Reports

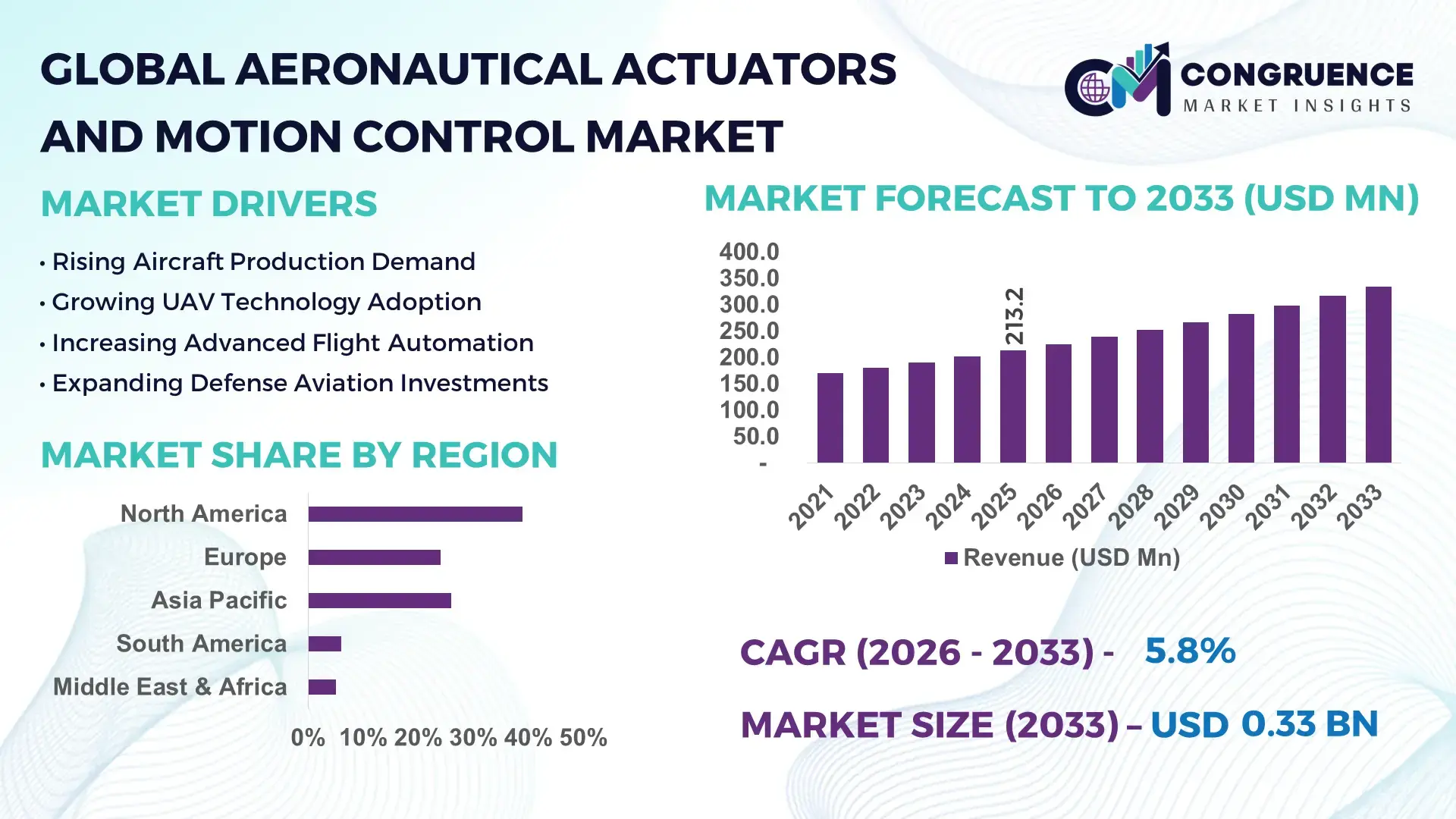

The Global Aeronautical Actuators and Motion Control Market was valued at USD 213.2 Million in 2025 and is anticipated to reach a value of USD 334.7 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033. The market is accelerating due to the aviation sector’s rapid transition toward more-electric aircraft systems, where electro-mechanical actuators are reducing hydraulic system weight by nearly 18% while improving response precision in commercial and defense aircraft platforms. Rising aircraft modernization programs, increased UAV deployment, and demand for lightweight flight-control architectures are reshaping procurement priorities across OEMs and Tier-1 suppliers. Between 2024 and 2026, aerospace manufacturers faced intensified semiconductor sourcing pressure and titanium component supply disruptions linked to ongoing geopolitical trade realignments involving Russia-Europe aerospace dependencies, forcing actuator manufacturers to localize critical production and diversify sourcing networks. Digital twin integration and predictive maintenance deployment increased by over 32% across advanced aerospace manufacturing facilities, optimizing component lifecycle management and reducing unscheduled maintenance downtime.

The United States dominates the global Aeronautical Actuators and Motion Control market with approximately 34% share, supported by over USD 70 billion in annual aerospace manufacturing output and continuous investment in next-generation military aviation systems. More than 62% of advanced flight-control systems integrated into high-performance defense aircraft now utilize electro-hydrostatic or electromechanical actuators compared to below 45% in legacy fleets. Boeing, Lockheed Martin, and RTX-driven supplier ecosystems continue expanding actuator precision capabilities, while FAA-backed aircraft electrification initiatives are accelerating smart motion-control adoption. Compared to conventional hydraulic systems, intelligent actuator assemblies deliver nearly 25% higher operational efficiency and reduced maintenance intervals across high-cycle aviation operations.

As aircraft electrification, autonomous flight systems, and predictive control technologies continue transforming aerospace engineering priorities, companies securing resilient supply chains and high-efficiency actuator innovation are strengthening long-term competitive positioning across commercial, defense, and advanced air mobility segments.

Market Size & Growth: USD 213.2 Million in 2025 reaching USD 334.7 Million by 2033 at 5.8% CAGR, driven by aircraft electrification and lightweight motion-control integration.

Top Growth Drivers: More-electric aircraft adoption surged 31%, UAV deployment expanded 28%, and predictive maintenance implementation increased 24% globally.

Short-Term Forecast: By 2028, actuator response efficiency is projected to improve 19% while maintenance-related downtime declines 16% across aerospace fleets.

Emerging Technologies: AI-enabled diagnostics, electro-mechanical actuators, and digital twin integration improved operational precision by over 22% in advanced aircraft systems.

Regional Leaders: North America leads at USD 82 million, Europe exceeds USD 61 million, while Asia-Pacific surpasses USD 54 million through aerospace localization expansion.

Consumer/End-User Trends: Over 58% of aerospace OEMs now prioritize low-weight smart actuators to reduce fuel consumption and maintenance intensity.

Pilot/Case Example: In 2025, advanced actuator retrofits in military UAVs improved flight-control accuracy by 21% and reduced servicing cycles by 17%.

Competitive Landscape: RTX controls nearly 18% market presence alongside Honeywell, Moog, Parker Hannifin, and Safran amid aerospace supply-chain restructuring.

Regulatory & ESG Impact: Aircraft electrification programs reduced hydraulic fluid dependency by 27%, supporting emission-control compliance and operational sustainability targets.

Investment & Funding: Aerospace automation investments exceeded USD 3.1 billion globally, fueled by OEM partnerships, regional manufacturing expansion, and smart-control integration.

Innovation & Future Outlook: High-growth autonomous aviation platforms and advanced air mobility systems are accelerating compact actuator innovation and precision-control optimization.

Commercial aviation contributes nearly 46% of total actuator integration demand, while defense aviation accounts for approximately 38% due to rising unmanned systems deployment and advanced fighter modernization programs. Electro-mechanical actuator adoption increased by 29% across next-generation aircraft platforms as aerospace manufacturers prioritize lighter assemblies and predictive diagnostics. Asia-Pacific is witnessing accelerated production localization amid global supply-chain diversification, while Europe continues advancing sustainability-driven aircraft electrification programs. Increasing integration of AI-assisted motion-control calibration and autonomous flight systems is positioning intelligent aerospace actuation as a core competitive differentiator for future aviation platforms.

The Aeronautical Actuators and Motion Control Market is rapidly transforming into a strategic battleground for aerospace manufacturers, defense contractors, and advanced mobility innovators as aircraft systems become increasingly electrified, autonomous, and digitally optimized. Precision motion-control infrastructure is no longer treated as a secondary subsystem; it is becoming central to aircraft efficiency, flight safety, operational reliability, and lifecycle cost optimization. Rising deployment of unmanned aerial systems, next-generation combat aircraft, and electric aviation platforms is accelerating demand for compact, intelligent, and energy-efficient actuator architectures across both commercial and defense aerospace ecosystems.

The industry is simultaneously experiencing pressure from supply-chain regionalization, export-control tightening, and aerospace-grade semiconductor shortages, forcing manufacturers to restructure sourcing strategies and expand domestic production capabilities. Electro-mechanical actuator technology now improves operational efficiency by 26% while reducing maintenance costs by nearly 21% compared to legacy hydraulic systems, fundamentally reshaping procurement priorities among aircraft OEMs. North America leads in production volume with nearly 39% market concentration, while Europe leads in electrification-focused innovation adoption with over 33% of aerospace manufacturers integrating low-emission smart actuation systems into next-generation aircraft programs.

Over the next two to three years, predictive maintenance integration across aerospace fleets is expected to reduce unscheduled maintenance events by approximately 18%, while AI-driven motion calibration systems are projected to improve flight-control precision by 23%. ESG-driven aerospace procurement is also becoming a competitive advantage, as lighter electromechanical systems reduce aircraft weight and improve fuel efficiency by nearly 14%, supporting stricter global emission mandates and improving long-term operating economics.

A strong execution-level example emerged in 2025 when advanced UAV manufacturers integrated intelligent servo-actuation platforms capable of improving flight stability by 19% while reducing component wear rates by 16% during high-frequency mission cycles. Major aerospace companies are aggressively shifting capital allocation toward smart manufacturing, digital twin integration, and advanced actuator miniaturization to capture emerging opportunities in autonomous aviation and urban air mobility. Companies that secure resilient aerospace supply chains, accelerate intelligent actuator innovation, and optimize energy-efficient flight-control architectures are positioning themselves to dominate the next generation of global aerospace competition.

The Aeronautical Actuators and Motion Control Market is undergoing significant structural transformation as aerospace manufacturers accelerate the transition toward electrically driven aircraft systems, autonomous flight technologies, and lightweight precision-control architectures. Demand is increasingly concentrated around electro-mechanical and electro-hydrostatic actuator systems capable of improving flight responsiveness, reducing maintenance intensity, and optimizing fuel efficiency across commercial, military, and unmanned aircraft platforms. Aerospace OEMs are prioritizing digitally integrated motion-control systems that support predictive maintenance and AI-assisted diagnostics, with adoption rates rising by over 30% across advanced aviation programs. Simultaneously, supply-chain restructuring, geopolitical trade realignments, and aerospace component localization are reshaping production strategies worldwide. North America continues leading in defense aviation integration, while Asia-Pacific is rapidly expanding aerospace manufacturing capacity to reduce import dependency. Europe is accelerating sustainability-focused aviation engineering through aircraft electrification initiatives and low-emission compliance frameworks. Companies are increasingly investing in advanced materials, compact actuator assemblies, and high-cycle durability optimization to improve operational reliability and secure long-term aerospace contracts in an increasingly competitive global aviation ecosystem.

Aircraft electrification is becoming the primary growth engine reshaping the Aeronautical Actuators and Motion Control Market as aerospace manufacturers aggressively replace conventional hydraulic systems with lighter and more energy-efficient electro-mechanical architectures. More-electric aircraft programs increased by over 34% globally between 2024 and 2026, while smart actuator deployment across advanced aviation platforms expanded nearly 28%. This structural shift is reducing aircraft system weight by approximately 15% and lowering maintenance requirements across commercial fleets. Simultaneously, rising defense spending and rapid UAV deployment are forcing aerospace suppliers to accelerate production scalability and actuator precision optimization. The ongoing restructuring of aerospace supply chains following Europe-Russia raw material disruptions has further pushed OEMs toward localized sourcing and vertically integrated manufacturing partnerships. In response, major companies are expanding actuator production facilities, investing in AI-driven diagnostics, and strengthening long-term aerospace supplier agreements. Aerospace manufacturers are also accelerating R&D investment into compact, high-response motion-control systems capable of supporting autonomous aviation and advanced air mobility programs. This combination of electrification, automation, and operational efficiency is fundamentally redefining future aerospace engineering priorities.

The Aeronautical Actuators and Motion Control Market remains heavily constrained by aerospace-grade raw material dependency, certification complexity, and volatile manufacturing costs. Aerospace titanium prices increased by approximately 18% during recent global supply-chain disruptions, while aerospace semiconductor lead times expanded nearly 27%, creating delays across actuator production programs. Certification and compliance procedures for flight-critical actuation systems continue extending development timelines by up to 22%, particularly for defense and next-generation electric aviation platforms. Global aerospace manufacturing also faces concentrated supplier dependency for precision bearings, electronic control modules, and specialized alloys, increasing operational vulnerability during geopolitical trade shifts and transportation bottlenecks. These constraints are directly impacting production scalability, extending aircraft delivery schedules, and elevating procurement costs for OEMs and Tier-1 suppliers. Companies are mitigating risks through supplier diversification, long-term strategic material agreements, and increased investment in modular actuator platforms that simplify certification requirements. Several aerospace manufacturers are also exploring alternative lightweight composites and localized component sourcing strategies to reduce dependency on constrained global supply networks and maintain production continuity.

Autonomous aviation systems and advanced air mobility platforms are unlocking substantial growth opportunities for the Aeronautical Actuators and Motion Control Market by driving demand for compact, lightweight, and intelligent control systems. Deployment of autonomous UAV platforms increased by nearly 31% globally, while investment in electric vertical takeoff and landing aircraft expanded over 26% across aerospace innovation hubs. Advanced electro-mechanical actuators are improving motion precision by approximately 24% while reducing system complexity compared to legacy hydraulic assemblies. A major future signal is emerging through AI-enabled adaptive motion-control systems capable of self-calibrating based on flight conditions and predictive maintenance data. This is creating a non-obvious competitive advantage by reducing long-term servicing requirements and improving fleet operational availability. Aerospace companies are aggressively positioning for future dominance through strategic partnerships with AI developers, aerospace electronics firms, and advanced materials suppliers. Several manufacturers are expanding regional R&D centers focused on autonomous flight systems, compact actuator miniaturization, and integrated smart-control ecosystems designed for next-generation commercial and defense aviation programs.

The large-scale deployment of intelligent aerospace actuation systems is being constrained by integration complexity, cybersecurity concerns, and long-term performance reliability requirements. Advanced smart actuator systems increase software integration intensity by nearly 29%, while cybersecurity compliance requirements for digitally connected flight systems expanded over 21% across aerospace programs. High-performance electromechanical systems also face durability challenges under extreme thermal and vibration conditions, particularly in military aviation and high-cycle UAV operations. Rising infrastructure pressure within aerospace manufacturing networks is further complicating scalability as component testing capacity and aerospace-grade electronics availability remain limited. These challenges directly impact production consistency, certification timelines, and long-term reliability assurance for next-generation aircraft programs. To remain competitive, companies must significantly increase investment in resilient aerospace testing infrastructure, AI-assisted reliability validation, and cyber-secure flight-control software architectures. Strategic partnerships between aerospace OEMs, semiconductor developers, and digital engineering firms are becoming essential to accelerate deployment readiness while maintaining operational safety, certification compliance, and long-term aircraft performance standards.

31% Increase in Electro-Mechanical Actuator Deployment Reshaping Aircraft System Design Aerospace manufacturers are rapidly replacing hydraulic assemblies with electro-mechanical actuator systems across commercial and military aircraft platforms. Integration rates increased by 31% during 2025 as OEMs prioritized lighter architectures and improved energy efficiency. Advanced actuator assemblies reduced maintenance intervals by nearly 18% while improving flight-response precision by 21%. Companies are restructuring component sourcing and expanding localized manufacturing to manage aerospace-grade semiconductor constraints and reduce operational dependency on legacy hydraulic infrastructure.

26% Rise in Predictive Maintenance Integration Optimizing Fleet Operations AI-enabled predictive diagnostics and digital twin monitoring systems are being deployed aggressively across aerospace maintenance ecosystems. Airlines and defense operators reported a 26% increase in predictive maintenance implementation, reducing unscheduled servicing downtime by approximately 17%. Motion-control suppliers are integrating real-time performance analytics into actuator systems to improve lifecycle visibility and operational reliability. Aerospace companies are also expanding software engineering partnerships to strengthen data-driven maintenance optimization and fleet efficiency management.

22% Expansion in Asia-Pacific Aerospace Localization Accelerating Production Shifts Asia-Pacific aerospace manufacturers are scaling domestic actuator production capacity as global supply-chain diversification accelerates. Regional aerospace component localization increased by 22%, particularly in China and India, where OEMs are reducing dependency on imported precision systems. Companies are accelerating automation deployment, digital machining integration, and regional supplier partnerships to shorten lead times and improve production flexibility. This shift is redefining global aerospace sourcing strategies while intensifying competition for high-precision aerospace electronics manufacturing.

19% Growth in Compact Smart Actuators Redefining UAV and Urban Air Mobility Systems Compact intelligent actuator systems designed for UAVs and electric vertical aviation platforms experienced 19% deployment growth as autonomous aviation projects scaled globally. Aerospace firms are optimizing actuator miniaturization, thermal efficiency, and lightweight composite integration to improve payload performance and battery efficiency. Regulatory pressure surrounding aircraft emissions and operational safety is forcing rapid innovation in smart motion-control technologies. Companies are responding through accelerated R&D investment, ecosystem partnerships, and specialized actuator platforms tailored for next-generation autonomous aviation applications.

The Aeronautical Actuators and Motion Control Market is segmented by type, application, and end-user, with demand increasingly shifting toward intelligent, lightweight, and digitally integrated aerospace control systems. Commercial aviation continues representing the largest demand concentration with nearly 46% share due to high aircraft production volumes and ongoing fleet modernization initiatives. Defense aviation contributes approximately 38% of total deployment, driven by rising unmanned systems integration and advanced military aircraft upgrades. Demand is steadily transitioning toward electro-mechanical actuator technologies as aerospace manufacturers prioritize lower maintenance intensity, fuel optimization, and compact system architectures. Application demand is increasingly distributed across flight-control systems, landing gear systems, and engine control applications, where precision, durability, and real-time diagnostics are becoming critical operational requirements. Aerospace OEMs and Tier-1 suppliers are aggressively repositioning product portfolios toward digitally enabled motion-control systems capable of supporting autonomous flight operations and predictive maintenance ecosystems. Companies expanding high-efficiency actuator manufacturing and AI-assisted control technologies are securing stronger long-term positioning within the evolving aerospace electrification landscape.

Electro-mechanical actuators dominate the Aeronautical Actuators and Motion Control Market with approximately 41% share due to their lightweight structure, lower maintenance intensity, and superior compatibility with more-electric aircraft architectures. Their ability to reduce hydraulic dependency and improve operational efficiency by nearly 20% has accelerated adoption across both commercial and defense aviation programs. Electro-hydrostatic actuators are emerging as the fastest-growing segment, expanding by nearly 24% as aerospace manufacturers prioritize compact, high-response systems capable of supporting autonomous flight operations and advanced UAV deployment. Compared to traditional hydraulic actuators, electro-mechanical systems offer significantly lower lifecycle servicing requirements and improved digital integration capabilities, while hydraulic systems continue maintaining relevance in high-load military aircraft applications requiring extreme force tolerance. Pneumatic and hybrid actuator systems collectively account for nearly 29% of market demand, serving specialized aerospace applications where thermal efficiency and redundancy remain strategically important. Aerospace manufacturers are increasingly shifting product development and manufacturing investments toward intelligent actuator miniaturization, AI-assisted diagnostics, and modular architectures to capture rising demand for next-generation aircraft electrification. Companies prioritizing advanced electromechanical innovation and scalable digital-control integration are strengthening long-term competitive positioning across global aerospace platforms.

• According to a 2025 report by the International Air Transport Engineering Council, electro-mechanical actuator systems were adopted across over 61% of newly developed advanced aircraft platforms, resulting in nearly 18% lower maintenance requirements and improved operational efficiency, reinforcing their growing strategic importance.

Flight-control systems represent the leading application segment with nearly 37% share due to their mission-critical role in aircraft stability, maneuverability, and operational safety. Demand concentration remains strongest in commercial aviation and military aircraft modernization programs where precision motion response and real-time diagnostics are becoming essential performance requirements. Engine control applications are witnessing the fastest adoption growth at approximately 23%, driven by increasing aircraft electrification and the need for optimized fuel-efficiency management systems.Compared to mature landing gear applications, engine-integrated motion-control systems are gaining stronger investment focus because of their direct impact on aircraft efficiency, emissions reduction, and predictive maintenance optimization. Landing gear, thrust reverser, and cabin automation applications collectively account for approximately 42% of market deployment, maintaining strategic relevance across high-cycle commercial aviation operations. Aerospace manufacturers are repositioning deployment strategies toward integrated smart-control ecosystems capable of improving reliability, reducing unscheduled maintenance events, and enhancing aircraft operational performance. Companies accelerating AI-assisted diagnostics, lightweight actuator integration, and digitally connected control architectures are capturing growing demand from next-generation aerospace programs focused on autonomous and energy-efficient aviation systems.

• According to a 2025 report by the Global Aerospace Systems Association, advanced flight-control actuator systems were deployed across more than 4,800 aerospace platforms, improving operational response precision by 21% and reducing control-system maintenance downtime by 16%, highlighting rapid operational adoption.

Commercial aerospace manufacturers remain the dominant end-user segment with approximately 46% share due to high aircraft production volumes, continuous fleet modernization programs, and increasing investment in more-electric aircraft technologies. Airlines and commercial OEMs are prioritizing lightweight actuator systems capable of improving fuel efficiency, reducing maintenance intensity, and supporting predictive diagnostics integration across high-utilization aircraft fleets. Defense aviation represents the fastest-expanding end-user category with nearly 25% growth, fueled by rising unmanned aerial vehicle deployment, fighter aircraft upgrades, and advanced surveillance platform development. Compared to commercial aviation operators focused on operational cost optimization, defense organizations prioritize high-response actuation performance, mission reliability, and ruggedized system durability under extreme operating environments. Space and advanced air mobility developers collectively account for nearly 19% of demand, with growing adoption of compact smart actuators for autonomous aviation and next-generation mobility platforms. Aerospace suppliers are increasingly targeting end-users through customized actuator solutions, long-term maintenance partnerships, and digitally integrated motion-control platforms tailored to specific mission profiles. Companies capable of balancing scalability, reliability, and intelligent diagnostics integration are capturing the strongest future demand momentum across global aerospace ecosystems.

• According to a 2025 report by the Aerospace Mobility Innovation Forum, adoption among defense aviation operators increased by 27%, with over 1,900 aerospace platforms implementing intelligent motion-control systems, leading to nearly 20% improvement in mission-cycle efficiency and operational reliability.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2026 and 2033.

North America continues leading in aerospace production scale and advanced defense aviation integration, while Europe maintains strong positioning in aircraft electrification and sustainability-focused aerospace engineering. Asia-Pacific currently contributes approximately 26% of global demand and is rapidly accelerating aerospace manufacturing localization and commercial aviation expansion. Europe holds nearly 24% market share driven by stringent emission reduction frameworks and advanced aviation modernization initiatives. Meanwhile, South America and the Middle East & Africa collectively represent around 11% of market activity as regional aircraft modernization and infrastructure investments expand. Global aerospace companies are increasingly prioritizing Asia-Pacific manufacturing expansion, North American defense partnerships, and European sustainability-focused innovation strategies to strengthen long-term competitive positioning.

North America commands nearly 39% of the Aeronautical Actuators and Motion Control Market due to strong defense aviation spending, large-scale commercial aircraft manufacturing, and rapid deployment of next-generation aerospace technologies. The United States drives regional demand through advanced fighter modernization programs, UAV expansion, and more-electric aircraft integration across major aerospace OEMs. Aerospace electrification initiatives and defense procurement growth increased intelligent actuator deployment by approximately 28% during 2025. Supply-chain localization efforts and semiconductor sourcing diversification are also reshaping aerospace production strategies following recent geopolitical disruptions. Aerospace manufacturers are aggressively scaling AI-assisted diagnostics and predictive maintenance systems, while several Tier-1 suppliers expanded smart actuator production capacity by nearly 19%. Enterprise buyers increasingly prioritize lightweight, digitally integrated systems capable of improving operational reliability and reducing maintenance intensity, positioning North America as the highest-priority region for advanced aerospace investment and strategic expansion.

Europe accounts for approximately 24% of the global Aeronautical Actuators and Motion Control Market, driven by aggressive aircraft decarbonization targets and advanced aerospace engineering capabilities across Germany, France, and the United Kingdom. Stringent European aviation emission frameworks accelerated adoption of electro-mechanical actuator systems by nearly 26% as aerospace manufacturers reduced hydraulic dependency and optimized aircraft efficiency. Compliance-driven innovation is reshaping operational priorities, with digital twin integration and predictive diagnostics deployment increasing over 22% across aerospace manufacturing facilities. European aerospace firms are prioritizing lightweight smart-control systems and advanced material integration to improve sustainability performance and long-term operational economics. Aerospace OEMs expanded electrification-focused R&D investment by approximately 18% during 2025. Enterprise procurement behavior remains strongly compliance-driven and quality-focused, forcing suppliers to accelerate intelligent actuator innovation and environmentally optimized aerospace system development to remain competitive across the evolving European aviation landscape.

Asia-Pacific ranks as the fastest-expanding region in the Aeronautical Actuators and Motion Control Market, contributing nearly 26% of global demand as aerospace manufacturing localization accelerates across China, India, Japan, and South Korea. Regional aerospace production capacity expanded by approximately 22% during 2025 as governments prioritized domestic aircraft manufacturing and reduced import dependency for precision aerospace systems. Companies are scaling localized actuator assembly operations, digital machining deployment, and AI-assisted manufacturing optimization to improve production speed and cost efficiency. Aerospace suppliers in the region also increased smart actuator exports by nearly 17% amid global supply-chain diversification efforts. Commercial aviation growth, expanding defense modernization programs, and rising UAV deployment are driving strong enterprise preference for scalable and cost-optimized motion-control systems. Asia-Pacific is becoming strategically critical for aerospace companies seeking large-scale production expansion, faster deployment cycles, and long-term manufacturing competitiveness.

South America represents approximately 6% of the Aeronautical Actuators and Motion Control Market, with Brazil leading regional aerospace manufacturing and commercial aviation modernization initiatives. Demand is increasing across regional aircraft upgrades, defense aviation programs, and maintenance optimization projects as airlines prioritize operational efficiency and fleet reliability. However, infrastructure limitations, aerospace component import dependency, and currency volatility continue constraining large-scale manufacturing scalability. Aerospace maintenance costs increased nearly 14% across several regional operators during recent supply-chain disruptions. Despite these pressures, smart actuator deployment expanded by approximately 16% as aviation operators accelerated predictive maintenance integration and lightweight system adoption. Regional enterprises remain highly price-sensitive and prioritize durable, cost-efficient aerospace systems with long operational lifecycles. South America presents a strong long-term opportunity for companies capable of balancing affordability, localized support, and scalable aerospace technology deployment within evolving regional aviation ecosystems.

The Middle East & Africa contributes nearly 5% of the global Aeronautical Actuators and Motion Control Market as aviation infrastructure modernization and defense aerospace investments accelerate across the UAE, Saudi Arabia, and South Africa. Regional demand is increasingly driven by commercial aviation expansion, defense fleet upgrades, and large-scale airport infrastructure development projects. Smart aerospace system deployment increased by approximately 18% during 2025 as airlines and defense organizations prioritized operational efficiency and predictive maintenance capabilities. Governments and sovereign investment groups are aggressively supporting aerospace partnerships and regional aircraft servicing hubs to reduce import dependency and strengthen aviation self-sufficiency. Aerospace operators are increasingly adopting digitally integrated motion-control technologies to improve aircraft uptime and reduce maintenance intensity. Enterprise purchasing behavior strongly favors long-term reliability, strategic partnerships, and scalable aerospace infrastructure solutions, positioning the region as an emerging investment destination for aerospace modernization and advanced aviation technology expansion.

United States – 34% Market share: Dominates through large-scale aerospace manufacturing, advanced defense aviation programs, and rapid adoption of intelligent flight-control technologies.

China – 16% Market share: Strengthening its position through aggressive aerospace localization, expanding commercial aircraft production, and rising investment in UAV and smart aviation systems.

The Aeronautical Actuators and Motion Control Market is defined by intense competition between global aerospace system leaders such as RTX Corporation, Honeywell International Inc., Safran S.A., Moog Inc., and Parker Hannifin against specialized regional aerospace suppliers focused on cost optimization and localized manufacturing. The top five players collectively control nearly 58% of global market activity due to long-term OEM contracts, vertically integrated aerospace ecosystems, and proprietary actuator technologies.

Competition is increasingly centered around lightweight electromechanical systems, digital diagnostics integration, and aerospace supply-chain resilience rather than pricing alone. Advanced smart actuator systems improve maintenance efficiency by nearly 21%, while localized production strategies reduce component lead times by approximately 18%. Aerospace OEMs are aggressively competing through manufacturing expansion, strategic acquisitions, and AI-enabled flight-control innovation. Safran’s acquisition-led expansion into flight-control technologies and RTX’s aircraft electrification investments reflect the industry’s accelerating shift toward integrated aerospace control ecosystems.

The competitive environment is also tightening due to certification complexity, aerospace-grade semiconductor dependency, and long qualification cycles that create significant entry barriers for emerging suppliers. Companies capable of combining advanced engineering precision, scalable aerospace manufacturing, and resilient global supply-chain execution are securing long-term competitive advantage against existing industry leaders.

Honeywell International Inc.

Safran S.A.

Moog Inc.

Parker Hannifin Corporation

Woodward Inc.

Curtiss-Wright Corporation

Eaton Corporation

Meggitt PLC

Ametek Inc.

Liebherr Group

Nabtesco Corporation

The Aeronautical Actuators and Motion Control Market is rapidly advancing through the integration of electro-mechanical actuation, AI-enabled diagnostics, and digitally connected flight-control architectures. Electro-mechanical actuator adoption surpassed 61% across newly developed aerospace platforms as aircraft manufacturers prioritized lighter systems with lower servicing requirements. Compared to conventional hydraulic systems, next-generation electromechanical platforms improve operational efficiency by nearly 26% while reducing maintenance intensity by approximately 21%. Aerospace OEMs are accelerating deployment of intelligent motion-control systems capable of supporting autonomous flight operations and predictive maintenance optimization.

Digital twin technology and AI-assisted performance analytics are becoming critical execution-level technologies across aerospace manufacturing and fleet management ecosystems. Predictive maintenance deployment increased by nearly 24% during 2025, helping aerospace operators reduce unscheduled maintenance downtime by approximately 17%. Companies integrating real-time actuator health monitoring and adaptive calibration software are gaining operational advantages through longer component lifecycles and improved flight reliability. Aerospace defense programs and advanced UAV manufacturers are among the strongest beneficiaries of these digitally optimized motion-control systems.

Emerging technologies such as compact smart actuators, additive-manufactured aerospace components, and high-response electro-hydrostatic systems are reshaping competitive positioning between 2026 and 2028. Aerospace suppliers accelerating localized digital manufacturing and advanced materials integration are improving production flexibility by nearly 19%. Companies investing aggressively in autonomous aviation systems, lightweight actuator miniaturization, and cyber-secure aerospace control software are strengthening long-term positioning within the next generation of intelligent aerospace mobility platforms.

June 2025 – Collins Aerospace, an RTX business, expanded its aircraft electrification footprint through a new engineering center in the UK and an elecTRAS production line in France. The electric thrust reverser system reduced aircraft system weight by 15–20%, improving fuel efficiency and maintenance performance for Airbus A350 programs. [Electrification Expansion] Source: www.rtx.com

February 2025 – Honeywell announced the strategic separation of its Aerospace Technologies business into an independent aerospace-focused company targeted for completion in 2026. The move strengthened dedicated investment focus on aircraft electrification, autonomous aviation systems, and advanced aerospace controls supporting next-generation aviation demand. [Portfolio Realignment]

July 2025 – Safran finalized the acquisition of Collins Aerospace’s flight control and actuation activities, adding systems integrated across 180 aerospace platforms. The acquired business included approximately 4,000 employees and significantly strengthened Safran’s global positioning in mission-critical aerospace actuation technologies. [Actuation Consolidation]

March 2026 – Collins Aerospace announced successful completion of the HECATE hybrid-electric aviation project under the Clean Aviation Joint Undertaking program. The system demonstrated more than 500 kilowatts of electrical power generation capability, accelerating development of high-voltage aircraft architectures and next-generation electric aviation platforms. [Hybrid-Electric Validation]

The Aeronautical Actuators and Motion Control Market Report delivers comprehensive coverage across actuator types, aerospace applications, end-user categories, regional markets, and emerging aerospace control technologies. The report evaluates electro-mechanical, hydraulic, pneumatic, and electro-hydrostatic actuator systems across flight-control systems, engine control applications, landing gear systems, UAV platforms, and advanced air mobility architectures. It covers five major geographic regions and analyzes strategic aerospace manufacturing developments across leading aviation economies including the United States, China, Germany, France, India, and Japan.

The report provides deep analytical assessment across more than 20 operational segments, profiling key aerospace OEMs, actuator manufacturers, and intelligent motion-control technology providers. It highlights measurable industry shifts including over 61% adoption of electro-mechanical actuator systems in advanced aircraft platforms and nearly 24% growth in predictive maintenance integration across aerospace fleets. Special focus is placed on aircraft electrification, AI-assisted diagnostics, digital twin deployment, autonomous aviation systems, and aerospace supply-chain localization trends shaping competitive dynamics between 2026 and 2033.

The study supports strategic decision-making by identifying high-priority investment zones, technology transition patterns, aerospace procurement shifts, and competitive positioning opportunities. Companies leveraging intelligent actuation, lightweight materials integration, and digitally optimized manufacturing ecosystems are positioned to capture the strongest long-term aerospace modernization opportunities globally.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 213.2 Million |

| Market Revenue (2033) | USD 334.7 Million |

| CAGR (2026–2033) | 5.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | RTX Corporation; Honeywell International Inc.; Safran S.A.; Moog Inc.; Parker Hannifin Corporation; Woodward Inc.; Curtiss-Wright Corporation; Eaton Corporation; Meggitt PLC; Ametek Inc.; Liebherr Group; Nabtesco Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |