Reports

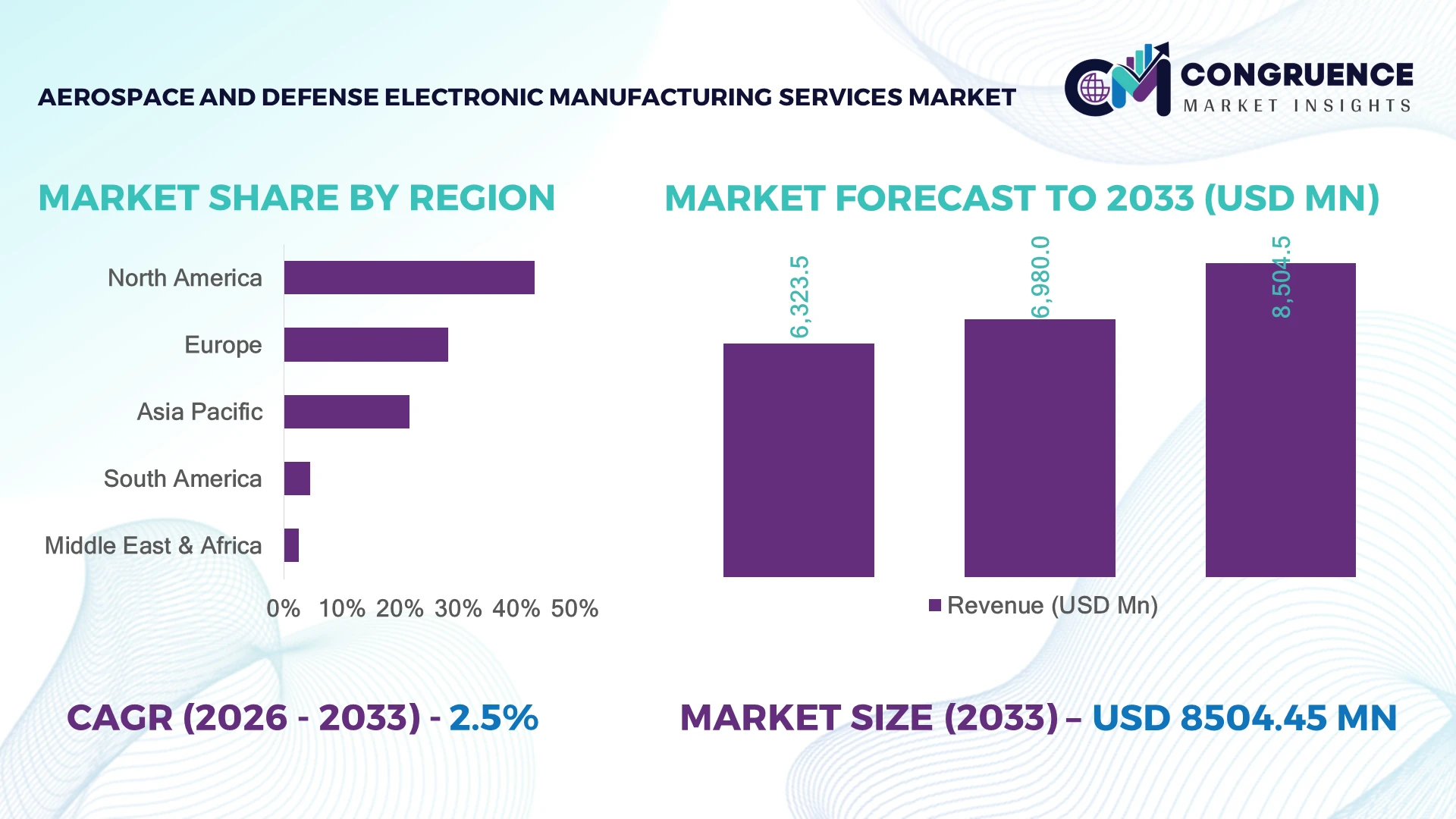

The Global Aerospace and Defense Electronic Manufacturing Services Market was valued at USD 6,980.0 Million in 2025 and is anticipated to reach a value of USD 8,504.5 Million by 2033 expanding at a CAGR of 2.5% between 2026 and 2033. Rising defense electronics modernization, increasing avionics outsourcing, and secure PCB assembly requirements for mission-critical platforms are accelerating global Aerospace and Defense Electronic Manufacturing Services market expansion.

The United States dominates with nearly 41% of global aerospace and defense EMS activity, supported by over USD 90 billion in annual defense electronics procurement, advanced aerospace manufacturing, and high-reliability PCB adoption across military programs. Compared with Germany's specialized precision manufacturing base, U.S. capacity remains significantly larger, strengthened by NATO-led defense modernization and accelerated adoption of AI-enabled electronics testing and production systems.

This market reinforces long-term investment priorities around resilient supply chains, certified manufacturing capabilities, and advanced electronics integration for strategic defense programs.

Market Size & Growth: USD 6,980.0 Million (2025) to USD 8,504.5 Million (2033) at 2.5% CAGR, driven by defense electronics outsourcing.

Top Growth Drivers: Defense modernization 32%, avionics digitalization 28%, secure electronics localization 24%.

Short-Term Forecast: By 2028, automated production cuts manufacturing defects by 18%.

Emerging Technologies: AI inspection, robotic assembly, and advanced miniaturized electronics improve production precision by 20%.

Regional Leaders: North America USD 3.4 Billion, Europe USD 2.1 Billion, Asia-Pacific USD 1.8 Billion, supported by regional manufacturing expansion.

Consumer/End-User Trends: Nearly 64% of defense OEMs increasingly outsource complex electronics manufacturing.

Pilot/Case Example: 2024 smart-factory deployment improved testing throughput by 22% for aerospace electronics.

Competitive Landscape: Top suppliers control nearly 45% of the market; Benchmark Electronics, Sanmina, Jabil, Plexus, and Kimball Electronics remain key participants.

Regulatory & ESG Impact: Digital compliance systems reduce certification processing time by 15% across regulated production.

Investment & Funding: More than USD 2.3 Billion supports advanced manufacturing expansion and strategic partnerships amid global supply-chain diversification.

Innovation & Future Outlook: Digital twins, AI-driven quality control, and resilient manufacturing networks strengthen next-generation aerospace electronics production.

The Aerospace and Defense Electronic Manufacturing Services Market is witnessing stronger demand from avionics, radar, satellite communications, and electronic warfare systems. AI-assisted inspection, automated optical testing, and advanced microelectronics packaging are improving manufacturing precision, while over 35% of new production lines incorporate smart automation. Ongoing supply-chain localization and stricter defense compliance standards continue reshaping sourcing strategies, setting the foundation for broader strategic market developments.

The Aerospace and Defense Electronic Manufacturing Services Market has become strategically important as governments and defense contractors prioritize secure electronics manufacturing, supply-chain resilience, and localized production capabilities. Defense procurement reforms, expanding aerospace modernization programs, and increased digitalization are transforming competitive dynamics while encouraging manufacturers to strengthen certified production capacity and vertically integrated operations.

Advanced AI-enabled inspection systems now identify manufacturing defects approximately 25% faster than conventional manual inspection while reducing quality-control costs by nearly 18%. North America continues to lead through large-scale defense production and advanced manufacturing infrastructure, whereas Asia-Pacific is expanding rapidly through electronics manufacturing capabilities, skilled labor availability, and government-backed industrial investments. Over the next two to three years, automated assembly adoption across high-reliability production facilities is expected to exceed 50%, improving throughput and traceability.

Manufacturers are expanding partnerships with aerospace OEMs to deliver integrated PCB assembly, testing, and lifecycle support under long-term defense contracts. Several companies are investing in smart factories equipped with digital production monitoring to improve operational efficiency, shorten production cycles, and strengthen compliance with defense standards. These strategic initiatives position suppliers to secure higher-value programs, reinforce competitive differentiation, and build sustainable long-term advantages in the evolving global aerospace and defense ecosystem.

Defense electronics modernization programs and increasing outsourcing of high-reliability manufacturing are accelerating demand for aerospace and defense electronic manufacturing services. More than 62% of advanced defense platforms now integrate digitally intensive avionics, while automated optical inspection improves production accuracy by nearly 20% and reduces rework by 15%. The United States continues expanding domestic defense electronics manufacturing following strengthened secure supply-chain initiatives, encouraging OEMs to shift certified production toward trusted EMS partners. This transition improves manufacturing resilience while shortening qualification cycles for mission-critical assemblies. In response, companies are expanding Class 3 manufacturing capacity, investing in AI-enabled inspection systems, and forming long-term partnerships with defense contractors to strengthen secure electronics production. A key strategic advantage increasingly lies in combining certified manufacturing expertise with vertically integrated testing and lifecycle support.

Supply dependency on specialized semiconductors and stringent aerospace certification requirements continue limiting manufacturing flexibility across the industry. Approximately 38% of aerospace-grade electronic components rely on highly specialized suppliers, while qualification and certification processes extend production schedules by 20–30% compared with commercial electronics. Export controls on advanced electronic components and persistent sourcing constraints have increased procurement complexity for manufacturers operating in the United States and allied markets. These structural pressures raise inventory costs, delay program execution, and reduce operational responsiveness for defense OEMs. To mitigate these challenges, manufacturers are diversifying supplier networks, increasing localized component sourcing, negotiating multi-year procurement contracts, and adopting digital supply-chain monitoring platforms. Companies securing qualified alternative suppliers gain stronger production continuity and improved contract competitiveness.

Rapid deployment of AI-enabled manufacturing, digital twins, and advanced electronics packaging creates substantial opportunities for aerospace and defense EMS providers. Smart manufacturing systems improve factory productivity by nearly 25%, while predictive maintenance reduces unexpected equipment downtime by approximately 18%. India is strengthening domestic aerospace manufacturing through defense industrial initiatives that encourage localized electronics production and technology collaboration, creating new opportunities for globally certified EMS providers. Companies are investing in advanced microelectronics packaging, automated testing laboratories, and collaborative R&D programs supporting autonomous systems, space electronics, and secure communications. An emerging strategic opportunity lies in offering integrated design-to-production services that reduce development cycles while improving certification readiness for increasingly complex defense electronics.

Scaling advanced aerospace electronics manufacturing requires specialized engineering talent, cybersecurity readiness, and seamless integration between digital production systems and legacy defense infrastructure. Nearly 35% of manufacturers report shortages of highly skilled electronics technicians, while secure manufacturing environments increase implementation costs by approximately 22% due to stricter cyber protection and compliance requirements. Germany and other advanced manufacturing economies continue facing competition for experienced aerospace engineers as digital production expands. These constraints affect deployment consistency, production scalability, and long-term operational resilience for high-reliability programs. Companies must accelerate workforce development, strengthen cyber-secure manufacturing architecture, and invest in automation partnerships with technology providers. Organizations that successfully combine digital production with specialized technical expertise will establish stronger competitive positioning in future defense manufacturing programs.

AI-Driven Factory Automation AI-enabled optical inspection, predictive analytics, and robotic assembly are transforming aerospace EMS operations. More than 45% of newly commissioned production lines now integrate AI-assisted quality control, while automated inspection reduces defect rates by nearly 22% and shortens testing cycles by 18%. U.S. manufacturers are expanding smart factories to meet defense qualification requirements, with EMS providers scaling digital production platforms and automated traceability systems.

Localized Supply Chain Expansion Supply-chain resilience has become a strategic priority as export controls and geopolitical uncertainty reshape sourcing decisions. Around 37% of leading aerospace OEMs have increased domestic supplier engagement, while localized procurement reduces logistics lead times by approximately 20%. Companies are restructuring sourcing networks, expanding certified regional facilities, and forming long-term component agreements to improve production continuity and contract reliability.

Advanced Electronics Miniaturization Demand for lighter, compact, and high-performance electronics continues accelerating across avionics and defense platforms. High-density PCB adoption has increased by 28%, while advanced packaging technologies improve thermal efficiency by nearly 16%. Manufacturers are investing in precision assembly equipment, microelectronics integration, and collaborative engineering programs to support next-generation radar, satellite, and electronic warfare applications with improved operational reliability.

Digital Compliance and Traceability Regulatory compliance is shifting toward fully digital manufacturing records and lifecycle traceability. Nearly 55% of aerospace electronics facilities now deploy digital manufacturing execution systems, reducing documentation processing time by 25%. European and U.S. defense contractors increasingly require end-to-end component traceability, prompting EMS providers to strengthen cybersecurity, digital certification workflows, and secure production environments while improving customer audit readiness.

Electronic Manufacturing represents the largest segment, accounting for approximately 52% of total market activity due to its central role in PCB assembly, system integration, cable harness production, and high-reliability electronic assemblies. Defense contractors increasingly outsource complex manufacturing to certified EMS providers that offer scalable production, advanced automation, and strict quality compliance. Companies continue expanding automated SMT lines and AI-assisted inspection capabilities to improve manufacturing consistency while reducing production defects by nearly 20%. Mature services such as Logistics Services remain strategically important for inventory optimization and lifecycle support across global aerospace supply chains. Test Development & Implementation is the fastest-growing segment as increasingly sophisticated avionics, radar systems, and mission-critical electronics require comprehensive validation before deployment. Automated testing now improves verification efficiency by approximately 24%, encouraging manufacturers to invest in digital test platforms and simulation-based validation. Meanwhile, Others continues supporting specialized engineering and aftermarket requirements, reflecting growing demand for integrated manufacturing ecosystems. Investment priorities increasingly favor providers capable of combining manufacturing, testing, and logistics under unified long-term contracts.

Military Aircraft remains the dominant application, representing nearly 46% of overall demand because modern combat aircraft incorporate advanced avionics, electronic warfare systems, flight-control electronics, and secure communications. Defense modernization programs continue increasing the electronic content of next-generation aircraft, while automated manufacturing improves production throughput by approximately 18%. EMS companies are strengthening partnerships with aircraft OEMs, expanding secure manufacturing facilities, and integrating advanced quality-control technologies to support long-duration defense programs. Space Systems is emerging as the fastest-growing application owing to expanding satellite constellations, national security missions, and commercial launch activity. High-reliability electronics deployment has increased by nearly 26%, encouraging suppliers to invest in radiation-resistant manufacturing and advanced electronics packaging. Civil & Commercial Aircraft continues generating stable replacement demand through avionics upgrades, while Unmanned Aerial Vehicles (UAVs) are gaining momentum through compact electronics and autonomous mission systems. Others supports specialized defense electronics and mission-specific platforms, broadening the addressable manufacturing landscape.

Defense & Military represents the largest end-user segment, contributing approximately 49% of overall demand because defense organizations require certified electronics, secure manufacturing environments, and long-term lifecycle support for mission-critical systems. Procurement programs increasingly prioritize trusted domestic manufacturing, while more than 60% of high-value defense electronics contracts require advanced traceability and compliance capabilities. EMS providers continue expanding dedicated defense production lines, strengthening cybersecurity infrastructure, and pursuing strategic partnerships with prime contractors. Space Exploration Agencies are the fastest-growing end-user group as satellite deployments, deep-space missions, and national space initiatives accelerate demand for highly reliable electronic assemblies. Production requirements for space-qualified electronics have increased by roughly 23%, encouraging manufacturers to invest in advanced testing and radiation-resistant technologies. Commercial Aerospace remains an established customer base driven by fleet modernization, while Government Contractors and OEMs increasingly seek vertically integrated manufacturing partners. Tier 1 & Tier 2 Suppliers are expanding collaborative manufacturing ecosystems to improve delivery performance and supply-chain resilience.

North America accounted for the largest market share at 43.1%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 3.4% CAGRbetween 2026 and 2033.

North America maintains the leading position through its mature aerospace manufacturing ecosystem, extensive defense procurement programs, and highly certified electronics production infrastructure. The region contributes approximately 43.1% of global market activity, supported by strong demand for avionics, radar electronics, secure communications, and mission-critical PCB assemblies. More than 65% of defense-focused EMS facilities have implemented AI-assisted inspection and digital manufacturing execution systems to improve traceability and production efficiency. Increasing localization initiatives, long-term government procurement contracts, and strategic collaborations between OEMs and EMS providers continue strengthening production resilience while accelerating qualification of advanced electronic assemblies for military and aerospace platforms.

United States Market Outlook: The United States remains the regional growth engine owing to its unmatched aerospace manufacturing capacity, advanced defense industrial base, and continuous investment in secure electronics production. The country accounts for nearly 80% of North America's aerospace EMS demand, supported by major defense contractors, certified manufacturing facilities, and vertically integrated electronics supply chains. Continued investment in automated PCB assembly, advanced testing laboratories, and digital quality assurance platforms enables manufacturers to shorten qualification timelines while supporting increasingly sophisticated aerospace and defense programs.

Europe represents the second-largest regional market, accounting for approximately 28.2% of global demand through strong aerospace manufacturing capabilities and increasing defense modernization initiatives. Growing cross-border industrial cooperation, advanced avionics production, and high-reliability electronics manufacturing continue strengthening regional competitiveness. Nearly 52% of aerospace electronics manufacturers are expanding automated inspection and traceability systems to comply with increasingly stringent certification standards. Defense procurement collaboration and long-term industrial partnerships are encouraging investments in advanced electronics manufacturing while improving supply-chain resilience for critical aerospace applications.

Germany Market Outlook: Germany leads the European market through its advanced industrial engineering capabilities, precision electronics manufacturing, and extensive aerospace supplier network. The country plays a critical role in producing high-reliability electronic assemblies for aircraft systems, satellites, and defense platforms. More than 40% of German aerospace electronics facilities have expanded smart manufacturing capabilities, allowing suppliers to improve production precision, digital traceability, and compliance with demanding aerospace certification requirements while strengthening partnerships across the European aerospace ecosystem.

Asia-Pacific is emerging as the fastest-growing regional market due to expanding aerospace manufacturing infrastructure, increasing defense self-reliance initiatives, and rising investment in advanced electronics production. The region contributes around 21.6% of global demand, supported by expanding PCB manufacturing capacity, semiconductor availability, and skilled engineering talent. Manufacturing automation adoption has increased by nearly 30%, while localized production strategies continue reducing dependence on imported electronic assemblies. Governments and private manufacturers are expanding certified aerospace production facilities, strengthening domestic supply chains, and accelerating deployment of advanced electronics manufacturing technologies.

China Market Outlook: China remains the largest market within Asia-Pacific through continuous investment in aerospace manufacturing, indigenous defense electronics development, and large-scale industrial modernization. Domestic manufacturers continue expanding advanced PCB production, electronic integration capabilities, and automated testing infrastructure to support military aviation, satellite systems, and unmanned platforms. More than 35% of new aerospace electronics production capacity added during recent years has incorporated intelligent manufacturing technologies, strengthening operational efficiency and supporting national localization objectives.

South America represents a developing market with approximately 4.5% of global demand, supported by expanding aerospace manufacturing activities, military equipment modernization, and localized industrial development. Aircraft maintenance, avionics upgrades, and specialized electronic assembly services remain key operational priorities across the region. Nearly 18% of aerospace manufacturers have expanded investment in automated production and electronic testing capabilities to improve manufacturing quality. Although dependence on imported high-end components remains a structural limitation, strategic industrial partnerships and localized production initiatives continue improving long-term manufacturing capability and supply-chain resilience.

Brazil Market Outlook: Brazil dominates the regional market through its established aerospace manufacturing ecosystem and strong commercial aircraft production capabilities. The country benefits from experienced engineering expertise, expanding avionics manufacturing, and increasing collaboration with international aerospace suppliers. Approximately 60% of South America's aerospace electronics manufacturing activity is concentrated in Brazil, where investments in advanced production technologies and certified manufacturing processes continue strengthening competitiveness across both commercial and defense aerospace sectors.

The Middle East & Africa market continues expanding through defense modernization programs, localized industrial development, and increasing investment in aerospace manufacturing infrastructure. The region contributes approximately 2.6% of global demand while steadily increasing participation in advanced electronics integration for military platforms. More than 25% of newly announced defense manufacturing initiatives include localized electronics production or technology transfer components. Governments are encouraging international partnerships, industrial offsets, and specialized manufacturing investments to strengthen domestic aerospace capabilities and reduce dependence on imported mission-critical electronic systems.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through ambitious defense localization strategies, expanding aerospace industrial infrastructure, and long-term investment in domestic manufacturing capabilities. The country continues strengthening partnerships with global aerospace companies while developing certified electronics manufacturing capacity for military applications. Defense localization initiatives target more than 50% domestic defense manufacturing participation over the long term, encouraging investments in advanced assembly, testing, workforce development, and technology transfer to establish a sustainable aerospace electronics ecosystem.

The market is led by Sanmina, Benchmark Electronics, Plexus, Jabil, and Kimball Electronics, competing directly with specialized regional EMS providers and vertically integrated aerospace manufacturers for high-value defense and avionics programs. The top five players collectively control approximately 44% of global market activity, creating a moderately consolidated competitive structure. Competition centers on certified manufacturing capability, engineering expertise, production speed, and supply-chain resilience rather than price alone. AI-enabled inspection improves production efficiency by nearly 20%, while automated testing reduces validation time by 18%, giving technology-focused suppliers a measurable advantage. Leading companies are expanding Class 3 manufacturing capacity, strengthening OEM partnerships, investing in digital factories, and integrating design, testing, and logistics services under single contracts. The competitive landscape is shifting toward secure domestic manufacturing and vertically integrated delivery models as defense procurement emphasizes trusted suppliers. Strict aerospace certification, cybersecurity compliance, and long qualification cycles remain significant entry barriers. Winning requires certified production excellence, resilient supply chains, advanced automation, and long-term strategic customer relationships.

Benchmark Electronics, Inc.

Plexus Corp.

Kimball Electronics, Inc.

Jabil Inc.

Flex Ltd.

Celestica Inc.

Cyient DLM Limited

Asteelflash Group

TT Electronics plc

SigmaTron International, Inc.

Nortech Systems Incorporated

Creation Technologies LP

ESCATEC Group

Artificial intelligence, digital manufacturing execution systems, and automated optical inspection have become core technologies across aerospace and defense EMS operations. AI-powered quality inspection reduces defect detection time by approximately 25%, while automated production analytics improve manufacturing throughput by nearly 18%. More than 55% of newly upgraded aerospace electronics facilities now integrate digital traceability platforms, enabling faster certification, improved compliance, and secure lifecycle documentation. Companies adopting these technologies achieve stronger operational consistency while meeting increasingly demanding defense qualification requirements.

Advanced electronics packaging, digital twins, and high-density PCB manufacturing are reshaping production capabilities. Compared with conventional manual inspection, AI-enabled inspection improves defect identification accuracy by roughly 20% while lowering rework costs by 15%. Prime defense contractors and globally certified EMS providers benefit most because integrated engineering and manufacturing shorten development cycles and accelerate product qualification. Smart factories combining robotics with predictive maintenance also improve equipment utilization and production scheduling.

Between 2026 and 2028, adoption of intelligent manufacturing platforms, cyber-secure production environments, and model-based digital engineering is expected to accelerate across defense electronics programs. Manufacturers investing in automated testing, secure cloud-based production monitoring, and advanced component traceability will strengthen competitive positioning, improve delivery reliability, and support increasingly complex avionics, satellite, and mission-critical electronics systems while reducing operational risk across global supply networks.

February 2025 – Cyient DLM secured a production contract with Boeing Global Services for precision-machined aerospace parts and assemblies, strengthening its long-term aerospace manufacturing portfolio and expanding high-precision production capabilities for commercial aviation programs. Business impact: reinforces strategic OEM collaboration. Source: www.prnewswire.com

February 2025 – RTX Collins Aerospace successfully tested its Enhanced Power and Cooling System (EPACS), delivering more than double the cooling capacity of the existing F-35 system. Business impact: supports next-generation defense electronics integration and future aircraft upgrades.

August 2025 – Anduril Industries became the third qualified U.S. solid rocket motor supplier, ending decades of limited supplier concentration for a critical defense component. Business impact: strengthens supply-chain resilience and expands domestic defense manufacturing capacity.

October 2025 – Honeywell Aerospace reported measurable improvements in aerospace electronics supply availability as production constraints eased across avionics programs, supporting more stable aircraft manufacturing schedules. Business impact: improves delivery predictability and strengthens electronics production planning.

This report provides a comprehensive assessment of the Aerospace and Defense Electronic Manufacturing Services Market across four types, five applications, and six end-user categories, delivering detailed analysis of manufacturing trends, procurement strategies, technology adoption, and competitive positioning. It evaluates operational developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while examining enterprise deployment patterns, certified manufacturing capabilities, and evolving supply-chain structures. More than 55% of analyzed production trends emphasize automation, digital traceability, and advanced electronics integration.

The study further examines emerging technologies including AI-enabled inspection, smart manufacturing, digital twins, automated testing, and advanced electronics packaging, together with regional manufacturing dynamics and leading company strategies. It supports investment planning, expansion decisions, supplier evaluation, partnership development, and competitive benchmarking between 2026 and 2033 by identifying high-priority application areas, evolving procurement behavior, technology adoption patterns, and long-term strategic opportunities across commercial aerospace, defense, space, and advanced electronic manufacturing ecosystems.

" "

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,980.0 Million |

| Market Revenue (2033) | USD 8,504.5 Million |

| CAGR (2026–2033) | 2.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sanmina Corporation; Benchmark Electronics, Inc.; Plexus Corp.; Kimball Electronics, Inc.; Jabil Inc.; Flex Ltd.; Celestica Inc.; Cyient DLM Limited; Asteelflash Group; TT Electronics plc; SigmaTron International, Inc.; Nortech Systems Incorporated; Creation Technologies LP; ESCATEC Group |

| Customization & Pricing | Available on Request (10% Customization Free) |