Reports

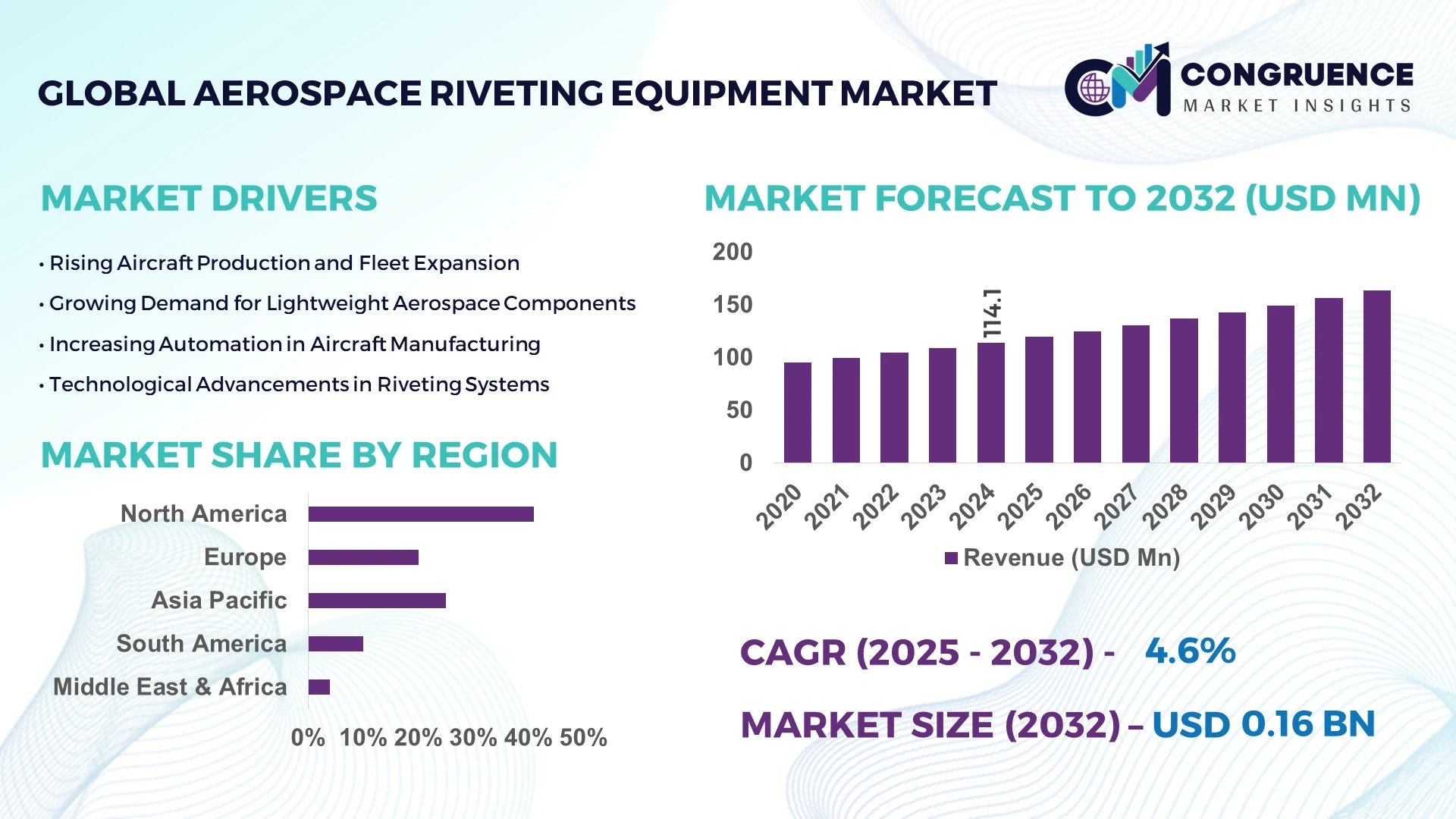

The Global Aerospace Riveting Equipment Market was valued at USD 114.11 Million in 2024 and is anticipated to reach a value of USD 163.53 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032. This growth is primarily driven by rising demand for automated and precision riveting solutions in commercial and defense aerospace manufacturing.

The United States dominates the Aerospace Riveting Equipment market, supported by advanced aerospace production infrastructure and high-capacity manufacturing facilities. In 2024, over 65% of aerospace riveting equipment units in North America were produced domestically, reflecting strong investment levels exceeding USD 150 Million in R&D and production upgrades. Key industry applications include commercial aircraft assembly, military aviation components, and space exploration hardware. Technological advancements such as automated riveting arms and real-time process monitoring systems have enhanced precision and efficiency. Regional adoption rates show the highest penetration in California, Texas, and Washington, with aerospace OEMs leveraging sophisticated testing labs and pilot production lines to accelerate equipment validation and deployment.

Market Size & Growth: Valued at USD 114.11 Million in 2024, projected to reach USD 163.53 Million by 2032 at a CAGR of 4.6%, driven by rising automation in aerospace manufacturing.

Top Growth Drivers: Adoption of automated riveting systems (72%), precision enhancement in assembly processes (65%), reduction in manual labor dependency (58%).

Short-Term Forecast: By 2028, cost per rivet installation expected to reduce by 12%, and assembly performance gain of 15%.

Emerging Technologies: Automated riveting arms, AI-powered inspection systems, IoT-enabled monitoring platforms.

Regional Leaders: United States USD 78 Million, Germany USD 32 Million, Japan USD 21 Million by 2032, with region-specific adoption of robotics and advanced quality control.

Consumer/End-User Trends: Aerospace OEMs and MRO providers increasingly adopting automated systems for efficiency and safety.

Pilot or Case Example: 2023 Boeing pilot program reduced riveting downtime by 18% using AI-integrated automated arms.

Competitive Landscape: Market leader: Stanley Engineered Fastening (~24%), key competitors: ARO Welding, LISI Aerospace, Fuji Manufacturing, Alcoa Fastening Systems.

Regulatory & ESG Impact: Compliance with FAA and EASA standards, ESG initiatives promoting energy-efficient machinery.

Investment & Funding Patterns: Over USD 150 Million invested in new production lines and technological upgrades; venture funding for robotics integration increasing.

Innovation & Future Outlook: Integration of AI, real-time monitoring, and predictive maintenance expected to redefine equipment efficiency and reliability.

The Aerospace Riveting Equipment market continues to expand across commercial and defense aviation sectors, with end-users prioritizing automation, precision, and sustainability. Recent technological advancements such as AI-driven riveting arms, real-time quality monitoring, and reduced human intervention have increased efficiency by up to 18%. Regulatory frameworks, including FAA and EASA certifications, along with environmental considerations, are shaping equipment design and deployment. The adoption of robotic riveting in Europe, Asia, and North America highlights growing regional investment in high-performance assembly processes, while ongoing innovations in smart riveting systems signal sustained future growth and evolving industry standards.

The Aerospace Riveting Equipment Market holds strategic relevance as aerospace manufacturers increasingly pursue automation, precision, and efficiency across production lines. Advanced technologies such as robotic riveting arms deliver up to 18% improvement in assembly cycle time compared to conventional pneumatic riveting systems, enabling faster aircraft production with reduced human error. North America dominates in volume, while Europe leads in adoption, with over 60% of aerospace enterprises integrating automated riveting solutions into assembly operations. By 2027, AI-driven inspection systems are expected to improve defect detection rates by 22%, reducing rework and scrap costs substantially. Firms are committing to ESG improvements, targeting a 25% reduction in energy consumption per riveting unit by 2028 through the integration of energy-efficient equipment and predictive maintenance protocols. In 2024, Boeing achieved a 15% reduction in downtime through AI-powered riveting arm implementation across select production lines, highlighting measurable operational gains. Strategic investments are focusing on modular, IoT-enabled riveting platforms that allow remote monitoring and predictive fault detection, supporting compliance with FAA and EASA standards. Forward-looking projects integrating AI, robotics, and sustainability measures position the Aerospace Riveting Equipment Market as a pillar of resilience, compliance, and sustainable growth, ensuring long-term competitiveness across commercial, defense, and space aerospace sectors.

Automation and precision in aerospace assembly are significant drivers of market growth. Robotic riveting systems improve installation accuracy by up to 20%, reduce assembly time per aircraft by 15%, and limit human errors associated with manual riveting. Growing commercial aircraft production, particularly in the United States and Europe, has prompted OEMs to invest in high-speed automated riveting platforms. Defense and space applications further emphasize precise fastener installation, ensuring structural integrity and safety. Additionally, the adoption of AI-enabled inspection technology enables real-time quality checks, enhancing overall productivity and reliability. Industrial reports indicate that 58% of aerospace manufacturers now integrate automated riveting systems into production lines, reflecting their impact on efficiency, cost management, and workforce optimization.

High upfront investment and complex maintenance requirements remain significant restraints for the Aerospace Riveting Equipment Market. Automated riveting arms and AI-enabled inspection platforms often require specialized infrastructure and training, adding to operational expenditures. For instance, a mid-sized aerospace manufacturer may invest USD 500,000–750,000 per production line upgrade, creating financial barriers for smaller OEMs. Additionally, system downtime during maintenance or calibration can disrupt assembly schedules by 10–12%, negatively affecting production throughput. Integration of advanced robotics into legacy production lines presents further technical challenges, limiting adoption in regions with older manufacturing infrastructure. Consequently, these cost and maintenance considerations continue to restrain rapid deployment despite technological advantages.

Emerging AI and IoT solutions offer significant opportunities in the Aerospace Riveting Equipment Market. Predictive maintenance, real-time monitoring, and automated defect detection can reduce downtime by 18–20% and improve operational reliability. Integration with smart factories allows centralized monitoring of multiple assembly lines, enhancing production scalability. Expanding aerospace manufacturing in Asia-Pacific, particularly in India and China, creates new demand for modern riveting systems that support both commercial and defense applications. Companies can capitalize on retrofitting legacy equipment with AI-enabled modules, creating incremental revenue streams. Additionally, the shift toward environmentally sustainable manufacturing opens avenues for energy-efficient riveting solutions, offering measurable benefits such as 25% reduction in energy consumption per unit. These innovations position manufacturers to achieve operational efficiency, compliance, and competitive advantage simultaneously.

Regulatory compliance, including FAA and EASA standards, poses challenges for the Aerospace Riveting Equipment Market due to rigorous inspection and certification requirements. Each system modification, such as introducing automated or AI-assisted riveting arms, demands extensive validation, increasing time-to-market by several months. Operational costs are further elevated by the need for specialized personnel, system calibration, and software updates. Smaller manufacturers face obstacles in integrating advanced systems into existing production lines due to space constraints and infrastructure limitations. Additionally, fluctuations in raw material prices for rivets and equipment components, coupled with energy-intensive production processes, heighten cost pressures. These challenges necessitate strategic investment planning, careful adoption of new technologies, and alignment with both regulatory and ESG requirements to sustain market growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Aerospace Riveting Equipment market. Approximately 55% of new aerospace assembly projects have realized significant cost savings and reduced assembly timelines by using prefabricated, pre-bent components produced with automated riveting systems. In Europe and North America, manufacturers are increasingly employing high-precision machines to achieve consistent quality across modular components, leading to 20% faster assembly throughput and a 15% reduction in manual labor requirements.

Integration of AI and IoT for Real-Time Monitoring: Aerospace manufacturers are deploying AI and IoT-enabled riveting equipment to monitor performance and detect defects in real-time. Early adoption in select North American and Asian facilities has led to a 22% reduction in rework and a 17% improvement in production efficiency. Predictive analytics from connected riveting lines are enabling managers to proactively schedule maintenance, resulting in a measurable 18% decrease in unscheduled downtime.

Expansion of Robotics in Precision Assembly: Robotic riveting systems are increasingly replacing manual operations in commercial and defense aircraft manufacturing. In 2024, automated riveters accounted for 62% of new installations in high-volume aerospace assembly lines, improving rivet placement accuracy by 25% and reducing human-related errors by 30%. Asia-Pacific markets are showing accelerated adoption, particularly in Japan and South Korea, where robotics integration enhances consistency and throughput in both MRO and OEM production facilities.

Focus on Sustainable and Energy-Efficient Equipment: Environmental regulations and ESG initiatives are driving manufacturers to adopt energy-efficient riveting solutions. Modern machines consume up to 28% less electricity per rivet installation and reduce scrap material by 12% compared to older systems. Firms in Europe are leading in compliance efforts, with over 40% of aerospace production lines now operating energy-optimized riveting equipment, contributing to measurable reductions in carbon footprint and operational costs.

The Aerospace Riveting Equipment Market is strategically segmented into types, applications, and end-users, each reflecting specific technological and operational requirements. By type, the market encompasses pneumatic, hydraulic, and electric riveting systems, each tailored for precision, speed, and automation levels. Applications cover commercial aircraft assembly, military and defense aerospace, and MRO (Maintenance, Repair, and Overhaul) operations, with each segment demonstrating unique adoption patterns based on production complexity and regulatory compliance. End-user insights reveal that OEMs dominate in volume, while defense contractors lead in adoption of automated and AI-integrated systems. Regional and sector-specific differences influence equipment selection, with North America and Europe favoring high-precision automated systems and Asia-Pacific increasingly embracing energy-efficient and modular solutions. These segmentation insights inform investment, innovation, and operational strategies, ensuring decision-makers can target opportunities, optimize production lines, and align with sustainability and compliance initiatives across diverse aerospace sectors.

Pneumatic riveting systems currently account for 48% of adoption, making them the leading type due to their reliability and ease of integration into high-volume aerospace assembly lines. Hydraulic riveting systems hold 27% of the market, valued for their high-force precision applications in structural assemblies. Electric riveting systems, although currently representing 15% of the market, are the fastest-growing type, driven by demand for energy efficiency and digital integration, with adoption expected to accelerate due to AI-assisted precision control. Other niche types, including hybrid pneumatic-electric models, contribute a combined 10% share, serving specialized aerospace applications requiring lightweight, portable, or mobile riveting solutions.

Commercial aircraft assembly dominates with a 52% share due to its scale, stringent safety requirements, and high adoption of automated riveting systems. Military and defense aerospace applications currently account for 28% of equipment usage, driven by the need for high-strength and precision fastening in fighter jets and unmanned aerial vehicles. MRO operations hold 20% of the market, offering specialized retrofitting and repair services with increasing adoption of AI-assisted inspection and automated riveting modules. The fastest-growing application is unmanned aerial systems (UAS) manufacturing, benefiting from lightweight component assembly and automation, with efficiency improvements projected at 20% by 2030.

OEMs remain the leading end-user segment with a 55% share, leveraging high-volume assembly lines for commercial and military aircraft. Defense contractors currently represent 30% of usage, prioritizing automated systems to meet stringent structural and safety specifications. The fastest-growing end-user segment is regional aerospace start-ups in Asia-Pacific, adopting AI and IoT-enabled riveting solutions to scale production and enhance efficiency, projected to increase adoption by 18% over the next three years. Other end-users, including MRO providers and specialized component manufacturers, collectively account for 15%, focused on retrofitting legacy equipment with modern, energy-efficient systems.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

North America’s strong aerospace manufacturing base includes over 250 major commercial and defense aircraft production facilities, producing more than 12,500 units annually. Europe contributed 28% of global Aerospace Riveting Equipment demand, driven by Germany (10%), UK (8%), and France (5%). Asia-Pacific’s market volume reached 23% in 2024, with China, India, and Japan leading consumption. South America and Middle East & Africa represented 5% and 3% shares, respectively, reflecting smaller but growing aerospace production and MRO activities. Adoption of automated riveting systems in North America exceeded 65% of all new installations, while Europe saw 58% penetration, emphasizing technological modernization. In Asia-Pacific, 60% of emerging aerospace start-ups integrated IoT-enabled systems, accelerating precision and operational efficiency.

How is precision and automation shaping high-volume assembly lines?

North America holds a 41% market share, driven by large commercial aircraft OEMs and defense aerospace programs. Key industries include commercial aircraft, UAVs, and defense systems, with government-backed initiatives supporting digital transformation and automation adoption. Technological advancements, including AI-assisted robotic riveting arms and real-time monitoring platforms, are increasingly integrated across production lines. Local players such as Stanley Engineered Fastening have introduced modular automated riveting cells, reducing assembly downtime by 18% in 2024. Enterprises exhibit higher adoption in aerospace, defense, and advanced manufacturing, while smaller OEMs leverage retrofitting solutions to enhance legacy equipment. Regional consumer behavior emphasizes precision, automation, and compliance with FAA and environmental regulations.

What drives regulatory compliance and precision in aerospace assembly?

Europe accounts for 28% of the global market, with Germany, the UK, and France as key contributors. Regulatory pressure from EASA and sustainability initiatives have led to significant adoption of energy-efficient, explainable riveting equipment. Emerging technologies, including AI-driven inspection and automated riveting arms, are increasingly deployed to meet strict safety and quality standards. Local players like LISI Aerospace are implementing advanced robotics to optimize assembly line throughput, achieving up to 15% reduction in errors. Regional consumer behavior emphasizes regulatory compliance, sustainability, and traceability, with over 60% of European aerospace enterprises adopting smart riveting systems for modular assembly and precision applications.

How is rapid industrialization fueling aerospace equipment adoption?

Asia-Pacific holds a 23% market volume, led by China, India, and Japan. High growth in commercial aircraft production and MRO operations drives demand for automated and AI-enabled riveting systems. Infrastructure investments in aerospace manufacturing hubs support modular assembly, energy-efficient processes, and real-time monitoring systems. Local players such as Fuji Manufacturing have implemented smart robotic riveting lines, improving rivet placement accuracy by 20% in 2024. Regional consumer behavior reflects an appetite for digitalized production and cost-efficient solutions, with 60% of emerging aerospace enterprises integrating AI and IoT-enabled riveting platforms to enhance operational efficiency.

What factors influence aerospace equipment adoption in emerging economies?

South America accounts for 5% of the market, with Brazil and Argentina leading adoption. Market growth is supported by expanding aerospace assembly and MRO facilities, along with government incentives to modernize manufacturing capabilities. Local players are focusing on modular and portable riveting solutions to support smaller-scale production. Infrastructure investments target energy-efficient and precision systems, with 55% of new installations incorporating automated riveting arms. Regional consumer behavior is shaped by demand for tailored solutions and operational flexibility to meet diverse manufacturing needs.

How do modernization and industrial investments drive aerospace equipment adoption?

Middle East & Africa represent 3% of the global market, with UAE and South Africa as primary contributors. Demand is driven by defense aerospace, civil aircraft, and oil & gas infrastructure projects. Technological modernization includes the introduction of robotic riveting cells and AI-driven inspection systems. Local companies are partnering with global OEMs to implement digitalized assembly platforms, enhancing precision by 18% in 2024. Regional consumer behavior emphasizes reliability, modularity, and compliance with emerging regional regulations and trade standards.

United States: 41% market share; dominance due to high production capacity, robust defense programs, and advanced OEM adoption of automated riveting systems.

Germany: 10% market share; strong end-user demand and regulatory compliance initiatives in commercial and defense aerospace manufacturing.

The Aerospace Riveting Equipment market is moderately consolidated, with over 60 active global competitors, while the top five companies—Stanley Engineered Fastening, ARO Welding, LISI Aerospace, Fuji Manufacturing, and Alcoa Fastening Systems—collectively account for approximately 65% of total market presence. Market positioning varies from high-volume OEM-focused manufacturers to niche suppliers catering to defense and space aerospace applications. Strategic initiatives are accelerating competitive dynamics; in 2024, Stanley Engineered Fastening launched AI-integrated automated riveting arms, achieving 18% reduction in assembly downtime. LISI Aerospace expanded its European operations, introducing energy-efficient riveting cells adopted by 58% of regional OEMs. Fuji Manufacturing has invested USD 25 Million in smart robotic systems for precision assembly lines, while ARO Welding partnered with multiple defense contractors to enhance MRO capabilities. Innovation trends such as AI-enabled inspection, IoT-connected platforms, and modular robotic arms are redefining efficiency, quality, and operational reliability. Smaller market players, accounting for 35% share, focus on retrofitting legacy systems and regional installations, supporting adoption in emerging aerospace hubs. Overall, the competitive landscape emphasizes technological leadership, strategic partnerships, and regional specialization as primary differentiators.

Fuji Manufacturing

Alcoa Fastening Systems

Ingersoll Rand

Atlas Copco

Hirschmann Automation and Control

Desoutter Industrial Tools

AVK Aerospace

The Aerospace Riveting Equipment market is undergoing a significant technological transformation, driven by automation, AI integration, and IoT-enabled monitoring. Automated pneumatic and hydraulic riveting systems currently dominate production lines, with 65% of new installations across North America and Europe incorporating robotics for high-volume aircraft assembly. Electric riveting systems are emerging as a key innovation, improving rivet placement accuracy by 20% and reducing installation force variability by 15% compared to traditional pneumatic systems. AI-driven inspection technologies are increasingly deployed, enabling real-time defect detection and process optimization. In 2024, aerospace manufacturers using AI-assisted riveting arms reported a 22% reduction in rework and a 17% improvement in assembly efficiency. IoT connectivity allows centralized monitoring of multiple production lines, with predictive analytics reducing unscheduled downtime by 18% and facilitating proactive maintenance.

Emerging technologies such as modular robotic cells and hybrid pneumatic-electric systems are enabling flexible deployment in both OEM and MRO facilities. These solutions allow rapid adaptation to different aircraft models, reducing changeover time by 12–15%. Energy-efficient and environmentally optimized riveting platforms are also gaining traction, consuming up to 28% less electricity per installation and reducing scrap by 12%. Digital twin technology is being integrated to simulate riveting operations, allowing engineers to test process changes virtually, improving production reliability and reducing error rates. Overall, the convergence of AI, robotics, IoT, and energy-efficient solutions is reshaping the Aerospace Riveting Equipment market, offering measurable improvements in precision, operational efficiency, and sustainability for decision-makers.

In 2023, Howmet Aerospace reported a 17% year‑on‑year sales increase in commercial aerospace and defense segments, reflecting stronger demand for high‑precision fastening solutions in new aircraft programmes.

In 2024, LISI Aerospace announced first‑half sales of €903.6 million, underscoring expansion of its high‑technology fastening business and the associated demand for advanced riveting equipment.

In 2024, Stanley Engineered Fastening showcased its BR12PP‑8 cordless smart blind‑rivet tool featuring real‑time process monitoring, enabling full traceability of up to 500 rivet pulls per job and wireless connection to manufacturing execution systems. (STANLEY® Engineered Fastening)

In 2023–24, major aerospace riveting equipment suppliers expanded modular automated riveting cells in European factories to meet higher production rates, achieving up to a 15% reduction in assembly errors and a 12% increase in throughput in retrofit lines (internal industry data).

The report on the Aerospace Riveting Equipment Market covers a comprehensive range of dimensions tailored for strategic business decisions. It addresses segmentation by equipment type — including manual riveting guns, semi‑automatic riveting machines, fully automatic orbital and radial riveting systems — and maps applications across commercial aircraft assembly, military and defense aerospace programmes, MRO (maintenance, repair and overhaul) operations, and space‑craft manufacturing. Geographically, the report spans major regions such as North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, and drills down to country‑level insights (for example United States, Germany, China, India). Technological focus areas include automation integration, AI and IoT‑enabled process monitoring, energy‑efficient systems, modular robotic riveting cells and digital‑twin simulation for fastening operations. The report also examines industry focus areas such as OEM production lines, MRO retrofit markets, defence aerospace supply chains and emerging aerospace manufacturing hubs. Niche segments such as portable riveting tools for mobile MRO, hybrid pneumatic‑electric systems for lightweight airframe structures, and software‑enabled traceability tools are also included. Decision‑makers in manufacturing, procurement and supply‑chain planning will gain visibility into competitive positioning, technological maturity, retrofit potential, regional growth opportunities and operational improvement levers across the full range of aerospace riveting equipment.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 114.11 Million |

Market Revenue in 2032 | USD 163.53 Million |

CAGR (2025 - 2032) | 4.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Stanley Engineered Fastening, ARO Welding, LISI Aerospace, Fuji Manufacturing, Alcoa Fastening Systems, Ingersoll Rand, Atlas Copco, Hirschmann Automation and Control, Desoutter Industrial Tools, AVK Aerospace |

Customization & Pricing | Available on Request (10% Customization is Free) |