Reports

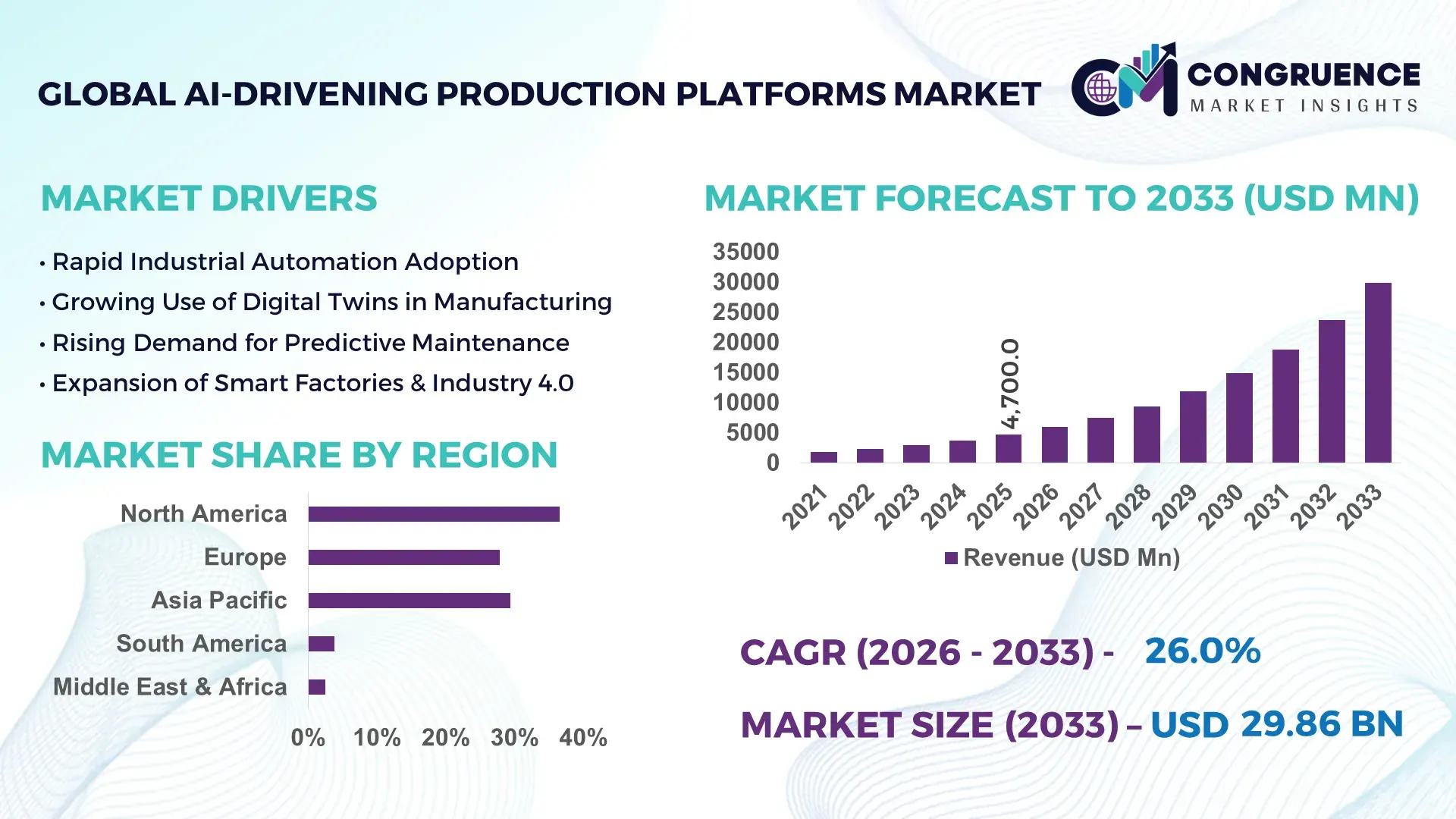

The Global AI-Drivening Production Platforms Market was valued at USD 4,700.0 Million in 2025 and is anticipated to reach USD 29,858.1 Million by 2033, expanding at a CAGR of 26% between 2026 and 2033, according to an analysis by Congruence Market Insights. This rapid expansion reflects the accelerating convergence of industrial automation, real-time analytics, and autonomous decisioning in high-volume production environments.

The United States leads the global AI-Drivening Production Platforms ecosystem through large-scale industrial deployment rather than share concentration. Over 2,100 smart factories currently operate with AI-enabled production stacks, supported by more than USD 38 billion in cumulative industrial AI investments since 2020. U.S. manufacturers integrate AI platforms across automotive, aerospace, semiconductors, and advanced chemicals, where predictive maintenance covers 70–75% of critical assets in leading plants. More than 65% of Tier-1 manufacturers use cloud-edge hybrid production architectures, while robotics density exceeds 285 robots per 10,000 workers in key manufacturing corridors such as the Midwest and Southeast. Semiconductor fabs in Arizona and Texas now run fully automated yield-optimization systems processing over 1.2 million wafers annually, while aerospace facilities in Washington and California employ AI-driven digital twins for continuous production optimization across 900+ high-value parts lines.

Market Size & Growth: USD 4.7 billion in 2025, projected to reach USD 29.9 billion by 2033, driven by rapid factory digitization and autonomous operations.

Top Growth Drivers: 58% rise in AI-enabled automation adoption; 32% improvement in asset uptime; 27% reduction in unplanned downtime.

Short-Term Forecast: By 2028, average plant cycle time is expected to drop by 22% through AI-driven scheduling.

Emerging Technologies: Edge AI orchestration, autonomous digital twins, and self-learning reinforcement systems for production control.

Regional Leaders: North America ~USD 11.2B (2033) with AI-first factories; Europe ~USD 8.4B emphasizing green manufacturing; Asia-Pacific ~USD 9.6B led by robotics-heavy electronics and automotive plants.

Consumer/End-User Trends: Automotive, electronics, and chemicals increasingly favor end-to-end AI platforms rather than point solutions.

Pilot Example (2024): A U.S. auto plant reduced line stoppages by 41% using AI-driven predictive control.

Competitive Landscape: One leading platform provider holds ~18% share, followed by Siemens, Rockwell Automation, AWS Industrial, Microsoft Azure Manufacturing, and NVIDIA Omniverse partners.

Regulatory & ESG Impact: Stricter energy-efficiency mandates and carbon-reporting rules are accelerating AI-based optimization.

Investment & Funding Patterns: Over USD 6.5 billion invested in industrial AI platforms since 2023 via corporate ventures and project finance.

Innovation & Future Outlook: Greater integration of generative AI with digital twins for fully autonomous production planning.

AI-Drivening Production Platforms are now embedded across automotive, electronics, metals, and chemicals, where they contribute an estimated 35–45% of productivity gains in advanced plants. Recent innovations include closed-loop reinforcement learning for process control, AI-native quality inspection reducing scrap rates by 18–25%, and energy-aware scheduling that trims industrial power use by 12–15%. Europe emphasizes carbon-efficient production, Asia-Pacific leads in robotics-intensive manufacturing, and North America prioritizes cloud–edge hybrid architectures. Growth is increasingly shaped by smart-factory mandates, workforce reskilling, and interoperable standards that enable cross-plant analytics and autonomous operations.

The strategic relevance of the AI-Drivening Production Platforms Market lies in its ability to transform fragmented, reactive manufacturing systems into integrated, predictive, and self-optimizing production ecosystems. These platforms combine edge computing, industrial IoT, and machine learning to orchestrate thousands of machines in real time, enabling continuous improvement rather than periodic optimization. Compared with traditional Manufacturing Execution Systems (MES), AI-native platforms deliver 28–35% faster throughput and 20–25% higher first-pass yield, fundamentally reshaping cost structures in capital-intensive industries.

Regionally, Asia-Pacific dominates in production volume, particularly in electronics and automotive assembly, while Europe leads in enterprise adoption, with roughly 62% of large manufacturers actively deploying AI-driven production stacks aligned with green manufacturing directives. North America maintains technological leadership through cloud–edge integration and advanced digital twins used in aerospace and semiconductor fabrication.

In the short term, by 2028, wider deployment of autonomous digital twins is expected to cut unplanned downtime by 30% and reduce maintenance costs by 18–22% across asset-heavy industries. Simultaneously, reinforcement learning controllers are projected to improve energy efficiency in continuous-process plants by 10–14%.

From a compliance and ESG perspective, leading firms have committed to 20–30% reductions in Scope 1 and 2 emissions by 2030, leveraging AI-driven energy optimization, predictive asset management, and waste minimization. Several manufacturers are also targeting 90% recyclable packaging and zero-landfill production lines by 2032, enabled by real-time material tracking.

A micro-scenario illustrates impact: in 2024, a German chemicals producer deployed an AI-driven process platform that cut solvent waste by 37% and reduced energy consumption by 16% while maintaining output stability.

Looking ahead, the AI-Drivening Production Platforms Market is poised to become a core pillar of industrial resilience, regulatory compliance, and sustainable growth—embedding intelligence directly into the operational fabric of global manufacturing.

The AI-Drivening Production Platforms Market is shaped by accelerating factory digitization, rising labor costs, and the shift toward autonomous operations. Widespread adoption of industrial IoT sensors has created massive data streams that require AI orchestration rather than manual control. Manufacturers increasingly favor cloud–edge hybrid architectures to balance latency, security, and scalability. Supply chain volatility has heightened demand for real-time visibility, predictive planning, and self-healing production lines. At the same time, stricter environmental regulations are pushing firms to use AI for energy optimization, emissions monitoring, and waste reduction. Integration with robotics, additive manufacturing, and digital twins is becoming standard, while interoperability standards such as OPC UA and open industrial APIs are reducing vendor lock-in. Workforce reskilling, cybersecurity risks, and capital intensity remain structural factors influencing deployment speed and platform design choices.

Global automation density continues to rise, with many leading manufacturing nations exceeding 250 robots per 10,000 workers, creating strong demand for centralized AI control layers that coordinate robotics, conveyors, and inspection systems. Traditional rule-based automation struggles with variability in materials, equipment aging, and demand fluctuations, whereas AI-driven platforms learn from operational data in real time. Predictive maintenance coverage has expanded to more than 70% of critical assets in advanced plants, reducing unexpected failures and costly line stoppages. Digital twins now mirror entire production sites, enabling scenario testing before physical changes are made. Shorter product life cycles in electronics and electric vehicles require faster reconfiguration of production lines, which AI platforms enable through adaptive scheduling and self-optimizing workflows. The growing complexity of mixed-model manufacturing further necessitates intelligent orchestration rather than manual intervention.

Deploying AI-driven production platforms requires significant capital investment in sensors, connectivity, data infrastructure, and skilled personnel, which can be prohibitive for small and mid-sized manufacturers. Many legacy plants operate on outdated control systems that are difficult and expensive to modernize, slowing adoption. Cybersecurity concerns are intensifying as more machines become connected to cloud-based analytics systems, increasing exposure to ransomware and industrial espionage. Data fragmentation across multiple vendors and proprietary protocols complicates system integration and interoperability. Additionally, workforce skill gaps in data engineering, AI operations, and industrial analytics limit effective deployment in several regions. Regulatory uncertainty around industrial data sharing and cross-border cloud usage also creates hesitation among multinational manufacturers considering large-scale platform rollouts.

The rapid expansion of smart factories creates substantial opportunities for AI-Drivening Production Platforms as core operational backbones. Governments and corporations are investing heavily in Industry 4.0 initiatives, with thousands of new digitalized facilities planned globally over the next decade. Digital twins allow manufacturers to simulate process changes, optimize layouts, and predict bottlenecks before physical implementation, reducing trial-and-error costs. Edge AI deployment enables real-time decision-making even in connectivity-constrained environments. The growing adoption of additive manufacturing and customized production increases the need for adaptive AI control systems. Integration with supply chain analytics also allows end-to-end optimization from raw materials to final delivery, improving inventory turnover and reducing waste across industrial ecosystems.

Industrial data remains highly heterogeneous, coming from thousands of machines with different formats, protocols, and quality levels, making standardization difficult. Many manufacturers operate multi-vendor ecosystems where systems do not natively communicate, requiring costly middleware solutions. Real-time data processing at scale demands advanced edge computing infrastructure that some plants lack. Ensuring data accuracy and reliability is critical, as poor-quality data can lead to faulty AI decisions and production disruptions. Cyber-physical security risks further complicate cloud integration strategies. Regulatory restrictions on data residency and cross-border transfers also limit centralized analytics in multinational operations. These technical and governance barriers slow enterprise-wide platform deployment despite strong business demand.

Rise in Modular and Prefabricated Production Architectures: More than 55% of new industrial projects report measurable cost benefits from modular, prefabricated production components integrated with AI platforms. Off-site fabrication using automated CNC and robotic cells reduces manual labor intensity by 30–40% while shortening build timelines by 25–35%. In Europe and North America, demand for high-precision AI-controlled machining centers has risen sharply, with installation rates up 18% in 2024. AI-driven quality inspection embedded in modular lines now cuts rework rates by 20–28% in construction-linked manufacturing such as steel and structural components.

Expansion of Edge-AI Control in Real Time: By 2025, over 60% of advanced factories had deployed edge AI for sub-millisecond decision-making on critical equipment. Latency-sensitive applications such as robotic welding and semiconductor lithography now rely on local AI inference, reducing network dependency by 35%. Plants using edge orchestration report 24% fewer line stoppages and 17% lower maintenance costs.

Autonomous Digital Twin Scaling: Enterprise-scale digital twins now cover entire production sites in roughly 42% of leading manufacturers, up from 28% in 2022. These systems enable scenario testing that reduces commissioning time for new lines by 20–30%. Predictive simulations have lowered scrap rates by 15–22% in metals and chemicals processing.

AI-Optimized Energy and Carbon Management: AI-driven production platforms are increasingly used for dynamic energy optimization, with smart factories achieving 10–15% reductions in electricity use during peak periods. Real-time emissions tracking now covers 65% of major industrial assets in regulated regions, helping firms meet tightening sustainability standards while maintaining throughput.

The AI-Drivening Production Platforms Market is structured around three primary lenses—type, application, and end-user—that together explain how intelligence is embedded across industrial value chains. By type, platforms are differentiated by the modality of AI models and data fusion approaches used to interpret visual, textual, sensory, and temporal signals on the shop floor. Application-based segmentation reflects how these platforms are deployed across core manufacturing functions such as predictive maintenance, quality control, production planning, and autonomous operations. End-user segmentation captures variations in adoption intensity across industries with different asset profiles, regulatory requirements, and digital maturity. Process industries (chemicals, metals, energy) favor continuous monitoring architectures, while discrete manufacturers (automotive, electronics, machinery) prioritize real-time orchestration and robotics coordination. Regional manufacturing policies, workforce automation levels, and digital infrastructure further shape segmentation patterns and investment priorities.

Vision-language production systems currently represent the backbone of AI-Drivening Production Platforms, accounting for 42% of adoption, as they can simultaneously interpret camera feeds, schematics, sensor dashboards, and textual work orders to guide real-time decisions. These systems dominate high-precision sectors such as semiconductors and automotive assembly, where automated visual inspection now covers more than 70% of critical quality checkpoints in advanced plants.

Audio-text industrial systems hold roughly 25% of adoption, primarily in maintenance coordination, safety monitoring, and voice-guided workflows for frontline workers. Their strength lies in hands-free operations in hazardous or confined environments, yet they remain less versatile than vision-based systems for complex defect detection.

Video-language models are the fastest-growing type, expanding at approximately 28% per year, driven by rising demand for continuous process monitoring, automated incident reconstruction, and AI-driven training of robotic workflows from recorded footage. These models are expected to exceed 30% adoption by 2033 as factories increasingly archive and analyze petabytes of production video data.

Remaining modalities—including sensor-only analytics, multimodal digital twins, and synthetic data simulators—collectively represent about 33% of the market, serving niche but critical roles in simulation, edge inference, and low-latency control.

• In 2025, a major global logistics and manufacturing group deployed video-language models across 120 automated sites to analyze conveyor incidents, reducing collision-related downtime by more than 35% and cutting manual review time by over half.

Predictive maintenance and asset optimization is the leading application, representing about 38% of usage, as manufacturers increasingly rely on AI to prevent failures rather than react to them. Plants using AI-driven condition monitoring now cover roughly 75% of mission-critical equipment, reducing emergency shutdowns and extending asset life.

The fastest-growing application is autonomous production control, advancing at roughly 27% per year, supported by real-time reinforcement learning, self-adjusting robotics, and closed-loop quality systems that continuously recalibrate processes without human intervention.

Quality inspection and defect detection account for approximately 22% of deployment, while production planning, demand forecasting, and digital twin simulation together contribute about 40% of remaining application activity. These latter uses are gaining traction as manufacturers seek end-to-end optimization from raw materials to finished goods.

Consumer and enterprise adoption trends further validate momentum: in 2025, over 40% of large enterprises reported piloting AI-driven production platforms for operational efficiency, and 63% of industrial firms under 35 years old leadership teams showed higher confidence in AI-integrated suppliers. In the United States, 44% of advanced manufacturers were testing AI models that fuse machine vision with operational records for continuous quality assurance.

• In 2025, a national industrial standards agency documented the rollout of AI-enabled inspection systems in more than 180 heavy-equipment facilities, enabling early fault detection for over 1.8 million critical components.

Automotive manufacturing is the leading end-user segment with roughly 36% adoption, reflecting its heavy reliance on robotics, computer vision, and real-time production orchestration. Modern vehicle plants now integrate AI across stamping, welding, painting, and final assembly, with many facilities operating more than 1,000 interconnected robots per site.

The fastest-growing end-user is semiconductors and electronics, expanding at about 29% per year, fueled by rising chip complexity, extreme precision requirements, and the need for zero-defect manufacturing in advanced nodes. AI platforms increasingly manage yield optimization, contamination control, and wafer traceability across highly automated fabs.

Other key users include chemicals and process industries (18% combined share), metals and heavy machinery (14%), and energy and utilities (12%), where AI is used for predictive reliability, energy optimization, and asset lifecycle management. Across these sectors, more than 55% of large plants report integrating AI analytics into core operations by 2025.

Adoption patterns are also shifting: over 39% of global enterprises stated they were piloting AI-driven production systems for customer fulfillment and supply reliability, while 61% of younger industrial decision-makers expressed greater trust in suppliers using multimodal AI for quality assurance.

• In 2025, a federal manufacturing modernization program recorded AI deployment across more than 520 small and mid-sized factories, enabling measurable gains in inventory accuracy and predictive maintenance coverage.

North America accounted for the largest market share at 36.5% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28.4% between 2026 and 2033.

Regional performance in the AI-Drivening Production Platforms Market reflects differences in industrial maturity, automation intensity, regulatory frameworks, and digital infrastructure readiness. North America leads due to early adoption of AI-native manufacturing platforms, with more than 62% of large industrial enterprises already integrating AI into core production workflows. Europe follows closely, driven by sustainability-linked digital transformation and compliance-focused AI deployments, accounting for 27.8% share. Asia-Pacific represents 29.4% of global demand by volume, supported by large-scale manufacturing capacity, smart factory investments, and electronics production hubs across China, Japan, South Korea, and India. South America and the Middle East & Africa together contribute around 6.3%, but are witnessing steady adoption as governments push industrial modernization, energy efficiency, and localization of production capabilities.

This region represents approximately 36.5% of the global AI-Drivening Production Platforms Market, making it the largest contributor worldwide. Demand is primarily driven by automotive, aerospace, healthcare manufacturing, semiconductors, and industrial equipment sectors, where AI-driven orchestration is embedded across planning, quality control, and predictive maintenance. Federal and state-level initiatives supporting smart manufacturing, cybersecurity compliance, and clean-energy production accelerate platform deployment. Digital transformation trends include widespread adoption of cloud–edge hybrid architectures and autonomous digital twins, now present in over 48% of advanced factories. Local technology providers and industrial automation leaders are increasingly offering AI-native production suites integrated with robotics and industrial IoT. Regional behavior shows higher enterprise adoption in healthcare, aerospace, and financial manufacturing, with over 70% of Tier-1 manufacturers prioritizing AI-driven operational resilience over manual optimization.

Europe accounts for roughly 27.8% of global market activity, with Germany, the United Kingdom, and France collectively contributing more than 65% of regional demand. Manufacturing sectors such as automotive, industrial machinery, chemicals, and renewable energy equipment are key adopters. Strong regulatory frameworks related to data governance, industrial safety, and carbon reporting are accelerating demand for transparent and explainable AI-driven production systems. Sustainability initiatives targeting 20–30% industrial energy reduction by 2030 are pushing manufacturers toward AI-based optimization platforms. Adoption of emerging technologies such as AI-powered digital twins and closed-loop quality systems is expanding rapidly in smart factories. Regional consumer and enterprise behavior reflects high sensitivity to compliance and explainability, with over 58% of industrial buyers preferring platforms offering audit-ready AI decision logs.

Asia-Pacific ranks first globally by production volume and holds around 29.4% market share, supported by manufacturing-heavy economies such as China, Japan, South Korea, and India. China alone hosts more than 45% of the region’s smart factories, while Japan and South Korea lead in robotics density and precision manufacturing. Infrastructure expansion, electronics assembly, automotive electrification, and semiconductor fabrication are major demand drivers. Regional innovation hubs are heavily focused on AI-enabled robotics, edge computing, and autonomous production control. Local technology firms are rapidly scaling AI platforms tailored for high-throughput factories. Consumer and enterprise behavior shows growth driven by e-commerce logistics, mobile AI applications, and rapid factory digitization, with over 60% of manufacturers planning AI-led production upgrades within three years.

South America contributes approximately 3.8% of the global market, led by Brazil and Argentina. Adoption is concentrated in food & beverage processing, mining equipment manufacturing, automotive assembly, and energy infrastructure. Governments are promoting industrial automation through tax incentives, import duty reductions on advanced machinery, and digital industry programs. Energy-sector modernization, particularly in oil, gas, and renewables, is driving interest in AI-driven production optimization. Local industrial players increasingly deploy AI platforms for predictive maintenance to manage aging assets. Regional consumer behavior shows demand closely tied to media localization, language-specific AI interfaces, and cost-sensitive automation, especially among mid-sized manufacturers.

The Middle East & Africa region holds around 2.5% market share, with demand centered in the UAE, Saudi Arabia, and South Africa. Oil & gas processing, construction materials, metals, and logistics hubs are primary adopters. National visions focused on industrial diversification and smart infrastructure are supporting AI-driven manufacturing platforms. Technological modernization trends include deployment of AI for predictive asset management and energy optimization in large industrial complexes. Regional regulations emphasize localization, data sovereignty, and strategic trade partnerships. Consumer and enterprise behavior reflects preference for turnkey AI platforms that reduce dependence on imported expertise and enable rapid operational scaling in capital-intensive industries.

United States – 28.9% Market Share: Dominance driven by high smart-factory density, advanced semiconductor and aerospace manufacturing, and early adoption of AI-native production platforms.

China – 21.4% Market Share: Leadership supported by massive industrial production capacity, rapid automation rollout, and large-scale deployment of AI-driven smart manufacturing zones.

The AI-Drivening Production Platforms Market is characterized by a moderately consolidated competitive environment with a broad mix of legacy industrial automation leaders, software and cloud platform providers, and emerging specialized AI innovators. Collectively, the top five companies hold an estimated 58–62% combined share of the addressable production platforms segment, reflecting strong positions for major incumbents alongside significant room for emerging challengers. Key competitors include industrial software giants with deep automation portfolios, platform providers embedding AI into manufacturing execution and ERP systems, and cloud/edge infrastructure vendors enabling scalable AI operations.

Market participation is robust, with dozens of active competitors ranging from established firms to agile startups. Strategic initiatives shaping competition include multi-party partnerships—for example, extended alliances between industrial players and hyperscale cloud vendors to integrate generative AI and digital thread technologies into production workflows. There are frequent product launches of advanced digital twin orchestration suites, AI-native quality inspection modules, and reinforcement learning-driven scheduling engines, along with ecosystem collaborations for agentic AI, predictive maintenance, and cross-enterprise analytics.

Innovation trends driving competitive dynamics include AI-enabled edge computing for low-latency decisioning, hybrid cloud–edge integration for secure operations, and domain-specific AI models tailored to discrete and process industries. Corporate strategies increasingly emphasize open platforms, partner ecosystems, and verticalized solutions that reduce integration friction for manufacturers. As a result, incumbents are rapidly evolving traditional automation portfolios into AI-centric platforms, while new entrants focus on niche capabilities such as machine health prediction, multimodal sensor fusion, or autonomous production control. The competitive landscape remains dynamic and technology-intensive, demanding strong R&D, ecosystem engagement, and operational scalability from all market participants.

Honeywell International Inc.

ABB Ltd.

IBM Corporation

GE Digital

Microsoft Azure AI

SAP SE

PTC Inc.

Dassault Systèmes (DELMIA)

Honeywell Forge

Authentise

DataRobot

C3.ai

Oracle AI Platform

AWS AI Services

Hexagon Manufacturing Intelligence

The AI-Drivening Production Platforms Market is being reshaped by a suite of advanced technologies that fundamentally enhance how manufacturing operations are executed and optimized. Core technologies include industrial digital twins, which generate virtual replicas of production lines that enable real-time simulation, scenario planning, and what-if analysis to mitigate risk before physical changes are made. Digital twin frameworks are now embedded in mainstream platforms, enabling end-to-end visibility across design, engineering, and shop floor execution. Edge computing and on-device AI inference are increasingly critical for low-latency decisioning; by moving analytics closer to sensors and robotics, manufacturers can achieve response times measured in milliseconds for safety and quality control tasks.

Generative design and agentic AI are emerging as powerful tools that automate blueprint creation, optimize production sequences, and synthesize repair strategies based on historical performance data. Generative approaches coupled with reinforcement learning are now automating production scheduling and resource allocation, adapting to variability in yields and supply chain constraints without human intervention. Robotics platforms integrated with AI perception stacks enable autonomous material handling and collaborative robot operations that reduce human intervention in repetitive or hazardous tasks.

Platform orchestration layers are integrating multimodal data streams from machine vision, time-series sensors, and maintenance logs into unified dashboards that provide contextual insights and predictive alerts. These systems are enhancing situational awareness for plant managers by interpreting anomalies, forecasting failures, and prescribing corrective actions. Hybrid cloud–on-premises architectures are enabling scalable analytics while balancing data sovereignty and security constraints.

Finally, programmable industrial AI models tailored to specific verticals—such as automotive, semiconductor, and process industries—are enabling deeper domain context, interpretability, and integration with existing ERP and MES systems. These technology trends are collectively driving operational resilience, higher throughput, and flexible production paradigms well beyond traditional automation.

• In October 2025, Siemens and NVIDIA expanded their strategic collaboration to build an Industrial AI Operating System designed to bring AI-driven innovation across design, engineering, production, and supply chains, enabling faster optimization and continuous manufacturing improvement. Source: www.nvidianews.nvidia.com

• In June 2025, Siemens recruited a leading AI expert from Amazon to lead its data and artificial intelligence initiatives, advancing development of AI tools such as Industrial Copilot that enhance productivity and human–machine collaboration in manufacturing ecosystems. Source: www.reuters.com

• In March 2025, Siemens announced a $285 million investment in U.S. manufacturing facilities, including support for AI data center infrastructure and production equipment, creating over 900 skilled manufacturing jobs and reinforcing AI-enabled industrial innovation. Source: www.apnews.com

• In December 2025, OpenAI and major industry participants revealed expanded AI infrastructure agreements, including plans for multi-gigawatt AI compute deployments and long-term chip procurement commitments to support large-scale enterprise AI workloads. Source: www.en.wikipedia.org

The AI-Drivening Production Platforms Market Report provides a comprehensive view of the technologies, applications, and industry strategies that shape how artificial intelligence is embedded in modern production environments. It spans product types including platform orchestration suites, industrial digital twins, edge AI controllers, robotics and automation interfaces, and predictive analytics modules. The report also covers application domains, such as predictive maintenance, autonomous production control, quality assurance, energy optimization, supply chain integration, and hybrid cloud–edge deployment models. Geographic coverage includes detailed insights for North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with region-specific trends in manufacturing digitization, regulatory frameworks, workforce evolution, and infrastructure readiness.

Industry verticals examined in the scope include automotive, semiconductors and electronics, chemicals and process industries, aerospace and defense, consumer goods, and energy & utilities, offering end-user perspectives on adoption intensity and operational value realization. Technology focus areas extend to digital twin orchestration, reinforcement learning for scheduling, multimodal data integration, autonomous robotics, and hybrid architectures balancing on-premises systems with cloud analytics. The report evaluates competitive positioning and innovation trends, assessing strategic partnerships, product launches, ecosystem alliances, and channel strategies shaping market leadership. It also highlights emerging segments such as agentic AI production agents, software-defined automation, and integrated human–AI collaboration tools that are defining next-generation production paradigms. Tailored for decision-makers, the report elucidates platform capabilities, integration challenges, implementation best practices, and operational outcomes to support strategic investments, partner selection, and digital transformation roadmaps.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,700.0 Million |

| Market Revenue (2033) | USD 29,858.1 Million |

| CAGR (2026–2033) | 26% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens; Rockwell Automation; NVIDIA; Honeywell; ABB; IBM; GE Digital; Microsoft Azure AI; SAP; PTC; Dassault Systèmes (DELMIA); Authentise; DataRobot; C3.ai; Oracle AI; AWS Industrial AI; Hexagon Manufacturing Intelligence |

| Customization & Pricing | Available on Request (10% Customization Free) |