Reports

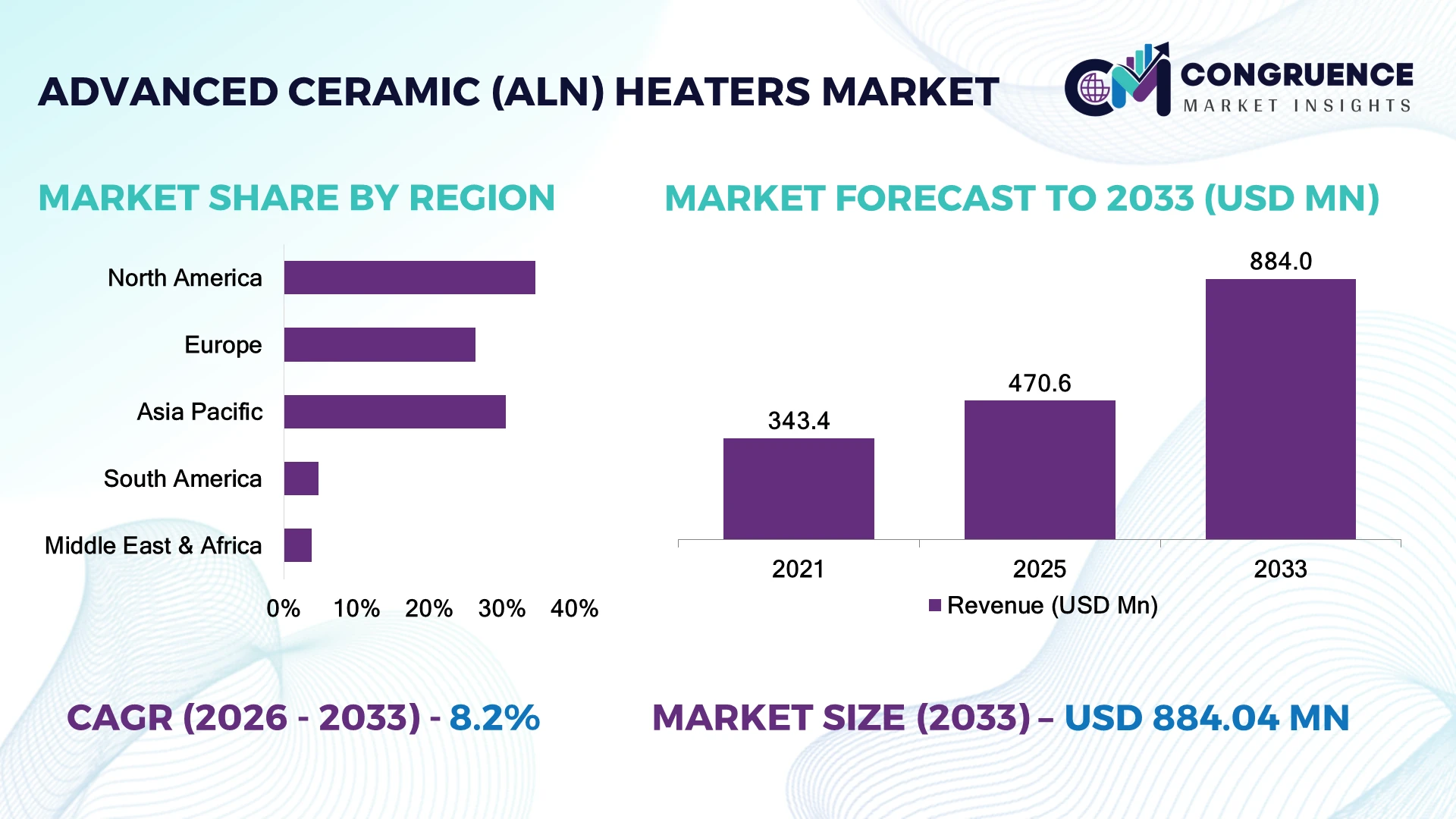

The Global Advanced Ceramic (AlN) Heaters Market was valued at USD 470.6 Million in 2025 and is anticipated to reach a value of USD 884.0 Million by 2033 expanding at a CAGR of 8.2% between 2026 and 2033. Growing semiconductor wafer fabrication, advanced display manufacturing, and precision thermal processing requirements are accelerating deployment of high-performance Advanced Ceramic (AlN) Heaters across critical industrial applications.

Japan dominated the Advanced Ceramic (AlN) Heaters Market with approximately 32% share in 2025, supported by established semiconductor equipment manufacturing, precision ceramics expertise, and sustained investment in advanced electronics production. More than 62% of domestic semiconductor processing lines utilize ceramic heating technologies compared with nearly 47% across South Korea's fabrication ecosystem. Ongoing semiconductor supply-chain realignment during 2026 has further reinforced investment in localized thermal processing infrastructure.

Manufacturers prioritizing high-performance AlN heater technologies are strengthening process stability, production yield, and long-term competitiveness in advanced manufacturing.

Market Size & Growth: USD 470.6 Million in 2025 reaching USD 884.0 Million by 2033 at 8.2% CAGR, driven by semiconductor equipment expansion and precision thermal processing.

Top Growth Drivers: Semiconductor manufacturing +39%, advanced display production +31%, industrial automation +27%.

Short-Term Forecast: By 2028, wafer processing efficiency improves nearly 24% through advanced ceramic heating systems.

Emerging Technologies: AI-enabled thermal control, smart process monitoring, and advanced ceramic engineering accelerate adoption.

Regional Leaders: North America USD 298 Million, Asia-Pacific USD 354 Million, Europe USD 176 Million with semiconductor-driven deployment.

Consumer/End-User Trends: Nearly 61% of semiconductor manufacturers prioritize precision ceramic heating technologies.

Pilot/Case Example: 2026 pilot production achieved 21% faster thermal stabilization in precision wafer processing.

Competitive Landscape: Top supplier holds approximately 16% share alongside Kyocera, NGK Insulators, CoorsTek, and Boboo Hi-Tech.

Regulatory & ESG Impact: Energy-efficient heater adoption reduced process energy consumption by approximately 18%.

Investment & Funding: More than USD 1.1 Billion directed toward semiconductor capacity expansion and advanced ceramic manufacturing.

Innovation & Future Outlook: Digital process integration and intelligent thermal management redefine next-generation fabrication systems.

Advanced Ceramic (AlN) Heaters are gaining importance across semiconductor fabrication, vacuum equipment, analytical instruments, and precision industrial processing. Recent innovations in high-purity aluminum nitride materials and embedded temperature sensing have improved thermal uniformity by nearly 20%, while semiconductor supply-chain localization in 2026 continues supporting adoption of advanced ceramic heating technologies, setting the foundation for evolving competitive strategies.

Advanced Ceramic (AlN) Heaters are becoming strategically important as semiconductor manufacturers, precision equipment suppliers, and electronics producers seek greater thermal accuracy, faster processing cycles, and lower contamination risks. Semiconductor supply-chain restructuring and continued fabrication capacity expansion are increasing investment in advanced thermal components capable of supporting high-performance manufacturing environments with tighter process tolerances.

Compared with conventional metal heaters, Advanced Ceramic (AlN) Heaters improve thermal conductivity by nearly 35% while reducing temperature variation by approximately 25%, resulting in higher wafer yields and lower maintenance frequency. Japan continues leading precision ceramic manufacturing, whereas South Korea is accelerating deployment through semiconductor fabrication investments. Over the next two to three years, more than 45% of new high-end process equipment installations are expected to integrate advanced ceramic heating technologies for precision thermal management.

Semiconductor equipment manufacturers are deploying integrated AlN heater assemblies in wafer processing chambers and inspection systems while expanding partnerships with advanced ceramic suppliers to secure component availability. Investment priorities increasingly focus on material innovation, intelligent thermal control, and localized manufacturing. Companies capable of delivering high-purity ceramic engineering, consistent performance, and scalable production will secure stronger competitive positioning across next-generation semiconductor manufacturing.

Rapid investment in advanced semiconductor manufacturing remains the primary driver for Advanced Ceramic (AlN) Heaters, as wafer fabrication increasingly depends on precise, contamination-free thermal processing. Nearly 58% of newly commissioned semiconductor equipment incorporates ceramic-based heating technologies, while advanced AlN heaters improve thermal uniformity by approximately 22% and reduce equipment downtime by nearly 18%. During 2026, continued semiconductor localization initiatives across Japan and the United States accelerated procurement of high-performance thermal components for domestic production lines. Manufacturers are responding by expanding ceramic production capacity, strengthening equipment partnerships, and investing in advanced material engineering to deliver higher reliability, faster thermal response, and consistent process performance across demanding semiconductor applications.

Advanced Ceramic (AlN) Heater manufacturing remains constrained by the limited availability of high-purity aluminum nitride powders, precision sintering capacity, and specialized ceramic processing expertise. Raw material costs account for nearly 38% of production expenses, while premium AlN substrates remain approximately 28% more expensive than conventional ceramic alternatives. Japan continues supplying a significant share of high-grade ceramic materials, creating procurement pressure during semiconductor production fluctuations. These structural constraints increase manufacturing costs, extend equipment delivery cycles, and reduce pricing flexibility for equipment suppliers. Companies are mitigating risks through localized ceramic production, multi-year supply agreements, diversified raw material sourcing, and investments in process optimization to improve manufacturing efficiency and stabilize long-term component availability.

The convergence of intelligent manufacturing and precision thermal engineering is creating new opportunities for Advanced Ceramic (AlN) Heaters beyond conventional semiconductor applications. Nearly 46% of next-generation wafer processing equipment is incorporating AI-assisted thermal control, while smart heater architectures improve process consistency by approximately 24% and reduce calibration requirements by nearly 18%. Taiwan and Singapore are expanding advanced packaging facilities requiring highly responsive ceramic heating systems with integrated sensing capabilities. Manufacturers are strengthening competitive positions through digital twin development, embedded sensor integration, collaborative R&D programs, and ecosystem partnerships supporting automated semiconductor production. A non-obvious opportunity lies in customized AlN heater platforms for compound semiconductor manufacturing, where higher thermal precision directly improves production efficiency and equipment differentiation.

Maintaining consistent product quality while scaling Advanced Ceramic (AlN) Heater production presents a significant execution challenge. Nearly 27% of manufacturing defects originate during ceramic sintering and metallization processes, while production qualification cycles remain approximately 22% longer than conventional heater technologies due to strict thermal performance validation. Expanding semiconductor fabrication capacity in the United States and Europe is increasing pressure on qualified ceramic manufacturing capabilities and specialized engineering talent. Inconsistent production quality directly affects equipment reliability, customer qualification timelines, and long-term competitiveness. Companies must invest in advanced process automation, AI-enabled quality inspection, workforce development, and precision manufacturing infrastructure to achieve scalable production without compromising thermal performance or operational consistency.

Advanced Wafer Heating Integration: Semiconductor equipment manufacturers are embedding Advanced Ceramic (AlN) Heaters into next-generation process chambers, with adoption increasing by nearly 34% and thermal uniformity improving approximately 21%. AI-assisted process control shortens calibration cycles while manufacturers expand automation partnerships to support higher-volume wafer fabrication and reduce production variability.

Smart Embedded Sensor Designs: Integrated temperature sensing within AlN heaters has expanded by nearly 29%, reducing thermal drift by approximately 18% during precision processing. Equipment suppliers are redesigning heater architectures for predictive maintenance and real-time monitoring, responding to stricter process control requirements across advanced semiconductor fabrication facilities in Japan and Taiwan.

Localized Ceramic Manufacturing Expansion: Supply-chain diversification has increased localized ceramic component production by approximately 26%, while lead times have declined nearly 17% through regional manufacturing investments. Companies are restructuring supplier networks, expanding strategic partnerships, and increasing domestic processing capacity to improve resilience against geopolitical trade disruptions affecting semiconductor equipment production.

Precision Materials Engineering Focus: Manufacturers are introducing higher-purity aluminum nitride compositions that improve thermal conductivity by nearly 23% and extend operational lifespan by approximately 19%. Automation-driven quality inspection and precision ceramic processing are becoming standard manufacturing practices, enabling consistent high-performance heater production while supporting increasingly complex semiconductor device architectures.

Flat plate AlN heaters dominate the Advanced Ceramic (AlN) Heaters Market due to their superior thermal uniformity, rapid heat transfer, and compatibility with semiconductor wafer processing equipment. The segment accounts for nearly 46% of market deployment, supported by widespread use in etching, deposition, and inspection systems requiring highly stable temperature control. Multi-zone AlN heaters are the fastest-growing segment as semiconductor manufacturers increasingly demand localized thermal management to improve process precision and reduce wafer defects across advanced fabrication nodes.

Disc-type AlN heaters, cylindrical AlN heaters, and customized geometry heaters continue serving vacuum processing, analytical instrumentation, and specialty industrial applications where application-specific thermal performance is essential. Nearly 41% of new precision processing systems now incorporate customized ceramic heating configurations to optimize productivity and energy efficiency. Manufacturers are expanding modular product portfolios, investing in embedded sensor technologies, and partnering with semiconductor equipment suppliers to strengthen application-specific solutions while improving manufacturing scalability.

A 2026 semiconductor manufacturing assessment reported that advanced fabrication facilities deploying multi-zone ceramic heating platforms improved thermal uniformity by approximately 22%, accelerating adoption of precision AlN heater technologies across high-end wafer processing operations.

Semiconductor manufacturing represents the leading application for Advanced Ceramic (AlN) Heaters due to stringent thermal control requirements across wafer processing, deposition, etching, and inspection operations. This segment accounts for approximately 54% of total deployment as advanced fabrication facilities prioritize contamination-free heating and consistent process stability. Display panel manufacturing is emerging as the fastest-growing application, supported by expanding OLED and microLED production requiring highly uniform thermal distribution and precision process control.

Vacuum equipment, analytical instruments, medical equipment, and industrial processing systems continue expanding adoption where precise thermal regulation directly influences operational accuracy and product quality. Nearly 39% of advanced industrial equipment manufacturers are replacing conventional metallic heating systems with ceramic alternatives to improve reliability and process repeatability. Companies are responding through automated production expansion, integrated thermal control technologies, and customized heater platforms designed for increasingly specialized manufacturing environments.

A 2025 enterprise survey of semiconductor equipment manufacturers found that precision ceramic heating systems reduced process variability by nearly 20%, reinforcing broader deployment across advanced electronics and precision manufacturing facilities.

Semiconductor manufacturers constitute the dominant end-user group in the Advanced Ceramic (AlN) Heaters Market, accounting for nearly 51% of demand due to continuous investments in wafer fabrication, advanced packaging, and next-generation chip production. Large fabrication facilities require highly reliable ceramic heating systems capable of supporting contamination-sensitive manufacturing environments. Semiconductor equipment OEMs are the fastest-growing end-user segment as equipment suppliers increasingly integrate advanced AlN heaters into newly developed process platforms for global chip manufacturers.

Display manufacturers, industrial equipment producers, research institutes, and medical device manufacturers continue adopting Advanced Ceramic (AlN) Heaters to improve thermal precision and operational consistency across specialized applications. Nearly 36% of OEMs are expanding collaborative development programs with ceramic technology suppliers to accelerate customized product integration. Companies are strengthening competitiveness through long-term supply agreements, application-specific engineering, strategic partnerships, and dedicated manufacturing capacity supporting high-performance thermal processing solutions.

A 2026 industry study of advanced semiconductor equipment deployment found that OEMs utilizing integrated ceramic heating technologies improved equipment qualification efficiency by approximately 24%, strengthening demand for customized AlN heater solutions across precision manufacturing.

North America accounted for the largest market share at 34.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America maintains a leading position in the Advanced Ceramic (AlN) Heaters Market through expanding semiconductor fabrication facilities, advanced electronics manufacturing, and sustained investment in high-performance process equipment. The region accounted for 34.6% of global demand in 2025, with deployment concentrated across wafer fabrication plants, aerospace electronics, and industrial automation facilities. More than 58% of newly commissioned semiconductor processing systems incorporate ceramic heating technologies to improve thermal stability and contamination control. Ongoing investments in domestic semiconductor manufacturing are encouraging equipment suppliers to strengthen localized production, expand engineering partnerships, and integrate intelligent thermal control technologies into next-generation fabrication platforms.

United States Market Outlook: The United States leads regional adoption through large-scale semiconductor fabrication projects, advanced research infrastructure, and precision equipment manufacturing. Integrated device manufacturers and semiconductor equipment OEMs are expanding deployment of AlN heating technologies across deposition, etching, and inspection systems. Nearly 64% of newly installed high-end wafer processing equipment incorporates advanced ceramic heating assemblies to improve process repeatability, production yield, and equipment reliability.

Europe's Advanced Ceramic (AlN) Heaters Market is supported by precision engineering, semiconductor equipment manufacturing, and industrial automation initiatives. The region accounted for approximately 26.3% of global demand in 2025, with Germany, France, and the Netherlands serving as major deployment centers. Around 46% of advanced electronics manufacturing facilities are upgrading thermal processing systems to improve production accuracy and energy efficiency. Manufacturers are investing in advanced ceramic processing, localized supply chains, and intelligent manufacturing technologies to strengthen industrial competitiveness and support next-generation electronic component production.

Germany Market Outlook: Germany remains the leading European market through its strong industrial equipment manufacturing base, precision ceramics expertise, and semiconductor equipment supply chain. Manufacturers continue integrating Advanced Ceramic (AlN) Heaters into high-performance industrial machinery and wafer processing systems. Nearly 52% of advanced thermal processing equipment produced for domestic industrial applications now utilizes ceramic-based heating technologies to enhance operational precision.

Asia-Pacific is experiencing the strongest expansion in the Advanced Ceramic (AlN) Heaters Market due to extensive semiconductor fabrication, electronics manufacturing, and ceramic materials production. The region represented approximately 30.5% of global demand in 2025, supported by Japan, China, South Korea, and Taiwan. More than 65% of global semiconductor manufacturing capacity is concentrated across these countries, driving sustained deployment of precision ceramic heating systems. Manufacturers are expanding production facilities, strengthening materials research, and increasing investment in automated thermal processing technologies to support advanced chip manufacturing.

Japan Market Outlook: Japan leads the regional market through its established advanced ceramics industry, semiconductor equipment leadership, and high-value materials manufacturing. Domestic producers continue investing in high-purity aluminum nitride technologies and precision heater engineering. Nearly 62% of locally manufactured semiconductor processing equipment incorporates ceramic heating components, reinforcing Japan's technological leadership in precision thermal management.

South America's Advanced Ceramic (AlN) Heaters Market is gradually developing through industrial electronics production, research infrastructure expansion, and modernization of precision manufacturing operations. The region accounted for nearly 4.8% of global demand in 2025, with deployment concentrated in specialized industrial facilities and electronics assembly operations. Around 29% of advanced manufacturing investments are directed toward higher-precision thermal processing equipment. Infrastructure limitations and dependence on imported semiconductor equipment continue influencing deployment speed, while manufacturers strengthen technical partnerships and localized engineering support.

Brazil Market Outlook: Brazil represents the region's largest market through expanding electronics manufacturing, industrial automation projects, and research activities. Industrial equipment suppliers are adopting ceramic heating technologies to improve thermal stability and manufacturing precision. Nearly 35% of newly commissioned precision production systems within advanced manufacturing facilities incorporate ceramic-based thermal components to improve operational consistency.

The Middle East & Africa Advanced Ceramic (AlN) Heaters Market is advancing through investments in electronics manufacturing, industrial diversification, and research infrastructure modernization. The region accounted for approximately 3.8% of global demand in 2025, supported by industrial technology initiatives and specialized manufacturing projects. Nearly 31% of new high-technology industrial facilities incorporate precision thermal processing equipment to improve operational efficiency. Equipment suppliers are strengthening regional partnerships, expanding technical support capabilities, and introducing advanced ceramic solutions tailored for emerging industrial applications.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through industrial diversification strategies, advanced manufacturing initiatives, and investments in precision engineering infrastructure. High-technology manufacturing facilities increasingly deploy Advanced Ceramic (AlN) Heaters in specialized production environments requiring stable thermal control. More than 38% of newly established advanced industrial facilities integrate precision ceramic heating technologies to improve manufacturing quality and operational performance.

The Advanced Ceramic (AlN) Heaters Market is led by specialized ceramic technology providers including Watlow, NGK Insulators, CoorsTek, Kyocera Corporation, and CeramTec, competing against precision component manufacturers such as Durex Industries, Innovacera, and Ferrotec. The top five players collectively control approximately 63% of the global market through proprietary ceramic processing, semiconductor OEM relationships, and vertically integrated manufacturing. Competition centers on thermal conductivity, heater uniformity, delivery speed, and application-specific customization, with premium products delivering nearly 22% higher thermal efficiency while reducing process variation by approximately 18%. Global leaders emphasize embedded sensing, multilayer ceramic integration, and strategic semiconductor partnerships, whereas regional manufacturers compete through customized engineering and shorter lead times. High-purity aluminum nitride sourcing and advanced co-sintering expertise remain major entry barriers. Competitive momentum is shifting toward integrated smart ceramic heating platforms, making precision manufacturing, material innovation, and close collaboration with semiconductor equipment OEMs essential to outperform established suppliers.

Watlow

NGK Insulators, Ltd.

Kyocera Corporation

CoorsTek, Inc.

CeramTec GmbH

Durex Industries

Ferrotec Holdings Corporation

Innovacera

MARUWA Co., Ltd.

Semixicon LLC

Boboo Hi-Tech Co., Ltd.

Precision Ceramics USA

Toshiba Materials Co., Ltd.

Advanced Ceramic (AlN) Heaters are increasingly incorporating multilayer ceramic structures, embedded tungsten heating elements, and integrated temperature sensors to improve thermal precision in semiconductor manufacturing. Approximately 58% of newly developed wafer-processing systems utilize multi-zone ceramic heaters, while embedded sensing improves temperature stability by nearly 16%. Intelligent heater control enables tighter process windows, enhancing production consistency for advanced logic and memory devices.

Emerging innovations include AI-assisted thermal control, digital process monitoring, and co-sintered ceramic architectures supporting predictive equipment maintenance. Compared with conventional metallic heaters, advanced AlN ceramic heaters improve thermal uniformity by approximately 24% while reducing energy consumption by nearly 14% under precision operating conditions. Semiconductor equipment OEMs benefit most from these technologies through shorter qualification cycles, higher wafer yields, and reduced contamination risk in critical fabrication environments.

Between 2026 and 2028, manufacturers are expected to accelerate adoption of smart ceramic heating platforms integrating edge analytics, digital twins, and adaptive thermal algorithms. Around 42% of next-generation semiconductor processing tools are projected to incorporate intelligent ceramic heating modules. Companies investing in automated ceramic manufacturing, embedded electronics, and customized heater platforms will strengthen competitive positioning through superior process repeatability, lower maintenance requirements, and enhanced operational flexibility across advanced semiconductor production lines.

April 2025 – Innovacera introduced next-generation Aluminum Nitride ceramic heaters capable of reaching 600°C within 5 seconds, improving thermal response for semiconductor and analytical equipment while supporting higher processing efficiency. Source: INNOVACERA

June 2025 – Durex Industries expanded its Advanced Ceramic Heater portfolio featuring multilayer AlN technology delivering up to 2,000 W/in² power density for demanding semiconductor and instrumentation applications, strengthening high-performance thermal processing capabilities. Source: Durex Industries

January 2024 – PW Ceramic introduced integrated AlN ceramic heaters with embedded electrodes and optimized thermal uniformity, supporting plasma processing applications while improving long-term operational stability through advanced ceramic fusion manufacturing. Source: PW Ceramic

2025 – Mecaro advanced a new Aluminum Nitride ceramic material design for semiconductor heater components emphasizing improved sintering density and thermal conductivity, strengthening next-generation heater material development for precision wafer processing. Source: Google Patents Google Patents

The report provides comprehensive analysis of the Advanced Ceramic (AlN) Heaters Market across product types, applications, end-users, and major geographic regions between 2026 and 2033. It evaluates flat plate, multi-zone, disc-type, cylindrical, and customized heater configurations deployed across semiconductor manufacturing, display production, vacuum equipment, analytical instrumentation, medical systems, and industrial processing. The study also examines adoption patterns across semiconductor manufacturers, equipment OEMs, research organizations, medical device producers, and industrial enterprises, with more than 50% of demand concentrated in semiconductor-related applications.

The report further assesses competitive positioning, manufacturing capabilities, regional deployment trends, emerging thermal management technologies, embedded sensing, and intelligent ceramic heating platforms. It delivers strategic insights into product innovation, supply-chain resilience, localization strategies, technology integration, and operational efficiency improvements, enabling stakeholders to evaluate expansion priorities, investment opportunities, competitive differentiation, and long-term market positioning across high-performance thermal processing industries.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 470.6 Million |

|

Market Revenue in 2033 |

USD 884.0 Million |

|

CAGR (2026 - 2033) |

8.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Watlow, NGK Insulators, Ltd., Kyocera Corporation, CoorsTek, Inc., CeramTec GmbH, Durex Industries, Ferrotec Holdings Corporation, Innovacera, MARUWA Co., Ltd., Semixicon LLC, Boboo Hi-Tech Co., Ltd., Precision Ceramics USA, Toshiba Materials Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |