Reports

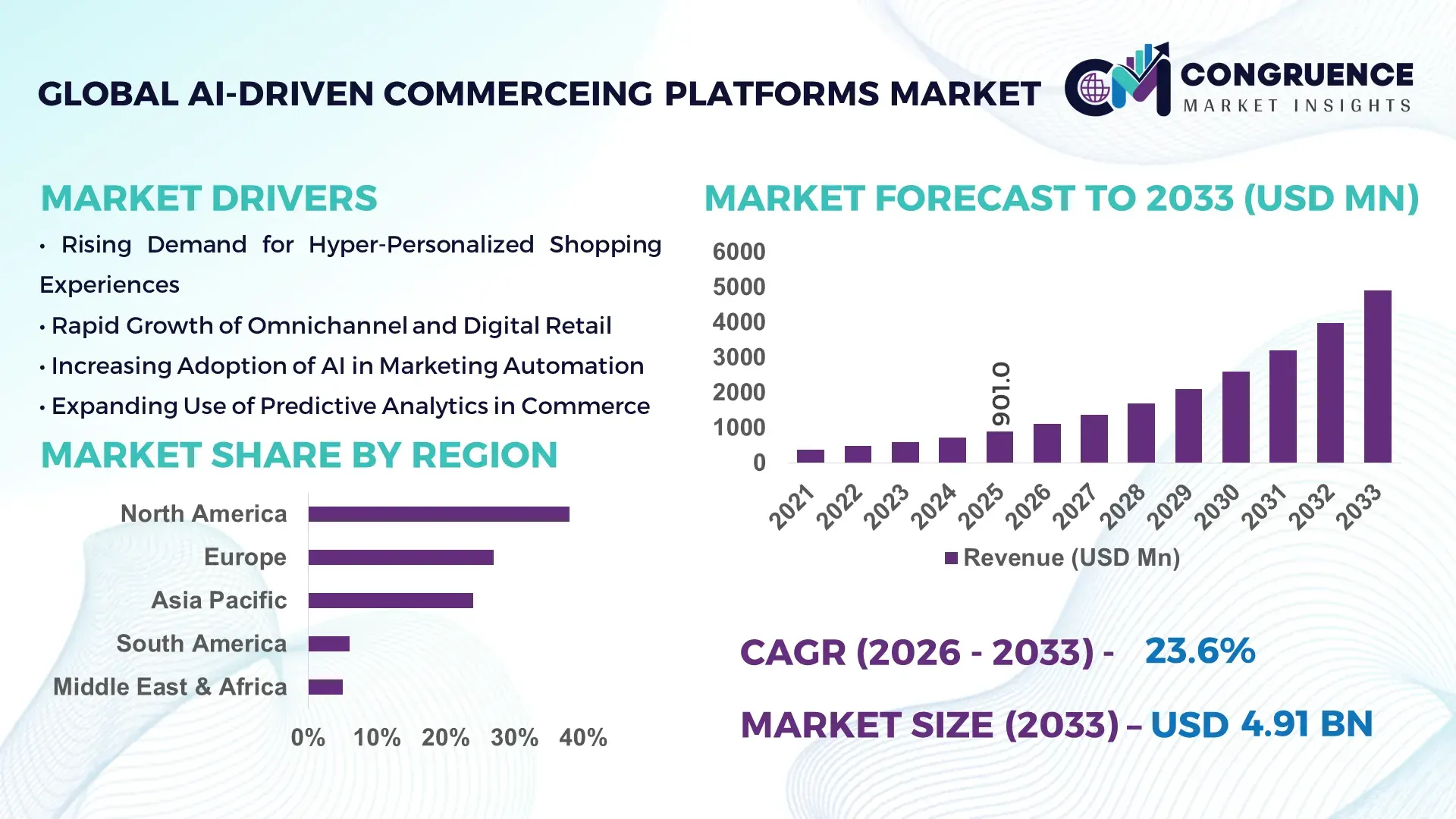

The Global AI-Driven Commerceing Platforms Market was valued at USD 901.0 Million in 2025 and is anticipated to reach a value of USD 4,907.6 Million by 2033 expanding at a CAGR of 23.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rapid enterprise adoption of AI-powered personalization, real-time pricing engines, and automated customer engagement tools across digital commerce ecosystems.

The United States represents the dominant country in the AI-Driven Commerceing Platforms Market, supported by advanced digital infrastructure and significant AI investments. In 2025, U.S.-based enterprises accounted for over 38% of global AI commerce platform deployments, with more than 72% of mid-to-large retailers integrating AI-driven recommendation engines. Annual private AI investment in the U.S. exceeded USD 60 billion, with a significant portion directed toward retail-tech and commerce automation platforms. Over 65% of U.S. e-commerce transactions involve AI-powered personalization layers, and fulfillment centers increasingly deploy AI-based demand forecasting systems achieving up to 30% inventory optimization improvements. The country also leads in cloud AI infrastructure capacity, hosting more than 40% of global hyperscale data centers supporting commerce AI workloads.

Market Size & Growth: Valued at USD 901.0 Million in 2025, projected to reach USD 4,907.6 Million by 2033, expanding at 23.6% CAGR due to increasing AI-driven personalization and automation in digital commerce.

Top Growth Drivers: 68% retailer adoption of AI recommendation engines; 45% improvement in conversion rates via AI personalization; 32% reduction in cart abandonment through predictive engagement tools.

Short-Term Forecast: By 2028, AI-powered pricing optimization is expected to improve gross margin efficiency by 18% and reduce customer acquisition costs by 22%.

Emerging Technologies: Generative AI storefront assistants, real-time behavioral analytics engines, autonomous inventory orchestration platforms.

Regional Leaders: North America projected at USD 1,950.0 Million by 2033 with high SaaS adoption; Asia-Pacific at USD 1,420.0 Million driven by mobile commerce growth; Europe at USD 980.0 Million supported by cross-border e-commerce digitization.

Consumer/End-User Trends: Over 74% of online shoppers prefer AI-curated recommendations; 58% engage with AI chat assistants during purchase journeys.

Pilot or Case Example: In 2024, a global retailer implemented AI demand forecasting and achieved 27% inventory holding cost reduction and 19% fulfillment time improvement.

Competitive Landscape: Market leader holds approximately 21% share, followed by Shopify, Salesforce Commerce Cloud, Adobe Commerce, SAP Commerce Cloud, and BigCommerce.

Regulatory & ESG Impact: Data protection frameworks and AI governance mandates are driving 40% increase in compliance-focused AI auditing tools adoption.

Investment & Funding Patterns: Over USD 8.5 Billion invested globally in AI-commerce startups between 2022–2025, with strong venture funding in predictive analytics and generative AI.

Innovation & Future Outlook: Increasing API-first architectures, AI-native commerce stacks, and embedded finance integration are shaping long-term digital retail transformation.

Retail contributes approximately 48% of total platform deployments, followed by consumer electronics (18%), fashion (16%), and grocery (11%). Generative AI storefronts and AI-powered visual search tools improved engagement rates by 35% in 2024 pilots. Data localization regulations across Europe and Asia are influencing regional cloud deployments. Mobile-first markets in Asia-Pacific account for over 60% of AI-commerce transaction interactions. The outlook indicates deeper AI-native commerce ecosystems and embedded predictive automation across supply chains.

The AI-Driven Commerceing Platforms Market holds strong strategic relevance as enterprises transition toward data-centric and predictive commerce ecosystems. AI-native commerce stacks are enabling hyper-personalization, automated merchandising, and real-time dynamic pricing across omnichannel retail environments. For example, generative AI-driven product recommendation systems deliver 45% higher conversion rates compared to rule-based personalization engines. Similarly, autonomous demand forecasting platforms reduce stockouts by 28% compared to traditional ERP-based planning tools.

North America dominates in deployment volume, while Asia-Pacific leads in mobile commerce adoption with over 64% of digital consumers interacting through AI-enabled mobile storefronts. European enterprises demonstrate strong AI governance integration, with more than 52% of retailers implementing AI compliance frameworks aligned with emerging regulatory standards.

By 2028, predictive AI engines are expected to reduce fulfillment cycle times by 25% and improve last-mile delivery efficiency by 18%. Firms are committing to ESG metrics such as 30% carbon footprint reduction in logistics networks by 2030 through AI-based route optimization and warehouse automation.

In 2024, a leading U.S.-based retailer achieved a 31% improvement in personalized marketing ROI through AI-driven behavioral analytics integration. The AI-Driven Commerceing Platforms Market is increasingly positioned as a pillar of digital resilience, regulatory compliance, and sustainable growth, enabling enterprises to scale operations while maintaining operational transparency and efficiency.

The AI-Driven Commerceing Platforms Market is shaped by rapid digital transformation across retail, B2B commerce, and direct-to-consumer channels. Increasing integration of AI-powered chatbots, recommendation systems, and predictive analytics tools has redefined digital engagement models. Over 70% of enterprise retailers now use at least one AI-enabled commerce function, reflecting mainstream adoption. Cloud-native deployment models, API-driven ecosystems, and composable commerce architectures are strengthening interoperability across digital systems. Additionally, rising consumer demand for real-time personalization and frictionless checkout experiences is accelerating AI investments. However, governance, cybersecurity, and high implementation complexity remain critical considerations for decision-makers evaluating AI-driven commerce modernization.

Hyper-personalization has emerged as a key growth catalyst in the AI-Driven Commerceing Platforms Market. Studies indicate that AI-driven recommendation engines improve customer retention by up to 36% and increase average order values by nearly 28%. Around 74% of digital consumers expect personalized product suggestions, while 63% prefer AI-curated offers tailored to browsing history. Retailers deploying real-time behavioral analytics report a 32% reduction in bounce rates. Additionally, AI-driven email marketing automation improves click-through rates by approximately 29%. As enterprises shift toward data-centric engagement models, hyper-personalization capabilities are becoming a competitive differentiator, driving widespread implementation across online marketplaces and omnichannel retail networks.

Stringent data protection regulations and AI governance frameworks present implementation challenges. Over 58% of enterprises report compliance complexity as a barrier to scaling AI-powered commerce solutions. Data localization mandates in multiple jurisdictions require region-specific cloud infrastructure, increasing deployment costs by approximately 20%. Consumer surveys indicate that 49% of online users are concerned about AI-based data tracking practices. Moreover, cybersecurity risks associated with AI algorithms handling large datasets have risen, with retail cyberattacks increasing by nearly 25% year-over-year. These factors collectively slow deployment timelines and necessitate robust compliance investments, impacting platform scalability.

Omnichannel retail expansion presents significant growth opportunities. Over 67% of global retailers now operate across at least three digital channels, creating demand for AI-powered unified commerce orchestration. AI-based cross-channel inventory management improves stock visibility accuracy by 34%. Additionally, predictive analytics enhances demand forecasting precision by 26%, reducing surplus inventory levels. Emerging markets in Asia-Pacific show mobile commerce penetration exceeding 70%, encouraging AI integration for localized recommendations and digital wallet optimization. Enterprises leveraging AI-driven customer data platforms achieve 22% higher campaign performance, underscoring strong expansion potential in integrated commerce ecosystems.

Integration complexity remains a significant challenge for enterprises modernizing legacy commerce systems. Approximately 46% of retailers report interoperability issues between AI modules and traditional ERP or CRM systems. Deployment cycles often extend 30–40% longer when legacy data infrastructure requires restructuring. Skilled AI talent shortages also persist, with nearly 35% of enterprises citing workforce capability gaps. Furthermore, continuous model training and algorithm optimization demand ongoing infrastructure investment. These operational complexities can delay full-scale implementation and impact expected performance improvements, particularly for mid-sized enterprises transitioning from conventional commerce platforms.

74% Surge in AI-Powered Personalization Deployment: Retailers increasingly embed AI recommendation engines, with 74% of large enterprises using real-time personalization tools in 2025. AI-driven product suggestions have lifted conversion rates by 45% and improved customer retention by 36%, reflecting measurable performance gains across digital storefronts.

52% Adoption of Generative AI Commerce Assistants: Over 52% of enterprise commerce platforms integrated generative AI chat assistants in 2024–2025. These assistants reduced customer query resolution time by 41% and improved engagement duration by 33%, enhancing digital shopping experiences and reducing support workload.

28% Improvement in AI-Based Demand Forecasting Accuracy: Advanced machine learning forecasting systems enhanced inventory accuracy by 28% and reduced stockouts by 24%. Warehouses using AI-driven predictive analytics observed 19% faster order processing cycles, strengthening supply chain responsiveness.

60% Growth in Mobile-First AI Commerce Interactions: In Asia-Pacific, more than 60% of AI-powered commerce interactions occur via mobile devices. AI-based mobile optimization improved checkout completion rates by 27% and increased digital wallet usage by 22%, reinforcing the importance of AI-native mobile commerce ecosystems.

The AI-Driven Commerceing Platforms Market is segmented by type, application, and end-user, reflecting the layered integration of artificial intelligence across digital commerce ecosystems. From a product perspective, the market includes AI personalization engines, predictive analytics and demand forecasting systems, conversational AI and virtual assistants, dynamic pricing engines, fraud detection modules, and AI-powered visual search solutions. Personalization and predictive analytics collectively account for more than 55% of total platform deployments due to their measurable impact on conversion optimization and operational efficiency. By application, digital retail and omnichannel commerce dominate usage, followed by marketing automation, supply chain optimization, customer engagement management, and fraud prevention. Over 70% of large enterprises deploy AI commerce tools across at least three functional areas. End-user segmentation highlights strong adoption among retail enterprises, direct-to-consumer brands, marketplaces, and B2B commerce providers. Enterprise-level retailers represent the highest deployment intensity, while SMEs are increasingly adopting SaaS-based AI commerce modules, contributing to a diversified and innovation-driven market landscape.

The AI-Driven Commerceing Platforms Market by type comprises AI personalization engines, predictive analytics & demand forecasting platforms, conversational AI & chatbots, dynamic pricing engines, fraud detection systems, and AI-based visual search solutions. AI personalization engines currently account for approximately 34% of overall adoption, as enterprises prioritize tailored recommendations and behavior-driven content delivery to improve engagement metrics. Predictive analytics platforms hold around 22%, driven by inventory optimization and real-time supply chain visibility. Conversational AI systems represent nearly 18% of implementations, while dynamic pricing engines contribute 14%. Fraud detection and visual search collectively account for the remaining 12% of deployments. Among these, predictive analytics and demand forecasting platforms are the fastest-growing segment, expanding at an estimated CAGR of 26.8%, supported by increasing cross-border commerce complexity and the need for inventory precision exceeding 90% accuracy rates. Retailers deploying AI forecasting report stockout reductions of up to 24% and warehouse efficiency gains of 19%. Conversational AI adoption is rising steadily due to 24/7 automated support capabilities, while AI-based visual search tools are gaining traction in fashion and consumer electronics, where image-based search improves product discovery rates by 27%.

Digital retail and omnichannel commerce currently represent the leading application area, accounting for nearly 46% of total AI-Driven Commerceing Platforms Market adoption. This dominance is driven by AI-powered product recommendations, personalized marketing workflows, and automated merchandising tools that enhance conversion rates by up to 45%. Marketing automation platforms hold approximately 21% of application usage, while supply chain and inventory optimization contribute around 17%. Customer service automation represents 9%, and fraud detection and risk management collectively account for the remaining 7%. Supply chain optimization is the fastest-growing application, expanding at an estimated CAGR of 27.4%, supported by rising global e-commerce transaction volumes and the need for predictive logistics orchestration. Enterprises implementing AI-based supply chain tools report delivery time reductions of 18% and fulfillment cost improvements of 15%. In 2025, more than 38% of enterprises globally reported piloting AI-driven commerce systems specifically for customer experience platforms. Additionally, over 60% of Gen Z consumers indicate stronger brand loyalty toward companies offering AI-personalized digital shopping journeys.

Retail enterprises remain the leading end-user segment, accounting for approximately 48% of total AI-Driven Commerceing Platforms Market adoption. Large-scale retailers deploy AI solutions across recommendation systems, pricing automation, and demand forecasting modules to manage high transaction volumes and omnichannel complexities. Online marketplaces represent about 19% of adoption, followed by direct-to-consumer (D2C) brands at 14%, and B2B commerce providers at 11%. Other sectors, including consumer electronics and grocery platforms, collectively contribute around 8%. SMEs constitute the fastest-growing end-user group, expanding at an estimated CAGR of 28.3%, driven by SaaS-based AI commerce subscriptions and low-code AI integration tools. Approximately 42% of SMEs in developed digital markets have adopted at least one AI-enabled commerce module. In 2025, more than 40% of global enterprises reported integrating AI-driven personalization within their primary commerce platforms. Furthermore, 58% of online consumers prefer AI-powered virtual assistants for product queries and order tracking.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 27.9% between 2026 and 2033.

North America’s leadership is supported by over 72% enterprise-level AI adoption in digital retail and more than 65% of mid-to-large retailers integrating AI-powered recommendation engines. Europe holds approximately 27% share, driven by cross-border e-commerce valued at over 30% of total online retail transactions within the region. Asia-Pacific accounts for nearly 24% of global adoption, supported by mobile commerce penetration exceeding 70% in major economies. South America contributes around 6%, while the Middle East & Africa collectively represent close to 5%, with increasing digital transformation initiatives and cloud infrastructure expansion across key economies. Regional disparities reflect differences in AI readiness, digital infrastructure density, and enterprise technology investments.

North America holds approximately 38% of the global AI-Driven Commerceing Platforms Market share, driven by strong enterprise IT budgets and advanced cloud infrastructure. The retail and consumer electronics sectors contribute over 55% of regional AI commerce deployments, followed by healthcare e-commerce and financial services platforms integrating AI-based personalization tools. Regulatory developments focusing on AI governance and consumer data protection have accelerated demand for explainable AI modules and compliance auditing tools. Technological advancements include API-first commerce architectures, AI-native SaaS platforms, and predictive analytics systems achieving over 85% forecast accuracy. A notable regional player, Shopify, continues expanding AI-enabled storefront automation and generative product description tools, supporting millions of merchants globally. Consumer behavior reflects high personalization expectations, with nearly 74% of digital shoppers engaging with AI-curated recommendations and over 60% using AI chat assistants during purchase journeys.

Europe accounts for nearly 27% of the global AI-Driven Commerceing Platforms Market share, with Germany, the United Kingdom, and France leading adoption. Cross-border digital trade represents over 30% of total online transactions in the region, encouraging AI-based localization and compliance tools. Regulatory frameworks emphasizing algorithm transparency and consumer privacy have driven a 40% increase in explainable AI implementation within commerce platforms. Emerging technologies such as AI-driven demand planning and sustainable supply chain analytics are gaining traction, particularly in Germany’s manufacturing-linked retail sector. SAP Commerce Cloud, headquartered in the region, continues integrating AI-based predictive merchandising modules for enterprise clients. Consumer preferences reflect strong data protection awareness, with 58% of online shoppers favoring platforms offering transparent AI decision-making mechanisms.

Asia-Pacific represents approximately 24% of global AI-Driven Commerceing Platforms Market adoption and ranks as the fastest-growing regional ecosystem. China, India, and Japan are the top consuming countries, collectively accounting for more than 65% of regional deployments. Mobile commerce accounts for over 70% of AI-driven transaction interactions in the region, significantly influencing platform architecture. Infrastructure expansion includes rapid cloud data center growth and digital payment integration across urban and semi-urban markets. Innovation hubs in China and India are accelerating AI-based visual search and conversational commerce technologies. Alibaba has integrated AI-powered recommendation systems and logistics optimization tools across its marketplaces, enhancing order accuracy above 90%. Consumer behavior trends show strong mobile engagement, with more than 68% of users interacting through AI-powered apps during purchasing decisions.

South America contributes approximately 6% of the global AI-Driven Commerceing Platforms Market share, with Brazil and Argentina leading regional adoption. Brazil accounts for over 55% of regional AI-commerce deployments due to rapid digital retail growth and fintech integration. Infrastructure improvements in broadband and cloud computing capacity have increased AI platform penetration by nearly 20% in major metropolitan centers. Government digital transformation programs and trade policy reforms are encouraging cross-border commerce digitization. Mercado Libre, a key regional player, has integrated AI-based fraud detection and recommendation engines, improving transaction security and personalization accuracy. Consumer behavior is influenced by language localization and mobile-first usage patterns, with over 62% of digital shoppers accessing platforms primarily via smartphones.

The Middle East & Africa region holds close to 5% of the global AI-Driven Commerceing Platforms Market share, with the UAE and South Africa emerging as key growth countries. Digital modernization initiatives and smart city programs are increasing AI platform integration within retail and service sectors. Over 50% of enterprise retailers in the UAE have adopted AI-powered customer analytics tools. Technological trends include AI-based logistics optimization and multilingual conversational commerce solutions tailored for diverse populations. Government-backed digital economy strategies are fostering cross-border e-commerce adoption and cloud investments. Regional consumer behavior reflects rising demand for seamless digital payments and AI-assisted shopping experiences, with nearly 57% of online consumers engaging with automated customer support tools during transactions.

United States – 34% Market Share: Dominates due to high enterprise AI investment levels, advanced cloud infrastructure, and widespread personalization engine deployment.

China – 21% Market Share: Leads in large-scale mobile commerce integration and AI-powered marketplace ecosystems supported by extensive digital payment infrastructure and platform innovation.

The AI-Driven Commerceing Platforms Market demonstrates a moderately fragmented competitive structure, with more than 120 active global and regional vendors offering AI-native commerce modules, SaaS-based personalization tools, and enterprise-grade predictive analytics platforms. The top five companies collectively account for approximately 52% of total market share, reflecting a semi-consolidated environment where established enterprise software providers coexist with agile AI-first startups.

Leading vendors compete primarily on AI model sophistication, ecosystem integration capability, cloud scalability, and compliance-readiness. Over 68% of enterprise buyers prioritize platforms that integrate seamlessly with ERP, CRM, and digital payment systems. Strategic initiatives between 2024 and 2025 included over 35 documented partnerships focused on generative AI integration, composable commerce architectures, and cross-border digital retail expansion. Product launches increasingly emphasize AI-powered recommendation engines delivering up to 45% higher conversion rates and predictive demand systems achieving 85–90% forecast accuracy.

Mergers and acquisitions remain active, particularly in AI-based customer data platforms and fraud detection solutions. Approximately 40% of competitive differentiation now stems from embedded generative AI capabilities and real-time behavioral analytics. Vendors are also investing heavily in ESG-aligned AI logistics tools, with 30% of new product rollouts featuring carbon-optimized supply chain modules. The competitive environment continues to evolve toward AI-native, API-first commerce ecosystems capable of supporting omnichannel and cross-border digital transactions.

SAP

BigCommerce

Oracle

Alibaba Group

Amazon Web Services

VTEX

Wix

commercetools

Spryker

Elastic Path

Dynamic Yield

Bloomreach

Algolia

Technological advancement in the AI-Driven Commerceing Platforms Market is driven by generative AI, machine learning-based predictive analytics, and composable commerce architectures. Generative AI storefront assistants are now deployed by over 50% of large retailers, enabling automated product descriptions, intelligent search results, and conversational purchasing journeys. These systems reduce manual content creation time by approximately 35% and improve engagement metrics by over 30%.

Predictive analytics engines leverage real-time behavioral datasets exceeding billions of transaction records daily, enhancing demand forecasting accuracy above 85%. Reinforcement learning-based pricing models dynamically adjust prices within milliseconds, improving margin optimization by up to 18%. AI-powered fraud detection platforms analyze over 200 data variables per transaction, reducing fraudulent payment attempts by nearly 25%.

Cloud-native infrastructure remains foundational, with more than 70% of AI commerce platforms deployed on multi-cloud or hybrid environments. API-first composable commerce frameworks enable enterprises to integrate over 15–20 microservices into a single digital storefront architecture. Edge AI computing is gaining momentum, reducing latency in mobile commerce transactions by 20–25%.

Emerging innovations include AI-driven visual search systems capable of recognizing over 100,000 SKU variants with image-matching accuracy exceeding 90%. Additionally, embedded finance integration—combining AI credit scoring and payment optimization—has improved checkout completion rates by 27%. For decision-makers, technology adoption is increasingly focused on scalability, governance, cybersecurity resilience, and measurable operational efficiency gains.

• In May 2025, Shopify launched its new integrated “AI Store Builder” feature, enabling merchants to automatically generate complete online stores — including layouts, images, and text — from descriptive keywords, significantly reducing setup time and simplifying digital commerce creation for sellers. Source: www.reuters.com

• In October 2025, Salesforce expanded its partnerships with OpenAI and Anthropic, integrating GPT-5 and Claude AI models into its Agentforce 360 platform, including a new Agentforce Commerce feature that enables merchants to facilitate product sales through ChatGPT Instant Checkout while retaining control of customer data. Source: www.reuters.com

• In March 2025, Adobe introduced AI agents within Adobe Experience Cloud, delivering advanced AI capabilities across customer journey optimization and personalized omnichannel experiences, including new AI modules for account orchestration, content generation, and automated performance insights for enterprises globally. Source: www.adobe.com

• In July 2025, Alibaba and Wix announced a strategic partnership to empower SMBs by integrating Wix’s AI-driven commerce tools with Alibaba’s B2B marketplace, allowing Wix merchants access to global sourcing and Alibaba sellers to leverage AI storefront and marketing automation tools. Source: www.techradar.com

The AI-Driven Commerceing Platforms Market Report provides comprehensive coverage of product types, application domains, end-user industries, technological innovations, and geographic distribution across five major regions and over 20 key countries. The report evaluates AI personalization engines, predictive analytics systems, conversational AI modules, dynamic pricing platforms, fraud detection tools, and visual search technologies deployed across digital commerce environments.

It analyzes application-level deployment across digital retail, omnichannel commerce, supply chain optimization, marketing automation, customer engagement management, and risk mitigation. Retail enterprises account for nearly 48% of total deployments, while marketplaces, D2C brands, and B2B commerce providers contribute significant adoption volumes.

Geographic coverage includes North America (38% share), Europe (27%), Asia-Pacific (24%), South America (6%), and the Middle East & Africa (5%), highlighting regional technology maturity, enterprise adoption rates, and infrastructure readiness. The report further assesses emerging segments such as embedded finance, AI-powered visual commerce, and generative AI storefront assistants.

Technology evaluation includes cloud-native AI stacks, composable commerce frameworks, multi-cloud orchestration, cybersecurity layers, and ESG-driven AI logistics optimization systems. Decision-makers gain insight into adoption metrics, operational performance benchmarks, competitive intensity, regulatory considerations, and digital transformation strategies shaping the next phase of AI-native commerce ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 901.0 Million |

| Market Revenue (2033) | USD 4,907.6 Million |

| CAGR (2026–2033) | 23.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Shopify; Salesforce; Adobe; SAP; BigCommerce; Oracle; Alibaba Group; Amazon Web Services; VTEX; Wix; commercetools; Spryker; Elastic Path; Dynamic Yield; Bloomreach; Algolia |

| Customization & Pricing | Available on Request (10% Customization Free) |