Reports

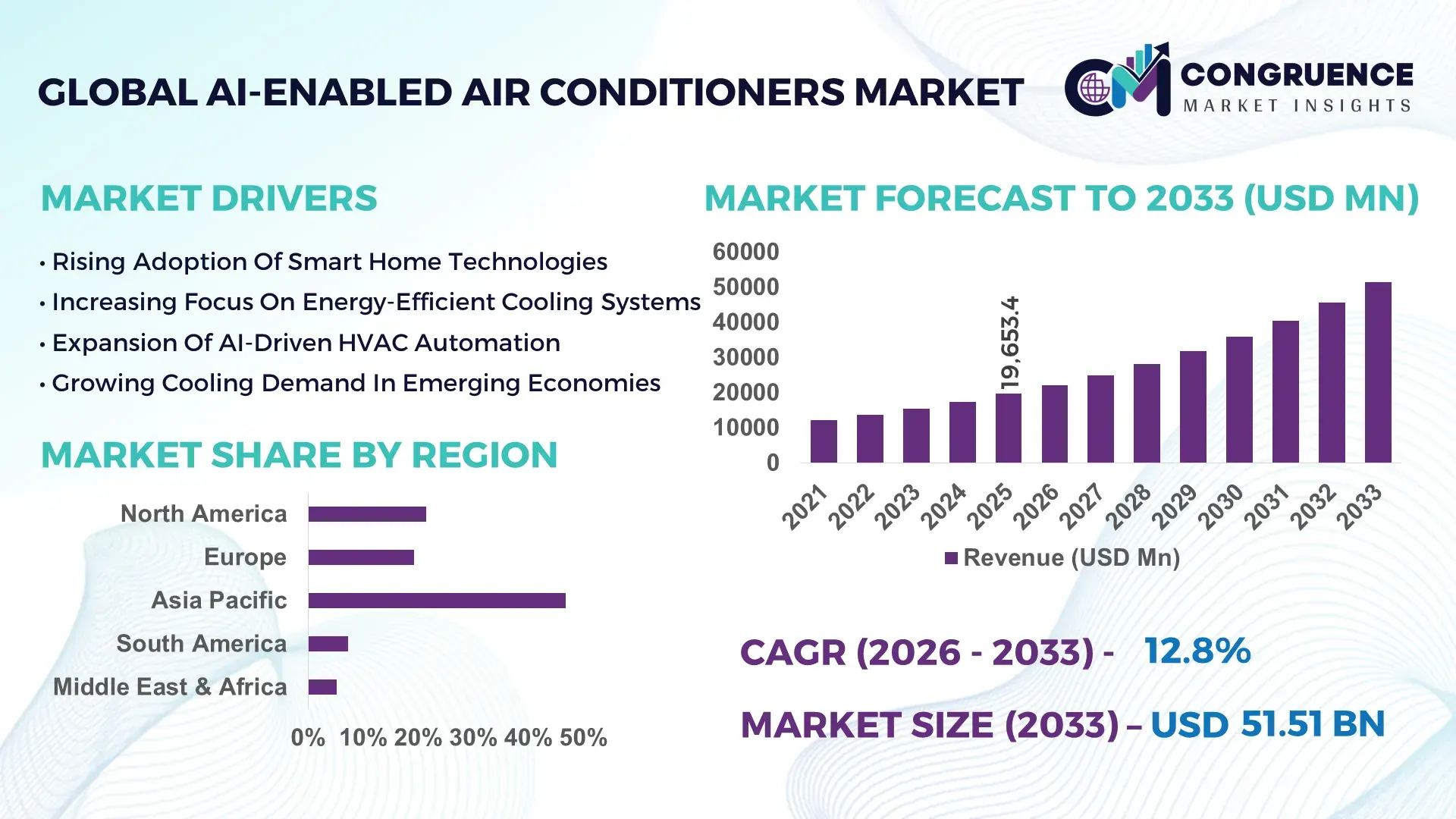

The Global AI-Enabled Air Conditioners Market was valued at USD 19,653.4 Million in 2025 and is anticipated to reach a value of USD 51,512.2 Million by 2033 expanding at a CAGR of 12.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rising demand for energy-efficient smart cooling systems integrated with machine learning-based temperature optimization and predictive maintenance capabilities.

China represents the most influential production hub in the AI-Enabled Air Conditioners market, supported by advanced manufacturing clusters and high-volume smart appliance exports. In 2025, China produced over 58 million smart air conditioning units, with nearly 35% equipped with AI-based climate optimization features. Government-backed investments exceeding USD 2.4 billion in smart home and IoT infrastructure accelerated integration of AI chipsets into residential and commercial HVAC systems. More than 42% of urban households in tier-1 cities adopted app-connected air conditioners, while industrial facilities deployed AI-driven HVAC automation to improve energy efficiency by up to 27%, reinforcing technological leadership in compressor innovation, inverter technology, and AI-powered adaptive cooling algorithms.

Market Size & Growth: Valued at USD 19,653.4 million in 2025, projected to reach USD 51,512.2 million by 2033, driven by intelligent climate automation and energy efficiency mandates.

Top Growth Drivers: Smart home penetration 46%, energy savings up to 30%, predictive maintenance adoption 33%.

Short-Term Forecast: By 2028, AI-based energy optimization is expected to reduce household cooling electricity costs by 22%.

Emerging Technologies: Edge AI temperature sensing, self-learning climate control algorithms, IoT-integrated HVAC analytics.

Regional Leaders: Asia-Pacific projected at USD 22.4 billion by 2033 with mass urban demand; North America at USD 13.8 billion driven by smart homes; Europe at USD 9.6 billion supported by green building standards.

Consumer/End-User Trends: Over 48% of buyers prefer AI-enabled air conditioners with mobile app control and voice assistant compatibility.

Pilot or Case Example: In 2024, a commercial building retrofit achieved 29% HVAC energy reduction using AI-based load forecasting.

Competitive Landscape: Daikin leads with approximately 18% share, followed by LG Electronics, Mitsubishi Electric, Panasonic, and Haier.

Regulatory & ESG Impact: Energy labeling mandates and carbon neutrality targets accelerating AI-driven efficiency upgrades.

Investment & Funding Patterns: More than USD 3.5 billion invested globally in AI-powered HVAC innovation between 2023–2025.

Innovation & Future Outlook: Integration with smart grids and demand-response systems shaping next-generation AI-enabled cooling platforms.

Residential applications account for approximately 61% of AI-Enabled Air Conditioners adoption, followed by commercial buildings at 29% and industrial facilities at 10%. Technological advancements such as inverter compressors, occupancy-based sensing, and AI climate zoning are redefining performance benchmarks. Stricter energy efficiency regulations and rising electricity tariffs continue to influence purchasing decisions, while urban heat stress and green building certifications accelerate intelligent cooling demand globally.

The AI-Enabled Air Conditioners Market is strategically positioned at the intersection of smart infrastructure, energy management, and sustainable urbanization. Intelligent cooling systems equipped with adaptive algorithms and predictive diagnostics enable real-time climate optimization, reducing operational energy consumption by up to 30% compared to conventional fixed-speed air conditioning systems. AI-driven inverter compressors deliver 18% higher efficiency compared to legacy non-inverter models, strengthening their value proposition in energy-conscious markets.

Asia-Pacific dominates in production volume, while North America leads in adoption with over 52% of newly constructed smart homes integrating AI-powered HVAC systems. Commercial real estate developers increasingly incorporate AI-enabled air conditioners to meet green building certifications and reduce building energy intensity. By 2027, AI-based demand-response integration is expected to improve grid load balancing efficiency by 21%, supporting utilities during peak consumption periods.

From an ESG perspective, manufacturers are committing to 35% reduction in refrigerant-related emissions and 25% recycled material integration by 2030. In 2024, Japan achieved a 24% improvement in building cooling efficiency through AI-driven district cooling optimization initiatives. The AI-Enabled Air Conditioners Market is evolving into a core enabler of resilient energy infrastructure, regulatory compliance, and sustainable climate control innovation across residential and commercial ecosystems.

The AI-Enabled Air Conditioners market is influenced by accelerating smart home adoption, rising electricity costs, and stricter environmental efficiency standards. Intelligent HVAC solutions are increasingly integrated with IoT platforms, enabling automated diagnostics and real-time climate adjustment. Urban heat island effects and climate variability have increased cooling demand by over 20% in densely populated cities. Simultaneously, advancements in edge computing and low-power AI chips are enhancing processing speed while reducing hardware footprint. Competitive differentiation centers on algorithm precision, smart connectivity, and long-term energy savings performance, shaping purchasing decisions among residential and commercial buyers.

Energy-efficient smart home penetration has exceeded 46% in developed urban markets, directly fueling AI-Enabled Air Conditioners adoption. AI-powered systems dynamically adjust cooling output based on occupancy and ambient temperature, cutting electricity usage by up to 30%. In 2025, more than 54% of newly built premium apartments integrated AI climate control as a standard feature. Smart thermostat synchronization reduced peak load demand by 17% in pilot residential clusters. Growing consumer awareness of carbon footprint reduction and long-term energy savings continues to accelerate demand for intelligent HVAC systems.

AI-enabled air conditioners typically cost 20–35% more than traditional inverter systems, limiting adoption in price-sensitive regions. Retrofitting older buildings with smart wiring and IoT connectivity can increase installation costs by 15%. In emerging economies, only 28% of households have compatible smart home infrastructure. Additionally, inconsistent broadband connectivity affects real-time cloud-based optimization features. These financial and infrastructural barriers slow penetration in rural and low-income markets.

Smart grid integration enables AI-Enabled Air Conditioners to participate in demand-response programs, improving grid efficiency by up to 21%. Utilities offering dynamic pricing models incentivize consumers to shift cooling loads during off-peak hours. In 2024, over 18 pilot smart city projects integrated AI HVAC systems with renewable energy networks. Commercial buildings leveraging AI-driven load forecasting reported 26% lower peak demand charges, presenting scalable growth opportunities across urban centers.

AI-connected air conditioners collect user behavior and energy consumption data, raising cybersecurity concerns. Approximately 19% of smart appliance users expressed privacy-related hesitation in 2025. Additionally, transitioning to low-GWP refrigerants requires redesign of compressor systems, increasing manufacturing complexity by 14%. Compliance with evolving environmental standards adds regulatory burdens and R&D costs, impacting product rollout timelines.

AI-Based Predictive Maintenance Expansion: Over 37% of commercial buildings adopted AI-driven predictive HVAC maintenance in 2025, reducing unexpected system downtime by 32% and extending equipment lifespan by 18%.

Integration with Renewable Energy Systems: Nearly 28% of new smart residential installations integrate AI-enabled air conditioners with rooftop solar systems, improving self-consumption rates by 24% and lowering grid dependency.

Voice & App-Controlled Climate Ecosystems: Around 52% of AI air conditioner buyers prioritize voice assistant compatibility, while app-based energy analytics improved user engagement by 34% in 2024.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the AI-Enabled Air Conditioners market. Research suggests that 55% of new projects achieved cost efficiencies using prefabricated HVAC modules, reducing installation time by 31% and minimizing labor requirements in Europe and North America.

The AI-Enabled Air Conditioners market is segmented by type, application, and end-user, reflecting varied adoption across residential, commercial, and industrial domains. Smart split air conditioners dominate urban households, while centralized AI-driven HVAC systems gain traction in commercial complexes. Applications span smart homes, office spaces, data centers, and hospitality environments. End-user insights reveal increasing adoption among energy-conscious consumers and facility managers seeking automated energy optimization.

Smart split AI air conditioners account for approximately 49% of total installations due to easy retrofitting and compatibility with residential IoT ecosystems. Centralized AI HVAC systems represent 28%, preferred for commercial buildings with multi-zone control requirements. Portable AI air conditioners and window-based smart units collectively contribute 23%, catering to smaller apartments and temporary installations.

Smart split systems are the fastest-growing segment, expanding at a CAGR of 13.6% driven by urban apartment demand and smartphone-based climate control. Their integration with occupancy sensors improves cooling efficiency by 25%.

In 2025, a national energy efficiency program reported that AI-integrated split air conditioners reduced household cooling consumption by an average of 21% across 1.8 million monitored units.

Residential usage leads with a 61% share, supported by rising smart home adoption and increased summer temperature extremes. Commercial buildings account for 29%, where AI-enabled air conditioners optimize multi-zone climate control and reduce operating costs. Industrial facilities contribute 10%, leveraging AI-driven HVAC for process stability.

Commercial applications are expanding at a CAGR of 12.1% as green building certifications require intelligent energy monitoring. In 2025, more than 41% of enterprises piloted AI-enabled HVAC systems to improve facility efficiency. Additionally, 57% of property developers incorporated AI climate analytics in new mixed-use projects.

In 2025, a public infrastructure modernization program implemented AI-based HVAC systems across 120 municipal buildings, achieving a 23% reduction in electricity consumption.

Households represent 61% of AI-Enabled Air Conditioners installations, driven by rising disposable incomes and digital lifestyle preferences. Commercial real estate operators account for 27%, while industrial end-users contribute 12%, focusing on energy optimization and equipment longevity.

Commercial users are the fastest-growing segment, projected to expand at a CAGR of 12.4% due to ESG compliance and cost optimization priorities. In 2025, 44% of large office facilities integrated AI-driven cooling analytics. Additionally, 63% of smart city pilot participants reported improved thermal comfort satisfaction.

In 2025, an international building performance assessment indicated that AI-integrated HVAC adoption among mid-sized enterprises increased by 24%, enabling over 600 facilities to reduce annual energy intensity significantly.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

Asia-Pacific shipped more than 72 million AI-enabled air conditioning units in 2025, supported by large-scale urban housing developments and rapid smart appliance penetration. China, Japan, and India collectively contributed over 78% of regional installations, with smart inverter-based AI systems representing 39% of new sales. North America recorded approximately 21.5% share, with over 18 million connected HVAC units integrated into smart home ecosystems. Europe held 19.2%, driven by green building retrofits across Germany, France, and the UK, where nearly 44% of commercial renovation projects included AI-powered HVAC optimization. South America and Middle East & Africa together represented 12.5%, with commercial cooling upgrades in Brazil, UAE, and South Africa increasing by 17% year-over-year due to rising temperature extremes and infrastructure modernization.

How are smart infrastructure investments accelerating intelligent cooling adoption?

This region accounted for approximately 21.5% of global AI-Enabled Air Conditioners installations in 2025, representing over 18 million connected units across residential and commercial buildings. Demand is driven by healthcare facilities, data centers, retail chains, and high-rise residential complexes. Updated federal energy efficiency standards and tax credits for energy-saving appliances increased smart HVAC upgrades by 23% in 2025. Digital transformation trends include integration with smart thermostats, voice assistants, and demand-response utility platforms. A prominent regional manufacturer introduced AI-based occupancy detection systems capable of reducing cooling waste by 26% in office buildings. Consumer behavior reflects strong enterprise adoption in healthcare and finance sectors, where over 49% of newly constructed facilities deploy AI-enabled air conditioners for real-time climate analytics and operational cost optimization.

Why is sustainability compliance reshaping intelligent climate control investments?

Europe represented nearly 19.2% of global AI-Enabled Air Conditioners demand in 2025, with Germany, the UK, and France accounting for more than 61% of installations. Regulatory mandates under eco-design and energy labeling frameworks accelerated adoption of AI-integrated inverter systems. Over 47% of new commercial building permits included requirements for advanced HVAC monitoring technologies. Sustainability initiatives promoting low-GWP refrigerants increased AI-based compressor redesign adoption by 18%. A major regional manufacturer expanded eco-smart air conditioners with adaptive load balancing, improving seasonal energy performance by 21%. Consumer behavior in Europe reflects regulatory-driven purchasing, with nearly 53% of buyers prioritizing transparent energy performance metrics and explainable AI control systems.

What drives mass-scale production and digital cooling innovation ecosystems?

Asia-Pacific led global unit volume in 2025 with over 72 million AI-enabled air conditioners shipped. China alone accounted for more than 41 million units, followed by India and Japan. Expanding urban housing programs added 12 million new residential units equipped with IoT-ready climate systems. Regional manufacturing hubs adopted AI-powered compressor calibration, reducing defect rates by 14%. Smart city initiatives in Japan and South Korea integrated AI-driven district cooling systems improving efficiency by 19%. A leading domestic brand deployed mobile AI diagnostics, with over 5 million app-connected users optimizing cooling remotely. Consumer adoption is strongly influenced by e-commerce channels, where nearly 46% of smart air conditioners are purchased online through mobile platforms.

How are urbanization and energy modernization stimulating intelligent HVAC demand?

South America accounted for approximately 7.3% of global installations in 2025, led by Brazil and Argentina. Brazil alone contributed nearly 58% of regional AI-enabled air conditioner demand due to expanding commercial infrastructure. Energy efficiency incentives reduced import duties on inverter-based units by 12%, encouraging technology upgrades. Infrastructure expansion in retail and hospitality increased smart HVAC deployments by 16%. A regional distributor partnered with AI climate software providers to localize cooling optimization for tropical environments, achieving 18% energy savings in pilot commercial facilities. Consumer preferences reflect demand tied to climate variability and media-driven smart appliance awareness, particularly among middle-income urban households.

Why is climate resilience pushing next-generation cooling systems adoption?

This region represented 5.2% of global AI-Enabled Air Conditioners installations in 2025, with UAE and South Africa emerging as leading adopters. Oil & gas facilities and large-scale construction projects increased demand for AI-integrated industrial HVAC systems by 21%. Smart building modernization initiatives in the Gulf states expanded connected cooling deployments across 34 major mixed-use developments. AI-based heat load optimization reduced peak energy demand by 17% in commercial complexes. A regional infrastructure group integrated AI-enabled chiller systems across 22 high-rise towers to enhance efficiency. Consumer behavior varies, with premium urban developments preferring high-end AI cooling systems, while mid-income segments prioritize durability and energy savings.

China AI-Enabled Air Conditioners Market – 32.4%: High production capacity, strong smart home penetration, and large-scale urban infrastructure investments.

United States AI-Enabled Air Conditioners Market – 18.7%: Advanced smart home ecosystems and regulatory incentives for energy-efficient HVAC upgrades.

The AI-Enabled Air Conditioners market is moderately consolidated, with approximately 35 major global manufacturers and over 60 regional smart appliance producers competing across residential and commercial segments. The top five companies collectively account for nearly 58% of total market presence, reflecting strong brand recognition and advanced R&D capabilities. Competitive positioning centers on AI-driven compressor innovation, inverter efficiency, and IoT ecosystem integration. Product development cycles average 18–24 months, with over 40% of new launches incorporating predictive maintenance algorithms in 2025. Strategic initiatives include partnerships with smart home platform providers, acquisitions of AI software startups, and expansion of manufacturing automation to reduce defect rates by 12%. Companies increasingly differentiate through energy savings performance metrics, app-based analytics dashboards, and low-GWP refrigerant compatibility, reinforcing innovation-led competition across developed and emerging markets.

Panasonic Corporation

Haier Smart Home

Samsung Electronics

Carrier Global Corporation

Johnson Controls

Trane Technologies

Midea Group

Hitachi Cooling & Heating

Toshiba Carrier

Blue Star Limited

Gree Electric Appliances

The AI-Enabled Air Conditioners market is characterized by rapid advancements in edge computing, machine learning algorithms, and smart sensor integration. Modern AI-powered air conditioners analyze up to 500 environmental data points per minute, including humidity, occupancy, and external weather patterns. Adaptive inverter compressors adjust output dynamically, improving seasonal efficiency ratios by 20–30% compared to fixed-speed systems.

Emerging technologies include self-learning climate zoning that personalizes cooling for multiple rooms, reducing overall energy waste by 18%. Predictive maintenance platforms use AI-based fault detection models capable of identifying anomalies with 92% accuracy before mechanical failure occurs. Integration with smart grids enables automated load shifting during peak hours, reducing energy demand spikes by 15–22%.

IoT connectivity through Wi-Fi 6 and Bluetooth Low Energy enhances real-time diagnostics and firmware updates. Additionally, AI-enabled refrigerant flow optimization improves heat exchange performance by 16%, supporting compliance with low-GWP refrigerant transitions. Data analytics dashboards provide users with granular consumption insights, with over 48% of commercial building managers using AI-driven energy reports to inform facility planning decisions. These technological innovations reinforce operational efficiency, digital transformation, and sustainable cooling objectives across residential and industrial sectors.

• In April 2025, Daikin Industries announced the expansion of its AI-integrated HVAC production line in Japan, increasing annual smart inverter unit capacity by 1.2 million units and integrating advanced IoT-based diagnostics for predictive maintenance. Source: www.daikin.com

• In January 2025, LG Electronics unveiled an upgraded AI Dual Inverter air conditioner featuring real-time occupancy sensing and energy optimization that reduces power consumption by up to 30% compared to previous models. Source: www.lg.com

• In September 2024, Mitsubishi Electric introduced an AI-based building HVAC management platform capable of optimizing multi-zone cooling loads, achieving up to 25% energy efficiency improvements in commercial facilities. Source: www.mitsubishielectric.com

• In June 2024, Panasonic expanded its smart air conditioning portfolio with nanoe™ air purification integrated with AI climate control, improving indoor air quality metrics by 20% in controlled testing environments. Source: www.panasonic.com

The AI-Enabled Air Conditioners Market Report provides comprehensive coverage across product types, applications, technologies, and regional demand patterns. The scope includes smart split systems, centralized AI-driven HVAC systems, portable intelligent units, and inverter-based window air conditioners. Applications evaluated encompass residential smart homes, commercial real estate, industrial facilities, data centers, healthcare institutions, and hospitality infrastructure.

Geographically, the report analyzes Asia-Pacific, North America, Europe, South America, and Middle East & Africa, incorporating country-level insights for China, the United States, Germany, Japan, India, Brazil, UAE, and South Africa. Technological assessment covers edge AI processors, machine learning-based load forecasting, IoT connectivity protocols, demand-response integration, and low-GWP refrigerant optimization.

The report further examines energy efficiency standards, smart grid integration, digital transformation in HVAC maintenance, and sustainability-driven product innovation. Emerging niches such as AI-enabled district cooling, solar-integrated air conditioning systems, and modular HVAC installations are evaluated. Quantitative insights include unit shipments, installation density, energy performance metrics, and smart home penetration levels, enabling manufacturers, investors, policymakers, and facility managers to align strategic planning with evolving intelligent cooling market dynamics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 19,653.4 Million |

|

Market Revenue in 2033 |

USD 51,512.2 Million |

|

CAGR (2026 - 2033) |

12.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daikin Industries, LG Electronics, Mitsubishi Electric, Panasonic Corporation, Haier Smart Home, Samsung Electronics, Carrier Global Corporation, Johnson Controls, Trane Technologies, Midea Group, Hitachi Cooling & Heating, Toshiba Carrier, Blue Star Limited, Gree Electric Appliances |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |