Reports

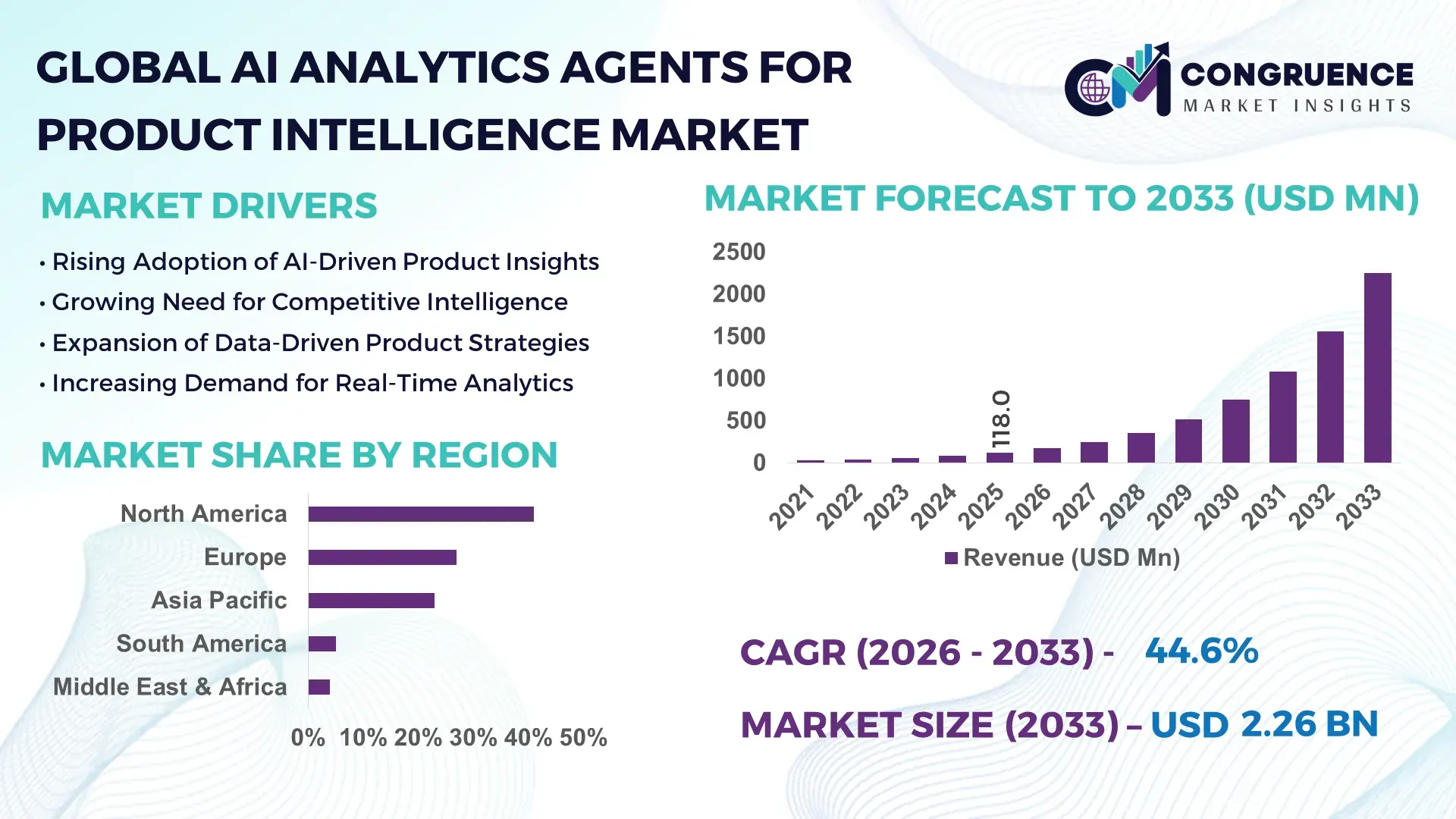

The Global AI Analytics Agents for Product Intelligence Market was valued at USD 118.0 Million in 2025 and is anticipated to reach a value of USD 2,255.4 Million by 2033 expanding at a CAGR of 44.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by the rapid adoption of autonomous AI agents that can continuously analyze product performance data, competitor features, and consumer feedback across digital channels to enable faster product innovation and strategic decision-making.

The United States currently represents the most advanced ecosystem for AI analytics agents used in product intelligence, supported by a mature AI infrastructure and extensive enterprise AI adoption. Over 62% of large enterprises in the country are already using AI-driven product analytics platforms to monitor customer behavior and competitive benchmarks. The country hosts more than 35% of global AI startups, many specializing in autonomous analytics agents and product intelligence platforms. Technology giants and enterprise software vendors collectively invest over USD 25 billion annually in AI R&D, accelerating the development of agent-based analytics solutions. In sectors such as e-commerce and SaaS, over 48% of product managers rely on AI-powered analytics dashboards and autonomous agents for feature optimization, pricing analysis, and customer sentiment monitoring.

Market Size & Growth: The market was valued at USD 118.0 Million in 2025 and is projected to reach USD 2,255.4 Million by 2033, expanding at a 44.6% CAGR due to rapid enterprise adoption of autonomous analytics agents for product lifecycle insights and competitive intelligence.

Top Growth Drivers: Adoption of AI-driven product analytics by 58% of digital enterprises, productivity gains of 35% in product research workflows, and 42% improvement in real-time customer insight analysis.

Short-Term Forecast: By 2028, AI analytics agents are expected to reduce manual product data analysis costs by 30% and improve feature development cycles by 25%.

Emerging Technologies: Integration of agentic AI architectures, vector database-driven semantic analytics, and multimodal product intelligence models capable of analyzing images, reviews, and behavioral data.

Regional Leaders: North America is projected to exceed USD 910 Million by 2033 driven by enterprise SaaS adoption, Asia-Pacific may reach USD 720 Million due to digital commerce expansion, while Europe could surpass USD 480 Million supported by strong AI governance frameworks.

Consumer/End-User Trends: Product teams increasingly deploy AI agents to monitor customer feedback, with over 45% of product managers using AI analytics dashboards to track feature usage, competitor benchmarks, and pricing trends.

Pilot or Case Example: In 2024, a global SaaS firm implemented autonomous product analytics agents, improving feature prioritization efficiency by 28% and reducing product research time by 40%.

Competitive Landscape: OpenAI-powered analytics ecosystems hold roughly 21% influence in enterprise deployments, followed by major technology companies including Microsoft, Google, IBM, Salesforce, and Oracle.

Regulatory & ESG Impact: AI governance regulations and transparency frameworks are pushing enterprises to adopt explainable analytics systems, with over 37% of AI deployments now incorporating ethical AI monitoring tools.

Investment & Funding Patterns: Global venture funding in agentic AI and product intelligence platforms exceeded USD 6.4 billion in recent investment rounds, with strong backing for enterprise analytics startups.

Innovation & Future Outlook: Autonomous product intelligence agents are evolving toward self-learning decision engines, enabling predictive product roadmap planning and automated competitive benchmarking across digital ecosystems.

AI analytics agents for product intelligence are increasingly deployed across SaaS, e-commerce, fintech, and consumer electronics industries, collectively contributing nearly 70% of enterprise deployments. Advances in large language models, semantic search, and vector databases are enabling deeper product insight generation. Growing regulatory frameworks around responsible AI and rising digital commerce adoption across Asia and Europe are also influencing demand. Over the next decade, integration with product lifecycle management platforms and customer experience systems is expected to transform data-driven product strategies.

AI analytics agents for product intelligence are emerging as a strategic asset for organizations seeking to transform raw data into actionable insights across product lifecycle management, competitive analysis, and customer experience optimization. Enterprises are increasingly integrating autonomous analytics agents with product development pipelines to continuously monitor consumer feedback, usage metrics, and competitor offerings. These AI-driven systems enable product teams to analyze large volumes of structured and unstructured data, significantly accelerating decision-making and reducing reliance on manual research.

Modern agentic AI architectures are transforming product intelligence capabilities. For instance, agent-based analytics platforms deliver nearly 40% improvement in real-time product insight generation compared to traditional business intelligence dashboards, which often require manual data integration and analysis. This improvement enables organizations to rapidly detect shifts in customer preferences and emerging market trends.

From a regional perspective, North America dominates in deployment volume, driven by the presence of leading AI technology vendors and digital enterprises. Meanwhile, Asia-Pacific leads in adoption growth, with nearly 52% of technology companies actively piloting AI analytics agents to support digital product innovation and e-commerce strategies. Europe is also gaining momentum as enterprises adopt AI analytics solutions compliant with strict governance frameworks and data transparency regulations.

Short-term projections indicate that by 2028, autonomous AI analytics agents will reduce product research cycle times by approximately 30%, enabling faster product releases and competitive benchmarking. At the same time, sustainability and responsible AI initiatives are shaping enterprise strategies. Firms are committing to ESG-aligned AI deployment practices, including up to 25% reduction in computational energy consumption by 2030 through optimized AI model architectures.

A notable micro-scenario occurred in 2024 when a U.S. SaaS company implemented an AI product intelligence agent network that improved feature adoption prediction accuracy by 33% through automated analysis of user behavior and product telemetry. As enterprises increasingly rely on continuous analytics for product innovation, the AI Analytics Agents for Product Intelligence Market is positioned as a critical pillar for operational resilience, regulatory compliance, and sustainable digital transformation.

The AI Analytics Agents for Product Intelligence Market is evolving rapidly as organizations adopt autonomous AI systems capable of analyzing product performance, customer sentiment, and competitive data in real time. Increasing volumes of digital product data generated through e-commerce platforms, SaaS applications, and mobile ecosystems are creating strong demand for intelligent analytics agents that can convert complex datasets into strategic insights. Enterprises are shifting from traditional dashboards to AI-driven decision engines capable of continuously monitoring product metrics, forecasting demand trends, and identifying emerging opportunities.

Technological advancements in large language models, vector databases, and multi-agent systems are enabling deeper contextual understanding of product data across multiple channels. Additionally, the integration of AI analytics agents with product lifecycle management platforms and customer experience systems is transforming how organizations manage product innovation and market positioning. Growing enterprise investments in AI infrastructure, increasing digital transformation initiatives, and rising competition in consumer-centric industries are further influencing market dynamics and accelerating adoption across global industries.

The rapid expansion of digital commerce and software-based products has significantly increased the volume of product-related data generated every day. Organizations now process billions of user interactions, reviews, and feature usage metrics, creating an urgent need for automated analytics solutions capable of interpreting these datasets in real time. AI analytics agents provide continuous monitoring and automated insights, enabling product managers to quickly identify performance gaps and emerging customer preferences. In modern digital platforms, over 70% of product decisions are now influenced by user analytics and behavioral data. AI agents help companies process this information faster by analyzing customer feedback, competitor features, and market signals simultaneously. These systems can automatically generate feature recommendations, detect sentiment trends, and forecast demand fluctuations. For example, AI analytics tools can analyze millions of product reviews and social media comments within minutes, enabling companies to adjust product strategies rapidly. This capability significantly improves product innovation cycles and operational efficiency, making AI analytics agents an increasingly essential tool for product intelligence across technology, retail, and consumer electronics industries.

Despite the strong growth potential of AI analytics agents, concerns related to data privacy, security, and system integration remain major obstacles for many organizations. Product intelligence platforms typically require access to large volumes of customer behavior data, product usage metrics, and competitive information. Handling such datasets raises compliance concerns, particularly in regions with strict data protection regulations and governance requirements. Enterprises also face technical challenges when integrating AI analytics agents with existing data systems such as CRM platforms, product lifecycle management tools, and enterprise analytics infrastructures. Many organizations operate on fragmented data architectures where product data is stored across multiple platforms, making seamless AI deployment difficult. Studies indicate that nearly 43% of enterprises report difficulties integrating AI tools with legacy analytics systems, resulting in slower adoption rates. Additionally, concerns about algorithm transparency and bias in AI decision-making can discourage organizations from fully automating product intelligence workflows, limiting the speed at which AI analytics agents are implemented across industries.

The rapid expansion of digital product ecosystems presents significant opportunities for the adoption of AI analytics agents. Modern products are increasingly connected to cloud platforms, mobile applications, and IoT ecosystems, generating continuous streams of product performance and user interaction data. These data flows create ideal conditions for AI-driven product intelligence systems that can process and interpret large datasets autonomously. For example, global mobile application ecosystems generate over 200 billion app downloads annually, producing vast amounts of user behavior data that can be analyzed using AI analytics agents. Similarly, e-commerce platforms process millions of transactions and customer reviews every day, providing valuable insights into product performance and consumer preferences. AI agents can automatically identify patterns in this data and generate strategic recommendations for product improvements, pricing optimization, and competitive benchmarking. As companies increasingly rely on digital channels for product distribution and customer engagement, the demand for AI-powered product intelligence solutions is expected to expand significantly across industries.

A key challenge affecting the AI Analytics Agents for Product Intelligence Market is the shortage of skilled professionals capable of designing, deploying, and managing advanced AI systems. Building autonomous analytics agents requires expertise in machine learning, natural language processing, data engineering, and software integration. However, global demand for AI specialists continues to exceed supply, creating talent gaps that slow the deployment of advanced analytics solutions. Operational costs also present difficulties for smaller organizations attempting to adopt AI analytics agents. Implementing these systems often requires investment in high-performance computing infrastructure, large datasets, and continuous model training processes. Additionally, maintaining data quality and monitoring AI outputs requires ongoing operational oversight. Surveys show that over 38% of companies cite AI infrastructure costs and resource limitations as barriers to large-scale deployment. These challenges can delay adoption timelines, particularly for small and medium-sized enterprises seeking to integrate AI analytics into their product intelligence strategies.

Growing Adoption of Autonomous Product Intelligence Agents: Enterprises are rapidly deploying autonomous AI agents to monitor product performance metrics across digital platforms. Recent enterprise technology surveys indicate that over 47% of product development teams are now experimenting with autonomous analytics agents capable of continuously analyzing product usage data and customer feedback. These systems can process over 10 million user interactions per day in large digital platforms, helping organizations detect emerging product trends earlier and respond faster to market changes.

Integration of Multimodal AI Analytics for Product Insights: Modern AI analytics agents increasingly combine text, image, and behavioral data to generate comprehensive product intelligence insights. For example, multimodal AI models can analyze over 500,000 product images and reviews simultaneously, identifying feature design patterns and customer sentiment trends. Adoption of multimodal analytics tools has grown by nearly 36% among e-commerce and SaaS companies, enabling deeper insights into consumer preferences and product performance.

Expansion of Real-Time Competitive Intelligence Platforms: AI analytics agents are now widely used to track competitor product features, pricing strategies, and market launches in real time. Approximately 52% of technology companies report using AI-driven competitive intelligence dashboards that continuously monitor competitor platforms and digital marketplaces. These systems can detect pricing changes or feature updates within minutes rather than days, significantly improving strategic decision-making for product managers.

Increasing Integration with Product Lifecycle Management Systems: Organizations are integrating AI analytics agents directly into product lifecycle management and product development platforms. Nearly 41% of global manufacturing and software companies are integrating AI analytics modules into PLM systems to track feature adoption, product defects, and customer feedback automatically. Such integration allows product teams to improve design cycles and reduce product update timelines by up to 22%, accelerating innovation across competitive industries.

The AI Analytics Agents for Product Intelligence Market is segmented by type, application, and end-user industries, reflecting the diverse ways organizations deploy autonomous analytics systems for product-related insights. AI analytics agents can be categorized into multiple technological types based on their capabilities, including predictive analytics agents, natural language processing agents, and multimodal analytics systems capable of processing complex data formats. Each type plays a distinct role in analyzing customer feedback, market trends, and product performance metrics.

From an application perspective, these AI agents support activities such as product development optimization, competitive intelligence analysis, pricing strategy development, and customer sentiment monitoring. Businesses use these applications to understand consumer behavior and identify product improvements in real time. End-user industries deploying AI analytics agents include technology companies, e-commerce platforms, financial services providers, and consumer electronics manufacturers. As digital products generate increasing volumes of customer interaction data, organizations are adopting AI analytics agents to enhance product decision-making and maintain competitiveness in rapidly evolving markets.

AI analytics agents for product intelligence can be categorized into predictive analytics agents, natural language processing (NLP) agents, multimodal analytics agents, and other specialized analytics systems. Among these, predictive analytics agents currently represent the leading segment with approximately 38% of market adoption, as they enable enterprises to forecast product demand trends, analyze usage patterns, and predict customer behavior based on historical datasets. These agents are widely used in digital product ecosystems where continuous forecasting of feature adoption and user engagement is essential. Multimodal analytics agents are emerging as the fastest-growing category with an estimated growth rate of around 47% annually, driven by the ability to analyze diverse data formats including images, text reviews, and behavioral metrics simultaneously. Organizations deploying multimodal AI systems can gain deeper insights into product design performance and customer preferences, particularly in e-commerce and consumer electronics sectors. Natural language processing agents account for nearly 27% of deployments, focusing primarily on analyzing customer feedback, reviews, and support interactions to extract product insights. Meanwhile, other specialized analytics systems such as anomaly-detection agents and recommendation agents collectively represent roughly 35% of the remaining market, serving niche analytics requirements within enterprise environments.

• In 2025, a major global e-commerce platform implemented multimodal AI analytics systems capable of processing over 2 million product reviews daily, enabling automated detection of product feature issues and improving product improvement cycles.

AI analytics agents are applied across several critical product intelligence functions including competitive product benchmarking, product performance monitoring, customer sentiment analysis, and pricing optimization. Among these, customer sentiment analysis represents the leading application with approximately 34% adoption, as companies increasingly rely on AI systems to analyze customer reviews, social media discussions, and feedback channels to understand product perception. Competitive intelligence analysis is the fastest-growing application with an estimated growth rate of about 46%, driven by organizations seeking real-time insights into competitor product launches, pricing strategies, and feature improvements. AI analytics agents enable companies to track competitor activities automatically and generate strategic alerts for product managers. Product performance monitoring accounts for roughly 28% of deployments, focusing on analyzing usage metrics and product telemetry to identify design improvements. Pricing optimization and market trend analysis collectively represent 38% of remaining applications, particularly within digital commerce and subscription-based product markets. In terms of consumer adoption trends, over 41% of enterprises globally reported testing AI-driven product analytics systems in 2025, particularly for improving customer experience insights. Additionally, nearly 58% of digital commerce companies use AI analytics to monitor customer feedback in real time.

• In 2024, a large global technology company deployed AI analytics agents across its software ecosystem, analyzing more than 100 million user interactions monthly to identify feature adoption patterns and guide product roadmap decisions.

The deployment of AI analytics agents for product intelligence varies across several industries, including technology and software companies, e-commerce platforms, financial services organizations, and consumer electronics manufacturers. Among these, technology and SaaS companies represent the largest end-user segment with approximately 36% adoption, as these firms generate extensive product telemetry and customer interaction data that require advanced analytics capabilities. AI agents enable these organizations to monitor feature adoption, optimize user experience, and refine product roadmaps. E-commerce platforms represent the fastest-growing end-user segment with an estimated annual growth rate of around 48%, driven by the need to analyze millions of product reviews, pricing changes, and customer interactions across digital marketplaces. AI analytics agents allow retailers to quickly identify product demand trends and improve catalog performance. Financial services and fintech companies account for roughly 22% of adoption, utilizing AI analytics agents to analyze customer usage patterns for digital banking products and financial applications. Consumer electronics manufacturers and other industrial users collectively represent about 42% of the remaining market, using AI analytics systems to monitor product performance and design improvements. From an adoption perspective, nearly 45% of global enterprises reported deploying AI-driven analytics tools for product intelligence workflows in 2025, particularly within digital product ecosystems. Additionally, around 39% of product management teams rely on AI insights to guide feature prioritization and product roadmap planning.

• In 2025, a multinational software company deployed AI analytics agents to analyze over 50 million product interactions annually, enabling product teams to reduce feature rollout delays and significantly improve product usability insights.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 46.2% between 2026 and 2033.

The strong position of North America is driven by the presence of over 8,500 AI startups and more than 65% enterprise AI adoption among Fortune 500 companies, particularly in SaaS, retail technology, and financial analytics. The region also hosts a significant portion of global AI infrastructure, including more than 35% of enterprise cloud AI data centers. Europe held approximately 27% of the global market in 2025, supported by strict data governance frameworks and strong enterprise demand for explainable AI analytics tools. Meanwhile, Asia-Pacific accounted for nearly 23% of the global deployments, with more than 3,000 AI-focused startups operating across China, India, Japan, and South Korea. Rapid growth of digital commerce platforms generating billions of customer interactions annually is accelerating adoption of AI product intelligence tools. South America represented about 5% of global demand, mainly concentrated in Brazil and Argentina where digital commerce penetration has crossed 72% of urban consumers. The Middle East & Africa contributed roughly 4% of deployments, driven by government-led AI initiatives and large-scale digital transformation programs in sectors such as finance, telecom, and energy.

North America represents the most mature ecosystem for AI analytics agents used in product intelligence, accounting for nearly 41% of global deployments. The region’s technology, SaaS, e-commerce, and financial services industries are primary demand drivers, collectively generating more than 60% of enterprise product analytics use cases. Over 68% of large enterprises in the United States and Canada have integrated AI-driven analytics into product development workflows, enabling real-time monitoring of user behavior, product features, and competitive benchmarks. Regulatory frameworks promoting responsible AI deployment and data transparency are also shaping enterprise adoption strategies. Technological advancements such as vector databases, agentic AI frameworks, and large language models are widely integrated with product lifecycle management platforms across the region. A notable example includes Salesforce, which is actively embedding autonomous analytics agents within its enterprise product intelligence ecosystem to help companies analyze millions of customer interactions daily. Regional consumer behavior also varies significantly, with higher enterprise adoption in healthcare, financial services, and digital commerce sectors, where AI analytics tools help monitor product usage patterns and improve customer experience metrics.

Europe holds approximately 27% of the global AI analytics agents for product intelligence market, supported by strong enterprise technology ecosystems in Germany, the United Kingdom, and France. The region has witnessed rapid growth in explainable AI solutions due to regulatory frameworks emphasizing algorithm transparency and responsible AI governance. Over 52% of European enterprises implementing AI analytics tools prioritize explainable AI capabilities to comply with emerging regulatory standards and data governance guidelines. Industrial technology firms, automotive manufacturers, and digital commerce platforms are key users of AI-driven product intelligence tools. The region is also experiencing increased adoption of multimodal analytics agents capable of analyzing product images, consumer reviews, and user interaction data simultaneously. European digital transformation initiatives have led to over 45% of medium and large enterprises integrating AI-driven analytics dashboards into product management systems. Local players such as SAP are actively developing enterprise AI analytics platforms that integrate product intelligence capabilities into enterprise resource planning systems. Consumer behavior patterns in this region indicate that regulatory pressure and compliance requirements significantly influence enterprise purchasing decisions for AI analytics technologies.

Asia-Pacific represents the fastest-growing region and the third-largest market by deployment volume, accounting for roughly 23% of global installations. The region’s rapid digitalization and expanding e-commerce ecosystems generate massive product data streams that require advanced analytics systems. China, India, Japan, and South Korea are the primary markets driving adoption, collectively contributing more than 70% of regional demand. China alone hosts more than 4,000 AI startups, many developing analytics agents and intelligent product monitoring platforms. Meanwhile, India’s technology ecosystem has experienced significant growth, with over 2,000 AI-driven software startups focusing on enterprise analytics and product intelligence solutions. Technology innovation hubs in cities such as Shenzhen, Bangalore, and Tokyo are accelerating AI product development. Local companies such as Alibaba Cloud are integrating AI analytics capabilities into cloud commerce platforms to analyze millions of product interactions daily. Regional consumer behavior also differs from Western markets, with adoption largely driven by e-commerce platforms, mobile AI applications, and digital marketplaces, which generate billions of product-related data points every day.

South America accounts for nearly 5% of the global AI analytics agents for product intelligence market, with Brazil and Argentina representing the largest markets in the region. Rapid expansion of digital commerce platforms and social media ecosystems has increased the need for advanced analytics systems capable of monitoring product sentiment and customer engagement. Brazil alone has more than 150 million active internet users, creating significant demand for AI-powered product analytics tools used by retailers and digital media companies. Infrastructure investments in cloud computing and data centers are also improving the region’s capacity to deploy AI analytics systems. Government initiatives supporting digital innovation and technology startups have accelerated enterprise adoption in sectors such as financial services, telecommunications, and e-commerce. Local AI technology firms such as Take Blip are developing conversational AI and analytics solutions that help businesses analyze customer interactions and product feedback at scale. Consumer behavior trends in the region reveal that demand for AI analytics is closely tied to digital media engagement, language localization, and customer sentiment analysis, particularly within retail and entertainment sectors.

The Middle East & Africa region represents approximately 4% of global AI analytics agent deployments, with strong demand emerging from the United Arab Emirates, Saudi Arabia, and South Africa. Governments in the region are investing heavily in artificial intelligence strategies and digital transformation initiatives across sectors including energy, financial services, telecommunications, and smart city infrastructure. The UAE’s national AI strategy has encouraged enterprises to integrate AI analytics systems into product development and digital services platforms. Technology modernization programs across Gulf economies are also expanding the deployment of AI-powered analytics systems capable of processing large datasets generated by digital services. Telecommunications operators and energy companies are particularly active adopters of AI-driven product intelligence tools. A notable example is G42, an AI technology company headquartered in Abu Dhabi, which is developing enterprise analytics platforms capable of analyzing massive operational datasets for product optimization. Regional consumer behavior indicates increasing adoption of AI-enabled digital services, with demand for analytics solutions driven by smart city initiatives, fintech innovation, and mobile service ecosystems.

United States – 36% Market Share: Strong AI innovation ecosystem, high enterprise adoption of product intelligence platforms, and large investments in agentic AI technologies drive dominance.

China – 18% Market Share: Rapid expansion of digital commerce platforms, large AI startup ecosystem, and high volumes of consumer interaction data accelerate deployment.

The competitive environment in the AI Analytics Agents for Product Intelligence Market is characterized by moderate fragmentation with increasing consolidation driven by partnerships and technology integration strategies. Currently, more than 120 technology companies and AI startups globally offer product intelligence analytics platforms, ranging from enterprise software vendors to specialized AI agent developers. The market is heavily influenced by large technology firms with strong cloud computing infrastructure and advanced AI research capabilities.

The top five companies collectively account for approximately 44% of total enterprise deployments, reflecting a relatively competitive landscape where both established software vendors and emerging AI startups compete for market share. Major players are focusing on integrating agentic AI architectures, large language models, and multimodal analytics capabilities into enterprise product intelligence platforms. Partnerships between AI startups and cloud providers are also accelerating product innovation and deployment scalability.

Strategic initiatives such as AI model integration, acquisitions of analytics startups, and expansion of enterprise AI platforms are shaping competitive dynamics. For instance, several large technology companies have launched autonomous analytics agents capable of analyzing billions of product interactions and customer feedback records across digital platforms. Additionally, competition is intensifying as SaaS companies integrate product intelligence capabilities directly into product lifecycle management and customer experience platforms. Continuous innovation in real-time analytics, semantic search technologies, and vector database infrastructure is expected to further intensify competition and encourage market consolidation over the coming years.

Salesforce

Ibm

Microsoft

Oracle

SAP

Databricks

Snowflake

Palantir Technologies

C3.ai

DataRobot

H2O.ai

ThoughtSpot

Qlik

Technological innovation is a fundamental driver shaping the AI Analytics Agents for Product Intelligence Market. Modern product intelligence platforms are increasingly powered by agentic AI architectures, enabling autonomous decision-making systems capable of continuously analyzing large volumes of product data without human intervention. These agents operate within distributed AI environments where they collect, process, and interpret information from multiple sources including product telemetry data, consumer feedback, social media platforms, and competitive intelligence databases.

One of the most influential technologies supporting these systems is the integration of large language models (LLMs) capable of analyzing textual datasets such as customer reviews, feature feedback, and support interactions. Advanced LLMs can process millions of product-related text records within seconds, allowing organizations to extract insights related to customer sentiment, feature requests, and product performance issues. Additionally, the adoption of vector databases and semantic search technologies has significantly improved the ability of AI agents to analyze unstructured datasets, enabling contextual understanding of product information.

Another key technological trend is the emergence of multimodal analytics systems, which combine image recognition, text analytics, and behavioral data analysis to generate comprehensive product intelligence insights. For example, AI agents can analyze product images alongside consumer reviews to detect design issues or identify popular product attributes across digital marketplaces. These multimodal capabilities allow organizations to evaluate product performance across multiple data channels simultaneously.

Cloud-based AI infrastructure also plays a critical role in enabling scalable deployment of analytics agents. Enterprise cloud platforms now support distributed AI processing environments capable of analyzing billions of product interaction events per day, allowing organizations to deploy product intelligence systems globally. Additionally, advances in reinforcement learning and adaptive AI algorithms are enabling analytics agents to continuously improve their decision-making accuracy as they process new datasets.

Emerging innovations such as self-learning autonomous agents, AI copilots for product managers, and automated competitive intelligence systems are expected to further transform the market. These technologies enable organizations to automate product strategy development, detect emerging consumer trends earlier, and optimize product roadmaps through continuous AI-driven analysis.

• In October 2024, Salesforce announced the general availability of Agentforce, an enterprise platform enabling organizations to deploy autonomous AI agents that connect to enterprise data and perform tasks across sales, service, marketing, and commerce workflows. These agents can analyze large volumes of customer and product interaction data to automate decision-making and analytics processes. Source: www.salesforce.com

• In June 2025, Salesforce introduced Agentforce 3, a major upgrade designed to improve enterprise control and visibility for large-scale AI agent deployments. The release enhanced interoperability across enterprise systems and strengthened governance frameworks to help organizations manage complex networks of autonomous analytics agents operating across multiple business workflows.

• In June 2025, Databricks announced Lakebase, a fully managed operational Postgres database built for AI applications and agents. The new platform layer allows developers and enterprises to build AI-driven data applications and analytics agents more efficiently on a unified multi-cloud data intelligence platform.

• In January 2024, Databricks launched a Data Intelligence Platform for communications providers, combining data lakehouse architecture with generative AI capabilities to enable advanced analytics and AI-driven automation across enterprise datasets. The platform allows companies to build AI-powered applications and analytics tools on large-scale operational data environments.

The AI Analytics Agents for Product Intelligence Market Report provides a comprehensive examination of the global ecosystem supporting the deployment of autonomous analytics systems designed to improve product intelligence and decision-making processes. The report analyzes multiple dimensions of the market including technological developments, enterprise adoption patterns, regional deployment trends, and industry-specific applications of AI analytics agents.

The scope of the report includes detailed evaluation of product types such as predictive analytics agents, natural language processing agents, and multimodal analytics systems used to analyze large volumes of product-related data. These technologies enable enterprises to extract insights from customer feedback, product usage metrics, and competitive intelligence datasets. The report also covers major application areas including customer sentiment analysis, competitive benchmarking, product performance monitoring, and pricing optimization, highlighting how AI analytics agents support strategic product management activities.

Geographically, the report evaluates adoption trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing the technological infrastructure, enterprise digital transformation initiatives, and industry demand driving AI analytics agent deployments in each region. Key end-user industries analyzed include technology and software companies, digital commerce platforms, financial services organizations, consumer electronics manufacturers, and telecommunications providers, all of which generate significant volumes of product data requiring advanced analytics solutions.

In addition, the report explores the broader technology ecosystem supporting the market, including cloud computing infrastructure, large language models, semantic search technologies, and vector database systems. Emerging areas such as autonomous AI decision agents, AI copilots for product management teams, and real-time competitive intelligence systems are also examined as part of the evolving product intelligence landscape.

The report further highlights market competition, technology innovation strategies, and enterprise deployment models shaping the future of the industry. By analyzing multiple industry segments and regional ecosystems, the report offers strategic insights to support technology vendors, investors, product development teams, and enterprise decision-makers seeking to leverage AI analytics agents for improved product intelligence and market competitiveness.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 118.0 Million |

| Market Revenue (2033) | USD 2,255.4 Million |

| CAGR (2026–2033) | 44.60% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | OpenAI; Salesforce Inc.; IBM; Microsoft Corporation; Google LLC; Oracle Corporation; SAP SE; Databricks Inc.; Snowflake Inc.; Palantir Technologies Inc.; C3.ai Inc.; DataRobot Inc.; H2O.ai; ThoughtSpot Inc.; QlikTech International AB |

| Customization & Pricing | Available on Request (10% Customization Free) |