Reports

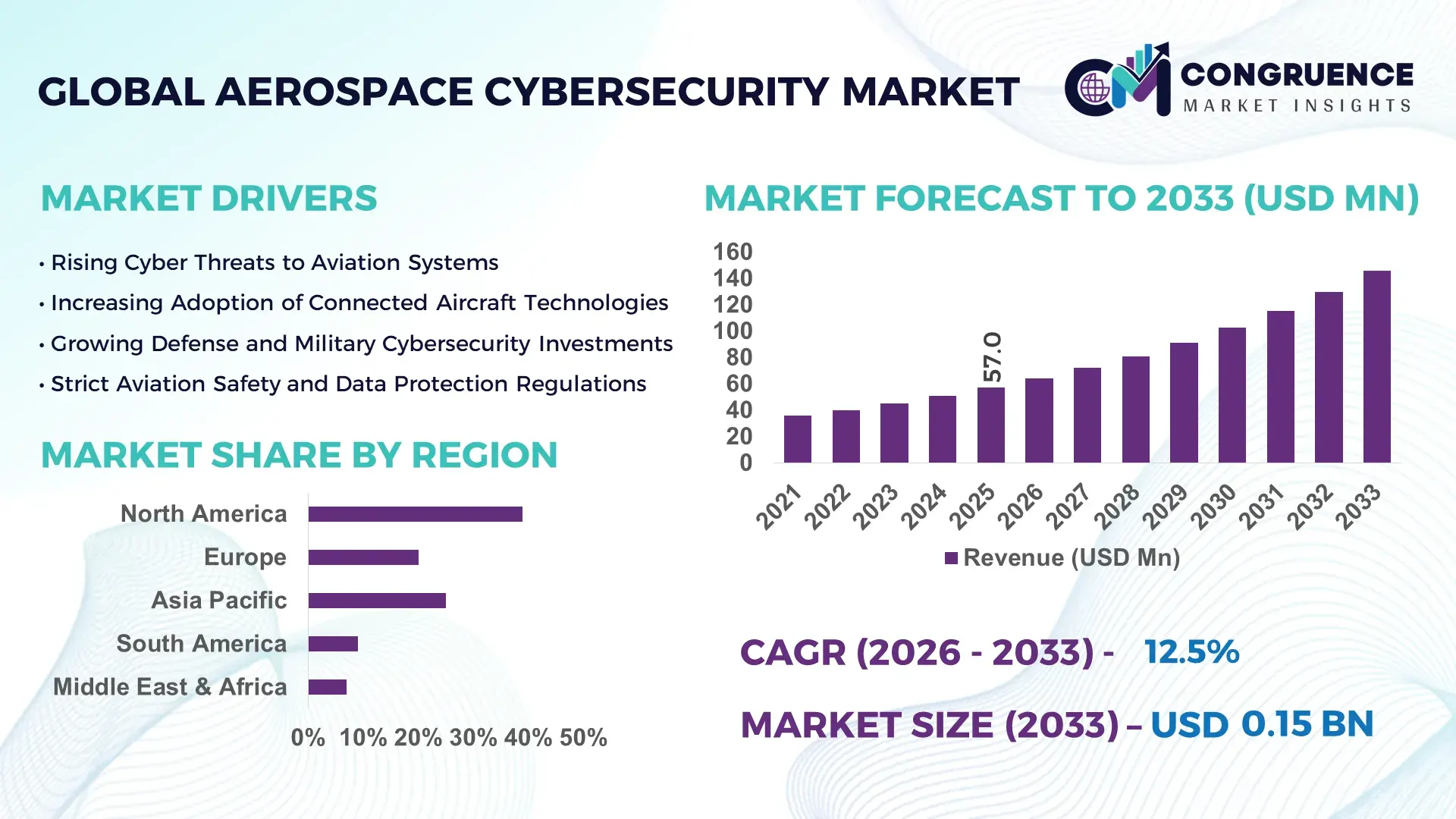

The Global Aerospace Cybersecurity Market was valued at USD 56.98 Million in 2025 and is anticipated to reach a value of USD 145.7 Million by 2033 expanding at a CAGR of 12.45% between 2026 and 2033. The growth is primarily driven by the increasing digitalization of aircraft systems, satellite networks, and defense communication infrastructure, which has significantly elevated the need for advanced aerospace cybersecurity solutions.

The United States maintains a highly developed aerospace cybersecurity ecosystem supported by extensive defense spending and large-scale aerospace manufacturing capabilities. The country operates more than 5,200 commercial aircraft fleets and supports over 3,000 active satellites that require continuous cybersecurity monitoring. The U.S. aerospace industry recorded over USD 955 billion in annual economic activity, with cybersecurity integrated into avionics systems, ground control networks, and satellite communication platforms. Investments exceeding USD 12 billion annually are directed toward defense cyber protection, secure avionics software, and threat intelligence platforms. Advanced programs focusing on secure flight control systems, AI-driven threat detection, and encrypted satellite communication networks are widely deployed across military aviation, space exploration missions, and commercial airline operations.

Market Size & Growth: The aerospace cybersecurity market is projected to expand from USD 56.98 million in 2025 to USD 145.7 million by 2033, supported by increased cyber-threat activity targeting aviation networks, satellite communication systems, and digital flight infrastructure.

Top Growth Drivers: Adoption of connected aircraft systems (68%), expansion of satellite-based communication platforms (54%), and increased defense cybersecurity spending (47%).

Short-Term Forecast: By 2028, advanced aerospace threat-detection platforms are expected to reduce cyber incident response time by nearly 35% while improving operational network resilience by approximately 28%.

Emerging Technologies: AI-driven anomaly detection, zero-trust aerospace security frameworks, and quantum-resistant encryption protocols are shaping next-generation aviation cybersecurity solutions.

Regional Leaders: North America is projected to reach USD 62 million by 2033 with strong defense aviation integration, Europe is expected to reach USD 38 million driven by satellite security programs, while Asia-Pacific could approach USD 29 million supported by expanding commercial aircraft fleets.

Consumer/End-User Trends: Airlines, space agencies, and defense aviation programs are increasingly deploying predictive cyber-risk monitoring tools, with over 60% of large airline operators implementing cybersecurity risk management systems.

Pilot or Case Example: In 2024, a secure aviation network pilot in Europe improved aircraft communication system resilience by 31% and reduced cyber-related operational disruptions by nearly 22%.

Competitive Landscape: Lockheed Martin leads with approximately 18% share, followed by Raytheon Technologies, Thales Group, BAE Systems, and Airbus CyberSecurity.

Regulatory & ESG Impact: Aviation regulators are enforcing stricter cybersecurity compliance frameworks including aircraft software security certification and satellite communication protection standards.

Investment & Funding Patterns: More than USD 2.4 billion has been invested globally in aerospace cybersecurity research, secure avionics systems, and satellite communication defense infrastructure during the past five years.

Innovation & Future Outlook: Emerging innovations such as secure digital twin platforms, autonomous threat detection systems, and cyber-resilient avionics architectures are expected to strengthen long-term aerospace cybersecurity capabilities.

The aerospace cybersecurity market spans multiple industry sectors including commercial aviation, defense aviation, satellite communications, and space exploration infrastructure. Defense aviation contributes nearly 45% of cybersecurity implementation due to mission-critical communication networks and classified data protection requirements. Commercial airlines represent about 32% of adoption as connected aircraft and digital maintenance platforms expand. Satellite communication systems account for nearly 18% of cybersecurity deployments, particularly for secure navigation, weather monitoring, and defense communication networks. Emerging trends include AI-based cyber threat prediction, blockchain-enabled aircraft maintenance data protection, and advanced encryption technologies securing satellite command links and ground control networks.

The aerospace cybersecurity market has become strategically essential as modern aircraft, satellites, and ground control systems rely heavily on digital communication networks and cloud-enabled operational platforms. Secure aviation infrastructure strategies increasingly prioritize zero-trust cybersecurity architectures and real-time threat monitoring systems to safeguard mission-critical aerospace assets. AI-based cyber-threat detection delivers nearly 40% faster anomaly identification compared to traditional rule-based intrusion detection systems, enabling aviation operators to respond more quickly to network threats. North America dominates in volume due to its extensive aerospace defense infrastructure, while Europe leads in cybersecurity adoption with nearly 64% of aerospace enterprises deploying integrated cyber risk management platforms.

By 2028, predictive cybersecurity analytics combined with automated threat intelligence platforms are expected to reduce aviation network vulnerabilities by approximately 30%. In parallel, aerospace organizations are committing to ESG-aligned digital security initiatives such as 25% energy-efficient data processing improvements in cybersecurity operations by 2030.

In 2024, a satellite network security initiative implemented in Japan improved communication encryption performance by 33% while reducing cyber-related signal disruptions by 27% through AI-driven anomaly monitoring. With the rapid expansion of digital aviation systems and space-based infrastructure, the aerospace cybersecurity market is positioned as a critical pillar of operational resilience, regulatory compliance, and sustainable technological growth.

The growing adoption of connected aircraft technology has significantly increased cybersecurity requirements across the aerospace industry. Modern commercial aircraft generate over 500 GB of operational data per flight, transmitted through satellite communication and onboard wireless networks. More than 70% of global airline fleets now utilize connected aircraft systems for predictive maintenance, passenger connectivity, and real-time operational monitoring. These digital platforms create multiple potential cyber-attack entry points, encouraging airlines and defense agencies to deploy advanced aviation cybersecurity frameworks. Additionally, the aviation sector experiences thousands of attempted cyber intrusions annually targeting flight management systems, communication networks, and airline data platforms. As aviation digitalization accelerates, secure avionics software protection, encrypted satellite communication, and AI-driven threat detection solutions are becoming essential components of aerospace cybersecurity infrastructure.

Many aerospace systems still rely on legacy avionics infrastructure that was originally designed without modern cybersecurity safeguards. A large portion of global aircraft fleets—particularly those manufactured before 2010—operate on older communication protocols and onboard systems that lack built-in cyber protection. Integrating advanced cybersecurity solutions into these legacy platforms often requires extensive system modifications, software upgrades, and certification procedures. Aircraft certification processes can take 18–36 months, slowing the deployment of new cybersecurity technologies. Additionally, retrofitting legacy systems may require redesigning avionics software architecture and revalidating flight safety standards, increasing operational complexity for airlines and aerospace manufacturers. These technical and regulatory challenges create barriers to rapid cybersecurity implementation across older aerospace platforms.

The rapid expansion of satellite-based communication systems presents significant growth opportunities for aerospace cybersecurity solutions. More than 9,000 active satellites are expected to operate globally by 2030, supporting aviation navigation, communication, weather forecasting, and defense operations. These satellites rely on ground control networks and encrypted communication links that must remain protected from cyber interference. Aerospace cybersecurity platforms capable of securing satellite command transmissions, preventing signal hijacking, and monitoring ground station networks are gaining increasing demand. Additionally, emerging low-earth-orbit satellite constellations supporting aviation connectivity are driving the adoption of advanced encryption technologies, secure command authentication systems, and AI-based anomaly detection platforms across space-based communication infrastructure.

Cyber-attack techniques targeting aviation and space infrastructure are becoming increasingly sophisticated, creating major challenges for cybersecurity providers. Aerospace communication networks are highly complex, involving interactions between aircraft avionics systems, satellite communication links, airline data centers, and air traffic control networks. Cybercriminals are increasingly using advanced persistent threat techniques, AI-enabled intrusion tools, and coordinated multi-network attacks to exploit vulnerabilities. The aviation sector recorded a significant rise in cyber incidents targeting airline reservation systems, navigation software, and satellite communication platforms in recent years. Detecting and responding to such highly complex threats requires continuous cybersecurity monitoring, advanced threat intelligence capabilities, and constant software updates, making long-term security management both technically demanding and resource intensive for aerospace organizations.

• Rapid Expansion of AI-Driven Threat Detection Systems:

Artificial intelligence–based cybersecurity platforms are increasingly deployed across aviation infrastructure to detect anomalies and cyber intrusions in real time. Nearly 62% of large airline operators have integrated AI-powered threat detection tools into their network monitoring systems to identify suspicious behavior within avionics data exchanges and ground communication networks. These systems process more than 15 million security events daily across aviation data centers, enabling faster threat recognition and automated response mechanisms. Machine learning algorithms used in aerospace cybersecurity platforms have demonstrated up to 40% improvement in threat detection accuracy compared to rule-based monitoring systems. Defense aviation networks are particularly active adopters, with more than 48% of military aviation cybersecurity programs incorporating AI analytics platforms to protect mission-critical systems and encrypted communication channels.

• Rising Deployment of Zero-Trust Security Architectures:

Zero-trust cybersecurity frameworks are rapidly transforming aviation network protection strategies. Approximately 58% of aerospace cybersecurity programs implemented zero-trust access controls by 2024, ensuring that all users, devices, and applications must undergo continuous authentication before accessing operational systems. In aircraft communication networks, zero-trust frameworks have reduced unauthorized access attempts by nearly 35%. Airlines operating large international fleets are adopting identity-based network segmentation, reducing lateral cyber movement across systems by 28%. Additionally, more than 70% of newly developed aerospace software platforms now incorporate zero-trust security architecture during design stages, ensuring continuous validation of network activities across aircraft avionics, satellite communication systems, and airline operational platforms.

• Growing Security Integration in Satellite Communication Networks:

The increasing reliance on satellite communication systems for aircraft connectivity, navigation, and real-time data transmission has significantly expanded cybersecurity investment across aerospace infrastructure. Modern connected aircraft rely on satellite links for transmitting more than 500 GB of operational data per flight, requiring robust encryption and cyber monitoring. Nearly 65% of global satellite ground stations now deploy advanced cybersecurity monitoring tools to protect command and data transmission networks. Additionally, low-earth-orbit satellite constellations supporting aviation connectivity are expected to exceed 8,500 operational satellites by 2030, further increasing the need for secure communication protocols. Aerospace operators deploying satellite cybersecurity frameworks report 31% improvement in signal integrity protection and reduced vulnerability to communication spoofing attempts.

• Expansion of Cybersecurity Compliance and Aviation Safety Regulations:

Aviation regulators worldwide are strengthening cybersecurity compliance standards for aircraft manufacturers, airlines, and satellite communication providers. More than 45 national aviation authorities have introduced updated cybersecurity certification requirements for aircraft software and avionics systems. These regulatory frameworks require continuous cybersecurity risk assessments, secure software development practices, and real-time incident monitoring systems. Compliance-driven cybersecurity investments among aerospace manufacturers increased by nearly 36% between 2022 and 2025, reflecting the rising regulatory pressure. Additionally, over 60% of new aircraft development programs now include dedicated cybersecurity engineering teams responsible for secure avionics design and cyber resilience testing. These regulatory initiatives are accelerating adoption of advanced cybersecurity solutions across both commercial aviation and defense aerospace sectors.

The aerospace cybersecurity market is segmented based on security solution types, operational applications, and end-user groups across the aviation and space industries. Security solution types primarily include network security, endpoint protection, cloud security, and application security systems designed to safeguard aviation data infrastructure. Applications span aircraft avionics protection, satellite communication security, airline operational systems, and air traffic management networks. End-user segments consist mainly of commercial airlines, defense aviation organizations, aerospace manufacturers, and satellite operators. Defense aviation contributes nearly 45% of cybersecurity implementations due to highly sensitive communication networks, while commercial aviation represents about 35% of cybersecurity deployments as connected aircraft platforms expand globally.

Network security solutions represent the leading segment in the aerospace cybersecurity market, accounting for approximately 38% of overall adoption due to the increasing reliance on interconnected aviation communication networks. These solutions focus on protecting aircraft data transmissions, airline operational systems, and satellite command networks from cyber intrusions. Endpoint security platforms represent around 24% of deployments, safeguarding onboard avionics devices, aircraft maintenance systems, and airline IT infrastructure. However, cloud security solutions are the fastest-growing segment, expanding at an estimated 14.2% growth rate, driven by the rapid migration of airline data platforms and predictive maintenance systems to cloud environments. Application security systems also play an important role, particularly in protecting flight management software, airline reservation platforms, and digital aircraft maintenance tools. Identity and access management technologies contribute nearly 18% of total cybersecurity implementation, ensuring secure authentication across airline operational networks.

Aircraft avionics protection represents the largest application segment, accounting for approximately 36% of aerospace cybersecurity deployments, as modern aircraft rely on complex digital avionics systems for navigation, flight control, and onboard communication. These systems exchange large volumes of operational data with airline ground networks and satellite communication systems, making cybersecurity protection essential. Satellite communication security accounts for nearly 28% of applications, ensuring encrypted communication links between aircraft, satellites, and ground control stations. Air traffic management cybersecurity is the fastest-growing application segment, expanding at an estimated 13.8% growth rate due to increasing digitalization of global air traffic control systems and the implementation of next-generation air navigation platforms. Additionally, airline operational technology security solutions covering reservation platforms, fleet management systems, and digital maintenance networks represent about 22% of cybersecurity deployments.

Defense aviation organizations represent the largest end-user segment in the aerospace cybersecurity market, accounting for approximately 42% of cybersecurity deployments due to the need to protect classified communication systems, mission-critical aircraft networks, and satellite defense infrastructure. Military aviation networks require advanced encryption technologies, continuous threat monitoring platforms, and cyber-resilient communication systems. Commercial airlines account for nearly 34% of cybersecurity adoption, driven by the expansion of connected aircraft platforms and increasing passenger data security requirements. Satellite operators represent the fastest-growing end-user segment, expanding at an estimated 15.1% growth rate as global satellite constellations supporting aviation communication and navigation services rapidly increase. Aerospace manufacturers also contribute significantly, accounting for approximately 14% of cybersecurity deployments, particularly in secure avionics software development and aircraft system integration.

Region North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

North America benefits from more than 5,000 active commercial aircraft, 3,000+ operational satellites, and over 120 major aerospace cybersecurity programs protecting aviation communication systems and defense networks. Europe holds approximately 27% of the market supported by more than 450 aviation cybersecurity projects across commercial aviation and satellite navigation systems. Asia-Pacific accounts for about 22% of deployments driven by rapidly expanding aircraft fleets exceeding 8,000 aircraft across China, India, and Japan. South America represents roughly 7% of global aerospace cybersecurity implementation, while the Middle East & Africa account for about 5%, supported by airport digitalization programs and aviation infrastructure modernization across more than 80 international airports.

How Is Advanced Aviation Digital Infrastructure Strengthening Aerospace Cybersecurity Adoption?

North America holds approximately 39% of the aerospace cybersecurity market, driven by strong demand from defense aviation, commercial airlines, and satellite communication networks. The United States alone operates more than 5,200 commercial aircraft and supports over 3,000 satellites requiring continuous cyber protection. Aviation regulators have strengthened aircraft cybersecurity certification standards, requiring integrated software security verification for new avionics platforms. The region also leads in AI-driven cyber defense platforms protecting aviation networks and aircraft data infrastructure. A major aerospace cybersecurity provider recently deployed advanced threat monitoring systems across more than 600 airline operational networks. Regional enterprise adoption is particularly high among aviation, defense, and aerospace manufacturing sectors where digital aircraft systems, satellite communications, and predictive maintenance platforms generate large volumes of operational data requiring secure protection.

How Are Aviation Regulations and Digital Aviation Transformation Driving Cybersecurity Demand?

Europe accounts for approximately 27% of the aerospace cybersecurity market, supported by strong aviation industries in Germany, the United Kingdom, and France. More than 450 aviation cybersecurity programs are active across European aviation infrastructure, including aircraft manufacturing, airline operations, and satellite communication networks. Aviation regulators have introduced strict cybersecurity certification requirements for aircraft software and avionics systems, encouraging the integration of secure digital flight systems. European aerospace manufacturers are increasingly implementing AI-based threat detection platforms across aircraft communication networks. A major aerospace security technology provider deployed cyber monitoring tools across more than 150 aviation control networks across Europe. Regulatory compliance and strong digital governance frameworks drive demand for explainable and auditable aerospace cybersecurity platforms across the region.

What Factors Are Accelerating Cybersecurity Deployment in Expanding Aviation Infrastructure?

Asia-Pacific ranks among the fastest-growing aerospace cybersecurity markets, accounting for roughly 22% of global adoption supported by expanding aviation infrastructure and aircraft manufacturing. China, India, and Japan collectively operate more than 8,000 commercial aircraft and support large satellite communication networks used for aviation navigation and communication systems. Regional aerospace manufacturing hubs are rapidly integrating cybersecurity protection into avionics software and satellite communication platforms. Technology innovation hubs in Japan and South Korea are advancing AI-based cyber monitoring solutions for aviation systems. A regional cybersecurity technology company recently implemented aviation network monitoring platforms across more than 80 airline communication networks. Regional consumer adoption trends indicate growing cybersecurity investments among airlines and aviation authorities as digital flight management and connected aircraft platforms expand.

How Is Aviation Infrastructure Modernization Increasing Cybersecurity Adoption?

South America represents approximately 7% of the aerospace cybersecurity market, led by Brazil and Argentina where aviation infrastructure modernization programs are expanding. Brazil operates more than 700 commercial aircraft and has implemented digital aviation network protection across major international airports. Governments across the region are investing in secure aviation communication networks and air traffic management cybersecurity upgrades. Aviation infrastructure development projects across more than 40 regional airports have integrated digital cybersecurity monitoring platforms. A regional aerospace technology provider recently deployed cyber protection tools across multiple airline data networks supporting aviation communication systems. Regional consumer behavior indicates increasing adoption of cybersecurity solutions within airline operations and airport digital systems as aviation digital transformation programs expand.

What Role Does Aviation Modernization Play in Cybersecurity Expansion?

The Middle East & Africa account for approximately 5% of the aerospace cybersecurity market, driven by aviation expansion in the United Arab Emirates, Saudi Arabia, and South Africa. More than 60 major international airports across the region are adopting digital aviation infrastructure requiring secure communication networks. Aviation modernization programs include integrated cybersecurity frameworks protecting aircraft communication, airline operational systems, and airport digital infrastructure. Governments are strengthening aviation cybersecurity regulations while forming international aviation security partnerships. A regional aerospace cybersecurity provider recently implemented secure aviation communication monitoring platforms across multiple airline networks operating from Gulf aviation hubs. Regional consumer behavior indicates growing cybersecurity investment among airlines and airport authorities as aviation passenger traffic and digital aviation services increase.

• United States – 34% market share in the Aerospace Cybersecurity market due to its extensive defense aviation infrastructure, large commercial aircraft fleet, and advanced aerospace cybersecurity technology development programs.

• China – 16% market share in the Aerospace Cybersecurity market supported by rapid aircraft fleet expansion, growing satellite communication networks, and increasing government investments in aviation cybersecurity systems.

The aerospace cybersecurity market features a moderately consolidated competitive landscape with more than 40 active technology providers delivering cybersecurity platforms designed specifically for aviation and space infrastructure. The top five companies collectively account for approximately 48% of the total market presence, reflecting strong technological specialization and high barriers to entry associated with aviation certification standards and defense security requirements. Leading companies compete through advanced threat detection platforms, secure avionics software solutions, and satellite communication cybersecurity technologies. Strategic partnerships between aerospace manufacturers and cybersecurity providers have increased significantly, with more than 60 joint development agreements focused on protecting connected aircraft systems and satellite communication networks.

Innovation is a primary competitive factor, particularly in areas such as artificial intelligence–based threat analytics, zero-trust security frameworks, and quantum-resistant encryption technologies. Aerospace cybersecurity vendors are increasingly integrating predictive threat intelligence platforms capable of analyzing millions of network events in real time across aviation communication networks. The competitive landscape also includes frequent product launches and technological upgrades designed to strengthen aviation cyber resilience. Several companies have expanded dedicated aerospace cybersecurity divisions to address growing demand from airlines, satellite operators, and defense aviation organizations.

Lockheed Martin

Raytheon Technologies

Thales Group

BAE Systems

Honeywell International

Northrop Grumman

Leonardo S.p.A.

Booz Allen Hamilton

General Dynamics Mission Systems

Palo Alto Networks

Fortinet

Advanced cybersecurity technologies are rapidly transforming the protection of aerospace communication networks, avionics systems, and satellite infrastructures. Artificial intelligence and machine learning platforms are widely deployed to analyze network traffic patterns and identify anomalies across aviation systems. Modern aerospace cybersecurity platforms can process more than 20 million security events daily across airline operational networks and satellite communication infrastructure. AI-driven threat detection tools improve anomaly detection accuracy by approximately 35–40% compared to traditional rule-based monitoring systems.

Zero-trust cybersecurity architecture is increasingly integrated into aircraft and satellite communication networks, ensuring continuous verification of users, devices, and applications. Nearly 70% of newly developed aviation software systems now incorporate identity-based access controls and network segmentation technologies. Blockchain-based cybersecurity frameworks are also emerging for aircraft maintenance data protection and secure communication between airlines and maintenance providers.

Quantum-resistant encryption technologies are gaining attention as aerospace operators prepare for next-generation cyber threats targeting satellite command links and defense communication networks. Additionally, secure digital twin platforms are being used to simulate aircraft network environments, enabling cybersecurity teams to test potential cyberattack scenarios before deployment. Edge-based cybersecurity systems integrated directly within aircraft avionics are also expanding, enabling real-time threat monitoring across onboard systems without relying entirely on centralized data networks.

• In October 2025, Lockheed Martin expanded its Cyber Resiliency Platform to enhance cyber protection for military aircraft and space systems. The platform integrates AI-driven threat monitoring and secure software architecture designed to protect mission-critical aerospace communication networks and digital avionics infrastructure. Source: www.lockheedmartin.com

• In March 2025, Thales launched a new aviation cybersecurity solution designed to protect connected aircraft systems and airline operational networks from cyber intrusions. The platform integrates advanced threat intelligence analytics and real-time monitoring capabilities to safeguard aircraft communication channels and ground-based aviation infrastructure. Source: www.thalesgroup.com

• In September 2024, Airbus Defence and Space introduced an upgraded cybersecurity monitoring system for satellite communication networks. The system enhances protection against signal interference, data manipulation, and unauthorized satellite command access across space communication infrastructure used by aviation and defense operators. Source: www.airbus.com

• In April 2024, Honeywell announced the expansion of its aerospace cybersecurity services portfolio to protect airline operational technology networks and connected aircraft systems. The new security platform integrates encrypted communication protocols and advanced cyber threat detection tools designed for aviation infrastructure protection. Source: www.honeywell.com

The Aerospace Cybersecurity Market Report provides a comprehensive analysis of cybersecurity solutions designed to protect aviation, satellite, and defense aerospace infrastructure from evolving cyber threats. The report evaluates key security technology segments including network security, endpoint protection, cloud security, application security, and identity management systems used across aviation digital ecosystems. It examines multiple applications such as aircraft avionics protection, satellite communication security, airline operational technology systems, and air traffic management cybersecurity platforms.

The report covers five major geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional technology adoption, aviation infrastructure growth, and cybersecurity investment trends. More than 20 countries with major aviation and aerospace industries are assessed within the report.

Additionally, the study evaluates end-user sectors including commercial airlines, defense aviation organizations, aerospace manufacturers, and satellite operators. The report also highlights emerging cybersecurity technologies such as artificial intelligence–driven threat detection, zero-trust aviation network architectures, blockchain-based aircraft data security, and quantum-resistant encryption protocols designed to protect next-generation aerospace communication systems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.45% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lockheed Martin, Raytheon Technologies, Thales Group, BAE Systems, Honeywell International, Northrop Grumman, Leonardo S.p.A., Booz Allen Hamilton, General Dynamics Mission Systems, Palo Alto Networks, Fortinet |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |