Reports

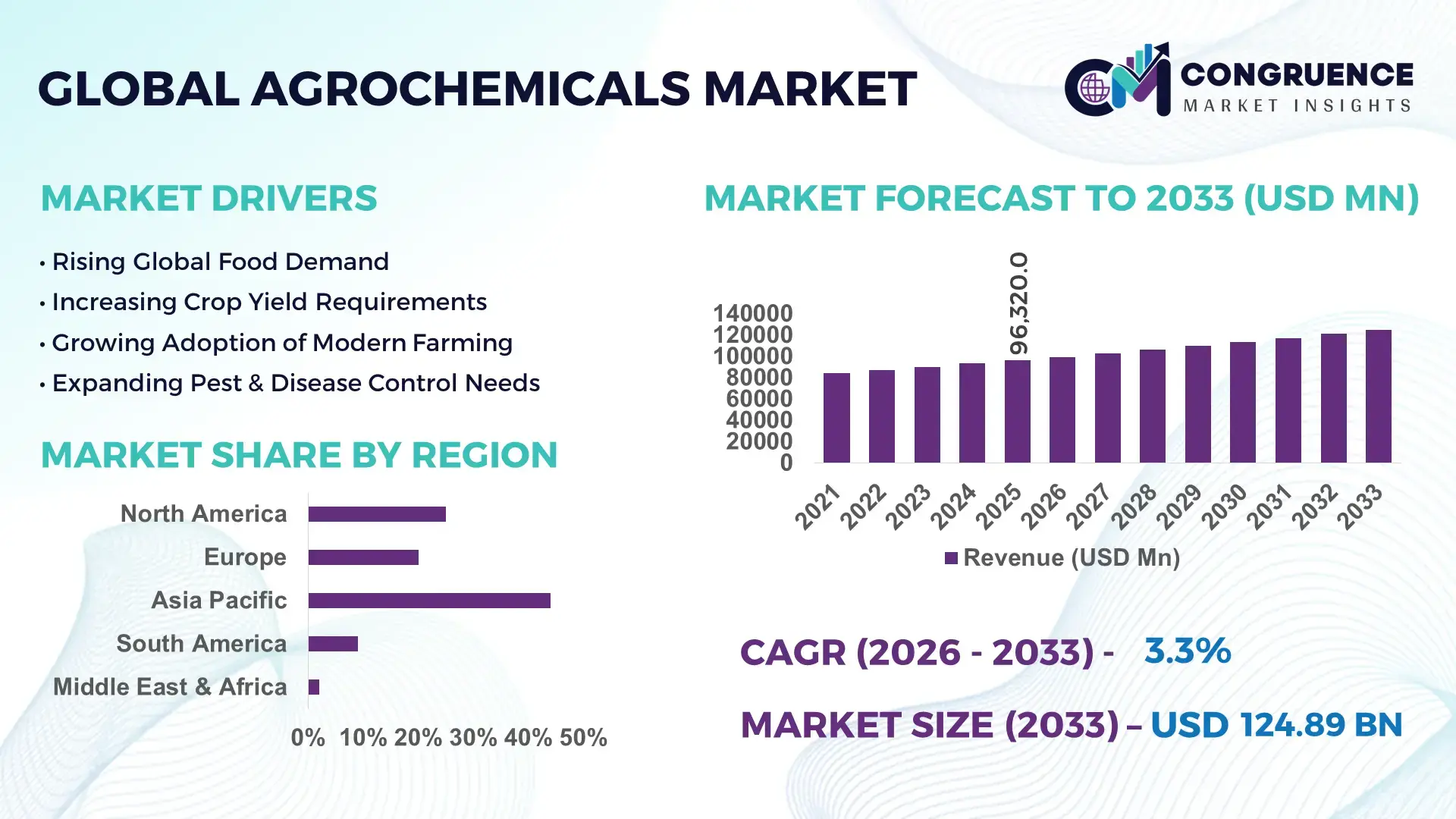

The Global Agrochemicals Market was valued at USD 96320 Million in 2025 and is anticipated to reach a value of USD 124887.52 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. The growth is primarily driven by increasing global food demand and the need to enhance agricultural productivity under limited arable land conditions.

China continues to represent the most influential production hub in the global agrochemicals market, with annual pesticide production exceeding 2.5 million metric tons and fertilizer output surpassing 55 million tons. The country has invested over USD 8 billion in agrochemical manufacturing upgrades and green chemistry initiatives over the past five years. Advanced formulation technologies, including controlled-release fertilizers and bio-based pesticides, are being rapidly deployed across large-scale farming operations. Approximately 65% of commercial farms in China have adopted integrated crop protection solutions, while precision agriculture tools have improved agrochemical application efficiency by nearly 20%. Strong domestic demand across cereals, fruits, and vegetables continues to support high-volume consumption and innovation in agrochemical products.

Market Size & Growth: USD 96320 Million in 2025 projected to reach USD 124887.52 Million by 2033 at 3.3% CAGR, driven by rising crop yield optimization needs and sustainable farming practices.

Top Growth Drivers: Precision farming adoption (35%), increasing crop protection demand (28%), bio-based agrochemical usage growth (22%).

Short-Term Forecast: By 2028, advanced agrochemical formulations are expected to reduce input wastage by 18% and improve yield efficiency by 15%.

Emerging Technologies: AI-driven crop monitoring, drone-based pesticide spraying, and nano-formulated fertilizers enhancing nutrient absorption.

Regional Leaders: Asia-Pacific projected at USD 52 billion by 2033 with high-volume consumption; North America at USD 28 billion driven by precision farming; Europe at USD 22 billion emphasizing sustainable inputs.

Consumer/End-User Trends: Large-scale commercial farms account for over 60% of agrochemical usage, with increasing adoption among smallholder farmers through subsidized programs.

Pilot or Case Example: In 2024, India-based smart spraying initiatives reduced pesticide usage by 25% while improving crop output by 12%.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players including global chemical manufacturers and agricultural solution providers.

Regulatory & ESG Impact: Stringent environmental regulations are driving a 30% shift toward bio-based and low-toxicity agrochemicals.

Investment & Funding Patterns: Over USD 12 billion invested globally in sustainable agrochemical R&D and digital agriculture platforms.

Innovation & Future Outlook: Growth in biodegradable pesticides, AI-integrated crop protection systems, and climate-resilient agrochemical formulations.

The agrochemicals market is strongly influenced by crop-specific demand patterns, where cereals contribute nearly 45% of total consumption, followed by fruits and vegetables at around 30%. Innovations such as microbial pesticides and slow-release fertilizers are improving nutrient efficiency by up to 25%. Regulatory frameworks across Europe and North America are pushing for reduced chemical toxicity, accelerating adoption of eco-friendly alternatives. Meanwhile, emerging economies are witnessing increased consumption due to government subsidies and expanding agricultural exports. Future trends indicate rising integration of digital agriculture with agrochemical usage, enhancing precision and minimizing environmental impact while ensuring consistent crop yields.

The agrochemicals market holds strategic importance as a critical enabler of global food security, agricultural efficiency, and sustainable crop production systems. Increasing pressure on food supply chains, coupled with shrinking arable land per capita, has accelerated the adoption of high-performance agrochemical inputs across both developed and developing economies. Advanced formulations such as nano-fertilizers deliver 30% higher nutrient absorption efficiency compared to conventional granular fertilizers, significantly improving yield outcomes while reducing environmental runoff.

Asia-Pacific dominates in volume due to large-scale agricultural output, while North America leads in adoption with over 70% of farms utilizing precision agriculture technologies integrated with agrochemical application systems. By 2028, AI-driven crop analytics platforms are expected to improve input optimization by 20%, reducing overuse and enhancing sustainability metrics across farming operations. ESG commitments are shaping industry transformation, with firms targeting a 25% reduction in chemical toxicity and a 40% increase in biodegradable product portfolios by 2030.

In 2024, India achieved a 22% reduction in pesticide consumption through drone-based precision spraying initiatives, demonstrating measurable efficiency gains and cost savings. Strategic investments are increasingly directed toward bio-based crop protection solutions and digital farming ecosystems, aligning with evolving regulatory frameworks and environmental compliance standards. As technological integration deepens and sustainability mandates strengthen, the agrochemicals market is positioned as a foundational pillar supporting resilient agricultural systems, regulatory alignment, and long-term sustainable growth.

The increasing global population, projected to surpass 8.5 billion within the next decade, is intensifying the demand for food production, thereby driving the agrochemicals market. Agricultural productivity must increase by approximately 50% to meet future food requirements, leading to greater reliance on fertilizers and crop protection chemicals. Enhanced agrochemical usage has been shown to improve crop yields by up to 40% in staple crops such as wheat and rice. Additionally, expanding agricultural exports from emerging economies are further boosting demand for high-efficiency agrochemical products. Governments are supporting this trend through subsidy programs and training initiatives, enabling farmers to adopt modern agrochemical solutions at scale.

Strict environmental and health regulations are limiting the use of certain chemical-based agrochemicals, particularly in regions such as Europe and North America. Regulatory bans on specific active ingredients have led to the withdrawal of numerous products from the market, reducing available options for farmers. Compliance costs for manufacturers have increased significantly, with product approval timelines extending beyond 8–10 years in some cases. Additionally, concerns regarding soil degradation, water contamination, and biodiversity loss are prompting tighter controls on chemical usage. These factors are compelling companies to invest heavily in reformulation and testing, which can delay product launches and increase operational costs.

The shift toward sustainable agriculture is creating substantial opportunities in the bio-based agrochemicals segment. Biopesticides and organic fertilizers are gaining traction due to their lower environmental impact and compatibility with organic farming practices. Adoption rates for bio-based products have increased by over 20% in the past five years, particularly in Europe and North America. Advances in microbial and enzyme-based formulations are improving efficacy levels, making them viable alternatives to traditional chemicals. Additionally, government incentives promoting sustainable farming and rising consumer preference for organic produce are further accelerating demand. These trends are opening new revenue streams and encouraging innovation in environmentally friendly agrochemical solutions.

The agrochemicals market faces significant challenges due to increasing raw material costs and supply chain disruptions. Key inputs such as natural gas, phosphate rock, and potash have experienced price volatility, directly impacting production costs. Transportation bottlenecks and geopolitical tensions have further complicated global supply chains, leading to delayed deliveries and reduced inventory availability. Manufacturers are also dealing with fluctuating energy prices, which affect large-scale production processes. These challenges are increasing the cost burden on farmers, potentially limiting adoption rates, especially in price-sensitive regions. Addressing these issues requires strategic sourcing, localized production, and improved supply chain resilience.

• Precision Agriculture Adoption Surpassing 65% Across Large Farms: The integration of precision agriculture technologies is transforming agrochemical application practices, with over 65% of large-scale farms globally adopting GPS-guided spraying and AI-based crop monitoring systems. These technologies have reduced agrochemical input wastage by nearly 20% while improving crop yield efficiency by approximately 15%. Automated spraying systems and drone-based pesticide delivery are gaining traction, particularly in North America and Asia-Pacific, where operational efficiency and cost optimization are critical. The use of variable rate technology (VRT) is also increasing, enabling farmers to adjust chemical application by up to 30% based on soil and crop conditions.

• Bio-Based Agrochemicals Usage Rising by Over 25% Globally: Sustainable farming practices are driving the adoption of bio-based agrochemicals, with global usage increasing by more than 25% over the past five years. Biopesticides now account for approximately 18% of total crop protection products, supported by regulatory restrictions on synthetic chemicals and rising demand for organic produce. Microbial fertilizers and enzyme-based formulations are improving nutrient absorption efficiency by up to 22%, while reducing soil toxicity levels by nearly 30%. Europe leads in adoption, with over 40% of farms incorporating at least one form of bio-based agrochemical solution.

• Digital Farming Platforms Enhancing Input Efficiency by 20%: The rise of digital agriculture platforms is significantly influencing agrochemical market dynamics, with over 50% of commercial farms utilizing farm management software for crop planning and chemical application tracking. These platforms enable real-time monitoring of soil health, weather patterns, and pest activity, improving decision-making accuracy by nearly 25%. Integration with IoT sensors has reduced excessive fertilizer usage by approximately 18%, while predictive analytics tools are helping farmers prevent crop losses by up to 12%. Adoption is particularly strong in technologically advanced agricultural economies.

• Nano-Formulated Agrochemicals Improving Absorption by 30%: Advances in nanotechnology are introducing highly efficient agrochemical formulations, with nano-fertilizers and nano-pesticides improving nutrient delivery and pest control effectiveness by up to 30%. These formulations require lower dosage volumes, reducing environmental impact by nearly 20% compared to conventional products. Adoption rates are steadily increasing, especially in regions facing soil degradation and water scarcity challenges. Research initiatives indicate that nano-enabled agrochemicals can extend nutrient release cycles by up to 40%, enhancing long-term soil fertility and crop productivity.

The agrochemicals market segmentation is defined by diverse product categories, application areas, and end-user groups, each contributing uniquely to overall market dynamics. By type, fertilizers dominate usage patterns due to their critical role in enhancing soil fertility and crop yield, followed by pesticides and herbicides that support crop protection. Applications are largely concentrated in cereals and grains, which account for a significant share of global agrochemical consumption due to their large cultivation areas and high demand. Horticulture and cash crops are also emerging as key application segments, driven by export-oriented farming practices. From an end-user perspective, large-scale commercial farms lead adoption due to higher investment capacity and access to advanced technologies, while smallholder farmers represent a growing segment supported by government subsidies and training programs. Increasing awareness of sustainable agriculture and regulatory compliance is influencing segmentation trends, particularly in developed regions.

Fertilizers represent the leading segment in the agrochemicals market, accounting for approximately 55% of total product usage due to their essential role in improving soil nutrient content and enhancing crop productivity. Nitrogen-based fertilizers dominate within this category, contributing to over 60% of fertilizer consumption, followed by phosphate and potash variants. Pesticides account for around 30% of the market, with insecticides and fungicides being widely used to protect crops from pests and diseases. Herbicides contribute nearly 15%, primarily used for weed control in large-scale farming operations. Bio-based agrochemicals are the fastest-growing type, expanding at an estimated CAGR of 9.5%, driven by increasing environmental regulations and demand for sustainable farming solutions. These products are gaining traction due to their lower toxicity and compatibility with organic agriculture practices. Other niche segments, including plant growth regulators and soil conditioners, collectively account for approximately 10% of the market, serving specialized agricultural needs.

Cereals and grains dominate the application segment, accounting for approximately 45% of agrochemical usage due to their extensive cultivation and high global demand. Agrochemicals are critical in this segment for improving yield stability and protecting crops from pests and diseases. Fruits and vegetables account for nearly 30% of applications, driven by the need for high-quality produce and export standards. However, oilseeds and pulses are emerging as the fastest-growing application segment, with an estimated CAGR of 8.2%, supported by increasing demand for plant-based proteins and expanding cultivation areas. Other applications, including turf management and ornamental plants, collectively contribute around 25% of the market, serving niche but growing segments. Technological advancements such as targeted spraying and precision nutrient delivery are further enhancing agrochemical efficiency across applications.

Commercial farming enterprises represent the leading end-user segment, accounting for approximately 60% of agrochemical consumption due to their large-scale operations and ability to invest in advanced technologies. These farms extensively utilize precision agriculture tools and integrated crop management systems to optimize agrochemical usage. Smallholder farmers account for around 30% of the market, with adoption rates increasing due to government subsidies, training programs, and access to affordable agrochemical products. Agri-cooperatives and contract farming organizations are the fastest-growing end-user segment, expanding at an estimated CAGR of 7.8%, driven by collective purchasing power and shared access to advanced farming technologies. These groups are enabling small-scale farmers to adopt modern agrochemical solutions more efficiently. Other end-users, including research institutions and agricultural service providers, collectively contribute approximately 10% of the market.

Region Asia-Pacific accounted for the largest market share at 47% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high agricultural output, with over 1.2 billion hectares of cultivated land and agrochemical consumption exceeding 60 million metric tons annually. China and India together contribute more than 55% of regional demand, driven by intensive farming practices and government-backed subsidy programs covering up to 30% of input costs. North America demonstrates rapid growth due to advanced farming technologies, where over 70% of farms utilize precision agriculture tools, improving agrochemical efficiency by nearly 20%. Europe holds approximately 22% of the market, with strict regulatory frameworks pushing bio-based product adoption above 35%. South America contributes around 18%, led by Brazil’s large-scale soybean and corn cultivation exceeding 80 million hectares. The Middle East & Africa region, accounting for nearly 8%, is witnessing rising demand due to expanding irrigation projects and increasing adoption of modern farming techniques across 25% of arable land.

How are advanced precision farming technologies reshaping agrochemical demand patterns?

North America holds approximately 21% of the global agrochemicals market, supported by highly mechanized agriculture and strong adoption of digital farming solutions. Key industries driving demand include large-scale grain production, particularly corn and wheat, along with specialty crops such as fruits and vegetables. Over 75% of farms in this region utilize GPS-guided equipment and data analytics platforms, improving chemical application efficiency by up to 18%. Regulatory frameworks emphasize environmental safety, with policies targeting a 25% reduction in chemical runoff and promoting bio-based alternatives. Technological advancements such as drone-based spraying and AI-powered crop monitoring are widely implemented. A leading regional player has invested in precision agriculture platforms, enabling farmers to reduce pesticide usage by 20% while maintaining yield levels. Consumer behavior reflects a strong preference for sustainable farming inputs, with over 40% of agricultural enterprises adopting eco-friendly agrochemical solutions.

Why is sustainability-driven innovation transforming agrochemical product demand patterns?

Europe accounts for nearly 22% of the agrochemicals market, with key countries including Germany, France, and the United Kingdom driving regional demand. The region is characterized by stringent environmental regulations, with over 50% of conventional chemical products undergoing reformulation to meet safety standards. Regulatory bodies are promoting sustainable agriculture initiatives, resulting in bio-based agrochemical adoption exceeding 38%. Precision farming technologies are increasingly integrated, with nearly 60% of farms utilizing digital monitoring tools for optimized chemical application. A prominent regional manufacturer has focused on developing low-toxicity pesticides, achieving a 30% reduction in environmental impact across its product portfolio. Consumer behavior is heavily influenced by regulatory pressure, leading to higher demand for transparent, environmentally compliant agrochemical solutions. Organic farming practices now account for approximately 12% of total agricultural land, further driving demand for sustainable inputs.

What factors are driving large-scale agrochemical consumption and innovation across high-growth agricultural economies?

Asia-Pacific leads the agrochemicals market in both volume and consumption, accounting for nearly 47% of global usage. Major consuming countries include China, India, and Japan, where agricultural activities span over 1.2 billion hectares. The region produces over 60 million metric tons of fertilizers annually, supported by extensive manufacturing infrastructure and government subsidies. Rapid industrialization and technological adoption are fostering innovation hubs focused on advanced agrochemical formulations and precision farming tools. A leading regional producer has expanded its production capacity by 15% in recent years, focusing on eco-friendly pesticide formulations. Consumer behavior varies widely, with smallholder farmers representing over 70% of the agricultural workforce, driving demand for cost-effective solutions. Mobile-based agricultural advisory platforms are used by nearly 50% of farmers, enhancing awareness and efficient agrochemical usage.

How are export-driven agricultural practices influencing agrochemical consumption patterns?

South America contributes approximately 18% to the global agrochemicals market, with Brazil and Argentina serving as key agricultural powerhouses. Brazil alone cultivates over 80 million hectares of soybean and corn, driving significant demand for fertilizers and crop protection chemicals. Infrastructure development in agricultural logistics has improved distribution efficiency by nearly 20%, supporting consistent agrochemical supply. Government incentives and favorable trade policies are encouraging increased agricultural exports, particularly to Asia and Europe. A regional agrochemical company has implemented integrated crop management solutions, improving yield efficiency by 15% across large farming operations. Consumer behavior is closely tied to export requirements, with farmers prioritizing high-performance agrochemicals to meet international quality standards. Adoption of advanced spraying technologies has increased by 25% in recent years.

What role do irrigation expansion and agricultural modernization play in shaping demand trends?

The Middle East & Africa region accounts for nearly 8% of the agrochemicals market, with growth driven by expanding irrigation projects and agricultural modernization initiatives. Key countries such as the UAE and South Africa are investing heavily in sustainable farming technologies, with irrigation coverage increasing by over 20% in arid regions. Demand is influenced by the need to enhance crop productivity under challenging climatic conditions, leading to increased adoption of high-efficiency fertilizers and pesticides. Technological advancements, including smart irrigation systems and soil monitoring tools, are improving agrochemical application efficiency by approximately 15%. A regional agricultural firm has introduced water-efficient fertilizer solutions, reducing water usage by 18% while maintaining crop yields. Consumer behavior reflects a growing emphasis on resource optimization, with over 30% of farms adopting modern agrochemical practices to address water scarcity and soil degradation challenges.

China Agrochemicals Market – 32% share: High production capacity exceeding 2.5 million metric tons of pesticides annually and strong domestic agricultural demand drive leadership.

India Agrochemicals Market – 18% share: Expanding agricultural base with over 160 million hectares of arable land and increasing adoption of modern farming inputs supports growth.

The agrochemicals market is moderately consolidated, with the top five companies accounting for approximately 55% of the global market share. The competitive environment is characterized by the presence of over 200 active players, including multinational corporations and regional manufacturers competing across product innovation, pricing strategies, and distribution networks. Leading companies are focusing on strategic mergers and acquisitions to strengthen their product portfolios and expand geographic reach. Over the past three years, more than 25 major partnerships have been formed to accelerate the development of bio-based agrochemicals and digital agriculture solutions.

Innovation remains a key differentiator, with companies investing nearly 8–10% of their annual budgets in research and development. Product launches in areas such as nano-formulations and microbial pesticides have increased by over 30%, reflecting the shift toward sustainable agriculture. Digital transformation is also influencing competition, with over 60% of leading firms integrating AI and data analytics into their product offerings. Additionally, companies are expanding production capacities by 10–15% to meet growing global demand. Competitive strategies increasingly emphasize sustainability, regulatory compliance, and technological advancement to maintain market positioning and capture emerging opportunities.

Bayer AG

Syngenta Group

BASF SE

Corteva Agriscience

FMC Corporation

UPL Limited

Sumitomo Chemical Co., Ltd.

Nufarm Limited

ADAMA Ltd.

Yara International ASA

Technological advancements are fundamentally transforming the agrochemicals market by improving efficiency, sustainability, and precision in agricultural practices. One of the most impactful developments is the integration of artificial intelligence and machine learning into crop management systems. AI-powered platforms are now used by over 55% of large-scale farms globally, enabling real-time analysis of soil conditions, weather patterns, and pest activity. These systems can optimize agrochemical application rates, reducing input usage by up to 20% while improving crop yields by approximately 15%.

Drone technology is another rapidly expanding innovation, with over 300,000 agricultural drones deployed worldwide for pesticide spraying and crop monitoring. These drones can cover up to 40 hectares per day, improving operational efficiency by nearly 25% compared to traditional manual methods. In parallel, the adoption of Internet of Things (IoT) sensors is increasing, with more than 45% of advanced farms using connected devices to monitor soil moisture, nutrient levels, and crop health. This data-driven approach has reduced fertilizer overuse by approximately 18% and enhanced nutrient efficiency by 22%.

Nanotechnology is gaining prominence in agrochemical formulations, particularly in the development of nano-fertilizers and nano-pesticides. These products improve nutrient delivery efficiency by up to 30% and extend release cycles by nearly 40%, reducing environmental impact. Additionally, biotechnology innovations such as genetically engineered crops compatible with specific agrochemical treatments are enhancing pest resistance and reducing chemical dependency by 25%. Digital farming ecosystems, integrating mobile applications and cloud-based analytics, are also expanding, with adoption rates exceeding 50% among progressive farming communities. These technologies collectively position the agrochemicals market for enhanced productivity, sustainability, and long-term operational optimization.

• In February 2025, Bayer AG announced the expansion of its biological crop protection portfolio with new microbial-based solutions targeting fungal diseases in cereals and fruits. These products demonstrated up to 20% improved disease resistance in field trials and are being scaled across multiple global agricultural markets. Source: www.bayer.com

• In October 2024, Syngenta Group launched a new digital agriculture platform integrating satellite imaging and AI-based crop analytics. The platform enables farmers to reduce pesticide usage by approximately 18% while improving yield efficiency by nearly 12% through precision application strategies. Source: www.syngenta.com

• In March 2025, BASF SE introduced an advanced herbicide formulation designed for resistance management in row crops. Field testing showed a 25% increase in weed control effectiveness and a 15% reduction in required application volume, supporting more sustainable farming practices. Source: www.basf.com

• In July 2024, Corteva Agriscience expanded its enzyme-based biopesticide line, targeting sustainable crop protection solutions. The innovation improved pest control efficiency by over 22% while reducing environmental residue levels by approximately 30%, aligning with stricter regulatory standards. Source: www.corteva.com

The Agrochemicals Market Report provides a comprehensive analysis of the global industry, covering a wide range of product categories, applications, technologies, and regional dynamics. The report evaluates key product segments including fertilizers, pesticides, herbicides, and emerging bio-based agrochemicals, which collectively account for over 90% of total market usage. It also examines specialized inputs such as plant growth regulators and soil conditioners, which contribute to targeted agricultural improvements across diverse crop types.

From an application perspective, the report covers major agricultural segments such as cereals and grains, fruits and vegetables, oilseeds, and pulses, which together represent more than 80% of agrochemical consumption. It also includes niche applications like turf management and horticulture, reflecting evolving agricultural practices and consumer preferences. The study further analyzes end-user categories, including commercial farms, smallholder farmers, and agricultural cooperatives, highlighting adoption patterns and technology integration levels across each segment.

Geographically, the report spans key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, providing insights into regional consumption patterns, production capacities, and regulatory frameworks. The scope also includes technological advancements such as precision agriculture, AI-driven crop monitoring, drone-based spraying systems, and nano-formulated agrochemicals, which are reshaping the industry landscape. Additionally, the report addresses sustainability trends, environmental compliance requirements, and innovation in eco-friendly products, offering a holistic view of the agrochemicals market for strategic decision-making and long-term planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, FMC Corporation, UPL Limited, Sumitomo Chemical Co., Ltd., Nufarm Limited, ADAMA Ltd., Yara International ASA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |