Reports

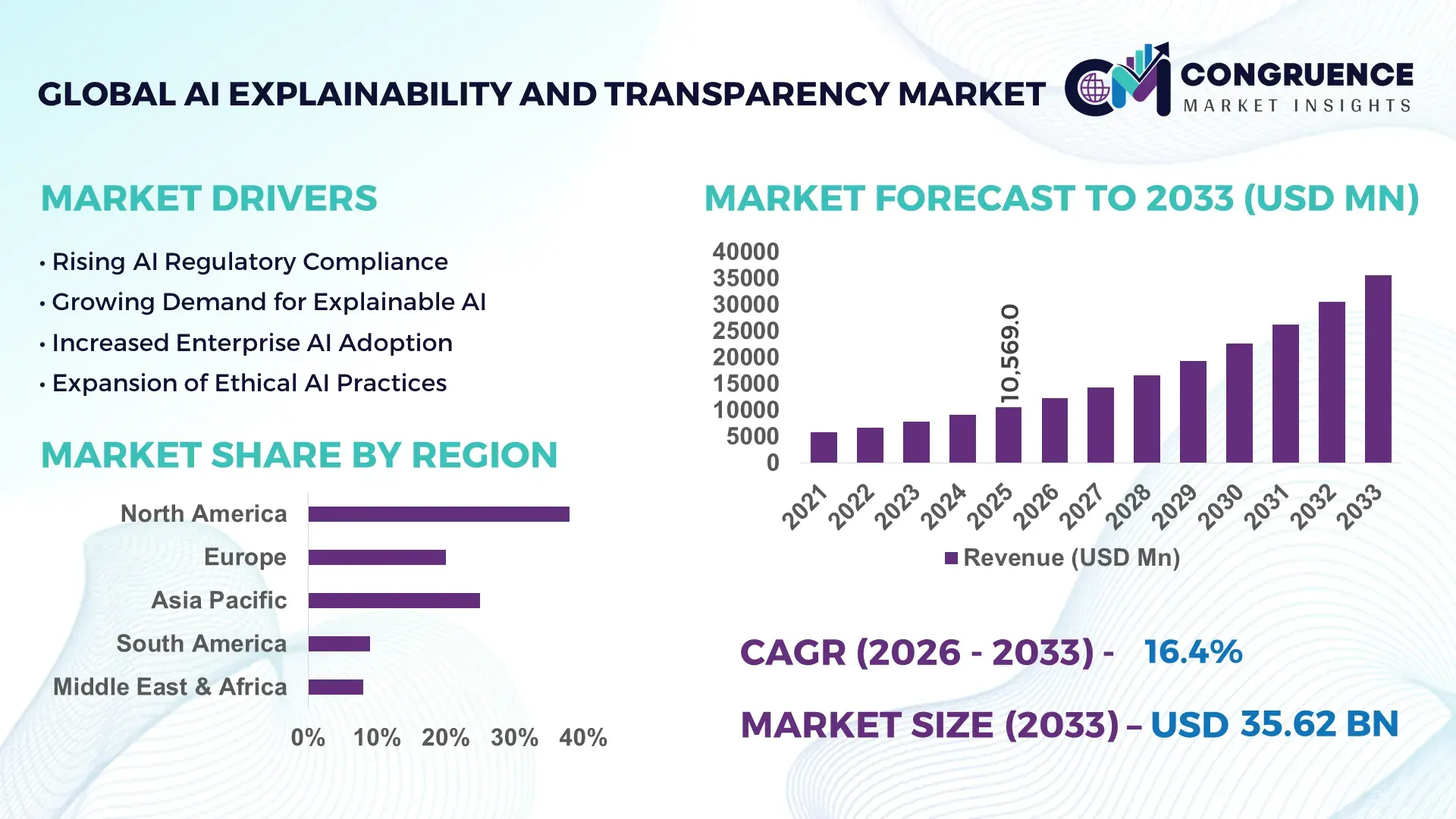

The Global AI Explainability and Transparency Market was valued at USD 10569 Million in 2025 and is anticipated to reach a value of USD 35617.03 Million by 2033 expanding at a CAGR of 16.4% between 2026 and 2033.

Enterprise deployment of explainable AI platforms accelerated by 38% across banking, healthcare, and defense sectors in 2025 as organizations prioritized audit-ready AI models, bias monitoring, and automated compliance reporting to reduce governance costs and improve model trustworthiness. Between 2024 and 2026, stricter AI governance mandates under the EU AI Act, U.S. federal procurement transparency standards, and cross-border data accountability rules reshaped global AI procurement strategies, pushing enterprises toward interpretable machine learning architectures over black-box systems.

The United States dominated the global AI explainability and transparency market with nearly 34% share in 2025, supported by over USD 4.8 billion in enterprise AI governance investments and rapid deployment across financial services, aerospace, and public-sector analytics. More than 61% of large U.S. enterprises integrated explainability dashboards into generative AI workflows, compared with approximately 37% adoption across emerging Asia-Pacific economies. Major cloud and semiconductor firms expanded responsible AI infrastructure spending by over 25% during 2025, while regulated industries increased AI audit frequency by 42% to address litigation, cybersecurity, and compliance risks tied to autonomous decision-making systems.

Organizations prioritizing transparent AI ecosystems are securing faster regulatory approvals, stronger enterprise adoption rates, and lower operational risk exposure in high-growth digital transformation programs.

Market Size & Growth: USD 10.57 billion in 2025 advancing toward USD 35.62 billion by 2033, driven by enterprise AI governance adoption and rising regulatory compliance integration across advanced digital industries.

Top Growth Drivers: Regulatory AI oversight expanded 41%, enterprise AI audit demand rose 36%, and explainable generative AI deployment increased 44% during 2025.

Short-Term Forecast: By 2027, automated model monitoring platforms are projected to reduce AI compliance review time by 31% and improve operational transparency efficiency by 28%.

Emerging Technologies: Explainable generative AI, causal AI analytics, and federated transparency frameworks improved model traceability by 33% while reducing bias detection time by 26%.

Regional Leaders: North America surpassed USD 4.1 billion with strong BFSI adoption, Europe exceeded USD 3 billion under strict AI regulation, and Asia-Pacific crossed USD 2.4 billion through rapid enterprise automation expansion.

Consumer/End-User Trends: Over 58% of enterprises now require explainability features before approving high-risk AI deployments in healthcare, insurance, and cybersecurity operations.

Pilot/Case Example: In 2025, a multinational banking AI audit program reduced false-risk alerts by 29% after integrating transparent decision-tracking algorithms.

Competitive Landscape: Leading vendors controlled approximately 46% market share, with strong competition among enterprise AI software, cloud infrastructure, and governance platform providers.

Regulatory & ESG Impact: AI transparency mandates improved algorithm accountability reporting by 35%, especially across Europe amid expanding digital compliance enforcement.

Investment & Funding: Global investments exceeded USD 6.3 billion in 2025, supported by enterprise partnerships, sovereign AI infrastructure expansion, and responsible AI startup funding.

Innovation & Future Outlook: Autonomous AI governance systems and real-time explainability engines are strengthening enterprise trust, accelerating secure global AI deployment strategies through 2030.

Banking, healthcare, and government analytics collectively contributed over 57% of total industry adoption in 2025 as enterprises intensified focus on interpretable decision systems and audit-ready AI operations. Advanced explainability engines integrated with generative AI platforms improved model validation accuracy by 32%, while Asia-Pacific demand expanded rapidly through large-scale enterprise automation programs. Europe strengthened procurement standards following stricter AI governance enforcement, accelerating transparent AI software deployment across regulated industries. The market is increasingly shifting toward real-time explainability layers embedded directly into enterprise AI infrastructure, setting the stage for broader strategic competition around trusted autonomous systems.

AI explainability and transparency platforms are rapidly transforming from compliance tools into core competitive infrastructure for enterprises deploying autonomous systems, generative AI, and predictive analytics at scale. More than 63% of regulated enterprises integrated explainability protocols into AI procurement frameworks during 2025 as board-level scrutiny intensified around algorithmic accountability, cybersecurity exposure, and litigation risk. Financial institutions and healthcare providers are accelerating capital allocation toward interpretable AI systems to reduce operational uncertainty and improve decision traceability across high-risk workflows. The market is increasingly shifting from post-deployment monitoring toward embedded transparency architecture integrated directly into enterprise AI pipelines.

Global regulatory pressure and cross-border AI governance reforms are forcing organizations to redesign AI deployment strategies around transparency, auditability, and ethical model governance standards. Explainable AI platforms powered by automated causal inference engines improve compliance efficiency by 41% while reducing operational review costs by 29% compared to legacy black-box monitoring systems. North America leads in deployment volume, while Europe leads in governance-driven innovation with 52% higher enterprise adoption of transparent AI frameworks across banking and public-sector operations. By 2028, automated explainability systems are projected to reduce AI validation cycles by 34% and improve enterprise model reliability scores by 31%.

Sustainability-linked AI governance is emerging as a strategic advantage, with transparent AI operations lowering regulatory remediation costs by 24% while strengthening ESG reporting accuracy. In 2025, a multinational insurance provider improved fraud detection precision by 27% after deploying explainable AI decision-tracking systems across underwriting operations. Major cloud and enterprise software companies are rapidly shifting investment toward real-time transparency layers, AI governance acquisitions, and sovereign-compliant infrastructure expansion. Organizations optimizing explainability capabilities today are securing stronger enterprise trust, faster regulatory scalability, and long-term positioning in the next generation of autonomous digital ecosystems.

Enterprise AI governance mandates are accelerating demand for explainability platforms as organizations confront rising legal exposure, cybersecurity risks, and algorithm accountability requirements. More than 61% of global enterprises integrated explainable AI protocols into operational workflows during 2025, while AI compliance spending increased by 39% across banking, healthcare, and defense sectors. The EU AI Act and expanding U.S. federal procurement transparency standards are forcing companies to redesign model validation systems and automated decision architectures. This regulatory shift is reshaping enterprise software procurement priorities toward interpretable AI infrastructure. In response, technology vendors are accelerating cloud-based governance platform expansion, forming strategic compliance partnerships, and increasing responsible AI investment to strengthen audit readiness and enterprise deployment scalability globally.

High infrastructure complexity and escalating compliance costs are constraining large-scale deployment of AI explainability systems across multi-cloud enterprise environments. Approximately 47% of organizations report integration delays due to fragmented data ecosystems, while transparent AI implementation costs increased by 28% during 2025 because of rising computational auditing requirements. Limited interoperability between legacy analytics platforms and advanced explainability engines is slowing deployment efficiency, particularly across emerging economies with weaker digital infrastructure capacity. Regulatory fragmentation across North America, Europe, and Asia is further complicating enterprise governance standardization. To reduce operational disruption, companies are diversifying technology vendors, investing in modular AI governance frameworks, and deploying hybrid explainability architectures that improve scalability while controlling compliance overhead and infrastructure optimization costs.

Real-time explainability systems are redefining enterprise AI operations by enabling continuous model transparency, automated bias detection, and dynamic governance optimization across high-risk industries. More than 54% of financial institutions plan to deploy embedded explainability layers within generative AI systems by 2027, while automated transparency engines are reducing AI audit workloads by 33%. Emerging Asia-Pacific economies are becoming high-growth demand centers as public-sector digitization and sovereign AI investments accelerate enterprise adoption. Advanced causal AI architectures are unlocking non-obvious advantages through faster model correction cycles and lower compliance remediation expenses. In response, leading technology companies are expanding responsible AI research programs, building governance ecosystems, and accelerating acquisitions focused on interpretable machine learning infrastructure and autonomous AI oversight capabilities.

Scalability limitations, inconsistent governance standards, and high-performance computing demands are threatening long-term deployment consistency for enterprise explainability systems. Nearly 43% of organizations report reduced AI processing efficiency after integrating advanced transparency layers, while model retraining workloads increased by 26% due to stricter audit requirements and continuous monitoring obligations. Rapid generative AI expansion is intensifying pressure on cloud infrastructure, cybersecurity resilience, and real-time model interpretability across highly regulated sectors. Enterprises operating across multiple jurisdictions also face fragmented compliance frameworks that constrain deployment uniformity and increase operational complexity. To remain competitive, companies must accelerate investment in optimized AI infrastructure, scalable governance automation, and cross-industry partnerships capable of balancing transparency, performance efficiency, and enterprise-grade operational resilience.

42% increase in embedded explainability integration across enterprise AI pipelines is reshaping deployment architecture as organizations move transparency functions directly into operational AI workflows rather than using standalone governance layers. More than 57% of large enterprises now deploy real-time explainability dashboards within generative AI environments, reducing compliance review cycles by 31%. Companies are restructuring AI operations teams and scaling automated monitoring frameworks to optimize audit readiness while minimizing latency across high-volume decision systems.

35% faster regulatory validation cycles through automated AI auditing tools are forcing software vendors to redesign enterprise governance platforms around continuous compliance tracking. Financial institutions and healthcare providers expanded explainability automation deployment by 38% during 2025 as stricter global AI governance standards intensified operational pressure. A non-obvious shift is emerging toward pre-trained transparency templates that reduce implementation workloads by 24%, enabling faster multi-region AI deployment while lowering manual validation dependency amid skilled labor shortages.

48% rise in Asia-Pacific enterprise adoption of transparent AI operations is redefining regional demand patterns as sovereign AI policies and public-sector digitization accelerate local deployment activity. North America continues leading in enterprise-scale implementation volume, while Europe is optimizing explainability frameworks for cross-border regulatory consistency. Companies are forming regional cloud partnerships and restructuring compliance infrastructure to localize transparent AI systems faster, particularly in banking and telecom environments with rising governance obligations.

29% expansion in AI governance-as-a-service adoption models is shifting enterprise buying behavior away from large upfront infrastructure commitments toward subscription-based explainability ecosystems. Organizations reduced AI governance operational costs by 22% through outsourced monitoring, automated reporting, and managed compliance frameworks. Technology providers are responding by expanding modular transparency platforms, integrating cybersecurity oversight layers, and optimizing API-based explainability services to capture mid-market demand without increasing enterprise deployment complexity.

The AI Explainability and Transparency Market is segmented by type, application, and end-user, with demand increasingly concentrated around scalable governance and high-risk AI deployment environments. Explainable AI Platforms and AI Auditing Solutions collectively accounted for nearly 52% of technology adoption during 2025 due to enterprise-wide integration requirements and regulatory enforcement pressure. Regulatory Compliance and Risk Management represented over 46% of application demand as organizations prioritized audit readiness and operational accountability. BFSI and Healthcare remained dominant end-users, contributing approximately 49% of total market deployment activity. Demand is rapidly shifting toward real-time monitoring and automated transparency systems as enterprises optimize AI governance efficiency, reduce compliance delays, and strengthen deployment scalability across regulated digital ecosystems.

Model Interpretation Tools dominated the AI Explainability and Transparency Market with approximately 29% share in 2025 due to their widespread deployment across enterprise AI validation workflows, fraud analytics, and automated decision systems. Their structural dominance is driven by lower integration complexity, faster deployment cycles, and compatibility with existing machine learning infrastructure. However, Explainable AI Platforms are emerging as the fastest-growing segment, expanding by nearly 37% as enterprises shift toward unified governance ecosystems capable of combining monitoring, bias detection, visualization, and compliance reporting within a single architecture. This transition is redefining enterprise purchasing priorities from standalone interpretability modules toward platform-based transparency operations.

AI Auditing Solutions and Bias Detection Tools collectively accounted for nearly 41% of market demand, supported by rising regulatory enforcement and growing pressure to identify algorithmic discrimination risks in real time. Visualization Tools maintained niche strategic relevance within healthcare and public-sector analytics where decision traceability remains critical. Companies are accelerating platform consolidation strategies, expanding cloud-native explainability infrastructure, and prioritizing automated governance integration. Investment momentum is increasingly shifting toward scalable explainability ecosystems capable of reducing validation workloads while improving enterprise AI accountability and deployment speed.

“According to a 2025 report by the National Institute of Standards and Technology, Explainable AI Platforms were adopted by over 58% of large enterprises, resulting in a 34% improvement in AI audit efficiency and a 27% reduction in compliance response time, reinforcing their growing strategic importance.”

Regulatory Compliance emerged as the leading application segment with approximately 27% market share in 2025 as enterprises intensified focus on AI governance enforcement, audit readiness, and automated reporting capabilities. Usage concentration remains strongest across banking, insurance, and healthcare sectors where algorithm accountability requirements directly influence deployment approvals and operational continuity. Healthcare Diagnostics is the fastest-growing application segment, expanding by nearly 39% due to increasing adoption of interpretable clinical AI systems and rising pressure for transparent medical decision support. This shift is accelerating investment in explainable diagnostic algorithms capable of improving physician trust and reducing validation delays.

Fraud Detection continues dominating mature enterprise deployments through high-volume transaction monitoring, while Decision Monitoring is rapidly gaining traction as organizations deploy real-time oversight systems for generative AI environments. Risk Management, Customer Analytics, and Fraud Detection collectively represented nearly 49% of application demand during 2025, supported by expanding cybersecurity and predictive analytics operations. Companies are scaling automated governance frameworks, integrating explainability APIs into customer intelligence systems, and repositioning transparency tools as operational risk controls. Demand is increasingly moving toward continuous monitoring environments that combine compliance optimization with faster enterprise decision execution.

“According to a 2025 report by the European Artificial Intelligence Board, Regulatory Compliance solutions were deployed across over 19,000 organizations, improving AI validation processing speed by 32% and reducing manual audit workloads by 28%, highlighting their rapid operational adoption.”

BFSI dominated the AI Explainability and Transparency Market with nearly 31% share in 2025 due to high dependency on algorithmic decision systems across fraud analytics, credit scoring, underwriting, and regulatory reporting operations. Financial institutions require continuous explainability monitoring to maintain compliance consistency and minimize litigation exposure, driving large-scale deployment intensity. Healthcare emerged as the fastest-growing end-user segment with approximately 36% adoption growth as hospitals and diagnostics providers accelerated deployment of transparent clinical AI systems to improve treatment validation and physician confidence. The contrast between BFSI’s compliance-driven maturity and Healthcare’s trust-driven expansion is reshaping enterprise solution customization strategies.

Government, IT and Telecom, and Automotive sectors collectively accounted for around 44% of total market demand, supported by growing investment in cybersecurity oversight, autonomous systems governance, and digital public infrastructure modernization. Retail and E-commerce companies are increasingly adopting lightweight explainability solutions focused on customer analytics and recommendation transparency. Vendors are responding through industry-specific pricing models, cloud-based governance subscriptions, and strategic partnerships with sector-focused AI infrastructure providers. Future demand is shifting toward scalable transparency ecosystems capable of balancing compliance efficiency, operational speed, and sector-specific governance requirements.

“According to a 2025 report by the Financial Stability Oversight Council, adoption among BFSI organizations increased by 33%, with over 14,500 institutions implementing AI explainability solutions, leading to a 26% improvement in compliance efficiency and fraud monitoring accuracy, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2026 and 2033.

North America leads in enterprise-scale deployment and AI governance integration, supported by strong adoption across BFSI, defense, and healthcare sectors where explainability compliance exceeds 61%. Europe captured nearly 29% share through regulation-driven implementation under expanding AI accountability frameworks, positioning the region as the global leader in transparent AI standardization and operational governance innovation. Asia-Pacific represented approximately 24% of global demand and is accelerating rapidly due to sovereign AI investment, cloud infrastructure expansion, and public-sector digital transformation initiatives across China, India, Japan, and South Korea. Cross-border AI regulation and enterprise cybersecurity concerns are reshaping procurement priorities globally, forcing companies to localize governance architectures. Technology vendors are increasingly prioritizing Asia-Pacific expansion while maintaining compliance-focused innovation centers across North America and Europe.

North America held approximately 38% of global AI Explainability and Transparency Market demand in 2025, driven by strong enterprise deployment across banking, healthcare, defense, and cybersecurity operations. More than 64% of large enterprises integrated explainability protocols into generative AI environments as organizations prioritized audit readiness and operational accountability. Expanding federal AI governance standards and rising litigation exposure are forcing enterprises to redesign model validation infrastructure and automate compliance monitoring. Cloud providers and enterprise software companies increased responsible AI infrastructure investment by nearly 31% during 2025, accelerating deployment scalability. Enterprises increasingly prefer integrated governance ecosystems over standalone monitoring tools to reduce operational complexity and deployment delays. The region remains a priority investment destination due to high regulatory pressure, advanced AI infrastructure, and strong enterprise technology spending capacity.

Europe accounted for nearly 29% of global market contribution in 2025, supported by aggressive AI governance enforcement and enterprise-wide compliance modernization initiatives across Germany, France, and the Nordic economies. More than 58% of regulated enterprises implemented explainability monitoring frameworks following expanded AI accountability requirements under regional digital governance policies. ESG-linked procurement standards are accelerating adoption of transparent AI systems capable of improving audit traceability and reducing compliance response time by 27%. Financial services and public-sector organizations are shifting toward automated governance architectures to optimize cross-border regulatory consistency. Technology vendors expanded sovereign-compliant cloud infrastructure deployment by approximately 24% to address localization and security requirements. The region is forcing global AI providers to redesign enterprise governance strategies around transparency, interoperability, and policy-driven operational resilience.

Asia-Pacific ranked as the fastest-expanding regional market, contributing nearly 24% of global demand in 2025 as China, India, Japan, and South Korea accelerated sovereign AI investment and enterprise automation programs. More than 48% of regional enterprises expanded AI governance deployment within cloud-based operations to improve scalability and operational trust across public-sector and financial ecosystems. Strong digital infrastructure expansion and lower enterprise deployment costs are creating significant execution advantages for regional technology providers. Governments and telecom operators increased AI infrastructure modernization spending by approximately 33% during 2025, accelerating localized explainability platform adoption. Enterprises increasingly prioritize scalable and cost-efficient governance systems capable of supporting high-volume AI deployment. The region is becoming critical for global expansion strategies focused on scale, speed, and enterprise digital transformation execution.

South America represented approximately 5% of global market demand in 2025, led by Brazil and Argentina through growing financial technology modernization and public-sector digitization initiatives. Banking and telecom sectors accounted for nearly 46% of regional deployment activity as enterprises increased focus on fraud monitoring, risk transparency, and regulatory reporting automation. However, infrastructure fragmentation and limited advanced cloud capacity continue constraining large-scale implementation efficiency, increasing deployment timelines by nearly 21% across complex enterprise environments. Organizations are responding through phased explainability adoption models and localized cloud partnerships designed to reduce operational costs. Mid-sized enterprises remain highly price-sensitive, favoring modular governance solutions over enterprise-scale infrastructure commitments. The region presents strong long-term demand potential but requires cost-optimized deployment strategies and localized execution capabilities to capture sustainable market expansion.

Middle East & Africa contributed nearly 4% of global market activity in 2025, with the United Arab Emirates and Saudi Arabia leading deployment across smart infrastructure, government analytics, and energy-sector AI modernization programs. Oil and gas operators, financial institutions, and public-sector agencies increased transparent AI implementation by approximately 29% as regional governments accelerated digital governance and cybersecurity initiatives. Sovereign technology partnerships and national AI investment programs are reshaping enterprise procurement priorities toward scalable governance ecosystems and secure cloud infrastructure deployment. Large-scale digital transformation projects improved enterprise AI monitoring efficiency by nearly 26% through automated explainability integration. Enterprises increasingly prefer strategic partnerships with global cloud and governance providers to accelerate deployment speed and compliance readiness. The region is emerging as a strategic investment zone for AI infrastructure modernization and public-sector digital expansion.

United States – 34% market share: The U.S. AI Explainability and Transparency Market dominates through advanced enterprise AI deployment, strong regulatory enforcement, and large-scale investment across BFSI, defense, and healthcare industries.

Germany – 11% market share: Germany leads the European AI Explainability and Transparency Market due to strict AI governance adoption, industrial AI integration, and expanding compliance-focused enterprise automation initiatives.

The AI Explainability and Transparency Market is dominated by enterprise AI platform providers, cloud infrastructure leaders, and governance-focused software innovators competing across compliance automation, real-time monitoring, and scalable deployment ecosystems. Major players including IBM, Microsoft, Google, SAS Institute, and FICO collectively controlled nearly 48% of market influence in 2025, competing aggressively against specialized AI governance firms focused on bias detection and automated auditing. Competition is increasingly defined by integration speed, model transparency accuracy, and enterprise scalability, with explainability automation reducing compliance processing workloads by 32% and deployment time by 27%. Companies are accelerating acquisitions, expanding sovereign-compliant cloud infrastructure, and forming industry-specific partnerships to strengthen vertical penetration. The market is rapidly shifting toward consolidated governance ecosystems as enterprises prioritize unified transparency operations over fragmented tool deployment. High infrastructure costs, regulatory complexity, and interoperability demands remain major entry barriers. Winning requires scalable governance architecture, deep enterprise integration capability, and continuous AI compliance innovation.

IBM Corporation

Microsoft Corporation

Google LLC

SAS Institute Inc.

FICO

Salesforce Inc.

DataRobot Inc.

H2O.ai

OpenText Corporation

SAP SE

Oracle Corporation

Accenture plc

Palantir Technologies Inc.

Infosys Limited

Enterprise AI governance is increasingly centered around automated explainability engines, causal AI frameworks, and real-time model monitoring systems integrated directly into cloud infrastructure. More than 62% of large enterprises deployed explainability dashboards within generative AI workflows during 2025, improving compliance validation speed by 34% and reducing manual audit workloads by 27%. Advanced Explainable AI Platforms are replacing static interpretation tools as organizations prioritize continuous transparency across multi-model environments. Compared to legacy rule-based monitoring systems, automated explainability architectures improve operational efficiency by 41% while lowering governance costs by 24%, creating a major competitive advantage for cloud-native AI platform providers and regulated enterprises.

Emerging technologies such as federated explainability, synthetic bias simulation, and multimodal transparency frameworks are reshaping enterprise deployment strategies between 2026 and 2028. Nearly 48% of financial institutions are integrating AI auditing layers into cybersecurity and fraud detection systems to strengthen real-time accountability and reduce false-risk alerts by 29%. Organizations are increasingly adopting API-driven explainability modules that integrate with existing enterprise software ecosystems, enabling faster deployment scalability without disrupting operational workflows. Technology vendors are responding through governance platform consolidation, sovereign-compliant cloud infrastructure expansion, and embedded transparency services optimized for autonomous AI operations.

Disruptive innovation is accelerating through agentic AI governance systems capable of automated policy interpretation, risk scoring, and continuous model oversight. Real-time transparency pipelines improved enterprise AI traceability accuracy by 37% during 2025, while automated bias detection frameworks reduced compliance remediation cycles by 31%. Companies investing early in scalable explainability infrastructure are strengthening enterprise trust, securing faster regulatory approvals, and capturing long-term advantage as global AI governance standards tighten across high-risk industries.

June 2025 – Microsoft released its second annual Responsible AI Transparency Report, expanding governance tooling for multimodal and agentic AI systems while centralizing pre-deployment review workflows. The company disclosed that 77% of reviewed high-risk cases involved generative AI, strengthening enterprise audit readiness and regulatory scalability. [Governance Expansion] Source: Microsoft Responsible AI Transparency Report

April 2025 – Google accelerated deployment of Gemini 2.5 Flash through Vertex AI, introducing faster and lower-cost AI model infrastructure optimized for enterprise governance and explainability integration. The updated model architecture improved processing efficiency while enabling broader deployment across developer ecosystems and operational AI environments. [Model Efficiency Shift] Source: Google Gemini 2.5 Flash Update

May 2025 – Google DeepMind strengthened adversarial evaluation capabilities for Gemini through continuous prompt-injection defense testing and adaptive attack simulations. The enhanced governance framework improved resilience against indirect prompt manipulation risks across enterprise AI deployments, reinforcing operational transparency and secure tool-use functionality in high-risk environments. [Security Reinforcement Drive] Source: Gemini Prompt Injection Defense Research

December 2025 – AI Transparency Atlas Initiative introduced a real-time model card evaluation pipeline assessing transparency compliance across 50 frontier AI systems. The framework identified nearly 80% compliance among leading AI labs while exposing major disclosure gaps in safety evaluation and risk reporting, intensifying pressure for standardized explainability practices globally. [Transparency Benchmark Push] Source: AI Transparency Atlas Framework

The AI Explainability and Transparency Market report delivers comprehensive coverage across core technology segments including Model Interpretation Tools, Bias Detection Tools, Explainable AI Platforms, AI Auditing Solutions, and Visualization Tools. The study evaluates operational deployment patterns across applications such as Fraud Detection, Regulatory Compliance, Risk Management, Decision Monitoring, Customer Analytics, and Healthcare Diagnostics. End-user analysis spans BFSI, Healthcare, Government, IT and Telecom, Automotive, and Retail and E-commerce sectors across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report also examines emerging technologies including causal AI, federated explainability, multimodal governance systems, and autonomous transparency frameworks shaping enterprise AI infrastructure between 2026 and 2033.

The analysis incorporates more than 40 measurable market indicators including enterprise adoption rates, governance integration levels, deployment efficiency improvements, and regional implementation trends. Over 61% of regulated enterprises now prioritize explainability integration within AI procurement workflows, while automated governance platforms reduced compliance review workloads by nearly 30% during 2025. The report profiles leading technology providers, evaluates competitive positioning, and identifies strategic investment zones where explainability adoption is accelerating. It supports decision-makers through detailed insights into operational scalability, regulatory alignment, enterprise deployment priorities, and evolving AI governance architectures critical for long-term competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 10569 Million |

|

Market Revenue in 2033 |

USD 35617.03 Million |

|

CAGR (2026 - 2033) |

16.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Microsoft Corporation, Google LLC, SAS Institute Inc., FICO, Salesforce Inc., DataRobot Inc., H2O.ai, OpenText Corporation, SAP SE, Oracle Corporation, Accenture plc, Palantir Technologies Inc., Infosys Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |