Reports

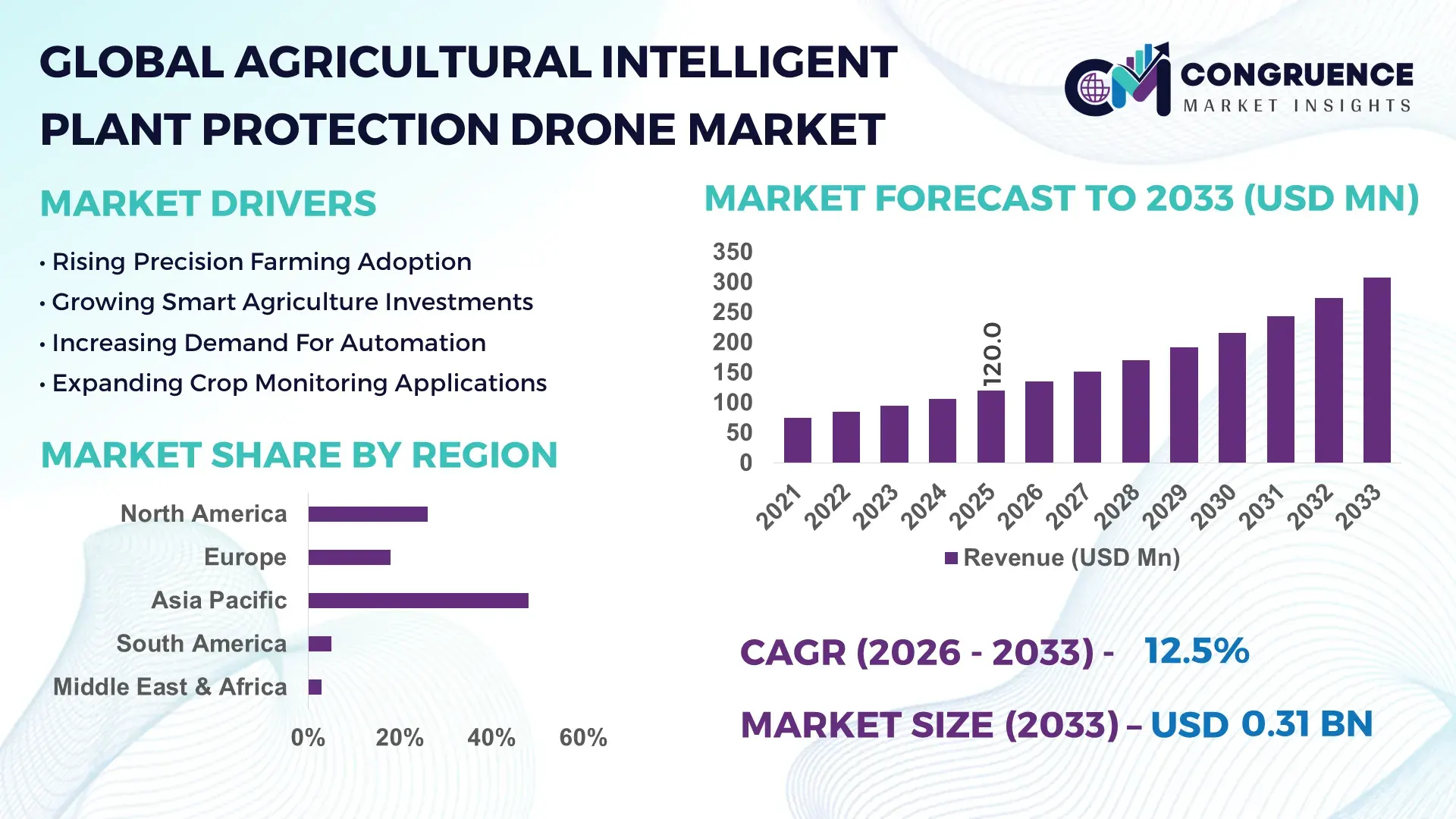

The Global Agricultural Intelligent Plant Protection Drone Market was valued at USD 120.0 Million in 2025 and is anticipated to reach a value of USD 307.9 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033. Rapid deployment of AI-enabled precision spraying systems, autonomous navigation software, and multispectral crop analytics is accelerating drone utilization across commercial farming operations, with pesticide consumption reduced by nearly 28% and field productivity improving by over 32% compared to conventional spraying methods. The market is further transforming as governments across Asia-Pacific, North America, and Europe tighten pesticide usage regulations between 2024 and 2026 while simultaneously supporting smart agriculture subsidies to strengthen food security and climate-resilient farming infrastructure amid ongoing agricultural labor shortages.

China continues to dominate the global Agricultural Intelligent Plant Protection Drone Market with approximately 41% market share, supported by over 220,000 operational agricultural drones and large-scale adoption across rice, wheat, and cotton cultivation. Chinese manufacturers account for more than 55% of global agricultural drone production capacity, while precision farming deployment across commercial farms expanded by 34% during the last two years. Compared to North America, where adoption is concentrated among large agribusinesses, China benefits from stronger manufacturing integration, lower deployment costs, and faster rural drone infrastructure expansion. The country has also accelerated autonomous spraying pilot programs across over 13 million hectares of farmland, reinforcing its execution-level leadership in advanced agricultural automation. The market is increasingly shaped by large-scale farming, precision crop protection demand, and intelligent fleet management systems, with cereals and grains contributing nearly 46% of deployment demand while orchard and specialty crop spraying adoption rises rapidly across high-value agriculture zones. AI-powered route optimization, swarm drone coordination, and battery-efficiency upgrades are improving operational productivity by over 30%, while stricter environmental compliance standards are forcing growers to shift toward low-drift aerial spraying technologies. Asia-Pacific remains the largest deployment hub, whereas North America and Europe are leading in autonomous software integration and regulatory-grade precision farming systems.

As agricultural supply chains face rising labor and resource constraints, companies are accelerating investments in scalable drone ecosystems, positioning intelligent plant protection platforms as a core competitive differentiator in next-generation precision agriculture strategies.

Market Size & Growth: USD 120.0 Million in 2025 reaching USD 307.9 Million by 2033, driven by 32% higher field efficiency through AI-enabled precision spraying systems.

Top Growth Drivers: Precision farming adoption expanded 34%, pesticide reduction efficiency reached 28%, and labor replacement demand increased 31% globally.

Short-Term Forecast: By 2028, autonomous spraying operations are projected to reduce crop protection costs by 24% while improving coverage speed by 37%.

Emerging Technologies: AI navigation, multispectral imaging, and swarm-drone coordination improved operational accuracy by over 29% across advanced farming deployments.

Regional Leaders: Asia-Pacific holds USD 49 Million demand leadership, North America leads software integration, while Europe accelerates ESG-driven smart farming deployment.

Consumer/End-User Trends: Nearly 46% of large commercial farms now prioritize drone-based crop protection to optimize chemical usage and labor efficiency.

Pilot/Case Example: In 2025, autonomous rice-field spraying projects in China improved pesticide utilization efficiency by 35% and reduced water usage by 30%.

Competitive Landscape: DJI controls approximately 38% global market share alongside XAG, Yamaha, Parrot, and EAVision in high-growth precision agriculture segments.

Regulatory & ESG Impact: Precision drone spraying reduced chemical drift by 27%, supporting tighter environmental compliance standards across Europe and North America.

Investment & Funding: Global agricultural drone ecosystem investments exceeded USD 850 Million, fueled by agri-tech partnerships and smart farming expansion initiatives.

Innovation & Future Outlook: Hydrogen-powered drones, automated charging hubs, and AI crop diagnostics are redefining scalable autonomous agricultural operations globally.

The Agricultural Intelligent Plant Protection Drone Market is rapidly transforming into a critical battleground for precision agriculture investment, operational efficiency, and food security optimization. Rising pressure on global agricultural productivity, combined with shrinking rural labor availability and stricter environmental compliance standards, is accelerating the transition toward autonomous crop protection systems. Large-scale agribusinesses are aggressively shifting capital allocation toward intelligent spraying fleets capable of reducing input waste, improving crop monitoring accuracy, and optimizing field-level decision-making in real time.

The market is simultaneously being reshaped by supply chain regionalization and digital agriculture mandates introduced across Asia-Pacific, Europe, and North America between 2024 and 2026. AI-enabled autonomous spraying technology improves operational efficiency by 36% while reducing chemical application costs by nearly 29% compared to legacy tractor-based spraying systems. Asia-Pacific leads in deployment volume with approximately 48% of global operational drone activity, while North America leads in precision software integration and autonomous farm analytics adoption with nearly 33% higher smart-farm penetration rates among large commercial growers.

Within the next two to three years, automated route optimization and fleet-coordination software are expected to reduce crop treatment turnaround times by over 40%, significantly improving seasonal yield protection cycles. ESG positioning has also become a measurable competitive advantage, as drone-enabled low-drift spraying systems reduce pesticide leakage by approximately 27%, helping agribusinesses comply with tightening environmental standards while lowering operational waste costs.

A strong execution-level example emerged in China’s rice cultivation sector, where coordinated drone spraying programs improved spraying accuracy by 35% and reduced water consumption by nearly 30% across large agricultural zones. Simultaneously, major agricultural technology companies are accelerating partnerships with battery manufacturers, AI firms, and smart farming platforms to strengthen vertically integrated precision agriculture ecosystems. The competitive landscape is now shifting from standalone drone hardware toward intelligent agricultural automation platforms that combine AI analytics, autonomous mobility, and cloud-based crop management systems. Companies capable of optimizing scalability, compliance efficiency, and precision execution are positioning themselves to dominate the next generation of global agricultural productivity transformation.

The Agricultural Intelligent Plant Protection Drone Market is undergoing rapid structural transformation as precision agriculture shifts from experimental deployment toward mainstream commercial execution. Increasing pressure to improve crop productivity while reducing chemical waste is accelerating the integration of AI-powered aerial spraying systems across large-scale farming operations. Commercial farms are increasingly prioritizing automated route planning, multispectral crop analysis, and low-drift spraying technologies to optimize resource utilization and improve field efficiency. Nearly 46% of high-volume agricultural enterprises now integrate drone-assisted crop monitoring into seasonal farm management operations. Simultaneously, tightening environmental regulations, rising labor shortages, and growing fuel costs are forcing agricultural operators to replace conventional spraying equipment with autonomous drone fleets capable of improving operational precision by over 30%. Strategic competition is intensifying as manufacturers expand battery capacity, payload performance, and intelligent navigation capabilities to strengthen long-term scalability across global precision farming ecosystems.

Precision agriculture adoption is becoming the primary structural growth engine accelerating deployment of Agricultural Intelligent Plant Protection Drone systems across global farming operations. AI-powered crop spraying platforms are improving pesticide utilization efficiency by nearly 28% while reducing field labor dependency by more than 30%, creating measurable economic advantages for commercial growers. Rising agricultural labor shortages across Asia-Pacific and North America, combined with tightening environmental controls on chemical spraying, are forcing rapid operational transformation toward automated crop protection technologies. Large-scale cereal and grain producers now account for approximately 46% of drone-assisted spraying demand due to high acreage scalability and seasonal productivity pressure. Global agricultural supply chain restructuring following fertilizer price volatility and climate-driven crop risks has further accelerated investment in autonomous spraying fleets capable of optimizing crop input management in real time. Companies are responding through aggressive production expansion, AI software integration, and strategic partnerships with smart farming platforms. Several manufacturers have increased battery endurance capacity by over 22% while integrating cloud-based analytics to strengthen precision decision-making across high-volume agricultural operations.

Despite accelerating adoption, infrastructure limitations and operational cost barriers continue constraining scalable deployment of Agricultural Intelligent Plant Protection Drone systems across several emerging agricultural economies. High-performance agricultural drones still carry operational costs approximately 35% higher than conventional spraying equipment in small-scale farming environments, limiting affordability for fragmented agricultural sectors. Battery dependency and charging infrastructure gaps also remain critical execution barriers, particularly across rural farming regions with inconsistent energy access and weak digital connectivity infrastructure. Regulatory fragmentation is further slowing cross-border scalability, as flight authorization frameworks and aerial spraying compliance standards differ significantly across North America, Europe, and Asia-Pacific markets. Nearly 29% of commercial agricultural operators cite certification complexity and operational licensing delays as major deployment obstacles. Supply concentration in advanced semiconductors, navigation systems, and lithium battery components also exposes manufacturers to geopolitical trade risks and component price volatility. In response, companies are diversifying supplier networks, accelerating localized manufacturing initiatives, and investing in hybrid power systems to reduce long-term dependency on constrained battery supply ecosystems.

The convergence of AI analytics, autonomous mobility systems, and cloud-connected farm management platforms is unlocking significant expansion opportunities across the Agricultural Intelligent Plant Protection Drone Market. Intelligent drone ecosystems capable of real-time crop disease detection and precision spraying are improving field productivity by nearly 33% while reducing excess chemical application by over 25%. This operational advantage is rapidly reshaping demand across high-value crops including vineyards, orchards, and specialty horticulture farms where precision execution directly impacts profitability. Emerging markets across Southeast Asia, Latin America, and the Middle East are increasingly investing in drone-enabled smart farming infrastructure to strengthen food security and agricultural efficiency. AI-driven predictive crop analysis platforms are also accelerating adoption of subscription-based agricultural drone services, creating new recurring-revenue business models beyond hardware sales. Companies are strategically expanding R&D investment into swarm-drone coordination, hydrogen-powered aerial systems, and automated charging infrastructure to capture next-generation scalability advantages. A particularly strong future signal is the growing integration of drones with satellite imaging and IoT-based irrigation systems, redefining fully connected precision agriculture ecosystems.

Operational scalability remains one of the most significant long-term challenges constraining consistent expansion across the Agricultural Intelligent Plant Protection Drone Market. Large agricultural deployments require high battery endurance, real-time connectivity, advanced route optimization, and highly trained operators, yet nearly 31% of commercial farms still lack sufficient digital infrastructure to support full-scale autonomous operations. Payload limitations also continue affecting spraying consistency across large-acreage farmland, particularly in high-wind and uneven terrain conditions where precision accuracy becomes operationally critical. Regulatory tightening surrounding aerial pesticide spraying and autonomous flight safety standards is further increasing compliance complexity across developed markets. Several agricultural operators now face approval timelines exceeding 20% longer than traditional mechanized spraying systems due to evolving aviation and environmental oversight requirements. Rising component costs tied to semiconductor and lithium supply concentration are also pressuring manufacturing scalability and long-term pricing competitiveness. To remain competitive, companies must accelerate investment into battery innovation, autonomous fleet coordination software, operator training ecosystems, and strategic partnerships with agricultural technology providers capable of strengthening deployment efficiency across large-scale precision farming networks.

Precision spraying deployment expanded 34% across commercial farms in 2025 as AI-driven route optimization reduced pesticide overlap by 26% and improved field coverage speed by 31%. Agricultural operators are increasingly replacing tractor-based crop protection systems with autonomous aerial fleets to reduce labor dependency and chemical waste. Companies are rapidly scaling software-integrated spraying platforms while partnering with farm analytics providers to optimize execution-level efficiency across large-acreage cultivation zones.

Battery endurance improvements exceeded 22% while automated charging infrastructure installations increased 29%, reshaping operational scalability across high-volume agricultural regions. Manufacturers are prioritizing fast-swap battery systems and intelligent power management to support longer spraying cycles and reduce downtime during peak farming seasons. Supply chain localization efforts across Asia-Pacific are also accelerating drone component manufacturing to stabilize production efficiency amid ongoing semiconductor sourcing pressure.

Multispectral imaging adoption rose 37% as precision crop monitoring shifted from seasonal assessment toward real-time predictive analytics deployment. Agricultural enterprises are integrating drone-generated crop intelligence with cloud-based farm management platforms to improve disease detection accuracy and optimize fertilizer application. Companies are restructuring product portfolios toward AI-enabled analytics ecosystems rather than standalone drone hardware, redefining competition around data-driven agricultural automation capabilities.

Subscription-based drone service models expanded 28% globally as mid-sized farms prioritized operational flexibility over direct equipment ownership. Agricultural cooperatives and service providers are increasingly deploying shared autonomous drone fleets to lower capital expenditure barriers and accelerate regional penetration. This shift is forcing manufacturers to reposition toward long-term ecosystem management, software licensing, and fleet maintenance partnerships while responding to rising regulatory compliance requirements around precision spraying operations.

The Agricultural Intelligent Plant Protection Drone Market is segmented by type, application, and end-user, reflecting shifting demand patterns across precision agriculture ecosystems. Demand remains heavily concentrated in autonomous multi-rotor drone systems due to their operational flexibility, while fixed-wing platforms are gaining traction in large-acreage commercial farming applications. Crop spraying continues dominating application demand with nearly 52% market concentration, supported by rising pressure to reduce pesticide waste and optimize field productivity. Commercial agribusinesses account for the largest end-user share as large-scale farming operations increasingly prioritize automated crop protection and AI-driven field monitoring. Demand is steadily shifting toward integrated drone ecosystems capable of combining spraying, imaging, and predictive crop analytics within unified precision farming operations. Companies are responding through specialized platform development, software integration, and scalable deployment strategies targeting both high-volume agriculture and emerging smart farming markets.

Multi-rotor agricultural drones continue dominating the Agricultural Intelligent Plant Protection Drone Market with approximately 58% market share due to superior maneuverability, precision spraying capability, and compatibility with complex crop environments including orchards, rice fields, and vineyards. Their ability to perform low-altitude autonomous operations while reducing pesticide drift by nearly 27% makes them structurally advantageous for high-precision agricultural applications. Fixed-wing drones are emerging as the fastest-growing segment, expanding deployment activity by nearly 24% due to their extended flight endurance and ability to cover large-scale farmland more efficiently than traditional rotary systems. Compared to fixed-wing systems, hybrid VTOL drone platforms are gaining traction across commercial agribusinesses seeking balanced endurance and operational flexibility. These advanced systems currently account for nearly 18% of market demand and are increasingly preferred for large multi-crop agricultural operations requiring both vertical mobility and broader field coverage. Remaining drone types collectively contribute approximately 24% share, serving specialized crop monitoring and localized spraying functions. Companies are strategically prioritizing payload optimization, AI-assisted navigation, and battery scalability to strengthen operational performance and capture expanding demand across precision farming ecosystems.

Crop spraying remains the leading application segment in the Agricultural Intelligent Plant Protection Drone Market, accounting for nearly 52% of total deployment demand due to rising pressure to reduce chemical waste, improve field precision, and accelerate treatment cycles across large-scale farming operations. Commercial cereal, rice, and cotton cultivation continue driving heavy utilization as autonomous spraying systems improve operational productivity by over 32% compared to conventional ground spraying methods. Crop monitoring and multispectral imaging applications are emerging as the fastest-growing segment, expanding adoption by approximately 26% as agricultural enterprises increasingly prioritize predictive analytics and early disease detection capabilities. Compared to mature spraying operations, crop surveillance applications are shifting demand toward AI-enabled analytics platforms capable of integrating real-time imaging with cloud-based farm management systems. Precision seeding and fertilizer distribution collectively account for approximately 29% of market activity, supported by growing interest in fully integrated autonomous farming ecosystems. Companies are aggressively repositioning product strategies toward multifunctional drone platforms combining spraying, monitoring, and analytics capabilities to strengthen recurring software revenue and long-term ecosystem control across precision agriculture markets.

Large commercial farming enterprises dominate the Agricultural Intelligent Plant Protection Drone Market with approximately 49% demand share due to extensive acreage management requirements, high operational intensity, and stronger investment capacity for precision agriculture technologies. These enterprises increasingly prioritize AI-powered autonomous spraying fleets to optimize seasonal productivity, reduce labor dependency, and strengthen field-level decision-making efficiency. Agricultural cooperatives are emerging as the fastest-growing end-user segment, expanding adoption rates by nearly 23% as shared drone-service models lower capital investment barriers for mid-sized and regional farming operations. Compared to individual farm operators, agribusiness corporations demonstrate higher adoption intensity due to integrated digital infrastructure and stronger scalability requirements across multiple crop regions. Government-backed agricultural programs, research institutions, and drone service providers collectively contribute approximately 34% of market demand, particularly across emerging smart agriculture ecosystems in Asia-Pacific and Latin America. Companies are targeting these segments through subscription-based deployment models, customized spraying platforms, and long-term software integration partnerships designed to accelerate ecosystem penetration and recurring operational revenue generation.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

Asia-Pacific dominates global Agricultural Intelligent Plant Protection Drone Market demand due to strong manufacturing capacity, large-scale agricultural deployment, and aggressive smart farming expansion across China, Japan, and India. North America holds approximately 26% market share and leads in AI-powered precision agriculture integration, autonomous farm analytics, and software-driven drone ecosystems. Europe contributes nearly 18% share, driven by environmental compliance mandates and sustainable crop protection initiatives focused on reducing chemical drift and pesticide waste. South America and the Middle East & Africa collectively account for 8% market participation, supported by growing commercial agriculture modernization and infrastructure investment. Global supply chain localization, battery manufacturing expansion, and precision agriculture policy incentives are increasingly forcing companies to prioritize Asia-Pacific for scale while targeting North America and Europe for technology-driven premium agricultural automation deployment.

North America represents approximately 26% of the global Agricultural Intelligent Plant Protection Drone Market, driven by large-scale commercial farming operations and rapid adoption of AI-enabled precision agriculture systems. The United States dominates regional demand due to high deployment across corn, soybean, and wheat cultivation zones where autonomous spraying improves field productivity by nearly 34%. Rising agricultural labor shortages and stricter environmental controls on pesticide application are accelerating investment in intelligent aerial spraying technologies. Commercial agribusinesses increasingly prioritize cloud-connected drone ecosystems integrated with predictive crop analytics and automated farm management systems. Drone-assisted crop monitoring deployment expanded by approximately 29% across large farming enterprises during the last two years. Companies are expanding regional partnerships, software integration capabilities, and autonomous fleet deployment infrastructure, positioning North America as a strategic hub for high-value precision agriculture innovation and premium technology adoption.

Europe accounts for nearly 18% of the global Agricultural Intelligent Plant Protection Drone Market, supported by strong regulatory pressure surrounding pesticide reduction, environmental sustainability, and precision agriculture modernization. Germany, France, and the Netherlands continue leading regional deployment due to aggressive adoption of low-drift spraying systems and AI-driven crop monitoring technologies. Environmental compliance initiatives targeting nearly 50% reduction in chemical pesticide usage are accelerating demand for intelligent drone-assisted spraying operations. Precision agriculture deployment across commercial farming operations increased by approximately 24%, particularly in high-value horticulture and vineyard cultivation sectors. Agricultural enterprises increasingly favor data-driven crop protection systems capable of optimizing chemical application accuracy and improving ESG compliance performance. Companies are accelerating R&D investment into autonomous flight safety systems, multispectral analytics, and eco-efficient spraying technologies to remain competitive in Europe’s highly regulated agricultural ecosystem.

Asia-Pacific leads the global Agricultural Intelligent Plant Protection Drone Market with approximately 48% market share, supported by large agricultural economies, advanced drone manufacturing ecosystems, and aggressive precision farming expansion. China remains the dominant regional market, while Japan and India are accelerating deployment across rice, wheat, and specialty crop cultivation. The region benefits from strong localized manufacturing capabilities that reduce production costs by nearly 21% compared to Western markets. Autonomous crop spraying deployment expanded by over 36% across commercial agricultural operations as governments intensified smart agriculture modernization initiatives between 2024 and 2026. Regional manufacturers are aggressively scaling battery production, AI navigation systems, and export-focused drone assembly infrastructure. Agricultural enterprises prioritize operational speed, scalability, and affordability, making Asia-Pacific the most critical global region for mass deployment, manufacturing expansion, and long-term precision agriculture ecosystem growth.

South America contributes approximately 5% of the global Agricultural Intelligent Plant Protection Drone Market, led primarily by Brazil and Argentina where large-scale soybean, sugarcane, and corn cultivation is driving precision spraying demand. Commercial farming enterprises are increasingly adopting autonomous crop protection systems to improve operational efficiency and reduce seasonal labor dependency. Precision spraying deployment improved agricultural productivity by nearly 27% across several high-volume farming regions. However, infrastructure limitations, uneven rural connectivity, and high equipment import costs continue constraining broader scalability across smaller agricultural operators. Agricultural drone service providers are responding through shared deployment models and localized maintenance partnerships designed to lower operational barriers. Regional enterprises remain highly price-sensitive but increasingly prioritize scalable automation technologies capable of improving crop yield consistency and reducing pesticide waste across export-driven agricultural production networks.

The Middle East & Africa region accounts for nearly 3% of the global Agricultural Intelligent Plant Protection Drone Market, supported by growing investment in agricultural modernization, food security programs, and water-efficient farming infrastructure. Countries including the UAE, Saudi Arabia, and South Africa are accelerating adoption of AI-assisted crop monitoring and precision spraying technologies to optimize agricultural productivity under resource-constrained conditions. Smart irrigation-linked drone deployment improved water utilization efficiency by approximately 25% across controlled farming projects. Governments and agribusiness operators are increasingly investing in precision agriculture partnerships, localized pilot programs, and autonomous farming infrastructure expansion. Agricultural enterprises prioritize operational efficiency, climate adaptability, and long-term sustainability as rising food import dependency intensifies regional modernization efforts. The region is emerging as a strategic growth market for advanced agricultural technology deployment and smart farming transformation initiatives.

China – 41% Market share: Dominates due to massive agricultural drone manufacturing capacity, extensive precision farming deployment, and strong government-backed smart agriculture initiatives.

United States – 19% Market share: Leads through advanced AI-powered precision agriculture adoption, large-scale commercial farming operations, and rapid integration of autonomous crop management technologies.

The Agricultural Intelligent Plant Protection Drone Market is dominated by aggressive competition between global drone technology leaders such as DJI, XAG, Yamaha Motor, EAVision, and Parrot, alongside rapidly scaling regional precision agriculture specialists focused on low-cost deployment models. The top five players collectively control approximately 68% of global market share, with Chinese manufacturers maintaining strong dominance through manufacturing scale, battery integration, and supply chain control. DJI and XAG compete primarily on autonomous navigation accuracy and payload performance, while regional players focus on pricing flexibility and localized agricultural customization.

Technology capability has become the primary competitive differentiator, with AI-enabled route optimization improving spraying efficiency by nearly 32% and reducing chemical drift by approximately 27%. Companies are also competing through faster deployment cycles, integrated software ecosystems, and strategic partnerships with precision farming platforms. Battery endurance improvements exceeding 22% and automated fleet coordination systems are redefining operational scalability advantages.

The market is now shifting from standalone drone hardware toward vertically integrated agricultural automation ecosystems combining AI analytics, cloud-based crop intelligence, and autonomous spraying infrastructure. High regulatory compliance requirements, advanced software integration costs, and semiconductor dependency continue creating strong entry barriers. Winning in this market increasingly requires scalable manufacturing, intelligent automation capabilities, localized service infrastructure, and full precision agriculture ecosystem integration rather than hardware-only competition.

XAG

Yamaha Motor Co., Ltd.

EAVision Technologies

Parrot SA

AeroVironment Inc.

AgEagle Aerial Systems Inc.

Hylio Inc.

MMC UAV

Delair

SZ DJI Technology Agriculture Division

American Robotics

Trimble Inc.

senseFly

Artificial intelligence, autonomous navigation, and multispectral imaging technologies are rapidly redefining the Agricultural Intelligent Plant Protection Drone Market. AI-powered spraying algorithms are improving route precision by nearly 34% while reducing pesticide overlap by approximately 26%, significantly lowering operational waste across large-scale farming operations. Nearly 48% of newly deployed agricultural drones now integrate real-time crop analytics and automated obstacle avoidance systems, strengthening precision agriculture execution at commercial scale.

The market is also witnessing rapid integration of multispectral imaging, LiDAR mapping, and cloud-connected farm management platforms. Compared to conventional GPS-guided spraying systems, AI-assisted autonomous drones improve crop monitoring accuracy by over 31% while reducing field inspection time by nearly 40%. This transition is giving large agribusinesses and precision farming service providers a major competitive advantage through faster decision-making and lower labor dependency. Companies focused on integrated software ecosystems are increasingly outperforming hardware-only manufacturers in long-term customer retention.

Battery innovation and intelligent fleet coordination are emerging as the next disruptive technologies shaping operational scalability. Advanced lithium battery systems have improved flight endurance by approximately 22%, while swarm-drone coordination technologies are optimizing simultaneous multi-field spraying operations. Between 2026 and 2028, hydrogen-assisted power systems, autonomous charging hubs, and predictive crop-disease AI models are expected to accelerate deployment across high-volume agricultural economies.

Technology leadership is increasingly shifting toward companies capable of combining autonomous flight systems, AI analytics, and cloud-based agricultural intelligence into fully integrated smart farming ecosystems. Early adopters are gaining measurable operational advantages in productivity, compliance efficiency, and large-scale agricultural automation execution.

July 2025 – DJI launched the Agras T100, T70P, and T25P agricultural drones globally with payload capacities reaching 100L spraying and 150L spreading capabilities, improving operational efficiency for large-scale farms. The launch strengthened DJI’s position in autonomous precision agriculture expansion across global commercial farming markets. [Payload Expansion] Source: www.dji.com

April 2024 – DJI introduced the Agras T50 and T25 drone platforms integrated with the upgraded SmartFarm application, supporting treatment across over 980 million acres globally and improving aerial crop protection execution efficiency. The development accelerated intelligent farm management adoption among commercial agricultural enterprises. [SmartFarm Integration]

March 2026 – China expanded deployment to over 300,000 agricultural drones operating across more than 460 million mu of farmland annually, reinforcing large-scale smart agriculture modernization. The expansion significantly strengthened precision farming infrastructure and accelerated autonomous crop protection implementation nationwide. [Scale Modernization]

July 2025 – DJI confirmed nearly 500,000 trained agricultural drone operators globally during the launch of its next-generation Agras systems, highlighting rapid workforce scaling in precision agriculture automation. The expansion improved operational deployment readiness and accelerated adoption across emerging agricultural technology markets. [Operator Ecosystem]

The Agricultural Intelligent Plant Protection Drone Market Report delivers comprehensive coverage of precision agriculture technologies, autonomous crop protection systems, and intelligent drone deployment ecosystems across global farming industries. The report evaluates market segmentation by drone type, application, and end-user categories, covering multi-rotor, fixed-wing, and hybrid drone platforms alongside crop spraying, monitoring, imaging, and precision seeding applications. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed assessment of regional deployment trends, manufacturing concentration, and operational adoption dynamics.

The report provides deep analytical evaluation of over 10 major industry participants, highlighting competitive positioning, technology integration strategies, operational scalability trends, and ecosystem expansion initiatives. More than 48% of global deployment activity analyzed in the report is concentrated within large-scale commercial agriculture operations, while approximately 29% of emerging adoption is linked to AI-enabled crop monitoring and autonomous spraying ecosystems. Advanced technologies including multispectral imaging, AI navigation, LiDAR mapping, and cloud-connected precision agriculture platforms are examined extensively.

The report also delivers forward-looking strategic coverage for 2026–2033, focusing on autonomous fleet coordination, hydrogen-assisted drone systems, smart agriculture infrastructure expansion, and evolving regulatory frameworks. It supports investment planning, market expansion, partnership evaluation, competitive benchmarking, and long-term precision agriculture positioning for technology providers, agribusiness operators, investors, and agricultural automation stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 120.0 Million |

| Market Revenue (2033) | USD 307.9 Million |

| CAGR (2026–2033) | 12.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DJI; XAG; Yamaha Motor Co., Ltd.; EAVision Technologies; Parrot SA; AeroVironment Inc.; AgEagle Aerial Systems Inc.; Hylio Inc.; MMC UAV; Delair; SZ DJI Technology Agriculture Division; American Robotics; Trimble Inc.; senseFly |

| Customization & Pricing | Available on Request (10% Customization Free) |