Reports

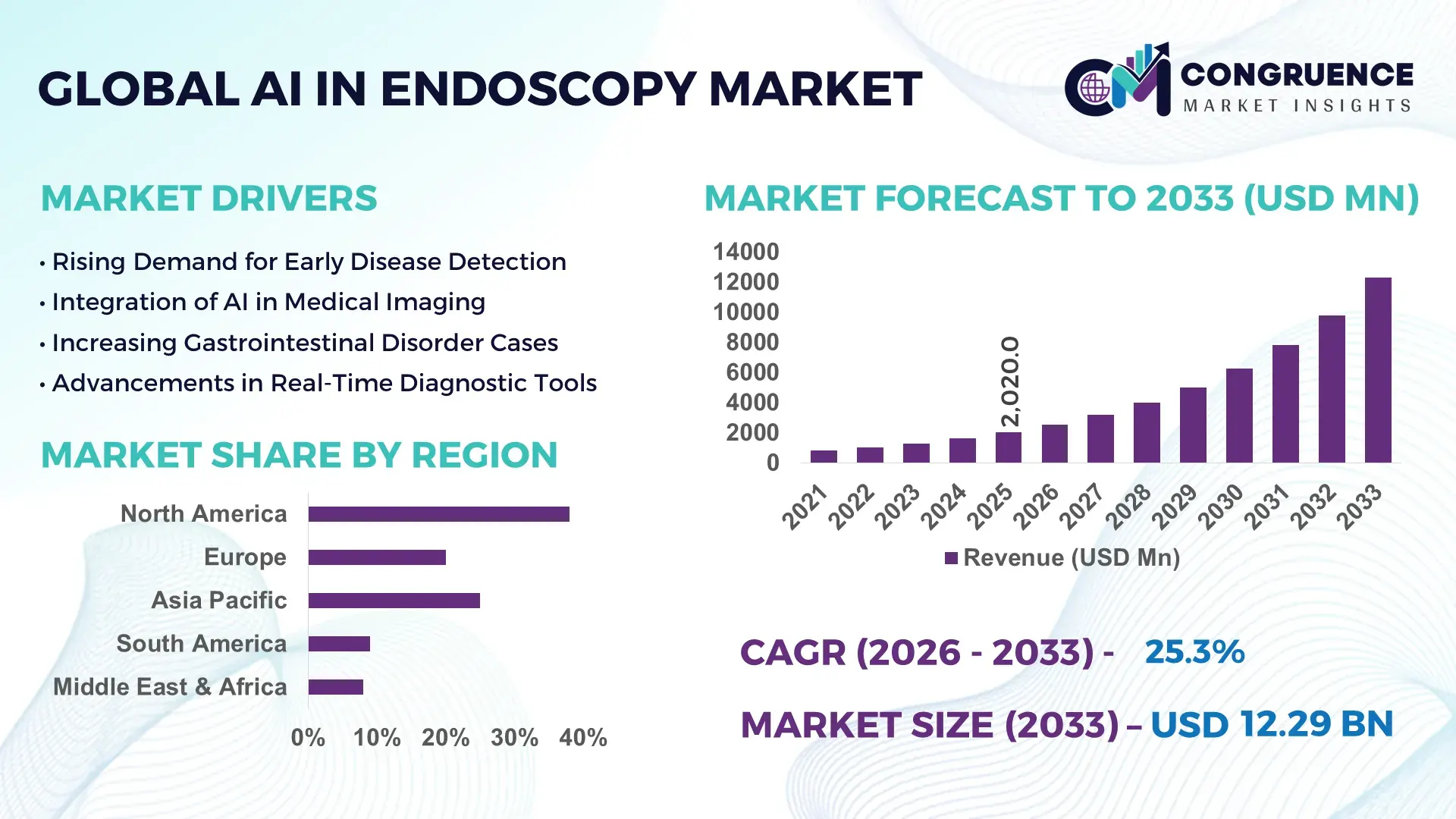

The Global AI In Endoscopy Market was valued at USD 2020 Million in 2025 and is anticipated to reach a value of USD 12288.94 Million by 2033 expanding at a CAGR of 25.32% between 2026 and 2033. Growth is driven by the increasing integration of artificial intelligence in diagnostic imaging to enhance real-time detection accuracy and improve clinical outcomes in minimally invasive procedures.

The United States continues to demonstrate strong clinical deployment and technological advancement in AI-driven endoscopy systems, supported by over 6,000 hospitals incorporating advanced imaging technologies. More than 70% of large healthcare institutions utilize AI-assisted diagnostic tools, particularly in gastrointestinal procedures, which account for nearly 60% of total applications. Investments in digital health technologies exceeded USD 15 billion in 2024, with a significant share allocated to AI-integrated medical imaging. Additionally, over 40 regulatory-approved AI endoscopy solutions are actively deployed, improving lesion detection rates by up to 30% and enhancing procedural efficiency across high-volume clinical environments.

Market Size & Growth: Valued at USD 2020 Million in 2025, projected to reach USD 12288.94 Million by 2033, growing at 25.32% CAGR due to rising demand for precision diagnostics and workflow automation.

Top Growth Drivers: AI-assisted detection improves polyp detection rates by 35%, reduces diagnostic errors by 25%, and enhances procedural efficiency by 40%.

Short-Term Forecast: By 2028, AI integration is expected to reduce diagnostic turnaround time by 30% and improve clinical workflow productivity by 28%.

Emerging Technologies: Deep learning-based computer-aided detection (CADe), real-time video analytics, and cloud-integrated endoscopic imaging platforms.

Regional Leaders: North America projected at USD 4500 Million by 2033 with advanced hospital adoption; Europe at USD 3200 Million driven by regulatory-backed innovation; Asia-Pacific at USD 2800 Million with rapid healthcare infrastructure expansion.

Consumer/End-User Trends: Hospitals account for over 65% usage, with increasing adoption in ambulatory surgical centers and specialty clinics focused on minimally invasive treatments.

Pilot or Case Example: In 2024, a Japan-based clinical implementation demonstrated a 32% increase in early-stage cancer detection using AI-assisted colonoscopy systems.

Competitive Landscape: Market leader holds approximately 22% share, followed by Olympus, Fujifilm, Medtronic, Pentax Medical, and Boston Scientific.

Regulatory & ESG Impact: Growing compliance with AI transparency standards and data privacy regulations, alongside energy-efficient imaging systems reducing device power consumption by 15%.

Investment & Funding Patterns: Over USD 3 billion invested globally in AI healthcare imaging startups between 2023 and 2025, driven by venture capital and strategic collaborations.

Innovation & Future Outlook: Integration of AI with robotic endoscopy and predictive analytics is transforming diagnostic precision and enabling personalized treatment pathways.

AI in endoscopy is expanding across gastroenterology, pulmonology, and urology, with gastrointestinal applications contributing more than 55% of overall demand. Advanced innovations such as real-time lesion characterization, automated reporting systems, and AI-driven workflow optimization are improving clinical efficiency and decision-making accuracy. Regulatory frameworks are increasingly focused on algorithm validation and patient data security, ensuring reliable deployment. Asia-Pacific is experiencing strong consumption growth due to expanding healthcare infrastructure and large-scale screening programs. Emerging trends include AI-enabled capsule endoscopy and integration with telemedicine platforms, enabling remote diagnostics and scalable healthcare delivery systems.

AI-powered computer-aided detection delivers up to 35% improvement in adenoma detection rates compared to conventional white-light endoscopy, significantly enhancing diagnostic precision. North America dominates in procedural volume, while Asia-Pacific leads in adoption with over 45% of healthcare institutions integrating AI-based imaging systems. By 2028, real-time AI analytics is expected to reduce procedural errors by 30% and improve diagnostic throughput by 25%, strengthening clinical efficiency.

Healthcare providers are aligning with ESG-focused strategies, targeting a 20% reduction in operational inefficiencies and improved energy optimization in medical imaging systems by 2030. In 2024, Japan achieved a 32% increase in early-stage gastrointestinal cancer detection through nationwide deployment of AI-assisted colonoscopy programs. Strategic collaborations between medical technology firms and AI developers are accelerating innovation in cloud-based diagnostics and predictive analytics platforms.

The AI In Endoscopy Market is increasingly positioned as a critical enabler of precision medicine, regulatory compliance, and sustainable healthcare transformation, supported by measurable improvements in diagnostic outcomes and operational performance.

The AI In Endoscopy Market is shaped by rapid advancements in artificial intelligence, growing demand for early disease detection, and increasing adoption of minimally invasive diagnostic procedures. Integration of machine learning algorithms into endoscopic systems enables real-time image analysis and clinical decision support, improving diagnostic consistency. Rising healthcare investments and supportive regulatory frameworks are accelerating market expansion. However, high implementation costs and data privacy concerns continue to influence adoption strategies across regions.

The rising incidence of gastrointestinal cancers has significantly increased demand for advanced diagnostic solutions, with screening programs implemented across more than 80 countries. AI-assisted endoscopy enhances adenoma detection rates by up to 35%, reducing missed lesions and improving patient outcomes. Healthcare facilities adopting AI-based systems report 25–30% improvement in diagnostic accuracy and reduced variability among clinicians. Government initiatives promoting preventive healthcare and early screening are further accelerating adoption.

AI-enabled endoscopic systems require substantial capital investment, often costing 20–30% more than traditional equipment. Smaller healthcare providers face financial limitations due to additional expenses related to system integration, training, and maintenance. Interoperability challenges with existing hospital IT infrastructure and limited reimbursement frameworks in certain regions further restrict adoption. Regulatory complexities and data security requirements also contribute to higher deployment costs and longer implementation timelines.

The rapid expansion of telemedicine is creating significant opportunities for AI-integrated endoscopy solutions, enabling remote diagnostics and expert consultations. AI-powered cloud platforms facilitate real-time sharing and analysis of endoscopic data, improving access to specialized care in underserved regions. Capsule endoscopy integrated with AI analytics is witnessing adoption growth exceeding 20% annually in emerging markets, enhancing screening accessibility and reducing healthcare disparities.

Strict regulatory requirements for AI-based medical devices demand extensive clinical validation and algorithm transparency, often extending approval timelines beyond 18–24 months. Variability in patient datasets across regions affects algorithm performance, requiring continuous updates and validation. Data privacy concerns and cybersecurity risks further complicate deployment, particularly for cloud-based systems. These challenges increase development costs and slow the commercialization of advanced AI-enabled endoscopy solutions.

• Real-Time AI Detection Enhancing Diagnostic Accuracy by Over 35%: AI-powered computer-aided detection systems are increasingly integrated into endoscopic workflows, improving adenoma detection rates by up to 35% and reducing missed lesions by nearly 25%. More than 60% of advanced endoscopy centers now deploy real-time AI analytics, enabling clinicians to identify abnormalities within milliseconds, significantly improving early-stage cancer detection outcomes.

• Expansion of AI-Integrated Capsule Endoscopy with 20%+ Adoption Growth: Capsule endoscopy combined with AI-based image analysis is witnessing rapid adoption, particularly in remote diagnostics. Clinical usage has increased by over 20% annually, with AI algorithms capable of analyzing more than 50,000 images per procedure, reducing physician review time by approximately 40% while maintaining diagnostic precision across gastrointestinal assessments.

• Cloud-Based Endoscopy Platforms Improving Workflow Efficiency by 30%: Cloud-integrated AI solutions are transforming data management and diagnostic workflows, with hospitals reporting up to 30% improvement in operational efficiency. Over 45% of large healthcare facilities now utilize cloud-enabled endoscopy systems for real-time data sharing, remote consultations, and centralized analytics, reducing reporting delays and enhancing multi-specialist collaboration.

• Increasing Regulatory Approvals Driving 25% Rise in Clinical Deployment: The number of AI-enabled endoscopy systems receiving regulatory clearance has increased by more than 25% between 2023 and 2025. Over 40 validated AI solutions are now clinically deployed, supporting standardized diagnostic protocols and improving consistency across practitioners, with up to 28% reduction in inter-operator variability during procedures.

The AI In Endoscopy Market is segmented by type, application, and end-user, each contributing to evolving clinical adoption patterns. By type, computer-aided detection systems dominate with over 45% share, driven by real-time diagnostic capabilities, while computer-aided diagnosis tools are rapidly expanding. By application, gastrointestinal procedures account for more than 55% of usage due to high screening volumes, followed by pulmonology and urology applications. In terms of end-users, hospitals lead with over 65% adoption, supported by advanced infrastructure, while ambulatory surgical centers and specialty clinics are witnessing increased uptake due to demand for minimally invasive and cost-efficient diagnostic solutions.

Computer-aided detection (CADe) systems currently dominate the AI In Endoscopy Market, accounting for approximately 45% of total adoption due to their ability to identify polyps and lesions in real time with detection accuracy improvements of up to 35%. Computer-aided diagnosis (CADx) systems hold around 30% share, focusing on lesion characterization and decision support, enhancing diagnostic confidence among clinicians. However, AI-based endoscopic imaging platforms integrating both detection and diagnostic capabilities are emerging as the fastest-growing segment, expanding at an estimated growth rate exceeding 28% annually, driven by demand for comprehensive clinical solutions and workflow integration.

Other types, including AI-enabled capsule endoscopy and robotic-assisted endoscopy systems, collectively contribute nearly 25% of the market, gaining traction in specialized applications such as small intestine imaging and minimally invasive procedures. These solutions offer improved patient comfort and expanded diagnostic reach, particularly in outpatient settings.

Gastrointestinal endoscopy remains the leading application segment, accounting for over 55% of total market usage due to the high prevalence of colorectal and digestive disorders. AI integration in this segment enhances adenoma detection rates by up to 35%, improving early diagnosis and patient outcomes. Pulmonology applications hold approximately 20% share, utilizing AI for bronchoscopy procedures to detect lung abnormalities with improved accuracy. Urology and other specialized applications collectively account for around 25%, focusing on bladder and urinary tract diagnostics.

Among these, capsule endoscopy and remote diagnostic applications represent the fastest-growing segment, expanding at an estimated rate above 26% annually, driven by increasing demand for non-invasive procedures and telemedicine integration. AI algorithms analyzing large volumes of imaging data enable faster and more precise diagnostics, particularly in underserved regions.

Hospitals dominate the AI In Endoscopy Market, accounting for over 65% of total adoption due to their advanced infrastructure, high patient volumes, and access to skilled specialists. Large healthcare institutions have integrated AI into more than 70% of their endoscopic procedures, improving diagnostic accuracy and reducing procedure time by up to 25%. Ambulatory surgical centers represent approximately 20% of the market, benefiting from AI-driven efficiency and reduced operational costs in outpatient settings.

Specialty clinics and diagnostic centers collectively contribute around 15%, focusing on targeted procedures and niche diagnostic services. These facilities are increasingly adopting AI solutions to enhance service quality and attract patient volumes through advanced diagnostic capabilities. Ambulatory surgical centers are the fastest-growing end-user segment, expanding at an estimated rate exceeding 27% annually, driven by increasing preference for minimally invasive procedures and cost-effective treatment options. Adoption rates in these centers have risen by over 30% in the past three years, supported by compact and scalable AI-enabled systems.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27.10% between 2026 and 2033.

Europe follows with approximately 28% share, supported by regulatory-driven adoption, while Asia-Pacific holds nearly 24% with rapidly expanding healthcare infrastructure. South America and Middle East & Africa collectively contribute around 10%, with increasing investments in digital healthcare. Over 65% of AI-enabled endoscopy deployments are concentrated in developed regions, while emerging markets are witnessing adoption growth exceeding 30% in hospital networks. More than 50% of new installations globally are AI-integrated systems, reflecting strong demand for advanced diagnostic capabilities.

How is advanced healthcare infrastructure accelerating AI-driven diagnostic adoption?

This region holds approximately 38% market share, driven by strong demand from hospitals and specialized diagnostic centers. Over 70% of large healthcare institutions have adopted AI-assisted endoscopy solutions, particularly in gastrointestinal diagnostics. Favorable regulatory frameworks, including accelerated approvals for AI-based medical devices, are supporting rapid deployment. Continuous digital transformation and integration of cloud-based imaging platforms are enhancing clinical workflows by up to 30%. A key player, Medtronic, is advancing AI-powered colonoscopy platforms to improve detection accuracy. Consumer behavior reflects high reliance on technologically advanced procedures, with over 65% of patients preferring minimally invasive diagnostics supported by AI tools.

Why is regulatory compliance shaping innovation in intelligent endoscopic systems?

Europe accounts for nearly 28% of the market, with key countries such as Germany, the UK, and France leading adoption. Regulatory bodies emphasize AI transparency and explainability, influencing product development and deployment. Over 60% of healthcare providers prioritize compliance-driven AI solutions, particularly in cancer screening programs. Adoption of AI-enabled imaging technologies has increased by more than 25% across major hospitals. Companies such as Olympus are strengthening their presence through advanced endoscopic imaging innovations. Consumer behavior indicates a strong preference for clinically validated and regulation-compliant technologies, driving demand for explainable AI systems in diagnostic procedures.

What factors are accelerating digital healthcare transformation and AI adoption?

Asia-Pacific ranks as the fastest-growing region, holding around 24% market share, with China, Japan, and India as major contributors. Over 40% of new healthcare infrastructure projects in this region incorporate AI-enabled diagnostic systems. Rapid expansion of hospital networks and government-led screening initiatives are driving demand. Japan leads in technological innovation, with AI-assisted endoscopy adoption exceeding 50% in advanced medical centers. Fujifilm is actively developing AI-integrated imaging systems to enhance diagnostic efficiency. Consumer behavior is influenced by increasing healthcare accessibility and mobile-based diagnostic platforms, with adoption rates rising by over 30% in urban healthcare facilities.

How are healthcare investments and policy reforms influencing diagnostic advancements?

South America represents approximately 6% of the global market, led by Brazil and Argentina. Increasing healthcare investments and modernization of diagnostic facilities are supporting AI adoption. Government initiatives promoting early disease detection are driving deployment of AI-based endoscopy systems across public hospitals. Infrastructure improvements have resulted in over 20% increase in advanced diagnostic installations. Regional adoption is supported by trade policies encouraging import of medical technologies. Consumer behavior reflects growing demand for affordable and efficient diagnostic solutions, with more than 35% of healthcare providers transitioning toward AI-assisted procedures.

How is technological modernization supporting advanced diagnostic capabilities?

Middle East & Africa accounts for nearly 4% of the market, with key growth in the UAE and South Africa. Healthcare modernization initiatives and increasing investments in digital infrastructure are accelerating AI adoption. Over 25% of new hospital projects include AI-integrated diagnostic systems. Strategic partnerships and trade agreements are facilitating technology transfer and deployment. Regional healthcare providers are focusing on improving diagnostic accuracy and reducing procedural time by up to 20%. Consumer behavior shows increasing preference for technologically advanced treatments, particularly in urban centers where AI-enabled healthcare solutions are gaining traction.

United States – 34% share: AI In Endoscopy market dominance driven by advanced healthcare infrastructure, high adoption of AI-assisted diagnostics, and strong regulatory support for medical AI innovations.

China – 18% share: AI In Endoscopy market growth supported by large-scale hospital expansion, increasing government healthcare investments, and rapid integration of AI technologies in diagnostic imaging.

The AI In Endoscopy Market is moderately consolidated, with the top five companies accounting for approximately 55% of the total market share. More than 25 active global and regional players are competing through technological innovation, strategic collaborations, and product differentiation. Leading companies are focusing on integrating deep learning algorithms with endoscopic imaging systems to enhance diagnostic accuracy by over 30%.

Strategic partnerships between medical device manufacturers and AI technology firms have increased by nearly 40% between 2023 and 2025, accelerating the development of advanced solutions. Product launches featuring real-time analytics and cloud connectivity have grown by over 35%, reflecting strong innovation momentum. Mergers and acquisitions are also shaping the competitive landscape, with companies targeting expansion in emerging markets and strengthening their digital capabilities.

Competitive intensity is further driven by regulatory approvals, with over 40 AI-enabled endoscopy systems receiving clearance globally. Companies are investing heavily in R&D, allocating up to 12–15% of their budgets toward AI development. The market is witnessing increased focus on personalized diagnostics, workflow automation, and integration with telemedicine platforms, positioning innovation as a key differentiator.

Olympus Corporation

Fujifilm Holdings Corporation

Medtronic plc

Boston Scientific Corporation

Pentax Medical

Siemens Healthineers

Karl Storz SE & Co. KG

Stryker Corporation

Ambu A/S

Hoya Corporation

Artificial intelligence technologies in endoscopy are rapidly evolving, with deep learning algorithms enabling real-time image analysis at speeds exceeding 30 frames per second. Computer-aided detection (CADe) systems improve polyp detection accuracy by up to 35%, while computer-aided diagnosis (CADx) tools enhance lesion characterization accuracy by nearly 25%. Integration of convolutional neural networks (CNNs) allows automated identification of abnormalities across more than 50,000 frames per procedure.

Cloud-based AI platforms are now deployed in over 45% of advanced healthcare facilities, enabling remote diagnostics, centralized data storage, and multi-specialist collaboration. Edge computing is also gaining traction, reducing latency by 20% and enabling instant decision support during procedures. AI-powered capsule endoscopy systems can process over 60,000 images per session, reducing physician review time by approximately 40%.

Emerging technologies such as 3D imaging, augmented reality overlays, and robotic-assisted endoscopy are further enhancing procedural precision. More than 30% of newly introduced endoscopy systems now incorporate AI-integrated imaging modules. Additionally, interoperability with electronic health records (EHR) systems is improving workflow efficiency by 25%, enabling seamless integration of patient data and diagnostic outputs across clinical environments.

• In April 2025, Medtronic expanded its GI Genius™ intelligent endoscopy module with enhanced AI algorithms capable of improving adenoma detection rates by over 30%, while integrating real-time visualization features compatible with multiple endoscopy platforms. Source: www.medtronic.com

• In March 2025, Olympus Corporation introduced an upgraded AI-powered endoscopy platform featuring advanced image-enhancement technology and deep learning models, enabling clinicians to achieve up to 27% higher diagnostic accuracy in early-stage gastrointestinal cancer detection. Source: www.olympus-global.com

• In October 2024, Fujifilm launched a next-generation AI-assisted endoscopy system with real-time lesion detection capabilities, supporting faster diagnosis and reducing procedure time by nearly 20% across high-volume clinical settings. Source: www.fujifilm.com

• In June 2024, Boston Scientific advanced its digital endoscopy solutions by integrating AI-driven analytics into its imaging systems, improving procedural efficiency by approximately 25% and enabling enhanced visualization during minimally invasive interventions. Source: www.bostonscientific.com

The AI In Endoscopy Market Report provides a comprehensive evaluation of key industry segments, including technology types, clinical applications, and end-user categories. It covers core technologies such as computer-aided detection, computer-aided diagnosis, capsule endoscopy, and AI-integrated robotic systems, which collectively account for over 70% of current technological adoption. The report analyzes major application areas including gastrointestinal, pulmonology, and urology procedures, with gastrointestinal applications contributing more than 55% of total usage.

Geographically, the report examines five major regions, with North America holding approximately 38% share, followed by Europe at 28% and Asia-Pacific at 24%, while emerging regions collectively contribute around 10%. It highlights adoption trends across hospitals, ambulatory surgical centers, and specialty clinics, where hospitals represent over 65% of total demand.

The scope also includes analysis of regulatory frameworks, digital health integration, and emerging innovations such as AI-enabled capsule endoscopy and cloud-based diagnostic platforms. Additionally, the report evaluates over 25 key market participants, focusing on product innovation, strategic partnerships, and deployment trends across more than 50 countries, providing actionable insights for stakeholders and decision-makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

25.32% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Olympus Corporation, Fujifilm Holdings Corporation, Medtronic plc, Boston Scientific Corporation, Pentax Medical, Siemens Healthineers, Karl Storz SE & Co. KG, Stryker Corporation, Ambu A/S, Hoya Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |