accountability. Companies are expanding industrial AI training programs, strengthening zero-trust cybersecurity architectures, and forming strategic partnerships with cloud infrastructure providers to improve deployment consistency. Competitive advantage increasingly depends on building scalable governance frameworks without slowing engineering responsiveness or cross-border collaboration efficiency.

• AI Copilots Reshape Engineering Enterprise manufacturers are embedding AI copilots into design and lifecycle workflows to accelerate product iteration and reduce engineering bottlenecks. More than 46% of automotive and industrial manufacturers integrated AI-assisted design recommendation tools in 2026, cutting validation cycles by nearly 24% and lowering redesign workloads by 19%. German and Japanese engineering firms are restructuring product teams around AI-supported collaboration platforms, while software vendors are expanding partnerships with CAD and simulation providers to standardize lifecycle automation across distributed production environments.

• Digital Thread Deployment Accelerates Companies are scaling connected digital thread architectures to improve supply-chain synchronization and compliance traceability following continued geopolitical sourcing disruptions. Nearly 52% of aerospace and semiconductor manufacturers now connect procurement, testing, and production datasets through unified lifecycle platforms, improving component traceability accuracy by 31%. United States defense contractors are increasing cloud-based PLM integration investments to support export-control compliance and supplier coordination, while enterprises prioritize interoperable engineering ecosystems to reduce production delays across multi-country operations.

• Sustainability Analytics Gain Priority Lifecycle carbon intelligence and automated compliance monitoring are becoming embedded operational requirements across manufacturing sectors responding to stricter European digital product passport frameworks. AI-driven sustainability analytics reduced material waste during prototyping by approximately 18% while improving lifecycle emissions tracking efficiency by 27%. Consumer electronics manufacturers in South Korea are deploying AI-enabled material optimization systems to lower compliance costs and improve ESG reporting consistency across supplier networks and assembly operations.

• Industrial Cloud Consolidation Expands Large manufacturers are consolidating fragmented engineering software environments into cloud-native PLM ecosystems to improve scalability and cybersecurity resilience. Around 58% of enterprise manufacturers shifted toward unified lifecycle management infrastructures in 2026, reducing cross-platform integration delays by nearly 22%. A less visible trend involves industrial companies relocating sensitive engineering workloads into sovereign cloud environments following rising cyberattacks targeting industrial software infrastructure, prompting strategic alliances between cloud providers, cybersecurity firms, and PLM software developers.

Predictive Analytics remains the dominant segment within the AI in Product Lifecycle Management Market due to its scalability across engineering optimization, maintenance forecasting, and operational risk reduction. More than 54% of large industrial manufacturers deploy predictive lifecycle intelligence tools to reduce downtime and improve production planning accuracy. Automotive and aerospace companies increasingly integrate predictive analytics into procurement and testing workflows, reducing engineering change orders by approximately 21%. Machine Learning Platforms continue supporting broader enterprise AI deployment by enabling adaptive modeling, supplier-risk forecasting, and intelligent design automation across connected manufacturing environments.

Generative Design is emerging as the fastest-growing segment as enterprises accelerate lightweight component engineering and simulation-driven product development strategies. In 2026, AI-assisted generative design reduced prototype material consumption by nearly 17% across EV manufacturing programs in Germany and South Korea. Digital Twin Solutions are strengthening adoption through factory-level simulation and asset synchronization capabilities, while Natural Language Processing Tools are improving engineering documentation efficiency and compliance automation. Companies are expanding investments through industrial AI partnerships, cloud-native PLM integration, and proprietary engineering model development to secure faster iteration cycles and lower lifecycle operational costs.

Product Design Optimization represents the leading application segment as manufacturers prioritize shorter engineering cycles, lower prototyping costs, and improved cross-functional collaboration. Nearly 59% of enterprise PLM deployments now focus on AI-assisted design refinement and simulation-based product validation, particularly within automotive, aerospace, and industrial equipment sectors. AI-enabled optimization platforms reduced physical testing requirements by approximately 23% while improving design accuracy and launch consistency across distributed production environments. Lifecycle Data Management remains operationally critical as enterprises consolidate fragmented engineering, procurement, and compliance datasets into centralized digital thread ecosystems.

Manufacturing Process Automation is the fastest-growing application segment due to rising labor cost pressure, supply-chain volatility, and smart factory modernization initiatives. Semiconductor manufacturers in Taiwan and South Korea increased AI-driven process automation integration by nearly 29% during 2026 to improve throughput consistency and defect detection performance. Predictive Maintenance continues expanding through connected asset monitoring systems, while Quality Management applications increasingly rely on AI-enabled anomaly detection and compliance tracking. Companies are scaling deployment through industrial cloud partnerships, automated workflow orchestration, and integrated factory intelligence platforms to strengthen production resilience and operational responsiveness.

Automotive remains the dominant end-user segment due to high-volume product iteration requirements, software-defined vehicle development, and extensive supplier coordination complexity. More than 62% of large automotive manufacturers now integrate AI-enabled PLM systems into engineering, testing, and procurement operations to accelerate EV development cycles and improve production flexibility. German and United States automakers reduced design modification delays by nearly 24% through AI-assisted simulation and digital twin deployment. Aerospace & Defense continues maintaining strong demand due to strict compliance management, advanced component traceability, and mission-critical lifecycle validation requirements.

Healthcare is emerging as the fastest-growing end-user segment as medical device manufacturers accelerate AI-supported regulatory documentation, product traceability, and precision engineering workflows. In 2026, healthcare-focused lifecycle management deployments increased by approximately 28% following stricter device compliance standards and growing connected-device manufacturing complexity. Consumer Electronics companies are expanding AI-driven lifecycle automation to support shorter product refresh cycles, while Industrial Manufacturing enterprises prioritize predictive engineering and factory-level integration capabilities. Retail & E-commerce adoption remains comparatively smaller but is increasing through AI-assisted packaging optimization and product customization strategies.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America leads the AI in Product Lifecycle Management Market through advanced industrial software deployment, aerospace digitization, and large-scale EV manufacturing modernization. The region contributes nearly 36% of global deployment activity, supported by expanding cloud engineering infrastructure and enterprise AI integration across automotive, semiconductor, and defense manufacturing ecosystems. More than 64% of large manufacturers integrated AI-assisted lifecycle analytics into engineering and procurement operations during 2026, improving product validation speed and supplier coordination efficiency. Industrial enterprises are prioritizing predictive simulation, digital thread orchestration, and automated compliance management following continued supply-chain restructuring and rising cybersecurity pressure on engineering environments. Technology providers are expanding strategic collaborations with OEMs and industrial cloud operators to improve interoperability, reduce lifecycle inefficiencies, and strengthen engineering responsiveness across globally distributed production networks.

United States Market Outlook: The United States dominates the regional market through strong enterprise AI spending, semiconductor fabrication expansion, and advanced aerospace manufacturing capabilities. Nearly 68% of Fortune 500 manufacturers accelerated cloud-native PLM modernization projects in 2026 to improve engineering collaboration and reduce design iteration delays. Defense modernization initiatives and EV supply-chain localization programs continue increasing demand for AI-enabled lifecycle intelligence, while software vendors are investing heavily in digital twin ecosystems, AI copilots, and secure engineering collaboration platforms to strengthen long-term operational resilience.

Europe remains a strategically important market due to strong Industry 4.0 integration, sustainability-focused manufacturing regulations, and advanced automotive engineering infrastructure. The region represents approximately 29% of global deployment concentration, supported by rising investment in digital product passport compliance and industrial automation modernization. German and French manufacturers increased AI-supported lifecycle simulation deployment by nearly 27% during 2026 to improve traceability, engineering precision, and cross-border production coordination. Industrial enterprises are prioritizing AI-enabled compliance analytics, automated design validation, and carbon tracking integration to align with evolving industrial sustainability requirements. Software providers are strengthening partnerships with factory automation firms and automotive suppliers to improve lifecycle interoperability and engineering workflow consistency across complex manufacturing ecosystems.

Germany Market Outlook: Germany leads the European market through its strong automotive manufacturing base, precision engineering expertise, and highly integrated industrial software environment. Around 61% of automotive manufacturers in Germany deployed AI-supported digital twin and predictive lifecycle platforms in 2026 to optimize EV production efficiency and reduce engineering modification cycles. National smart factory modernization programs and industrial cloud adoption continue accelerating AI-driven PLM implementation across machinery, aerospace, and electronics manufacturing sectors, while enterprises increasingly prioritize predictive engineering and automated compliance management to maintain export competitiveness.

Asia-Pacific is emerging as the fastest-expanding market due to rapid smart factory expansion, semiconductor manufacturing growth, and aggressive industrial AI deployment strategies. The region contributes approximately 31% of global manufacturing-linked PLM implementation activity, driven by China, Japan, South Korea, and Taiwan. More than 58% of electronics and semiconductor manufacturers integrated AI-assisted lifecycle systems during 2026 to improve throughput consistency, supplier synchronization, and product launch speed. Industrial companies are increasingly deploying AI-enabled simulation, predictive engineering analytics, and automated workflow coordination to strengthen export competitiveness amid ongoing global sourcing realignment. Cloud providers and industrial software vendors are expanding regional infrastructure partnerships to support scalable lifecycle intelligence deployment across high-volume manufacturing environments.

China Market Outlook: China dominates the Asia-Pacific market through extensive smart manufacturing expansion, semiconductor infrastructure investment, and strong industrial AI policy support. Industrial enterprises increased AI-integrated PLM deployment by nearly 33% across electronics, EV, and heavy machinery sectors during 2026 to improve engineering agility and supply-chain visibility. Government-backed factory modernization programs and domestic industrial software ecosystem development continue strengthening enterprise AI adoption, while manufacturers prioritize automated compliance management and predictive lifecycle optimization to reduce operational fragmentation and strengthen global production competitiveness.

South America is witnessing steady AI in Product Lifecycle Management adoption through industrial modernization and manufacturing digitization initiatives across automotive, mining, and industrial processing sectors. The region maintains a developing share of global deployment activity, supported by rising enterprise cloud adoption and operational efficiency priorities. Brazilian manufacturers increased AI-enabled lifecycle management implementation by approximately 19% during 2026 to improve engineering coordination and reduce production inefficiencies. Infrastructure limitations and fragmented software integration environments continue constraining large-scale deployment consistency, particularly among mid-sized industrial enterprises. Companies are responding through phased cloud migration strategies, localized software customization, and AI-assisted workflow automation focused on strengthening production continuity and supply-chain visibility.

Brazil Market Outlook: Brazil remains the leading regional market due to its automotive assembly capacity, industrial manufacturing infrastructure, and growing enterprise digitization initiatives. Nearly 47% of large industrial companies expanded digital engineering modernization programs during 2026 to improve lifecycle data coordination and production planning efficiency. Automotive and industrial equipment manufacturers are prioritizing predictive maintenance integration and AI-assisted factory workflow optimization, while enterprise software providers continue investing in regional implementation support and localized industrial cloud capabilities to strengthen long-term operational scalability.

The Middle East & Africa market is advancing through infrastructure modernization, industrial diversification programs, and enterprise digitization initiatives across energy, aerospace, and manufacturing sectors. The region accounts for a developing but strategically expanding share of global AI-enabled PLM deployment activity, supported by smart industrial infrastructure investments and cloud engineering integration. Gulf industrial enterprises increased AI-assisted lifecycle analytics adoption by nearly 21% during 2026 to improve asset performance visibility and operational coordination. Governments and enterprise groups are strengthening partnerships with industrial software vendors and cloud providers to accelerate manufacturing localization and industrial AI ecosystem development. Engineering workforce limitations and inconsistent digital infrastructure continue affecting deployment scalability across several African industrial markets.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale industrial diversification investments, advanced infrastructure modernization, and expanding smart manufacturing initiatives. More than 42% of major industrial operators accelerated AI-enabled engineering and lifecycle optimization deployment during 2026 across petrochemical, energy, and industrial equipment manufacturing sectors. National digital transformation strategies continue driving enterprise cloud adoption and industrial AI integration, while strategic partnerships with global industrial software providers are strengthening local engineering capabilities and long-term manufacturing competitiveness.

The AI in Product Lifecycle Management Market is dominated by Siemens, PTC, Dassault Systèmes, SAP, and Autodesk, with the top five players collectively controlling nearly 46% of enterprise deployment activity. Global software leaders compete directly on AI-driven simulation depth, digital twin scalability, cloud-native lifecycle orchestration, and engineering interoperability, while specialized industrial software firms focus on customization speed and sector-specific implementation flexibility. Automotive and aerospace manufacturers increasingly prioritize vendors offering integrated supplier-network visibility and AI-assisted compliance automation, reducing engineering validation timelines by nearly 24%. Competition intensified during 2026 as generative AI-enabled engineering copilots improved product iteration efficiency by approximately 31% across enterprise environments. Companies are expanding through industrial cloud partnerships, predictive analytics acquisitions, and regional engineering hub development. Cybersecurity resilience, sovereign cloud compatibility, and multi-platform interoperability remain major competitive pressure points. Winning requires scalable AI architecture, deep industrial expertise, strong ecosystem integration, and long-term enterprise modernization capabilities.

Siemens

PTC

Dassault Systèmes

SAP

Autodesk

Oracle

IBM

Ansys

Hexagon AB

Aras Corporation

Altair Engineering

Infor

Synopsys

AVEVA

AI-native digital twins, predictive analytics engines, and cloud-connected lifecycle orchestration platforms are redefining industrial product development workflows across automotive, aerospace, and semiconductor manufacturing. More than 61% of enterprise manufacturers integrated AI-assisted simulation and lifecycle analytics platforms during 2026, improving engineering validation efficiency by nearly 28% while reducing redesign costs by approximately 19%. Companies are increasingly combining digital thread architectures with real-time operational data to improve supplier coordination, compliance automation, and production planning accuracy across distributed manufacturing environments.

Generative AI and autonomous engineering copilots are emerging as the most disruptive technologies within AI in Product Lifecycle Management ecosystems. AI-assisted engineering systems delivered nearly 35% faster product iteration compared with legacy rule-based lifecycle platforms dependent on fragmented datasets and manual validation workflows. Industrial enterprises in Germany, the United States, and Japan are accelerating deployment of simulation-driven design tools, immersive digital twin visualization, and AI-native workflow automation to shorten prototyping cycles and improve cross-functional engineering responsiveness under increasing supply-chain complexity.

Between 2026 and 2028, industrial AI operating systems, adaptive manufacturing orchestration, and AI-driven lifecycle intelligence platforms will become core competitive differentiators. Companies deploying integrated AI-enabled PLM environments are expected to improve production throughput by 20% while reducing engineering bottlenecks through automated design validation and predictive lifecycle coordination. Software leaders expanding cloud partnerships, industrial metaverse integration, and AI copilot ecosystems will secure stronger operational scalability and faster enterprise adoption.

January 2026 – Siemens expanded its partnership with NVIDIA to build an Industrial AI Operating System integrating AI-native simulation, adaptive manufacturing, and digital twin orchestration. PepsiCo achieved a 20% throughput increase and identified up to 90% of engineering issues before physical deployment, strengthening enterprise-scale lifecycle optimization capabilities. Source: https://news.siemens.com

March 2026 – Siemens launched Teamcenter Digital Reality Viewer and Digital Twin Composer in India, combining NVIDIA Omniverse libraries with industrial AI infrastructure for immersive lifecycle engineering. The deployment improved collaborative engineering visualization and accelerated digital workflow scalability across manufacturing environments supporting complex production coordination.

May 2026 – Siemens entered a strategic partnership with Xometry to integrate AI-native supply-chain intelligence into Siemens Xcelerator platforms. The collaboration included an approximately USD 50 million minority investment and expanded design-to-source lifecycle intelligence for mechanical and industrial component procurement optimization.

April 2026 – Siemens introduced the Eigen Engineering Agent at Hannover Messe 2026, enabling autonomous execution of industrial engineering workflows. The platform delivered up to 50% engineering efficiency gains and accelerated workflow execution by 2–5 times across automation coding, validation, and industrial configuration environments. Source: https://www.reddit.com

This report delivers detailed analysis of the AI in Product Lifecycle Management Market across core technology segments, enterprise applications, end-user industries, and regional deployment trends between 2026 and 2033. The study covers Predictive Analytics, Digital Twin Solutions, Generative Design, Machine Learning Platforms, and Natural Language Processing Tools, alongside operational applications including Product Design Optimization, Manufacturing Process Automation, Predictive Maintenance, and Lifecycle Data Management. More than 60% of enterprise deployments remain concentrated within automotive, aerospace, industrial manufacturing, and semiconductor ecosystems integrating AI-driven engineering workflows and digital thread architectures.

The report evaluates strategic market positioning across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting deployment concentration, smart factory modernization, industrial AI infrastructure expansion, and cloud-native PLM integration patterns. It provides business-focused insights into enterprise adoption strategies, competitive benchmarking, partnership activity, supply-chain transformation, interoperability challenges, cybersecurity priorities, and emerging AI-enabled lifecycle intelligence capabilities shaping next-generation industrial product development environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 10561.6 Million |

|

Market Revenue in 2033 |

USD 31861.39 Million |

|

CAGR (2026 - 2033) |

14.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens, PTC, Dassault Systèmes, SAP, Autodesk, Oracle, IBM, Ansys, Hexagon AB, Aras Corporation, Altair Engineering, Infor, Synopsys, AVEVA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |