Reports

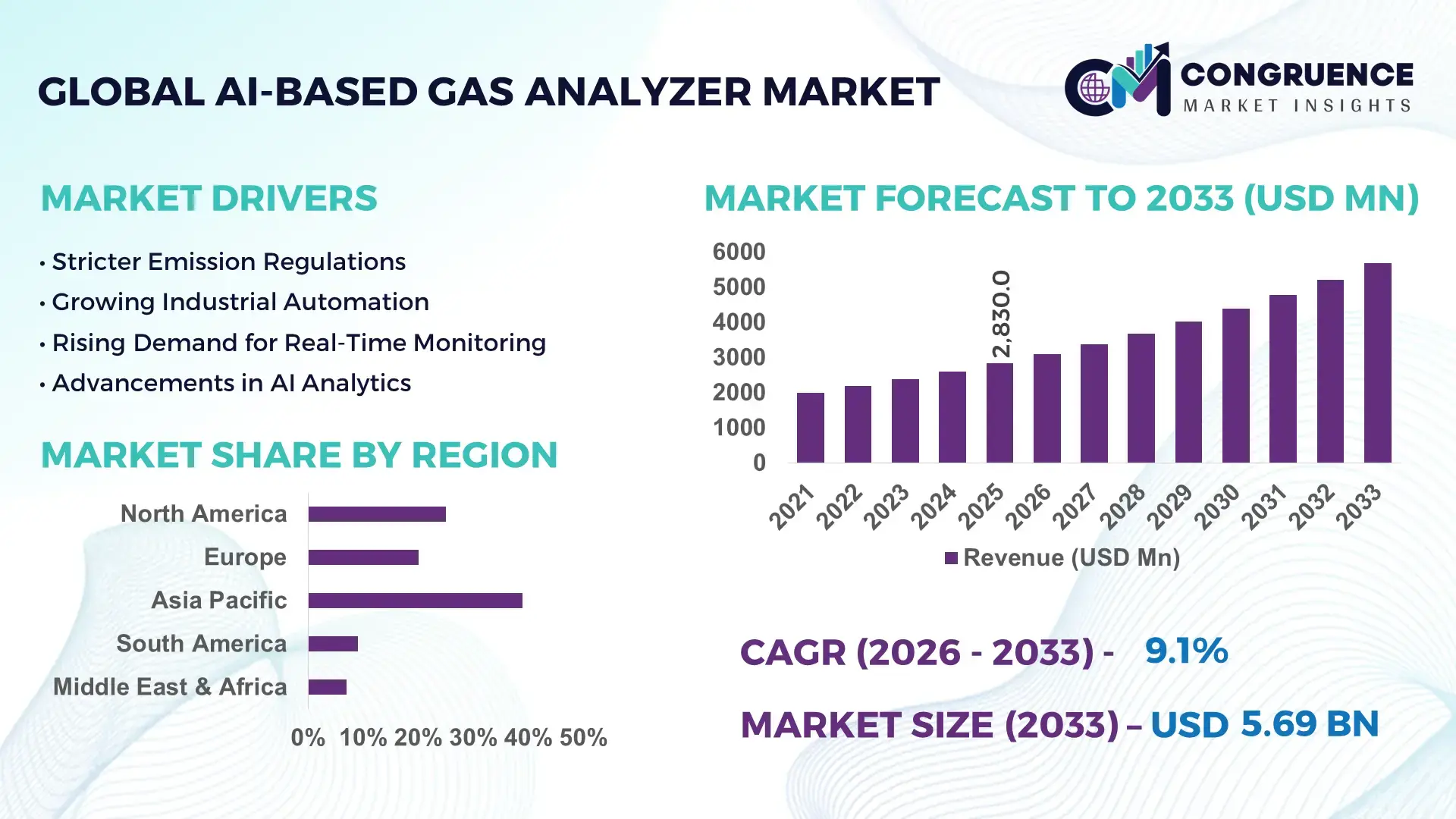

The Global AI-Based Gas Analyzer Market was valued at USD 2830 Million in 2025 and is anticipated to reach a value of USD 5688.8 Million by 2033 expanding at a CAGR of 9.12% between 2026 and 2033. Growth is accelerating through AI-enabled predictive emission monitoring, hydrogen infrastructure expansion, and stricter industrial air-quality compliance across energy, chemicals, semiconductor, and LNG processing facilities.

China leads the global AI-based gas analyzer market with nearly 34% manufacturing share supported by more than USD 12 billion in smart industrial monitoring investments linked to carbon-neutrality targets and industrial safety modernization programs. In 2026, advanced optical gas analyzers integrated with edge AI systems achieved over 28% faster leak detection accuracy compared to conventional infrared monitoring platforms across petrochemical and steel facilities. The United States maintains strong deployment across shale gas, semiconductor fabrication, and defense sectors, while European industries accelerated adoption following tighter methane monitoring mandates introduced after the energy supply disruptions triggered by the Russia-Ukraine conflict. Industrial operators deploying cloud-connected analyzers reported up to 22% lower unplanned downtime through predictive maintenance integration.

Strategic expansion into AI-integrated compliance monitoring and multi-gas automation platforms is becoming essential for manufacturers targeting long-term industrial contracts and regulatory-driven procurement cycles.

Market Size & Growth: Industry value expands from USD 2830 Million in 2025 to USD 5688.8 Million by 2033, driven by AI-powered industrial emission tracking and smart refinery automation.

Top Growth Drivers: Industrial safety upgrades contribute 31%, hydrogen infrastructure deployment 26%, and stricter emission compliance adoption 24% of market acceleration.

Short-Term Forecast: By 2027, AI-enabled analyzers reduce manual inspection costs by 21% while improving gas leak detection efficiency by 29%.

Emerging Technologies: Edge AI, laser-based spectroscopy, and cloud-connected predictive analytics improve monitoring precision by over 32% in high-risk facilities.

Regional Leaders: Asia-Pacific exceeds USD 2200 Million through manufacturing digitization, North America crosses USD 1500 Million with LNG expansion, and Europe surpasses USD 1100 Million through methane-control initiatives.

Consumer/End-User Trends: More than 58% of chemical and energy operators prioritize real-time multi-gas analytics integration within automated plant systems.

Pilot/Case Example: In 2026, a smart refinery deployment improved hazardous gas response time by 37% through AI-assisted anomaly detection systems.

Competitive Landscape: Leading manufacturers control approximately 41% combined share, with competition centered on AI integration, remote diagnostics, and industrial automation partnerships.

Regulatory & ESG Impact: Emission-control mandates lowered industrial methane leakage by nearly 18% across regulated European and North American facilities.

Investment & Funding: Global investments exceeded USD 4.3 billion in 2026, supported by automation partnerships, semiconductor expansion, and energy-transition infrastructure projects.

Innovation & Future Outlook: Next-generation portable analyzers with edge computing and autonomous calibration capabilities are reshaping high-growth industrial monitoring strategies.

The market is strongly supported by oil and gas, chemicals, semiconductor manufacturing, and power generation sectors, which collectively account for over 68% of advanced gas analyzer deployments. AI-enabled spectroscopy systems, autonomous calibration modules, and cloud-based predictive diagnostics are improving operational accuracy and reducing maintenance cycles across large industrial facilities. Asia-Pacific continues leading installation volumes, while North America strengthens demand through LNG expansion and hydrogen infrastructure modernization. Increasing regulatory scrutiny on industrial emissions and ongoing semiconductor supply chain localization are accelerating adoption of compact, real-time monitoring systems. This transition toward intelligent, connected analyzers is positioning the market for broader integration into next-generation industrial automation strategies.

The AI-based gas analyzer market is becoming strategically critical as industrial operators prioritize automated emission intelligence, predictive maintenance, and real-time compliance management across energy, semiconductor, chemicals, and hydrogen-processing facilities. Tightened methane-monitoring regulations in the United States and Europe, combined with industrial supply-chain restructuring after recent energy security disruptions, accelerated deployment of connected sensing infrastructure by more than 27% during 2025–2026. Companies are integrating AI-driven analyzers into centralized industrial control platforms to reduce manual inspection dependency and strengthen operational continuity in high-risk processing environments.

AI-enabled laser spectroscopy systems now deliver nearly 31% faster anomaly detection and 24% lower calibration downtime compared to legacy infrared analyzers used across older industrial plants. China continues leading large-scale manufacturing deployment through smart factory modernization, while Germany and Japan prioritize ultra-precision analyzers for semiconductor and specialty chemical production. In the next two to three years, over 45% of newly commissioned LNG and hydrogen facilities are expected to integrate cloud-connected gas monitoring systems as standard operational infrastructure.

In 2026, several refinery operators deployed edge AI analyzers integrated with predictive maintenance software, reducing hazardous leak response times by 34% and lowering maintenance intervention frequency. Industrial technology firms are expanding partnerships with automation providers and semiconductor sensor manufacturers to strengthen analytics capabilities and shorten deployment cycles. Companies securing scalable AI-integrated monitoring ecosystems are expected to gain stronger regulatory positioning, lower operational risk exposure, and higher-value industrial service contracts.

Industrial facilities are accelerating adoption of AI-based gas analyzers as automated compliance monitoring and predictive safety systems become operational priorities across refining, chemicals, and semiconductor manufacturing. More than 52% of large industrial plants upgraded continuous gas monitoring infrastructure during 2025–2026 to reduce manual inspection dependency and improve process visibility. In China, smart manufacturing investments increased deployment of AI-integrated analyzers by nearly 33% within heavy industrial clusters, while U.S. LNG facilities improved leak detection precision by 29% through edge analytics integration. Tightened methane-emission rules and workforce shortages are directly increasing demand for autonomous monitoring systems. In response, manufacturers are expanding sensor production capacity, forming industrial automation partnerships, and integrating machine-learning diagnostics into multi-gas platforms to strengthen long-term service contracts and operational differentiation.

Advanced AI-based gas analyzers remain exposed to semiconductor supply dependency, high integration costs, and interoperability limitations across aging industrial infrastructure. Precision optical sensors and AI processing modules account for nearly 38% of total deployment expenditure, creating procurement pressure for mid-sized operators. During 2025–2026, lead times for specialized sensing chips in Japan and Taiwan extended by approximately 18%, affecting delivery schedules for industrial monitoring systems. Many legacy refineries and chemical plants still operate incompatible control architectures, increasing system retrofitting costs by nearly 22%. These constraints are slowing deployment scalability across cost-sensitive facilities. To reduce operational exposure, companies are localizing component sourcing, securing long-term semiconductor supply agreements, and developing modular analyzer platforms compatible with existing industrial automation networks.

Expansion of hydrogen production, carbon capture infrastructure, and autonomous industrial operations is creating high-value opportunities for AI-based gas analyzer providers. More than 41% of newly planned hydrogen-processing projects in South Korea and the United States now specify continuous AI-assisted gas monitoring systems within operational safety frameworks. AI-driven predictive analytics platforms are reducing false alarm frequency by nearly 26% while improving maintenance scheduling efficiency across large industrial facilities. Portable wireless analyzers integrated with cloud-based diagnostics are gaining traction in remote mining, LNG transportation, and offshore processing environments. Companies are increasing R&D investment into miniaturized spectroscopy systems and digital twin integration to support real-time operational modeling. A key strategic opportunity is emerging in subscription-based monitoring services, where analytics-driven compliance management is generating recurring industrial service revenue beyond hardware sales.

The market faces growing execution challenges linked to cybersecurity exposure, industrial data integration complexity, and workforce capability gaps surrounding AI-enabled operational systems. Nearly 36% of industrial operators reported delays integrating gas analyzers with existing SCADA and cloud infrastructure during 2025 due to incompatible data protocols and fragmented industrial software environments. In Germany and the United States, rising cyber-risk concerns around connected industrial monitoring systems increased compliance-related deployment costs by approximately 19%. Large-scale facilities also face shortages of AI-capable instrumentation engineers, limiting deployment consistency across multi-site operations. Companies must strengthen encrypted industrial communication systems, invest in workforce training, and expand partnerships with cybersecurity and automation providers. Long-term competitiveness will depend on building scalable, secure, and interoperable monitoring ecosystems capable of supporting continuously connected industrial operations.

Edge AI Monitoring Expansion Industrial operators are rapidly deploying edge AI-enabled gas analyzers to reduce response latency and minimize cloud dependency in hazardous environments. During 2025–2026, deployment of localized analytics systems increased by 36% across LNG terminals and semiconductor facilities in the United States and South Korea. Companies reported nearly 27% faster incident identification and 19% lower network-processing costs compared to centralized monitoring architectures. In response to cybersecurity concerns and rising industrial data loads, manufacturers are integrating onboard diagnostics, encrypted communication modules, and autonomous calibration features into next-generation analyzer platforms.

Portable Detection Systems Scaling Workforce mobility constraints and remote infrastructure expansion are accelerating adoption of portable multi-gas analyzers across mining, offshore drilling, and industrial maintenance operations. Portable analyzer utilization increased by approximately 31% in Australia and Canada during 2026 as operators prioritized rapid deployment flexibility and lower maintenance downtime. Advanced battery systems improved uninterrupted operating duration by 22%, allowing continuous field inspections across large industrial zones. Companies are expanding rental-based deployment models and forming service partnerships to address temporary project demand without increasing permanent capital expenditure.

Hydrogen Facility Compliance Integration Hydrogen-processing infrastructure projects are reshaping analyzer configuration standards as facilities require continuous leak detection and precision gas composition monitoring. More than 44% of newly commissioned hydrogen plants in Germany and Japan integrated AI-assisted analyzers with automated shutdown systems during 2026. Optical sensing technologies improved low-concentration hydrogen detection accuracy by nearly 26% compared to conventional electrochemical systems. Equipment manufacturers are restructuring product portfolios toward hydrogen-compatible analyzers and increasing partnerships with industrial automation firms to support large-scale energy transition projects.

Predictive Maintenance Workflow Adoption Industrial enterprises are increasingly linking gas analyzers with predictive maintenance software to reduce unexpected shutdowns and optimize maintenance scheduling. In 2026, predictive analytics integration expanded by 34% across petrochemical and chemical processing plants in China, lowering emergency maintenance interventions by approximately 24%. A non-obvious operational shift is emerging as companies use analyzer-generated process data to optimize energy consumption and compressor efficiency beyond safety monitoring functions. Vendors are strengthening AI software capabilities and cloud interoperability to position analyzers as integrated industrial intelligence platforms rather than standalone sensing devices.

Fixed Gas Analyzers remain the dominant segment due to continuous monitoring capability, integration compatibility with industrial automation systems, and strong deployment across refineries, LNG facilities, and chemical plants. Nearly 48% of large-scale industrial monitoring installations in 2026 relied on fixed analyzers because of centralized operational control and lower long-term maintenance frequency. Multi-Gas Analyzers are emerging as the fastest-growing category, supported by increasing demand for integrated detection across hydrogen, methane, carbon monoxide, and volatile organic compounds within a single platform. Adoption increased by approximately 32% across advanced manufacturing and offshore processing facilities where operational flexibility is critical. Portable Gas Analyzers continue gaining relevance for field inspection and remote asset monitoring, while Infrared Gas Analyzers maintain strong penetration in high-precision emission analysis due to superior stability and detection sensitivity. Electrochemical Gas Analyzers remain cost-efficient for smaller industrial environments and workplace safety compliance. Companies are prioritizing AI-integrated fixed and multi-gas systems through automation partnerships, modular product launches, and expansion of remote diagnostics capabilities.

Emission Monitoring continues leading application demand as industrial operators strengthen compliance infrastructure for methane, carbon dioxide, and hazardous gas tracking across refining, power generation, and heavy manufacturing facilities. More than 46% of industrial analyzer deployments during 2026 were linked directly to continuous emission management requirements and automated reporting systems. Leak Detection is the fastest-growing application as LNG terminals, hydrogen facilities, and semiconductor plants prioritize real-time anomaly identification and operational risk reduction. AI-enabled leak detection systems improved hazardous gas response efficiency by nearly 29% compared to conventional manual inspection workflows. Industrial Safety remains operationally critical in mining, offshore drilling, and confined manufacturing environments, while Process Control applications are expanding through integration with digital twin and predictive maintenance platforms. Air Quality Monitoring and Environmental Monitoring are gaining traction in urban industrial corridors where stricter environmental oversight is increasing continuous sensing requirements. Companies are scaling cloud-connected monitoring infrastructure and deploying automated analytics systems to improve compliance accuracy and reduce operational interruptions.

Oil and Gas remains the dominant end-user segment due to high infrastructure dependency on continuous leak detection, emission control, and hazardous environment monitoring across upstream, midstream, and downstream operations. Nearly 43% of AI-based gas analyzer deployments in 2026 were concentrated within refinery, LNG, and offshore production assets where uninterrupted monitoring is operationally mandatory. Energy and Utilities represents the fastest-growing end-user category as hydrogen projects, carbon capture facilities, and grid modernization programs accelerate deployment of AI-integrated sensing systems. Adoption within utility-scale energy infrastructure increased by approximately 34% during 2025–2026. The Chemical Industry continues investing heavily in predictive process monitoring and automated safety systems, while Manufacturing facilities are integrating analyzers with industrial automation platforms to improve workplace compliance and energy optimization. Healthcare and Environmental Agencies are expanding portable analyzer deployment for laboratory diagnostics and urban air-quality surveillance. Companies are responding through customized analyzer configurations, long-term service contracts, and AI-enabled remote monitoring ecosystems tailored to sector-specific operational requirements.

Asia-Pacific accounted for the largest market share at 39% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Industrial Automation and LNG Monitoring Expansion

North America maintains strong deployment leadership through advanced refinery infrastructure, LNG terminal expansion, semiconductor manufacturing growth, and strict industrial emission compliance frameworks. The region accounted for nearly 28% of global deployment concentration in 2025, supported by high integration rates of AI-enabled continuous monitoring systems across oil, gas, and chemical processing operations. In the United States, industrial operators accelerated predictive maintenance integration, improving hazardous leak response efficiency by approximately 30% across large processing facilities. Hydrogen infrastructure projects and methane-monitoring regulations are further increasing demand for cloud-connected analyzers and edge diagnostics. Companies are strengthening regional manufacturing partnerships and expanding industrial automation integration capabilities to support large-scale modernization programs and faster operational deployment cycles.

United States Market Outlook: The United States remains the region’s most strategically significant market due to extensive LNG infrastructure, advanced industrial automation ecosystems, and strong environmental compliance enforcement. More than 47% of newly upgraded refinery and gas-processing facilities integrated AI-enabled multi-gas analyzers during 2026 to improve predictive maintenance and automated reporting capabilities. Domestic technology providers are prioritizing semiconductor-based sensing innovation, while energy operators continue expanding connected monitoring infrastructure across shale production and hydrogen-processing projects.

Methane Compliance and Sustainability Modernization

Europe is strengthening its position through aggressive industrial decarbonization policies, methane-emission monitoring mandates, and modernization of energy-intensive manufacturing infrastructure. Nearly 24% of global high-precision gas analyzer deployments in 2025 were concentrated within Germany, France, and the Nordic industrial corridor, where advanced spectroscopy systems are widely integrated into chemical and energy operations. Industrial facilities adopting AI-assisted emission monitoring reported approximately 26% lower manual compliance management workloads during 2026. Tightened environmental oversight following energy supply restructuring accelerated replacement of conventional monitoring equipment with automated multi-gas systems. Companies are expanding partnerships with industrial software providers and automation firms to strengthen predictive diagnostics, reporting accuracy, and remote asset management across large industrial networks.

Germany Market Outlook: Germany leads the European market through its advanced chemical manufacturing base, hydrogen infrastructure investments, and strong industrial automation ecosystem. More than 42% of newly commissioned hydrogen-processing facilities in Germany integrated AI-assisted gas analysis systems during 2026 to support continuous leak detection and precision process monitoring. Industrial equipment manufacturers are increasingly focusing on energy-efficient sensing platforms and digital factory integration to improve operational transparency and support long-term industrial sustainability targets.

Manufacturing Scale and Smart Factory Acceleration

Asia-Pacific dominates the global market through large-scale industrial manufacturing, refinery expansion, semiconductor production growth, and rapid smart factory deployment across China, Japan, South Korea, and India. The region contributed approximately 39% of global analyzer deployment activity in 2025, supported by aggressive industrial automation investment and expanding environmental compliance infrastructure. China and South Korea accelerated adoption of AI-integrated fixed monitoring systems by nearly 35% across semiconductor and petrochemical facilities during 2026. Rising demand for hydrogen processing, LNG transportation, and urban industrial air-quality management is strengthening deployment volumes. Companies are increasing regional manufacturing capacity, localizing sensor supply chains, and expanding automation partnerships to improve scalability and reduce deployment lead times across high-volume industrial markets.

China Market Outlook: China remains the largest country-level market due to its dominant industrial manufacturing footprint, rapid refinery modernization, and extensive semiconductor production infrastructure. During 2026, more than 51% of newly upgraded heavy industrial facilities adopted continuous AI-based emission monitoring systems linked with centralized automation platforms. Domestic manufacturers are scaling optical sensing production and edge AI integration capabilities to reduce import dependency and strengthen competitiveness within industrial compliance and smart manufacturing applications.

Energy Infrastructure and Mining Demand Growth

South America is experiencing steady market expansion driven by offshore oil production, mining operations, and modernization of industrial safety infrastructure across Brazil, Chile, and Argentina. The region represented nearly 6% of global deployment activity in 2025, with demand concentrated in hydrocarbon processing and metal extraction facilities requiring continuous hazardous gas monitoring. Brazilian offshore energy operators increased deployment of remote multi-gas analyzers by approximately 22% during 2026 to improve operational safety and reduce manual inspection frequency. Infrastructure limitations and uneven industrial digitization continue affecting large-scale deployment consistency across secondary markets. In response, companies are prioritizing modular analyzer systems, localized service networks, and flexible deployment partnerships to improve installation efficiency and long-term operational reliability.

Brazil Market Outlook: Brazil leads the regional market through its offshore oil infrastructure, biofuel processing capacity, and expanding industrial modernization initiatives. More than 38% of newly commissioned offshore processing assets in 2026 integrated AI-assisted gas monitoring systems for predictive maintenance and automated safety management. Industrial operators are increasingly investing in cloud-connected analyzers and portable detection systems to strengthen compliance efficiency across remote offshore and mining environments.

Hydrogen Investments and Refinery Modernization

Middle East & Africa is emerging as the fastest-transforming market due to refinery expansion, hydrogen infrastructure investment, and modernization of large hydrocarbon processing facilities across Saudi Arabia, the UAE, and Qatar. The region accounted for approximately 9% of global deployment activity in 2025, with strong concentration in petrochemical and LNG infrastructure projects. During 2026, deployment of AI-enabled continuous gas monitoring systems increased by nearly 33% across newly upgraded Gulf refinery assets to improve automated compliance management and operational safety performance. National industrial diversification programs and carbon-management initiatives are accelerating demand for advanced monitoring platforms. Companies are strengthening regional engineering partnerships and expanding localized technical support capabilities to secure long-term infrastructure contracts and improve deployment responsiveness.

Saudi Arabia Market Outlook: Saudi Arabia remains the region’s most influential market due to large-scale refinery modernization programs, hydrogen investment activity, and expanding petrochemical infrastructure. In 2026, nearly 46% of newly upgraded energy-processing facilities integrated AI-assisted gas analyzers connected with centralized industrial automation systems. Energy operators are prioritizing predictive monitoring technologies and high-precision spectroscopy platforms to improve operational continuity, emission management, and long-term industrial efficiency across large hydrocarbon assets.

Global leaders such as Honeywell, ABB, Siemens, Emerson, and Yokogawa compete directly against regional instrumentation manufacturers and low-cost Asian sensor suppliers, while AI-focused analytics firms challenge traditional OEMs through software-driven monitoring platforms. The top five players collectively control nearly 49% of the market, supported by integrated automation portfolios, industrial service networks, and long-term refinery relationships. Competition is centered on detection precision, AI integration, deployment speed, and lifecycle operating efficiency. Advanced AI-enabled analyzers improved predictive maintenance efficiency by approximately 28%, while modular cloud-connected systems reduced industrial calibration downtime by nearly 21% compared to conventional fixed analyzers. Companies are expanding through automation partnerships, localized manufacturing, hydrogen-monitoring product launches, and vertical integration into industrial analytics ecosystems. Technology transition toward edge AI and connected infrastructure is accelerating consolidation pressure. Winning requires scalable sensing accuracy, cybersecurity-ready platforms, semiconductor supply resilience, and deep industrial integration capabilities.

Honeywell International Inc.

ABB Ltd.

Siemens AG

Emerson Electric Co.

Yokogawa Electric Corporation

Endress+Hauser Group

HORIBA Ltd.

Teledyne Technologies Incorporated

AMETEK Inc.

Servomex Group Limited

Fuji Electric Co., Ltd.

Mettler-Toledo International Inc.

Drägerwerk AG & Co. KGaA

SICK AG

AI-integrated spectroscopy and edge analytics are becoming core technologies across industrial gas monitoring systems. Fixed analyzers using non-dispersive infrared and tunable diode laser absorption spectroscopy improved leak detection precision by nearly 28% during 2026 across LNG and petrochemical facilities. More than 54% of newly deployed industrial analyzers now integrate cloud-connected diagnostics and predictive maintenance functions. Companies adopting AI-enabled continuous monitoring platforms reduced calibration downtime by approximately 21%, strengthening operational uptime and regulatory reporting accuracy. Industrial automation providers are increasingly integrating analyzers into SCADA and digital twin environments to improve centralized process visibility.

Emerging technologies are shifting toward portable multi-gas systems with embedded AI chips, autonomous calibration modules, and wireless industrial connectivity. Compared to legacy electrochemical analyzers, advanced optical systems deliver nearly 32% longer operational stability and 24% lower maintenance intervention frequency. Semiconductor manufacturers and hydrogen-processing operators are accelerating deployment of compact analyzers capable of real-time contamination detection across high-precision production environments. Companies with strong sensor miniaturization and AI software capabilities are gaining competitive advantage in high-value industrial contracts.

Between 2026 and 2028, disruptive innovation will center on edge AI inference, digital twin integration, and hydrogen-compatible sensing architectures. Autonomous analyzers capable of self-diagnostics and remote optimization are expected to exceed 46% deployment penetration across newly commissioned industrial facilities. Manufacturers acting now through AI partnerships, localized semiconductor sourcing, and software-driven monitoring ecosystems are strengthening long-term operational positioning and industrial automation relevance.

March 2026 – Honeywell launched the AI-powered Experion Operations Assistant, enabling industrial operators to predict alarm incidents 5–10 minutes earlier, improving plant response efficiency and reducing unplanned operational disruptions across energy-processing facilities. Source: Honeywell

December 2025 – ABB introduced the Sensi+ NG four-gas analyzer for biogas and natural gas applications, integrating oxygen measurement into a single platform and reducing multi-device monitoring complexity across industrial processing environments. Source: gasworld

February 2026 – ABB launched its integrated carbon-capture gas measurement solution combining three analyzer technologies into one industrial package, strengthening CO₂ stream quality assurance and accelerating deployment efficiency within hard-to-abate industrial sectors. Source: Gas Processing & LNG

February 2026 – Honeywell and TCS formed a strategic industrial AI partnership to integrate operational technology and cloud intelligence, improving autonomous industrial decision-making and accelerating enterprise-wide predictive monitoring deployment capabilities.

The report provides detailed strategic analysis of the AI-based gas analyzer market across major types including portable, fixed, multi-gas, infrared, and electrochemical analyzers, covering operational deployment patterns, industrial adoption trends, and technology integration shifts between 2026 and 2033. The study evaluates core applications such as emission monitoring, industrial safety, process control, leak detection, air quality monitoring, and environmental monitoring across oil and gas, chemicals, manufacturing, healthcare, utilities, and regulatory agencies. More than 60% of current enterprise deployments are concentrated in continuous industrial monitoring and automated compliance infrastructure.

The report further analyzes regional industrial dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, hydrogen expansion, semiconductor manufacturing growth, and predictive maintenance integration trends. It includes competitive benchmarking, technology transition analysis, deployment scalability assessment, and operational positioning insights to support investment planning, industrial expansion strategies, supply-chain alignment, and long-term competitive decision-making across advanced industrial monitoring ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2830 Million |

|

Market Revenue in 2033 |

USD 5688.8 Million |

|

CAGR (2026 - 2033) |

9.12% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell International Inc., ABB Ltd., Siemens AG, Emerson Electric Co., Yokogawa Electric Corporation, Endress+Hauser Group, HORIBA Ltd., Teledyne Technologies Incorporated, AMETEK Inc., Servomex Group Limited, Fuji Electric Co., Ltd., Mettler-Toledo International Inc., Drägerwerk AG & Co. KGaA, SICK AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |