Reports

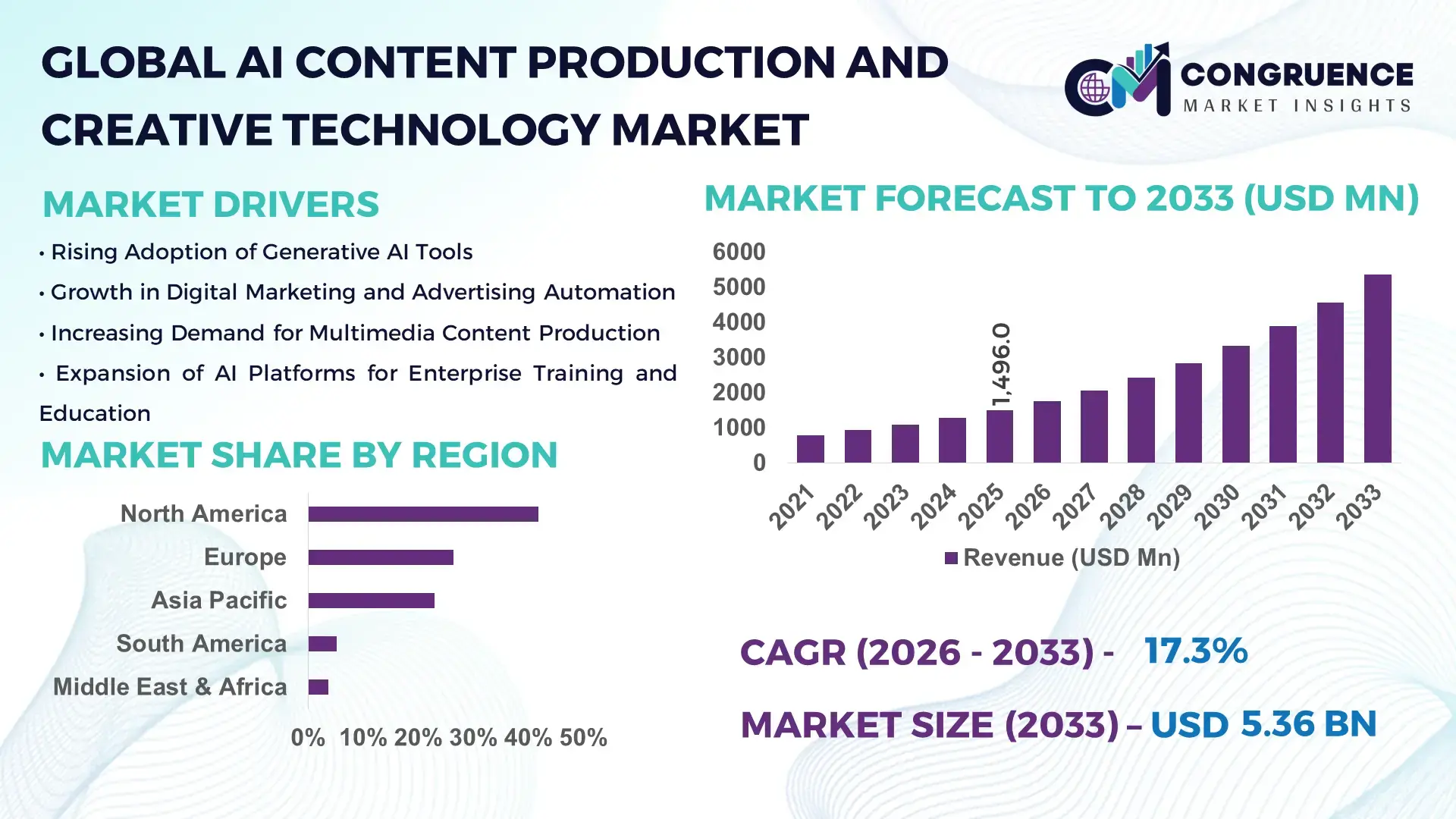

The Global AI Content Production and Creative Technology Market was valued at USD 1,496.0 Million in 2025 and is anticipated to reach a value of USD 5,361.9 Million by 2033 expanding at a CAGR of 17.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rapid enterprise adoption of generative AI platforms to automate content creation workflows, enhance creative productivity, and reduce time-to-market across media, marketing, and digital commerce ecosystems.

The United States dominates the global AI Content Production and Creative Technology Market, supported by advanced AI production infrastructure, high capital inflows, and widespread enterprise deployment. In 2024, U.S.-based firms accounted for over USD 45 billion in generative AI investment, with more than 68% of large media and marketing enterprises integrating AI-driven content tools into daily operations. The country leads in large-scale deployment of multimodal foundation models, AI-assisted video production, and real-time personalization engines. Over 72% of global AI content startups are headquartered or operate major R&D centers in the U.S., while cloud-based creative AI workloads exceed 60 exaFLOPS in processing capacity. Adoption is particularly strong in advertising, entertainment, gaming, and e-commerce, where AI-generated assets now represent over 40% of digital content outputs, supported by continuous advancements in natural language processing, diffusion-based image generation, and AI video synthesis technologies.

Market Size & Growth: Valued at USD 1,496.0 Million in 2025 and projected to reach USD 5,361.9 Million by 2033, expanding at a CAGR of 17.3%, driven by automation of creative workflows and rising demand for scalable digital content.

Top Growth Drivers: Enterprise generative AI adoption (62%), creative productivity improvement (48%), reduction in content production timelines (41%).

Short-Term Forecast: By 2028, AI-driven content automation is expected to reduce average production costs by 32% across media and marketing operations.

Emerging Technologies: Multimodal generative AI, real-time AI video synthesis, and AI-powered creative copilots.

Regional Leaders: North America projected at USD 2,140.0 Million by 2033 with enterprise-scale adoption; Europe at USD 1,380.0 Million driven by regulatory-aligned AI tools; Asia Pacific at USD 1,120.0 Million supported by creator economy expansion.

Consumer/End-User Trends: Media houses, digital marketers, and e-commerce platforms account for over 65% of AI content tool usage.

Pilot or Case Example: In 2024, a U.S.-based streaming platform achieved a 37% reduction in content localization time using AI dubbing and subtitling.

Competitive Landscape: Market leader Adobe with ~28% share, followed by OpenAI, Microsoft, Meta, Runway AI, and Stability AI.

Regulatory & ESG Impact: AI transparency rules and copyright compliance frameworks accelerating responsible AI deployment.

Investment & Funding Patterns: Over USD 22 billion invested globally in creative AI platforms during the last two years, led by venture capital and strategic partnerships.

Innovation & Future Outlook: Integration of AI with AR/VR, real-time personalization engines, and enterprise creative clouds shaping next-generation content ecosystems.

AI Content Production and Creative Technology Market solutions serve media & entertainment (34%), advertising & marketing (29%), e-commerce (18%), and gaming & immersive media (11%). Recent innovations include AI video generators, text-to-3D engines, and rights-aware content models. Regulatory focus on ethical AI, regional consumption growth in Asia Pacific, and increasing demand for personalized digital experiences are defining long-term market momentum.

The AI Content Production and Creative Technology Market has become strategically critical as enterprises shift toward scalable, data-driven, and personalized digital engagement models. Organizations are increasingly embedding generative AI into content pipelines to reduce manual effort, accelerate creative cycles, and improve audience targeting. For instance, multimodal generative AI delivers 45% faster asset creation compared to traditional manual creative workflows. North America dominates in content production volume, while Europe leads in structured enterprise adoption with 58% of large firms deploying governed AI creative platforms.

In the short term, by 2028, real-time generative AI personalization is expected to improve campaign performance metrics such as click-through rates by 30% and reduce creative iteration cycles by 40%. Compliance and ESG considerations are also shaping strategy, with firms committing to responsible AI frameworks, including 50% reduction in non-compliant content risks by 2027 through watermarking and content traceability tools.

A micro-scenario illustrates this impact: in 2024, a U.S.-based global retailer achieved a 35% reduction in content localization costs by deploying AI-driven multilingual creative engines across 20 markets. Looking ahead, the AI Content Production and Creative Technology Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable digital growth, enabling enterprises to scale creativity while maintaining governance and efficiency.

The AI Content Production and Creative Technology Market is shaped by accelerating digital transformation, rising demand for personalized content, and advances in generative AI architectures. Enterprises are transitioning from manual content creation toward AI-augmented workflows to manage growing content volumes across omnichannel platforms. The market is influenced by improvements in computing efficiency, expanding cloud AI infrastructure, and increasing integration of creative AI into enterprise software ecosystems. At the same time, regulatory scrutiny around AI ethics, copyright protection, and data governance is shaping deployment strategies. Competitive intensity is increasing as technology vendors focus on multimodal capabilities, real-time generation, and enterprise-grade governance features to meet evolving customer requirements.

Enterprises are facing exponential growth in digital touchpoints, requiring high-volume, customized content across platforms. AI-driven creative tools enable automation of text, image, video, and audio production, reducing dependency on manual resources. Surveys indicate that over 60% of enterprises using AI content tools report faster campaign launches, while 52% experience improved brand consistency across regions. Marketing teams using AI copilots generate up to 3× more content outputs per quarter, supporting rapid market responsiveness. This scalability requirement is a primary driver of sustained market expansion.

Concerns around copyright infringement, data sourcing transparency, and content ownership remain significant barriers. Nearly 48% of enterprises cite uncertainty around AI-generated content rights as a deployment challenge. Legal disputes related to training data usage and content attribution have increased compliance costs, delaying adoption in regulated industries such as publishing and broadcasting. These issues necessitate advanced governance frameworks, increasing implementation complexity and slowing market penetration in certain regions.

AI enables hyper-personalized content experiences based on user behavior, language, and preferences. Platforms leveraging AI-driven personalization report 25–40% improvements in engagement metrics. Emerging opportunities exist in AI-generated immersive content, real-time adaptive advertising, and localized creative assets for global brands. As consumer expectations for tailored experiences rise, demand for AI-powered creative personalization solutions continues to expand.

Despite automation benefits, effective AI content deployment requires skilled talent and robust infrastructure. Approximately 44% of organizations report skill gaps in AI model governance and creative AI integration. High-performance computing requirements and integration with legacy systems increase operational complexity. Addressing these challenges requires sustained investment in workforce upskilling and scalable cloud infrastructure.

Expansion of Multimodal Generative AI Platforms: Enterprises increasingly deploy multimodal models combining text, image, audio, and video generation. In 2024, over 57% of new AI content deployments supported at least three content formats, improving cross-channel consistency and reducing asset development cycles by 38%.

Rise of Real-Time AI Personalization Engines: AI systems now dynamically adapt content based on user behavior and context. Brands using real-time AI personalization report 29% higher engagement rates and 22% improvement in conversion efficiency, particularly in e-commerce and digital advertising.

Integration of AI Creative Tools into Enterprise Software: Creative AI is being embedded into CRM, CMS, and marketing automation platforms. Nearly 61% of large enterprises now access AI content tools directly within existing software stacks, reducing workflow friction and improving collaboration efficiency by 33%.

Governance-First AI Content Frameworks: Adoption of watermarking, audit trails, and rights management tools is accelerating. By 2025, over 46% of enterprises plan to deploy AI content governance solutions to mitigate compliance risks and improve transparency, supporting long-term responsible AI adoption.

The AI Content Production and Creative Technology Market is segmented based on type, application, and end-user, reflecting the diverse ways AI is embedded across creative value chains. By type, the market spans language-based, vision-based, audio-based, and multimodal AI systems, each enabling different levels of automation and creative augmentation. Application-wise, adoption is concentrated in media production, digital marketing, entertainment, gaming, and enterprise communications, where content volume, personalization, and speed are critical. End-user segmentation highlights strong uptake among media & entertainment companies, marketing agencies, enterprises, and emerging creator-led businesses. Across all segments, demand is shaped by the need for scalable content creation, cross-platform consistency, multilingual delivery, and governance-ready AI systems, making segmentation a key lens for understanding competitive positioning and adoption behavior.

The market by type includes text-based AI models, vision-language models, audio-text systems, video-language models, and multimodal generative AI platforms. Vision-language models currently represent the leading type, accounting for approximately 42% of overall adoption, due to their widespread use in image generation, design automation, and visual content tagging across marketing and media workflows. Audio-text systems follow with around 25% adoption, driven by AI voiceovers, transcription, and podcast automation. However, video-language models are the fastest-growing type, with adoption expanding at an estimated CAGR of 24%, supported by rising demand for AI-generated video ads, automated editing, and short-form social media content. Text-only AI models and niche creative AI tools collectively account for the remaining 33% share, serving specialized use cases such as copywriting, script ideation, and localization. Growth in advanced multimodal systems is increasingly blurring type boundaries, enabling unified creative pipelines across formats.

In 2025, a large global streaming platform deployed video-language AI systems to automatically generate captions, trailers, and scene summaries, improving accessibility features for over 10 million active users.

By application, media and entertainment remains the leading segment, contributing approximately 34% of total adoption, driven by high-volume content production, localization needs, and audience personalization. Advertising and digital marketing follows closely, supported by AI-driven campaign optimization, creative testing, and dynamic asset generation. The fastest-growing application is e-commerce and digital retail content automation, expanding at an estimated CAGR of 22%, fueled by the need for personalized product descriptions, AI-generated visuals, and multilingual storefront content. Other applications—including corporate communications, education content, and gaming—collectively account for around 31% of adoption, benefiting from AI-assisted storytelling and immersive experiences.

Consumer adoption trends indicate that over 38% of enterprises globally were piloting AI content systems for customer experience platforms in 2025, while more than 60% of Gen Z consumers show higher engagement with brands using AI-powered interactive content.

In 2025, AI-driven content automation tools were deployed across hundreds of global retail platforms, enabling real-time generation of localized product visuals and descriptions, improving engagement metrics by over 25%.

From an end-user perspective, media & entertainment companies lead the market with approximately 36% adoption, leveraging AI to manage large-scale content libraries, accelerate production cycles, and enhance audience personalization. Marketing agencies and brand owners follow with about 28% share, as AI tools enable rapid creative iteration and data-driven campaign optimization. The fastest-growing end-user group is small and mid-sized enterprises (SMEs), expanding at an estimated CAGR of 21%, driven by affordable cloud-based AI creative platforms that lower entry barriers. Other end-users—including independent creators, gaming studios, and educational institutions—collectively represent around 36% of adoption, with usage rates exceeding 45% in digital-first creator businesses. In 2025, over 40% of enterprises reported active deployment of AI content tools across internal and external communications.

In 2025, a large cohort of retail and media-focused SMEs adopted AI creative platforms, enabling hundreds of organizations to reduce content production timelines by over 30% while maintaining brand consistency.

North America accounted for the largest market share at 41.8% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.6% between 2026 and 2033.

Regional performance in the AI Content Production and Creative Technology Market is shaped by digital maturity, enterprise AI readiness, regulatory frameworks, and content consumption behavior. North America leads due to early adoption across media, marketing, and enterprise software, with over 68% of large organizations actively deploying AI-driven creative tools. Europe follows with 26.4% share, driven by strong demand for explainable and compliant AI systems across regulated industries. Asia-Pacific holds 22.9% share in 2025, supported by rapid digitalization, mobile-first content consumption, and a growing creator economy exceeding 300 million digital creators. South America and the Middle East & Africa together account for 8.9%, with growth tied to language localization, government-backed digital transformation, and expanding media platforms.

North America holds approximately 41.8% of the global AI Content Production and Creative Technology Market, reflecting its advanced digital infrastructure and early AI commercialization. Key industries driving demand include media & entertainment, advertising, e-commerce, healthcare communications, and financial services. Regulatory clarity around AI governance and copyright frameworks has accelerated enterprise confidence, while federal and state-level innovation grants support AI R&D. Technologically, over 70% of enterprises integrate AI content tools within cloud-based CRM and marketing platforms. A notable regional player, Adobe, continues expanding generative AI capabilities across design and video workflows, supporting millions of professional users. Consumer behavior shows higher enterprise-led adoption, with healthcare and finance organizations accounting for over 45% of AI-driven content use cases, emphasizing compliance-ready and secure creative AI solutions.

Europe represents around 26.4% of global market share, with Germany, the UK, and France leading adoption. Strong regulatory oversight from pan-European bodies has driven demand for explainable, transparent, and auditable AI content systems. Sustainability and ethical AI initiatives influence procurement decisions, with over 52% of enterprises prioritizing governance features in creative AI platforms. Emerging technologies such as multilingual AI models and rights-managed generative systems are widely adopted to address diverse linguistic markets. A prominent European AI software provider is focusing on compliant generative design tools for publishing and marketing. Regional consumer behavior reflects regulatory sensitivity, with enterprises favoring AI solutions that offer traceability, watermarking, and bias mitigation capabilities.

Asia-Pacific ranks third by market volume with 22.9% share, led by China, India, and Japan. The region benefits from rapid digital infrastructure expansion, high smartphone penetration exceeding 78%, and a booming creator economy. Manufacturing of AI hardware, regional cloud investments, and government-backed AI innovation hubs support large-scale deployment. Local players in China and India are developing multilingual AI content platforms tailored for regional languages, supporting over 20 major dialect groups. Consumer behavior is heavily mobile-driven, with e-commerce platforms and social media apps accounting for over 55% of AI-generated content usage, particularly in short-form video and interactive media.

South America accounts for approximately 5.2% of global market share, with Brazil and Argentina as key contributors. Demand is driven by media localization, advertising, and digital marketing for multilingual audiences. Infrastructure upgrades in cloud computing and broadband connectivity are improving AI deployment capabilities. Governments are offering digital economy incentives and cross-border trade policies supporting AI software adoption. Regional media technology firms are deploying AI tools for automated translation and voice synthesis in Spanish and Portuguese. Consumer behavior highlights strong demand for localized entertainment and marketing content, with over 48% of digital campaigns incorporating AI-generated localized assets.

The Middle East & Africa region contributes about 3.7% of global adoption, led by the UAE and South Africa. Demand is linked to smart city initiatives, government communications, tourism promotion, and media modernization. National AI strategies and regional trade partnerships support technology transfer and enterprise AI adoption. Local players are integrating AI content tools into public-sector digital platforms and large-scale event marketing. Consumer behavior varies widely, with higher adoption in government-led projects and media localization for multicultural audiences, particularly in Arabic, English, and French-language content.

United States – 38.5% Market Share: Dominance driven by advanced AI infrastructure, high enterprise adoption, and concentration of leading creative AI platform developers.

China – 14.2% Market Share: Strong position supported by large-scale digital content consumption, multilingual AI development, and extensive government-backed AI innovation programs.

The AI Content Production and Creative Technology Market is moderately consolidated with a competitive landscape comprising dozens of active competitors, including global technology giants and specialized creative AI innovators. The top 5 companies collectively command an estimated 57–63% of overall market influence, underscoring leadership concentration while notable fragmentation persists among emerging startups driving niche innovations. Market positioning reflects diverse strategic initiatives, including strategic partnerships, product launches, model integrations, and creative ecosystem expansions, which intensify competition and differentiation. For example, Adobe has unveiled expanded AI audio, video, and photo-generation tools across its Express, Firefly, and Creative Cloud suite to strengthen enterprise and professional creator adoption. Meanwhile, generative AI platforms like Google’s enhanced Veo tool emphasize mobile-optimized realistic video generation, targeting high-definition and professional-tier content creation. Collaboration dynamics are also active — companies such as Runway are partnering with major entertainment channels to demonstrate AI-powered previsualization and marketing capabilities across film and broadcast pipelines.

Innovation trends shaping the competitive environment include multimodal AI integration, workflow automation APIs, plug-and-play creative models, and brand-customized AI engines tailored for enterprise-specific content needs. The nature of competition blends traditional software vendor rivalries with rapid launch cycles from agile startups harnessing advanced foundation models, enabling creative automation, natural user interfaces, and scalable enterprise-ready APIs. As the market evolves, strategic alliances, ecosystem-building, and AI model differentiation remain central to sustained competitive advantage.

Microsoft

Meta

Runway

Stability AI

Anthropic

Nvidia

Kuaishou (Kling AI)

MarketFully

Utopai Studios

Uniphore

Cognition

Luma AI

The AI Content Production and Creative Technology Market is being shaped by a convergence of foundational and applied technologies that are redefining how digital creative assets are generated, managed, and integrated into business workflows. Central to this evolution are multimodal generative models — AI systems capable of synthesizing text, images, audio, and video from unified prompts — which are enabling enterprises to automate complex creative tasks that previously required discrete tools and manual orchestration. These technologies are driving quantum improvements in throughput, with advanced models now able to produce broadcast-quality visuals and realistic soundtracks without human pre-editing.

A key technological trend is the embedding of real-time personalization engines, which adapt content for diverse audience segments — from personalized video ads to tailored audio narratives — increasing engagement metrics and reducing production cycles. Generative vision-language and video-language models are increasingly integrated into content management systems (CMS), digital asset pipelines, and marketing automation stacks, enabling seamless transitions from ideation to execution. Beyond asset creation, AI-augmented collaboration tools are enhancing creative team workflows by providing context-aware suggestions, version control automation, and dynamic narrative expansion capabilities for scriptwriting and concept generation.

Infrastructure innovations, such as edge-optimized inference engines and cloud GPU elasticity, support scalable deployment across enterprise environments, ensuring that compute resources align with demand spikes during campaign launches or media events. Security and governance layers — including watermarking, usage tracking, and explainability modules — are being incorporated to address compliance concerns and intellectual property constraints. Together, these technologies are transforming not only the output of creative work but also the operational architecture of creative teams, elevating AI from a utility to a strategic enabler of content differentiation and brand amplification.

• In October 2025, Adobe launched a new suite of AI audio, video, and photo tools across Adobe Express, Firefly, and Creative Cloud, including the Firefly Image Model 5 and integration of Google’s Nano Banana model to enhance studio-quality content generation for individual creators and enterprises. Source: www.timesofindia.indiatimes.com

• In December 2025, Meta signed a multi-year AI partnership with several international media outlets, including Le Monde and Télérama, formalizing regulated use of media content in Meta’s AI tools to ensure contextualized output and protect editorial integrity under evolving legal frameworks. Source: www.lemonde.fr

• In late 2025, Adobe and Qualcomm partnered with Saudi Arabia-backed Humain to develop Arabic-language generative AI tools aimed at creative use cases in marketing, film, and television, supported by plans to deploy up to 200 megawatts of AI chip-powered data center infrastructure. Source: www.reuters.com

• In June 2025, Google released Veo 3.1, an upgraded version of its generative AI video creation tool with mobile-optimized formats and high-definition features that improve motion generation and scene consistency for professional video production workflows. Source: www.timesofindia.indiatimes.com

The scope of the AI Content Production and Creative Technology Market Report encompasses a broad range of facets critical to understanding, evaluating, and making strategic decisions within this rapidly evolving domain. The report covers market segmentation by type, application, and end-user, providing detailed insights into the adoption patterns of different AI models — including text-based, vision-language, audio-text, and multimodal generative systems — and highlighting how each contributes to varied content workflows such as media production, digital marketing, enterprise communications, and immersive experiences. Regional analysis spans major geographies, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering contextual perspectives on infrastructure readiness, consumer behavior variations, and regulatory or innovation ecosystems that affect AI content adoption.

In addition to technology penetration, the report examines emerging technology trends — such as real-time personalization engines, integrated creative automation platforms, and AI-powered collaboration tools — and how these influence operational efficiency and creative scale. End-user insights detail adoption rates across sectors like media & entertainment, advertising, e-commerce, and corporate communications, while profiling competitive dynamics with comprehensive company profiles and strategic initiatives that shape market leadership.

Key industry focus areas include the integration of governance and compliance technologies, enabling enterprises to align AI content generation with intellectual property and ethical standards, and the rise of niche segments such as regional language creative AI, 3D content generation, and explainable AI for strategic content co-creation. By synthesizing segmentation, technology, regional insights, and competitive landscapes, the report equips decision-makers with a holistic understanding of market opportunities, barriers, and future trajectories in the AI-driven creative economy.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,496.0 Million |

| Market Revenue (2033) | USD 5,361.9 Million |

| CAGR (2026–2033) | 17.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Adobe, OpenAI, Google (Veo & Gemini tools), Microsoft, Meta, Runway, Stability AI, Anthropic, Nvidia, Kuaishou (Kling AI), MarketFully, Utopai Studios, Uniphore, Cognition, Luma AI |

| Customization & Pricing | Available on Request (10% Customization Free) |