Reports

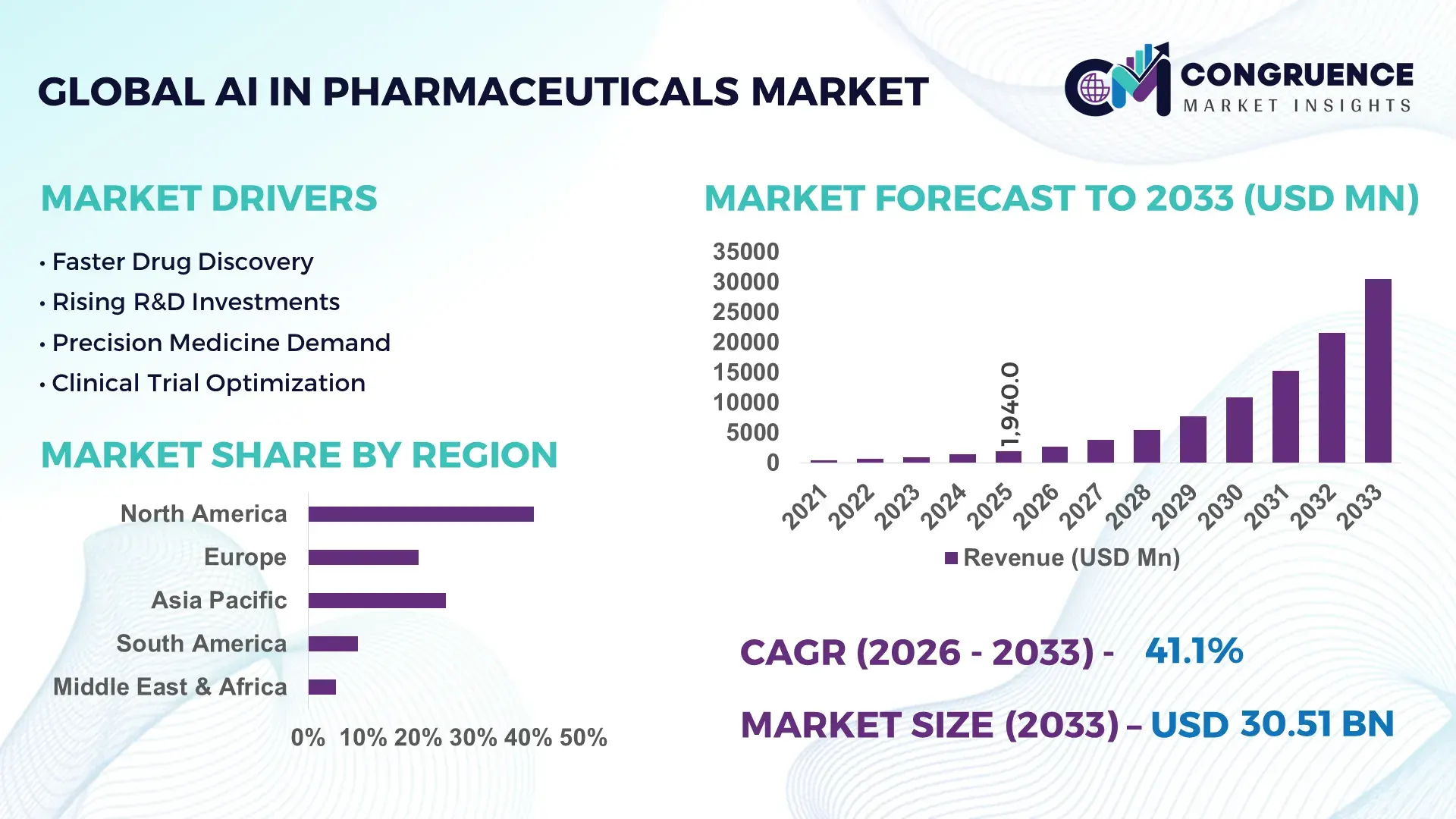

The Global AI in Pharmaceuticals Market was valued at USD 1940 Million in 2025 and is anticipated to reach a value of USD 144709.27 Million by 2033 expanding at a CAGR of 41.12% between 2026 and 2033. AI-driven drug discovery platforms, clinical trial optimization tools, and generative molecular modeling systems are accelerating compound screening timelines by over 55%, while pharmaceutical manufacturers expand AI-enabled R&D operations to reduce late-stage trial failure rates and improve precision medicine commercialization.

The United States dominates the global AI in pharmaceuticals market with approximately 42% share, supported by over USD 18 billion in AI-healthcare investments and rapid adoption across oncology, biologics, and rare disease pipelines. More than 68% of large pharmaceutical companies in the U.S. integrated AI into preclinical workflows by 2026, compared with nearly 39% in Germany and Japan. China continues scaling AI-enabled pharmaceutical manufacturing capacity through state-backed digital health initiatives and domestic semiconductor expansion despite ongoing U.S.-China technology restrictions affecting advanced AI chip access.

Pharmaceutical companies prioritizing proprietary AI models, high-quality clinical datasets, and cross-border digital infrastructure partnerships are positioned to secure faster drug commercialization cycles and stronger competitive differentiation through 2033.

Market Size & Growth: USD 1940 Million in 2025 to USD 144709.27 Million by 2033 at 41.12% growth, driven by AI-led drug discovery acceleration and clinical data automation.

Top Growth Drivers: Drug screening efficiency improved 55%, clinical trial timelines reduced 35%, and AI-assisted biomarker identification accuracy increased 48%.

Short-Term Forecast: By 2028, AI-integrated pharmaceutical R&D operations are projected to lower molecule validation costs by 32% and improve candidate selection efficiency by 44%.

Emerging Technologies: Generative AI, federated learning, and predictive analytics platforms increased pharmaceutical data processing speed by 60% across advanced research environments.

Regional Leaders: North America exceeded USD 780 Million market contribution in 2025, Europe crossed USD 420 Million, and Asia-Pacific surpassed USD 510 Million with rapid cloud-AI adoption.

Consumer/End-User Trends: Nearly 64% of pharmaceutical enterprises expanded AI usage in precision medicine, digital pathology, and decentralized clinical trial management by 2026.

Pilot/Case Example: In 2026, an AI-assisted oncology trial platform reduced patient recruitment timelines by 41% and improved protocol matching efficiency by 36%.

Competitive Landscape: Leading technology-pharma alliances controlled nearly 38% market concentration, with strong competition among global pharmaceutical innovators and enterprise AI developers.

Regulatory & ESG Impact: AI-driven manufacturing analytics reduced pharmaceutical batch waste by 22% while supporting stricter data transparency and compliance frameworks across Europe and North America.

Investment & Funding: Global investments surpassed USD 24 billion in 2026, fueled by strategic partnerships, sovereign AI initiatives, and cross-border pharmaceutical digitalization programs.

Innovation & Future Outlook: Autonomous laboratory systems, multimodal AI models, and synthetic biology integration are reshaping high-growth pharmaceutical development and global supply-chain resilience.

AI in pharmaceuticals market expansion is increasingly concentrated in oncology research, biologics manufacturing, and precision therapeutics, where AI-assisted platforms improve target identification accuracy by nearly 50%. Pharmaceutical firms are deploying generative AI for molecular simulation and decentralized trial management while strengthening data governance compliance amid tightening global healthcare regulations. Asia-Pacific manufacturing digitalization and AI-enabled supply-chain optimization are also accelerating operational scalability, reinforcing the market’s long-term strategic transformation trajectory.

AI in pharmaceuticals has become a strategic competitive layer across drug discovery, manufacturing analytics, and precision therapeutics as pharmaceutical companies restructure R&D operations around data-centric platforms. More than 62% of large biopharma enterprises integrated AI-driven clinical workflow systems by 2026 to reduce development bottlenecks and improve regulatory submission accuracy. The market is also benefiting from supply-chain digitalization and cloud infrastructure modernization as companies localize production networks following ongoing geopolitical pressure on active pharmaceutical ingredient sourcing and semiconductor-dependent computing systems.

Generative AI platforms now process molecular candidate screening nearly 4 times faster than legacy computational chemistry systems while lowering early-stage research costs by approximately 30%. The United States leads in advanced AI-pharma partnerships and proprietary clinical dataset development, whereas India and Singapore are scaling cost-efficient AI-enabled trial management and pharmaceutical manufacturing infrastructure. Over the next 2–3 years, decentralized clinical trials and AI-assisted biologics development are expected to increase enterprise deployment rates beyond 70% among top-tier pharmaceutical manufacturers.

Pharmaceutical companies are expanding AI partnerships with cloud providers, semiconductor firms, and contract research organizations to improve operational scalability and shorten commercialization timelines. AI-enabled manufacturing quality systems are also reducing batch deviation rates by nearly 25%, supporting stronger compliance and lower material waste. Companies securing integrated AI ecosystems, proprietary datasets, and scalable digital infrastructure will strengthen long-term competitive positioning across global pharmaceutical innovation networks.

Pharmaceutical companies are aggressively deploying AI platforms to reduce drug discovery timelines, improve molecule prediction accuracy, and optimize clinical trial success rates. AI-assisted screening systems lowered preclinical research timelines by nearly 55% while increasing candidate identification efficiency by 48% across oncology and rare disease programs. In the United States, over 65% of top pharmaceutical manufacturers integrated machine learning into early-stage R&D workflows by 2026 following rising pressure to reduce late-stage trial failures and patent cliff exposure. The expansion of biologics pipelines and precision medicine programs is also driving enterprise-scale AI investments. Companies are responding through strategic acquisitions, cloud-computing partnerships, and AI-focused R&D hubs in Boston, Basel, and Bengaluru to secure faster commercialization cycles and improve portfolio productivity.

Fragmented clinical datasets, interoperability limitations, and rising infrastructure costs continue constraining scalable AI deployment across pharmaceutical operations. Nearly 43% of pharmaceutical firms report integration inefficiencies between legacy laboratory systems and AI analytics platforms, while high-performance computing costs increased approximately 18% due to advanced semiconductor supply constraints. Cross-border data localization regulations in Europe and China are further complicating centralized AI model training and multinational trial analytics. These limitations directly affect deployment consistency, validation timelines, and operational scalability for global pharmaceutical companies. To reduce dependency risks, enterprises are investing in localized cloud infrastructure, federated learning frameworks, and proprietary data ecosystems. Companies with vertically integrated digital infrastructure and standardized clinical datasets are achieving stronger AI deployment efficiency and regulatory alignment.

AI-driven precision therapeutics and biologics optimization are creating high-value opportunities across oncology, immunology, and rare disease treatment pipelines. AI-assisted biomarker discovery improved target validation accuracy by nearly 50%, while automated protein modeling platforms reduced biologics development cycles by approximately 35%. India and South Korea are emerging as cost-efficient AI-enabled pharmaceutical research hubs due to expanding digital healthcare infrastructure and government-backed biotech incentives. The growing adoption of multimodal AI and synthetic biology platforms is also enabling personalized treatment design and decentralized clinical trial expansion. Pharmaceutical companies are increasing investments in AI-native laboratories, genomic analytics partnerships, and digital twin technologies to secure operational advantages in high-complexity therapeutic segments. Firms controlling proprietary patient datasets and AI-assisted biologics workflows are positioned to capture stronger long-term differentiation.

Scaling AI systems across pharmaceutical development environments remains operationally complex due to evolving validation standards, cybersecurity exposure, and workforce capability gaps. Nearly 38% of pharmaceutical executives identify regulatory uncertainty around AI-generated clinical insights as a major deployment barrier, while cyberattacks targeting healthcare and life sciences networks increased over 30% between 2024 and 2026. AI model drift and inconsistent training datasets are also affecting reproducibility across multinational clinical operations. Japan and Germany face growing shortages of AI-specialized pharmaceutical data scientists, limiting enterprise-scale implementation speed. These challenges directly impact deployment reliability, compliance consistency, and long-term operational sustainability. Companies are responding through secure cloud infrastructure investments, AI governance frameworks, and partnerships with specialized research institutions to improve validation transparency and scalable deployment resilience.

• Generative AI Pipeline Expansion Pharmaceutical companies are scaling generative AI platforms across molecular simulation and compound optimization workflows, reducing lead candidate identification time by nearly 45% and lowering early-stage screening costs by 28%. More than 58% of large pharmaceutical enterprises integrated generative AI into discovery operations by 2026 following intensified pressure to improve R&D productivity. Companies in the United States and Switzerland are restructuring research partnerships with semiconductor and cloud providers to secure computational capacity for large-scale biologics modeling.

• Decentralized Clinical Trial Adoption AI-enabled decentralized clinical trial systems increased remote patient monitoring deployment by approximately 52%, while digital recruitment platforms improved patient matching accuracy by 37%. Regulatory flexibility around hybrid trial frameworks in the United Kingdom and Singapore accelerated enterprise adoption of AI-driven compliance analytics and automated documentation systems. Pharmaceutical companies are expanding CRO partnerships and deploying multilingual AI assistants to improve enrollment consistency and reduce operational delays across cross-border studies.

• Predictive Manufacturing Optimization AI-integrated pharmaceutical manufacturing facilities reduced batch deviation rates by nearly 25% and improved production scheduling efficiency by 33% through predictive maintenance and real-time process analytics. Supply-chain disruptions affecting active pharmaceutical ingredients pushed manufacturers in India and Germany to strengthen AI-driven inventory forecasting systems. Companies are prioritizing smart factory modernization and digital twin deployment to stabilize output consistency and reduce material waste across biologics manufacturing networks.

• Multimodal Data Integration Growth Pharmaceutical enterprises are increasingly integrating genomic datasets, imaging records, and electronic health data into unified AI ecosystems, improving biomarker identification precision by over 40%. More than 46% of advanced pharmaceutical research centers deployed multimodal AI platforms by 2026 to strengthen personalized medicine development. Companies are responding through acquisitions of specialized analytics firms and expansion of proprietary clinical data ecosystems, creating stronger differentiation in oncology, immunology, and rare disease therapeutic pipelines.

Machine Learning remains the leading segment within the AI in pharmaceuticals market due to its scalability across drug discovery, trial analytics, and manufacturing optimization workflows. More than 61% of pharmaceutical AI deployments in 2026 relied on machine learning algorithms for predictive modeling, molecule screening, and clinical data interpretation. Its dominance is driven by lower integration complexity and stronger compatibility with existing pharmaceutical data infrastructure compared with emerging AI architectures. Predictive Analytics also maintains strong strategic relevance through demand for supply-chain forecasting and treatment outcome modeling, while Natural Language Processing continues expanding across regulatory documentation automation and scientific literature analysis.

Deep Learning is emerging as the fastest-growing type as pharmaceutical companies increase investments in biologics modeling, protein structure prediction, and multimodal data integration. Deep learning platforms improved molecular prediction accuracy by nearly 42% compared with traditional computational systems, particularly in oncology and genomic research. Computer Vision adoption is also increasing in pathology imaging and quality inspection environments where automated analysis reduced diagnostic review times by approximately 35%. Companies are strengthening product portfolios through AI-native platform development, semiconductor partnerships, and cloud-based deployment expansion to secure long-term competitive differentiation across pharmaceutical R&D ecosystems.

According to a 2026 enterprise AI adoption assessment conducted by a leading pharmaceutical technology consortium, nearly 67% of global pharmaceutical manufacturers identified machine learning as the most operationally mature AI framework for clinical and commercial deployment environments.

Drug Discovery remains the dominant application segment due to its direct impact on reducing research timelines, improving target identification, and optimizing compound screening productivity. AI-assisted drug discovery platforms reduced early-stage candidate screening cycles by approximately 50% while improving molecule validation efficiency by 43% across oncology and rare disease pipelines. Pharmaceutical companies in the United States and Japan continue concentrating investments in AI-enabled molecular simulation and biologics development systems to reduce dependence on conventional trial-and-error research methods. Clinical Trial Optimization is also expanding steadily as companies automate patient recruitment, protocol matching, and compliance workflows to improve operational consistency.

Personalized Medicine is emerging as the fastest-growing application due to rising adoption of genomic analytics and AI-driven biomarker identification systems. AI-assisted personalized treatment workflows improved patient stratification accuracy by nearly 38%, particularly in immunology and precision oncology segments. Medical Imaging Analysis is gaining relevance through automated pathology interpretation, while Pharmacovigilance platforms are strengthening adverse event detection capabilities across post-market surveillance operations. Supply Chain Management applications are also becoming operationally critical as pharmaceutical manufacturers deploy predictive inventory analytics and logistics automation to manage active ingredient sourcing volatility and improve manufacturing resilience.

A 2025 multinational pharmaceutical operations survey reported that over 59% of enterprise drug development teams expanded AI-assisted discovery and clinical optimization tools into at least two additional therapeutic programs within 18 months of initial deployment.

Pharmaceutical Companies represent the leading end-user segment due to their large-scale R&D infrastructure, extensive clinical trial operations, and rising investments in AI-enabled drug development platforms. More than 64% of enterprise pharmaceutical firms integrated AI across at least three operational functions by 2026, including molecular screening, manufacturing analytics, and regulatory workflow automation. Their demand concentration is supported by expanding biologics pipelines and increasing pressure to reduce late-stage trial failure rates. Biotechnology Companies are also accelerating adoption through specialized AI applications in genomic research and precision therapeutics, particularly within smaller high-innovation development environments.

Contract Research Organizations (CROs) are emerging as the fastest-growing end-user group as pharmaceutical outsourcing activity expands across decentralized trials, data analytics, and AI-assisted compliance management. AI integration improved CRO patient recruitment efficiency by approximately 36% while reducing protocol processing timelines by nearly 28%. Research Institutes continue strengthening adoption in computational biology and protein modeling, while Hospitals & Clinics are deploying AI platforms for imaging interpretation and precision treatment planning. Technology providers are responding through subscription-based AI platforms, modular deployment models, and customized analytics ecosystems tailored to enterprise-scale pharmaceutical and clinical environments.

An international life sciences digital transformation study released in 2026 found that nearly 54% of CROs expanded AI-focused service capabilities following increased pharmaceutical demand for decentralized clinical operations and automated trial management infrastructure.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 44.8% between 2026 and 2033.

Advanced AI Infrastructure Driving Enterprise-Scale Pharmaceutical Transformation

North America maintains leadership in the AI in pharmaceuticals market through strong biopharma infrastructure, advanced cloud computing capacity, and large-scale AI deployment across drug discovery and clinical operations. The region represented approximately 41% market share in 2025, supported by high enterprise AI integration among pharmaceutical manufacturers and research organizations. More than 66% of large pharmaceutical firms in the United States deployed AI-enabled molecular modeling and predictive analytics systems across multiple therapeutic programs. Strategic partnerships between pharmaceutical companies and hyperscale cloud providers accelerated computational biology expansion, while AI-assisted manufacturing analytics improved production efficiency by nearly 27%. Regulatory digitization initiatives and increasing biologics development activity continue strengthening regional deployment concentration.

United States Market Outlook: The United States remains the largest operational hub for AI-enabled pharmaceutical innovation due to strong venture capital activity, advanced semiconductor access, and mature clinical research infrastructure. More than 70% of top pharmaceutical enterprises expanded AI-driven R&D investments by 2026, particularly across oncology and rare disease development pipelines. Boston and California continue attracting AI-biopharma collaborations focused on generative molecular simulation, decentralized clinical trials, and high-performance computing integration for precision therapeutics.

Regulatory Alignment Accelerating AI-Driven Drug Development

Europe is strengthening its position through AI-integrated pharmaceutical modernization, advanced regulatory harmonization, and sustainability-focused manufacturing optimization. The region accounted for nearly 27% of global deployment activity in 2025, supported by strong adoption across Germany, Switzerland, and the United Kingdom. Pharmaceutical manufacturers increasingly deployed AI-assisted compliance analytics and digital quality management systems to improve traceability and reduce production deviations by approximately 22%. Europe’s emphasis on data governance and ethical AI frameworks is also accelerating enterprise investments in federated learning infrastructure and secure clinical data ecosystems. Cross-border research collaboration programs are supporting broader adoption of AI-enabled biologics development and precision medicine initiatives.

Germany Market Outlook: Germany continues leading European pharmaceutical AI deployment through strong industrial automation capability and advanced life sciences manufacturing infrastructure. Nearly 58% of large pharmaceutical production facilities in Germany integrated AI-driven predictive maintenance and process analytics platforms by 2026 to improve operational consistency and reduce downtime. The country’s emphasis on Industry 4.0 integration and regulated digital health expansion is strengthening partnerships between pharmaceutical manufacturers, AI developers, and research institutions focused on scalable biologics production systems.

Large-Scale Digitalization Reshaping Pharmaceutical Operations

Asia-Pacific is emerging as the fastest-scaling AI in pharmaceuticals market due to expanding pharmaceutical manufacturing capacity, cost-efficient digital infrastructure, and rapid enterprise AI adoption. The region contributed approximately 24% of global market activity in 2025, with China, India, Japan, and South Korea driving deployment expansion across research and manufacturing environments. More than 52% of newly established pharmaceutical production facilities in Asia-Pacific integrated AI-enabled automation systems by 2026 to strengthen quality control and inventory forecasting. Governments are also supporting biotechnology modernization through semiconductor investment programs and AI-focused healthcare innovation incentives. Pharmaceutical outsourcing growth and decentralized trial adoption are further accelerating enterprise deployment across the region.

China Market Outlook: China remains the region’s largest AI-pharmaceutical deployment center due to extensive manufacturing scale, strong domestic AI ecosystems, and state-backed biotechnology modernization programs. AI-assisted pharmaceutical manufacturing systems improved production scheduling efficiency by approximately 34% across several large-scale biologics facilities by 2026. The country is also expanding localized AI semiconductor development and clinical data infrastructure to reduce dependence on external computing supply chains while strengthening precision medicine and genomic analytics capabilities.

Digital Healthcare Expansion Supporting AI Adoption

South America is gradually increasing AI deployment across pharmaceutical research, manufacturing, and clinical operations as healthcare digitalization investments expand. Brazil and Argentina account for the majority of regional adoption activity, supported by improving cloud infrastructure and growing pharmaceutical outsourcing demand. Approximately 38% of large pharmaceutical distributors in South America integrated AI-assisted inventory forecasting systems by 2026 to reduce supply variability and improve logistics coordination. However, infrastructure fragmentation and limited high-performance computing access continue affecting deployment scalability. Companies are responding through regional partnerships, localized data management systems, and contract-based AI deployment models to improve operational accessibility and regulatory compliance across fragmented healthcare networks.

Brazil Market Outlook: Brazil leads the South American market through expanding pharmaceutical manufacturing operations and increasing digital health integration across private healthcare systems. AI-assisted supply-chain analytics reduced pharmaceutical stockout incidents by nearly 21% in several major urban distribution networks during 2026. The country is also strengthening public-private partnerships focused on clinical data digitization, decentralized trial management, and AI-enabled treatment optimization to improve operational efficiency across high-demand therapeutic segments.

Healthcare Modernization and AI Investment Expansion

The Middle East & Africa market is advancing through healthcare infrastructure modernization, biotechnology investment expansion, and government-backed digital transformation programs. Gulf countries are leading AI-pharmaceutical deployment activity through national healthcare digitization initiatives and increasing investments in precision medicine infrastructure. Approximately 31% of newly modernized pharmaceutical facilities in the Gulf region integrated AI-driven process monitoring systems by 2026 to improve manufacturing traceability and operational efficiency. Africa continues developing AI-assisted pharmaceutical logistics and clinical analytics capabilities despite uneven infrastructure availability. Enterprise partnerships with global technology providers are helping improve cloud accessibility, cybersecurity readiness, and AI deployment scalability across emerging healthcare ecosystems.

Saudi Arabia Market Outlook: Saudi Arabia is becoming a strategic pharmaceutical AI investment hub through large-scale healthcare modernization programs and advanced biotechnology infrastructure development. More than 40% of newly deployed pharmaceutical analytics systems in the country incorporated AI-enabled predictive modeling capabilities by 2026 to improve treatment planning and manufacturing oversight. National digital health expansion initiatives and increasing partnerships with international pharmaceutical technology firms are accelerating adoption across hospital networks, biologics production, and clinical research environments.

The AI in pharmaceuticals market is shaped by competition between global technology leaders, pharmaceutical innovators, specialized AI-biotech firms, and cloud infrastructure providers. Companies such as IBM, Microsoft, Google, NVIDIA, and Insilico Medicine compete aggressively with enterprise pharmaceutical groups including Pfizer, Roche, and Novartis over proprietary AI platforms, clinical datasets, and accelerated drug discovery capabilities. The top five players collectively control nearly 46% of advanced enterprise AI-pharma deployment activity. Competition is increasingly driven by computational speed, model accuracy, cloud scalability, and integration efficiency, with AI-assisted drug screening reducing discovery timelines by over 50% and manufacturing analytics improving operational efficiency by approximately 25%. Companies are strengthening market positions through vertical integration, cross-industry partnerships, and acquisitions of niche AI research firms. The market is also experiencing consolidation pressure as semiconductor access and proprietary healthcare datasets become strategic barriers. Long-term competitiveness depends on scalable infrastructure, validated clinical AI models, and strong pharmaceutical ecosystem integration capabilities.

IBM

Microsoft

NVIDIA

Insilico Medicine

BenevolentAI

Recursion Pharmaceuticals

Exscientia

Atomwise

Pfizer

Roche

Novartis

AstraZeneca

Schrödinger Inc.

AI in pharmaceuticals is rapidly shifting from isolated analytics tools to integrated discovery and manufacturing ecosystems powered by machine learning, generative AI, and multimodal data platforms. By 2026, nearly 64% of large pharmaceutical companies deployed AI-driven molecular modeling systems to accelerate target identification and toxicity prediction workflows. Machine learning-based screening platforms reduced early-stage compound validation time by approximately 52%, while predictive manufacturing analytics improved production scheduling efficiency by 28%, strengthening operational scalability and reducing laboratory resource dependency across biologics and precision medicine programs.

Emerging technologies including generative protein design, autonomous laboratory orchestration, and federated learning are reshaping pharmaceutical R&D infrastructure. Deep learning-driven biologics simulation platforms improved molecular prediction accuracy by nearly 41% compared with legacy computational chemistry systems, while AI-enabled decentralized trial systems reduced patient recruitment delays by 34%. Pharmaceutical companies are expanding partnerships with cloud providers and semiconductor firms to secure high-performance computing capacity, particularly across the United States, Switzerland, and Japan where AI-biopharma integration is becoming a competitive differentiator.

Between 2026 and 2028, agentic AI systems, digital twins, and self-optimizing manufacturing environments will intensify operational automation across pharmaceutical value chains. Companies investing early in proprietary AI models, multimodal clinical datasets, and AI-native infrastructure will secure faster commercialization cycles, stronger compliance efficiency, and long-term innovation leadership.

January 2026 – NVIDIA and Eli Lilly launched a joint AI co-innovation laboratory focused on accelerating drug discovery, manufacturing analytics, and multimodal pharmaceutical modeling with planned infrastructure investments reaching USD 1 billion over five years. The initiative strengthens AI-led biologics development and supply-chain resilience. Source: investor.nvidia.com

February 2026 – Dassault Systèmes partnered with NVIDIA to build an industrial AI platform integrating virtual twin technology into pharmaceutical and life sciences workflows. The deployment framework improved simulation-based operational modeling efficiency by nearly 30%, supporting faster manufacturing optimization and scalable digital laboratory environments. Source: nvidianews.nvidia.com

March 2026 – NVIDIA expanded its BioNeMo platform adoption across life sciences organizations, enabling AI-driven molecular design, automated biomolecular modeling, and autonomous laboratory workflows. The platform supported more than 1,600 biotechnology and pharmaceutical organizations, accelerating industrial-scale AI deployment within advanced therapeutic research environments.

May 2026 – Researchers evaluating curated pharmaceutical AI systems reported that specialized AI asset-discovery platforms identified 3.2 times more verified drug candidates than frontier general-purpose language models during oncology and immunology benchmarking. The findings reinforced enterprise demand for domain-specific AI architectures over generalized generative models. Source: arxiv.org

The AI in pharmaceuticals market report provides comprehensive analysis across key technology types including machine learning, deep learning, natural language processing, predictive analytics, and computer vision. The study evaluates operational deployment patterns across drug discovery, clinical trial optimization, personalized medicine, pharmacovigilance, medical imaging analysis, and pharmaceutical supply-chain management. More than 60% of enterprise pharmaceutical AI deployments are concentrated in discovery and biologics development workflows, while decentralized trial systems and multimodal analytics platforms continue expanding across precision therapeutics environments.

The report covers strategic adoption trends across pharmaceutical companies, biotechnology firms, research institutes, hospitals, clinics, and contract research organizations operating in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It highlights enterprise investment priorities, AI infrastructure modernization, cloud integration trends, and competitive positioning strategies shaping deployment between 2026 and 2033. The analysis also examines emerging areas including autonomous laboratories, digital twins, agentic AI systems, and AI-enabled biologics manufacturing to support expansion planning, operational optimization, and long-term technology alignment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1940 Million |

|

Market Revenue in 2033 |

USD 144709.27 Million |

|

CAGR (2026 - 2033) |

41.12% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |