Reports

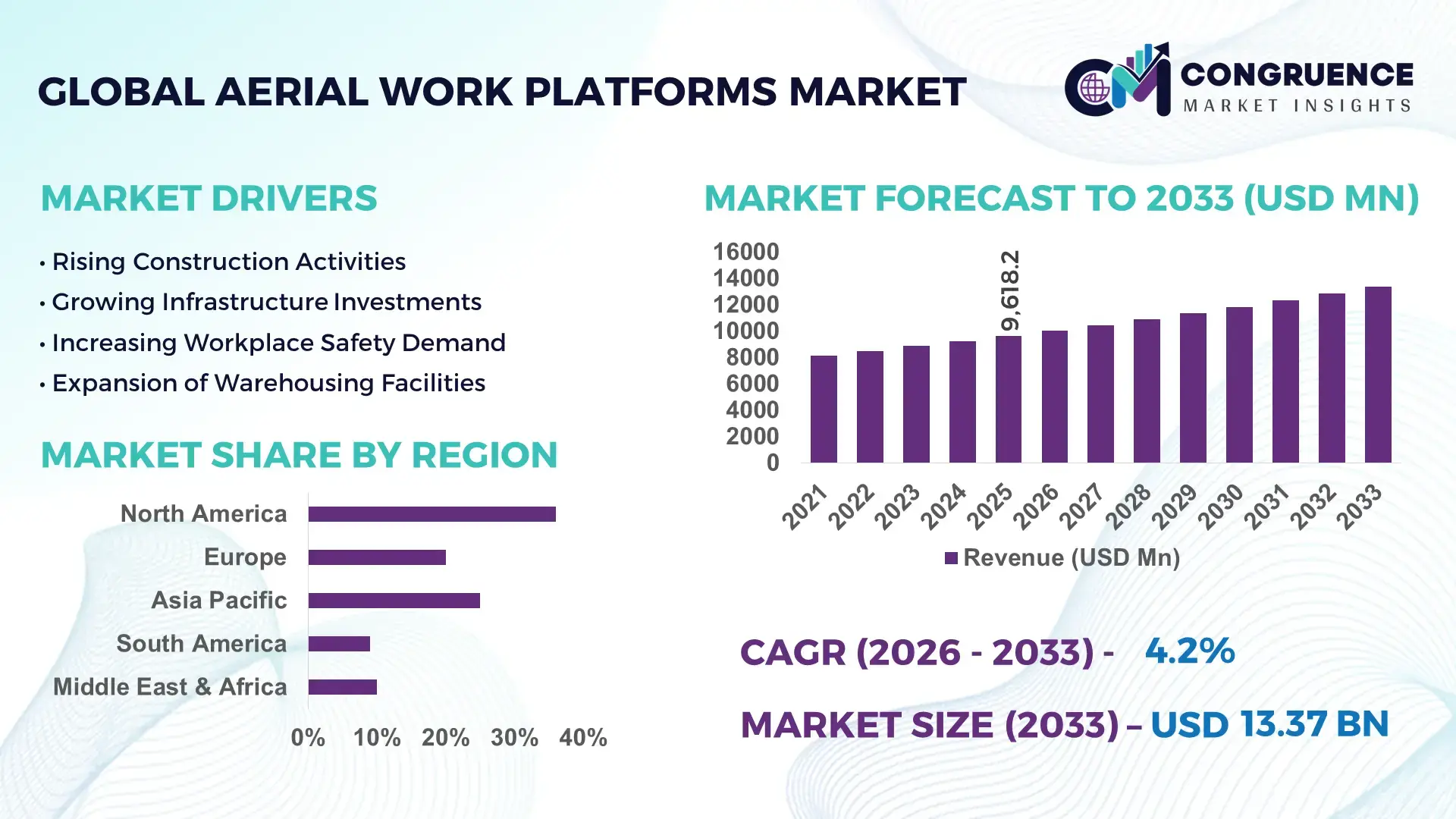

The Global Aerial Work Platforms Market was valued at USD 9618.24 Million in 2025 and is anticipated to reach a value of USD 13367.1 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. Electrified boom lifts and telematics-enabled scissor platforms are accelerating fleet modernization, with lithium-powered units reducing operating costs by nearly 18% and improving indoor deployment efficiency by over 25% across logistics, commercial construction, and industrial maintenance applications.

The United States continues to dominate the global aerial work platforms market with approximately 34% share, supported by over USD 18 billion in active infrastructure modernization programs and rapid warehouse automation deployment. Construction and utility maintenance sectors account for more than 58% of national equipment utilization, while electric-powered platforms represent nearly 41% of new fleet additions in 2026 compared to below 25% in 2021. Large rental companies are expanding smart fleet integration, improving equipment uptime by nearly 15%, while domestic manufacturing investments and reshoring initiatives strengthen supply resilience against ongoing Red Sea and Asia-Europe logistics disruptions.

Manufacturers prioritizing electric fleet expansion, AI-driven diagnostics, and rental network partnerships are positioned to secure higher-margin contracts across infrastructure, industrial servicing, and smart construction ecosystems.

Market Size & Growth: USD 9618.24 Million in 2025 reaching USD 13367.1 Million by 2033 at 4.2% CAGR, driven by electric fleet upgrades and infrastructure modernization.

Top Growth Drivers: Electric platform adoption rose 31%, rental fleet utilization increased 22%, and smart telematics integration expanded 27% globally.

Short-Term Forecast: By 2028, predictive maintenance systems reduce downtime by 19% while fleet operating efficiency improves 24%.

Emerging Technologies: AI diagnostics, lithium-ion battery systems, and IoT fleet monitoring improve energy efficiency by over 20%.

Regional Leaders: North America exceeds USD 4.1 billion with rental fleet expansion; Europe crosses USD 3 billion through emission-compliant equipment demand; Asia-Pacific approaches USD 3.8 billion from smart city projects.

Consumer/End-User Trends: Over 46% of contractors prefer rented aerial work platforms to reduce capital expenditure and maintenance costs.

Pilot/Case Example: In 2025, a large logistics warehouse modernization project improved elevated maintenance productivity by 28% using autonomous-ready scissor lifts.

Competitive Landscape: Leading manufacturers control nearly 48% market share, with major competition centered around electrification, digital fleet management, and compact platform design.

Regulatory & ESG Impact: Low-emission equipment adoption increased 33% after updated workplace emission standards and urban noise regulations across Europe.

Investment & Funding: Global investments surpassed USD 2.4 billion between 2024 and 2026, focused on battery production, regional assembly expansion, and rental partnerships.

Innovation & Future Outlook: Hybrid aerial platforms, remote operation systems, and AI-enabled safety analytics are reshaping high-growth industrial access strategies.

Construction and infrastructure projects contribute nearly 44% of total aerial work platform demand, followed by industrial maintenance and warehousing sectors with a combined 36% share. Electric boom lifts and compact indoor scissor lifts gained over 30% adoption growth due to emission regulations and smart facility expansion. Asia-Pacific demand strengthened through urban transit and manufacturing investments, while Europe accelerated low-noise fleet replacement amid stricter sustainability standards and supply chain localization efforts. Advanced connected fleet ecosystems and autonomous positioning features are set to define the next phase of competitive differentiation across global rental and equipment manufacturing markets.

The aerial work platforms market is transforming into a critical investment arena as infrastructure modernization, industrial automation, and urban maintenance projects accelerate globally. Rental operators and equipment manufacturers are aggressively optimizing fleet electrification and smart asset utilization to secure long-term service contracts and operational scale advantages. Tightened emission mandates and elevated worker safety standards are forcing rapid replacement of diesel-powered legacy fleets, particularly across North America and Europe, while Asia-Pacific construction expansion is reshaping global equipment demand distribution.

Lithium-powered aerial platforms improve energy efficiency by 28% while reducing maintenance costs by 21% compared to legacy hydraulic diesel systems. North America leads in deployment volume, while Europe leads in electrified platform adoption with nearly 46% of new fleet additions integrating low-emission systems and AI-enabled diagnostics. Over the next three years, predictive maintenance platforms are projected to reduce fleet downtime by 18% and increase rental utilization rates by 24%. ESG-focused fleet conversion is also becoming a direct competitive advantage, lowering urban compliance costs by nearly 15% and expanding access to government-backed infrastructure projects.

In 2025, a major logistics operator integrated connected scissor lifts across automated warehouses, improving maintenance response efficiency by 32% and reducing equipment idle time by 17%. Leading manufacturers are shifting capital allocation toward battery production, compact urban platforms, and digital fleet ecosystems to accelerate aftermarket profitability. Companies securing intelligent electrified fleets, regional manufacturing resilience, and predictive service capabilities are defining the next competitive hierarchy of the global aerial work platforms market.

Large-scale infrastructure expansion and stricter workplace safety regulations are accelerating aerial work platform replacement cycles across construction, warehousing, and industrial maintenance sectors. Electric-powered platforms recorded nearly 31% higher adoption in 2025 as contractors prioritized low-emission fleets for urban projects and indoor operations. Global rental fleet utilization increased by 22%, while connected equipment reduced service downtime by approximately 18%. Ongoing semiconductor plant construction in the United States and renewable energy installation projects across Europe are forcing faster equipment deployment and capacity expansion. In response, manufacturers are accelerating battery platform investments, expanding localized assembly operations, and forming strategic rental partnerships to secure long-term contracts and optimize supply responsiveness amid shifting regional procurement patterns globally.

Rising battery material costs, electronic component shortages, and freight volatility are constraining scalable aerial work platform deployment across price-sensitive markets. Lithium battery pack prices increased nearly 14% between 2024 and 2025, while delivery lead times for advanced boom lifts expanded by approximately 19% due to semiconductor supply concentration in East Asia. High financing costs and limited charging infrastructure are also delaying fleet electrification among mid-sized rental operators. These pressures directly increase procurement costs, compress rental margins, and slow replacement cycles for aging diesel fleets. To mitigate operational risk, manufacturers are diversifying supplier networks, securing long-term raw material agreements, and developing hybrid power platforms that reduce dependence on fully electric systems while maintaining compliance with evolving emission regulations globally.

Smart fleet ecosystems, autonomous diagnostics, and compact electric aerial platforms are redefining high-growth opportunities across dense urban construction and automated industrial facilities. AI-enabled telematics improved fleet productivity by nearly 26% in 2025, while predictive maintenance systems lowered unexpected repair costs by approximately 20%. Rapid smart city investments across Southeast Asia and Middle Eastern infrastructure corridors are creating strong demand for low-noise, high-efficiency access equipment. A major innovation shift toward modular battery-swapping systems is also accelerating equipment uptime and rental turnover rates. Companies are responding through aggressive R&D spending, regional manufacturing expansion, and software integration partnerships to build connected equipment ecosystems that strengthen recurring service revenue, optimize lifecycle management, and secure future dominance in digitally managed industrial access operations globally.

Grid infrastructure limitations, uneven charging accessibility, and advanced technician shortages are constraining long-term scalability of electrified aerial work platform fleets. Nearly 37% of rental operators report operational delays linked to inadequate fast-charging infrastructure, while advanced diagnostic maintenance costs increased by approximately 16% in 2025. Urban construction sites with restricted power access are also limiting deployment consistency for large electric boom lifts. These operational barriers reduce asset utilization efficiency and complicate fleet standardization strategies across multiple regions. To remain competitive, companies must accelerate charging ecosystem investments, strengthen technician training programs, and establish strategic energy partnerships that improve fleet reliability. Manufacturers failing to optimize service infrastructure and digital maintenance capabilities risk losing position in increasingly technology-driven equipment procurement cycles globally.

Electric fleet adoption increased 34% across urban projects in 2025, reshaping equipment deployment priorities. Contractors are replacing diesel-powered boom lifts with lithium-based platforms to comply with low-emission construction mandates and indoor safety regulations. Fleet operators reduced maintenance intervals by 21% while improving equipment uptime by nearly 18% through battery standardization. Manufacturers are accelerating compact electric platform production and restructuring supplier agreements to secure battery availability amid continuing logistics volatility.

AI-enabled fleet monitoring improved equipment utilization by 26%, redefining rental fleet operations globally. Rental companies are integrating predictive diagnostics and remote tracking systems to optimize asset allocation and reduce idle equipment by approximately 19%. Automated service scheduling lowered unexpected repair incidents by 16%, particularly across high-turnover warehouse and utility operations. Companies are scaling connected fleet ecosystems and partnering with software providers to strengthen aftermarket service retention and operational transparency.

Asia-Pacific platform deployment expanded 29%, while Europe accelerated low-noise equipment transition by 31%. Infrastructure-led demand across India, Southeast Asia, and the Middle East is forcing faster production localization and regional assembly expansion. In contrast, European contractors are prioritizing compact electric lifts for dense urban retrofitting projects where noise and emission restrictions tightened sharply in 2025. Manufacturers are optimizing regional product portfolios to balance volume growth against regulatory compliance pressures.

Rental-based procurement surpassed 46% of new equipment utilization, shifting capital allocation models. Mid-sized contractors increasingly prefer flexible access models to avoid rising financing costs and volatile equipment ownership expenses. Subscription-style maintenance agreements improved fleet servicing speed by 22% and reduced unplanned downtime by 14%. Equipment producers are responding through integrated financing partnerships, bundled telematics services, and direct rental network expansion, transforming recurring service revenue into a primary competitive lever.

The aerial work platforms market is segmented by type, application, and end-user, with demand concentrated around high-utilization construction and industrial operations. Boom lifts and scissor lifts together account for nearly 68% of equipment deployment due to their scalability and operational flexibility across infrastructure and warehouse environments. Construction and maintenance applications contribute over 40% of equipment usage, while logistics-driven demand is accelerating through warehouse automation and high-density storage expansion. Construction remains the dominant end-user segment, although utilities and telecommunications are rapidly increasing fleet adoption to improve maintenance response efficiency and worker safety compliance. Companies are strategically shifting toward electrified compact platforms and connected fleet systems to capture evolving urban and industrial demand patterns globally.

Scissor lifts dominate the aerial work platforms market with approximately 38% share due to their cost efficiency, high platform stability, and strong deployment across warehouses, commercial construction, and indoor maintenance operations. Their lower maintenance requirements and compatibility with electric power systems continue strengthening large rental fleet adoption. Boom lifts remain the most versatile heavy-access solution, but spider lifts are emerging as the fastest-growing segment with nearly 17% deployment growth driven by demand for compact maneuverability in urban infrastructure retrofitting and confined industrial spaces. Boom lifts currently maintain stronger outdoor infrastructure dominance, while spider lifts are capturing specialized access applications requiring lightweight mobility and minimal surface impact.

Vertical mast lifts, truck-mounted lifts, and spider lifts collectively account for nearly 34% of market demand, serving telecommunications servicing, utility maintenance, and narrow-access industrial operations. Truck-mounted lifts are gaining traction in utility line repair due to faster deployment capability and improved roadside operational safety. Manufacturers are accelerating production of hybrid boom lifts and compact electric scissor lifts while expanding telematics integration to optimize fleet monitoring. Investment focus is increasingly shifting toward electrified compact platforms where operational efficiency, urban compliance, and rental scalability are generating stronger long-term margins.

“According to a 2025 report by International Powered Access Federation, electric scissor lifts were adopted by over 52% of large rental fleet operators, resulting in nearly 23% lower maintenance costs and improved indoor operational efficiency, reinforcing their growing strategic importance.”

Construction and maintenance remains the leading application segment, contributing nearly 42% of aerial work platform utilization due to intensive deployment across commercial buildings, transport infrastructure, and energy projects. High equipment dependency, elevated worker safety standards, and rapid project turnaround requirements continue concentrating demand within this segment. Warehousing operations represent the fastest-growing application with approximately 19% deployment growth as automated distribution centers and high-rack storage facilities expand globally. Compared with mature construction usage, warehousing demand is shifting toward compact electric lifts optimized for continuous indoor mobility and low-noise operation.

Utility line repair, facility management, industrial installation, and painting and cleaning collectively account for approximately 44% of market activity. Utility providers are increasing truck-mounted lift deployment to improve maintenance response times and reduce outage-related service disruptions. Facility management operators are also accelerating connected platform adoption to streamline inspection cycles and reduce labor dependency. Equipment suppliers are repositioning product portfolios around low-emission compact systems and predictive maintenance services to capture higher-frequency urban applications. Demand is increasingly moving toward multi-purpose platforms capable of supporting both indoor automation environments and infrastructure-intensive outdoor maintenance operations.

“According to a 2025 report by Occupational Safety and Health Administration, aerial work platforms for warehousing operations were deployed across over 18,000 logistics facilities, improving elevated inventory handling efficiency by 27%, highlighting rapid operational adoption.”

Construction remains the dominant end-user segment with approximately 41% of aerial work platform demand due to continuous infrastructure expansion, high equipment utilization intensity, and strict worker safety compliance requirements. Large contractors are increasing electrified fleet procurement to improve operational efficiency and secure access to low-emission urban projects. Logistics and warehousing is the fastest-growing end-user segment with nearly 21% adoption growth, fueled by e-commerce expansion, automated storage systems, and high-frequency indoor maintenance requirements. Compared with construction’s large outdoor equipment focus, warehouse operators are prioritizing compact electric scissor lifts with advanced maneuverability and telematics integration.

Utilities, manufacturing, telecommunications, and the aviation industry collectively contribute approximately 46% of market demand through specialized elevated maintenance and servicing applications. Telecommunications providers are accelerating vertical mast lift deployment to support rapid network infrastructure upgrades and tower servicing efficiency. Aviation operators are also increasing use of compact articulated platforms to optimize aircraft maintenance turnaround times. Manufacturers are responding with sector-specific customization strategies, flexible rental agreements, and integrated digital fleet services. Future demand is increasingly shifting toward end-users requiring continuous uptime, predictive maintenance support, and emission-compliant fleet operations across high-density industrial environments.

“According to a 2025 report by International Labour Organization, adoption among logistics and warehousing operators increased by 24%, with over 11,500 facilities implementing electric aerial work platforms, leading to nearly 20% improvement in maintenance productivity and operational efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

North America continues leading global aerial work platform demand through large-scale infrastructure modernization, warehouse automation, and mature rental fleet penetration exceeding 62%. Europe accounts for nearly 28% of market activity and leads in electrified platform adoption, with over 46% of new fleet additions integrating low-emission systems due to tightening urban sustainability regulations. Asia-Pacific contributes approximately 31% of global equipment deployment and is accelerating through manufacturing expansion, smart city construction, and localized production scaling across China and India. Supply chain regionalization and battery sourcing diversification are reshaping production strategies globally. Companies are increasingly prioritizing Asia-Pacific for volume expansion, Europe for compliance-driven innovation, and North America for high-value fleet modernization and connected equipment deployment.

North America holds approximately 36% of global aerial work platform demand, driven by infrastructure upgrades, logistics automation, and utility maintenance expansion across the United States and Canada. Construction and warehousing applications together contribute nearly 61% of regional equipment utilization, while rental fleet penetration exceeds 62%, forcing faster fleet replacement cycles. Tightened workplace safety regulations and reshoring-related industrial projects are accelerating demand for electric boom lifts and connected scissor platforms. Rental operators increased telematics-enabled fleet deployment by 27% in 2025 to optimize asset utilization and reduce maintenance downtime. Enterprise buyers increasingly prioritize lifecycle efficiency, low-emission compliance, and predictive maintenance integration, making North America a critical region for high-margin fleet modernization and advanced equipment service expansion strategies.

Europe represents nearly 28% of global aerial work platform activity, with Germany, France, and the United Kingdom driving large-scale adoption across urban construction and industrial retrofitting projects. Strict emission compliance policies and low-noise urban operating standards are reshaping procurement behavior, with electric-powered platforms accounting for approximately 46% of new fleet additions in 2025. Contractors are accelerating compact equipment deployment to meet dense city infrastructure requirements while reducing operational emissions and energy costs. Fleet operators improved maintenance efficiency by nearly 18% through AI-driven diagnostics and connected fleet systems. Enterprise buyers remain strongly compliance-driven, prioritizing premium-quality electrified platforms with advanced safety systems, positioning Europe as the region forcing continuous innovation, operational adaptation, and ESG-focused product differentiation.

Asia-Pacific contributes approximately 31% of global aerial work platform deployment, led by China, India, and Southeast Asian infrastructure expansion programs. Large-scale manufacturing activity, smart city development, and logistics warehouse construction are accelerating regional equipment demand and localized production investment. Domestic manufacturers increased compact electric platform output by nearly 29% in 2025 to support urban infrastructure and industrial maintenance projects. Rental adoption is also rising rapidly as contractors prioritize faster deployment and lower upfront ownership costs. Enterprise buyers across the region strongly favor scalable, cost-efficient equipment capable of supporting high-volume project execution. Manufacturers are expanding assembly capacity, strengthening regional supply chains, and accelerating digital fleet integration, making Asia-Pacific the most critical region for long-term scale expansion and production competitiveness.

South America accounts for approximately 7% of global aerial work platform demand, with Brazil and Chile leading deployment across mining, infrastructure rehabilitation, and industrial maintenance sectors. Construction modernization and energy infrastructure upgrades are supporting rising equipment utilization, particularly for boom lifts and truck-mounted platforms. However, high financing costs and import dependency continue constraining large-scale electrified fleet adoption across price-sensitive markets. Rental fleet deployment increased by nearly 18% in 2025 as contractors shifted toward flexible access models to manage capital expenditure pressures. Buyers increasingly prioritize durable, multi-purpose equipment with lower maintenance requirements and localized servicing support. The region presents strong infrastructure-driven growth potential, but companies must balance expansion opportunities against operational cost volatility and uneven equipment financing accessibility.

The Middle East & Africa region contributes nearly 9% of global aerial work platform demand, driven by large-scale infrastructure, oil and gas maintenance, and commercial construction activity across Saudi Arabia, the United Arab Emirates, and South Africa. Industrial diversification programs and smart city investments are accelerating demand for advanced boom lifts and compact electric access equipment. Equipment deployment across infrastructure megaprojects increased by approximately 24% in 2025, while rental fleet utilization expanded by nearly 19% due to faster project execution requirements. Enterprise buyers increasingly prefer rental-based access solutions with integrated maintenance support to improve operational flexibility. Manufacturers are strengthening regional partnerships and service networks, positioning the region as a strategically important market for infrastructure-led expansion and long-cycle industrial equipment demand.

United States Aerial Work Platforms Market – 34% Share: Dominates through extensive infrastructure modernization, high rental fleet penetration, and strong warehousing and industrial maintenance demand.

China Aerial Work Platforms Market – 21% Share: Leads rapid production scaling and infrastructure-driven deployment supported by localized manufacturing expansion and smart city construction activity.

The aerial work platforms market is dominated by global OEM leaders including JLG Industries, Terex Corporation, Haulotte Group, Sinoboom, and Zoomlion competing aggressively against regional manufacturers and rental-focused equipment suppliers. The top five players collectively control nearly 52% of global market activity, with competition centered on electrification, telematics integration, supply chain resilience, and fleet operating efficiency. Premium manufacturers are differentiating through AI-enabled diagnostics and lithium-powered platforms that improve maintenance efficiency by approximately 20%, while cost-focused Asian producers compete through localized manufacturing and faster delivery cycles reducing lead times by nearly 18%. Companies are accelerating regional assembly expansion, battery partnerships, and vertical integration strategies to secure component availability amid ongoing logistics pressure. Market consolidation is intensifying as rental operators prioritize connected fleet ecosystems and lifecycle service contracts. Winning in this market increasingly requires electrified product depth, digital fleet intelligence, regional production agility, and strong aftermarket service infrastructure.

JLG Industries

Terex Corporation

Haulotte Group

Sinoboom Intelligent Equipment

Zoomlion Heavy Industry Science & Technology

Zhejiang Dingli Machinery

Aichi Corporation

Tadano Ltd.

Manitou Group

Skyjack

MEC Aerial Work Platforms

Snorkel International

Niftylift Limited

Linamar Corporation

Electric drive systems, IoT-enabled telematics, and lithium-ion battery integration are currently reshaping aerial work platform operations across construction, warehousing, and industrial maintenance sectors. Electric scissor lifts reduce maintenance costs by nearly 23% while improving indoor operational efficiency by approximately 28% compared to diesel-powered legacy systems. More than 46% of newly deployed urban platforms in 2026 integrate low-emission electric architecture, particularly across Europe and North America. Rental operators are accelerating connected fleet adoption to optimize asset tracking, reduce idle equipment, and strengthen lifecycle profitability through predictive maintenance systems.

AI-driven diagnostics, remote fleet management, and over-the-air software updates are emerging as major competitive differentiators between premium manufacturers and low-cost regional suppliers. Connected telematics platforms improved fleet utilization by nearly 26% while reducing unexpected maintenance incidents by approximately 18% in 2025. Companies integrating Bluetooth mesh connectivity and digital analyzer systems are optimizing multi-site equipment deployment and minimizing technician response delays. Manufacturers focusing on intelligent fleet ecosystems are securing stronger aftermarket retention and higher-value infrastructure contracts compared to companies competing primarily on equipment pricing.

Between 2026 and 2028, autonomous positioning assistance, modular battery-swapping systems, and AI-powered load management are expected to redefine fleet scalability and uptime performance. Compact electric rough-terrain platforms capable of full-height movement are improving operational productivity by nearly 20% across logistics and infrastructure projects. Companies investing early in software-integrated electrified fleets, smart diagnostics, and energy-efficient platform engineering are positioning themselves to capture high-frequency rental demand and compliance-driven urban deployment opportunities globally.

April 2025 – JLG Industries expanded its ClearSky Smart Fleet IoT platform with Digital Analyzer Reader, Automatic Site Networks, and Elevation-Based Localization features, improving real-time fleet diagnostics and multi-site tracking efficiency. The platform strengthened remote maintenance capability and reduced manual equipment monitoring complexity for rental operators. [Connected Fleet Shift] Source: (JLG Industries)

February 2025 – JLG Industries launched the ES2646 electric-drive scissor lift Aviation Package integrating ultrasonic detection and LiDAR sensing technology for aircraft maintenance applications. The system enhanced contact-free servicing precision and improved elevated maintenance safety performance across aviation assembly operations. [Aviation Safety Upgrade] Source: (JLG Industries)

September 2024 – Haulotte Group introduced the HS5390 E MAX electric rough-terrain scissor lift with full-height driving capability, reducing unnecessary repositioning cycles and improving operational productivity on linear construction applications. The platform expanded electric equipment usability across both indoor and outdoor high-access environments. [Electric Terrain Expansion] Source:(haulotte-usa.com)

August 2025 – Haulotte Group launched the next-generation HA20 E and HA20 E PRO articulated boom lifts featuring two-day rough-terrain electric operation capability and zero-emission performance. The deployment strengthened contractor demand for low-noise urban infrastructure equipment while supporting compliance-focused fleet modernization strategies. [Zero-Emission Scaling] Source: (haulotte.in)

This report delivers comprehensive analysis across aerial work platform types including scissor lifts, boom lifts, vertical mast lifts, truck-mounted lifts, and spider lifts, alongside key applications such as construction and maintenance, warehousing operations, utility line repair, industrial installation, and facility management. End-user coverage spans construction, logistics and warehousing, utilities, manufacturing, telecommunications, and aviation industries across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study also evaluates emerging technologies including lithium-powered electric platforms, AI-enabled telematics, predictive diagnostics, modular battery systems, and connected fleet ecosystems shaping equipment deployment between 2026 and 2033.

The report analyzes more than 15 strategic market segments and profiles major global manufacturers competing through electrification, digital fleet integration, and localized production expansion. Electric-powered platform adoption exceeded 46% across urban fleet additions, while telematics-enabled fleet systems improved utilization efficiency by nearly 26% in high-frequency rental operations. Regional insights compare infrastructure-driven demand concentration, compliance-led innovation shifts, and production localization trends impacting competitive positioning.

The report supports investment planning, product strategy, regional expansion, supply chain optimization, and competitive benchmarking by identifying operational shifts, adoption patterns, technology deployment trends, and evolving customer procurement behavior across global aerial work platform ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9618.24 Million |

|

Market Revenue in 2033 |

USD 13367.1 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

JLG Industries, Terex Corporation, Haulotte Group, Sinoboom Intelligent Equipment, Zoomlion Heavy Industry Science & Technology, Zhejiang Dingli Machinery, Aichi Corporation, Tadano Ltd., Manitou Group, Skyjack, MEC Aerial Work Platforms, Snorkel International, Niftylift Limited, Linamar Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |