Reports

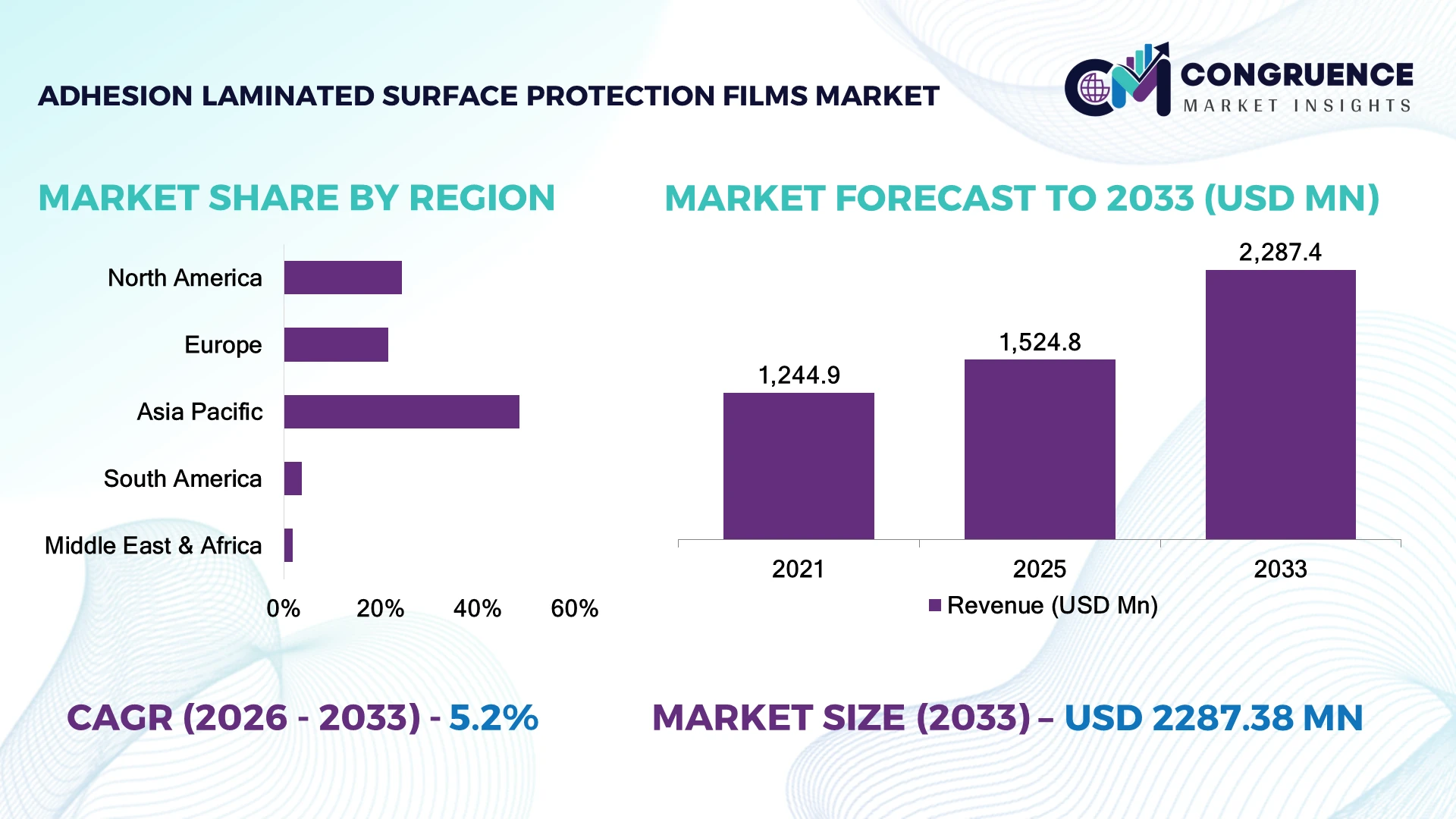

The Global Adhesion Laminated Surface Protection Films Market was valued at USD 1,524.0 Million in 2025 and is anticipated to reach a value of USD 2,287.4 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is driven by expanding electronics manufacturing, rising automotive surface protection requirements, and increased adoption of high-performance removable protective films in industrial processing.

China dominates the global market with nearly 39% of production capacity, supported by large-scale electronics, automotive, and construction manufacturing clusters alongside continuous investments in advanced polymer processing facilities. Japan follows with high-value specialty film production, while India is expanding manufacturing capacity through industrial modernization initiatives. More than 65% of premium-grade protective film output is supplied across Asia-Pacific, strengthening regional export competitiveness amid ongoing supply-chain diversification.

This leadership reinforces Asia-Pacific as the preferred investment destination for production expansion, technology partnerships, and resilient procurement strategies.

Market Size & Growth: USD 1,524.0 Million in 2025, projected to reach USD 2,287.4 Million by 2033 at a CAGR of 5.2%, supported by advanced electronics and automotive manufacturing expansion.

Top Growth Drivers: Electronics manufacturing (+24%), automotive lightweight components (+19%), and industrial automation (+17%) continue accelerating product adoption.

Short-Term Forecast: By 2028, manufacturing waste is expected to decline by nearly 14% through improved multilayer film processing and precision coating technologies.

Emerging Technologies: AI-driven coating inspection, automated roll-to-roll lamination, and nano-engineered adhesive materials are improving production quality and consistency.

Regional Leaders: Asia-Pacific (~USD 1.18 Billion), North America (~USD 0.46 Billion), and Europe (~USD 0.39 Billion) lead through electronics production, industrial automation, and sustainable manufacturing adoption.

Consumer/End-User Trends: More than 58% of industrial users prefer multilayer protective films offering residue-free removal and improved surface durability.

Pilot/Case Example: In 2024, an automated film coating project improved production efficiency by approximately 18% while reducing material defects.

Competitive Landscape: Top manufacturers collectively account for nearly 42% of the global market, led by Nitto Denko, 3M, LINTEC, Saint-Gobain, and Avery Dennison.

Regulatory & ESG Impact: Solvent-reduction initiatives lowered VOC emissions by nearly 20%, encouraging wider adoption of environmentally responsible coating technologies.

Investment & Funding: More than USD 600 Million has been directed toward production expansion, strategic partnerships, and advanced coating facilities across Asia and North America.

Innovation & Future Outlook: Smart protective films, recyclable polymer structures, and precision adhesive technologies are strengthening long-term product differentiation and supply-chain resilience.

Adhesion Laminated Surface Protection Films are witnessing strong demand across consumer electronics, automotive components, architectural panels, and metal fabrication due to increasing requirements for temporary surface protection and defect-free product delivery. Advanced low-residue adhesive formulations and multilayer film structures continue improving durability and application efficiency. Nearly 30% of new industrial installations now prioritize sustainable film solutions, while regional supply-chain diversification is accelerating innovation and strategic manufacturing investments.

Protective surface films have become an essential component of modern manufacturing as producers focus on minimizing product damage, reducing quality losses, and improving production efficiency. Increasing supply-chain restructuring and localization of advanced manufacturing have encouraged companies to establish regional coating and lamination facilities, improving delivery reliability while supporting industrial competitiveness across electronics, automotive, and construction sectors.

Modern multilayer laminated films equipped with precision-coated adhesive systems deliver approximately 20% higher application efficiency and significantly lower residue compared with conventional single-layer protection films. Asia-Pacific continues leading large-scale production through integrated manufacturing ecosystems, while North America emphasizes premium specialty films for aerospace and advanced industrial applications. Europe maintains strong momentum through environmentally responsible manufacturing standards and sustainable material innovation. During the next two to three years, automated inspection systems are expected to exceed 55% adoption across newly commissioned production lines.

Manufacturers are expanding strategic partnerships with polymer suppliers and equipment providers to strengthen localized production, improve material performance, and shorten delivery cycles. Recent investments in automated roll-to-roll coating facilities demonstrate the industry's focus on productivity, product consistency, and operational flexibility. Companies establishing resilient manufacturing networks and advanced coating capabilities will secure stronger competitive positioning as customers increasingly prioritize premium surface protection, process efficiency, and long-term manufacturing reliability.

Rapid expansion of electronics, automotive, and metal processing industries is accelerating demand for advanced adhesion laminated surface protection films capable of preventing scratches, contamination, and handling damage during manufacturing and logistics. More than 68% of premium consumer electronics now utilize temporary protective films during assembly, while automated production lines have improved film application efficiency by nearly 22%. China's ongoing investment in semiconductor and advanced manufacturing capacity continues to strengthen demand for precision protective materials as supply-chain localization gains momentum. In response, leading manufacturers are expanding multilayer film production, investing in high-performance adhesive formulations, and partnering with OEMs to deliver customized protection solutions. This integration of advanced materials directly enhances product quality, lowers rejection rates, and strengthens long-term supplier relationships across industrial value chains.

The market continues to face pressure from fluctuating prices of polyethylene, polypropylene, acrylic adhesives, and specialty coating chemicals, creating uncertainty in manufacturing costs and procurement planning. Raw material costs account for nearly 55% of total production expenses, while adhesive price fluctuations exceeding 15% have affected production margins across several manufacturing hubs. Supply disruptions linked to Red Sea shipping rerouting and global logistics bottlenecks have further increased lead times for specialty chemicals. Companies are responding through long-term supplier agreements, localized sourcing strategies, and greater use of alternative polymer formulations to improve procurement resilience. Businesses capable of reducing dependence on single-source suppliers are achieving stronger operational stability and maintaining consistent delivery performance.

Growing adoption of recyclable protective films, solvent-free adhesive technologies, and AI-enabled coating inspection is creating significant opportunities beyond conventional manufacturing applications. More than 45% of newly installed coating lines now incorporate automated quality inspection, while recyclable polymer structures can reduce production waste by approximately 18%. India and Vietnam are emerging as attractive manufacturing destinations as electronics production expands under industrial incentive programs and export-focused investments. Companies are strengthening competitive positioning through research into bio-based polymers, digital production monitoring, and collaborative innovation with equipment suppliers. A notable strategic opportunity lies in integrating smart manufacturing analytics with coating operations, enabling predictive quality control and lower production costs without compromising film performance.

Maintaining uniform adhesive performance across increasingly sophisticated multilayer film structures remains a critical execution challenge as industrial quality standards become more stringent. Production defects can increase by nearly 12% when coating thickness varies beyond acceptable tolerances, while advanced automated coating systems require approximately 25% higher capital investment than conventional production lines. Japan and Germany continue raising quality expectations for electronics and automotive components, requiring manufacturers to achieve tighter process control and higher traceability. Companies must strengthen workforce expertise, invest in precision inspection technologies, and modernize coating infrastructure to ensure consistent product performance. Successfully balancing production scalability with strict quality assurance will become a decisive competitive advantage for manufacturers serving high-value industrial applications.

Smart Coating Line Automation: Manufacturers are integrating AI-enabled optical inspection and automated roll-to-roll coating systems, reducing inspection time by nearly 28% while improving coating consistency by approximately 20%. More than 52% of newly commissioned production lines now incorporate digital process monitoring to address labor shortages and stricter quality requirements. Companies are expanding automated facilities to improve throughput, reduce material waste, and shorten production cycles.

Sustainable Film Material Transition: Demand for recyclable polyolefin films and solvent-free adhesive technologies continues to accelerate as environmental compliance requirements tighten. Around 35% of newly developed industrial protective films now incorporate recyclable structures, while VOC emissions during coating operations have declined by nearly 18% through cleaner manufacturing processes. Producers are redesigning product portfolios, modernizing coating facilities, and increasing investment in environmentally compatible adhesive systems.

Electronics Supply-Chain Localization: Electronics manufacturers are diversifying production beyond traditional manufacturing hubs, increasing localized procurement of protective films by approximately 24%. Industrial parks in India and Vietnam have expanded converter partnerships, while OEMs are shortening sourcing distances to improve delivery reliability. Film manufacturers are establishing regional coating operations, strengthening distributor networks, and customizing products for localized electronics and appliance production.

Premium Multi-Layer Film Adoption: High-performance multilayer films now account for nearly 46% of industrial-grade product demand because they provide superior scratch resistance, residue-free removal, and extended outdoor durability. Advanced adhesive engineering has reduced application defects by almost 16% during automated manufacturing. Companies are accelerating product differentiation through specialty coatings, customized film thickness, and strategic collaborations with automotive and electronics manufacturers.

The market is segmented into Polyethylene (PE) Films, Polypropylene (PP) Films, Polyvinyl Chloride (PVC) Films, Polyethylene Terephthalate (PET) Films, and Others. Polyethylene (PE) Films dominate the market with an estimated 41% share due to their excellent flexibility, competitive production costs, easy processability, and compatibility with diverse adhesive systems. Their extensive application across metal sheets, construction materials, glass panels, and consumer electronics continues supporting large-volume demand. Polypropylene films remain widely adopted for lightweight industrial packaging, while PVC films retain importance in construction and architectural surface protection where durability remains essential. PET Films represent the fastest-growing segment as manufacturers increasingly require superior dimensional stability, higher temperature resistance, and optical clarity for electronics, automotive displays, and precision manufacturing. Nearly 32% of new premium protective film developments now utilize PET-based structures, while demand for multilayer laminated films has increased by approximately 21%. Manufacturers are expanding PET coating capacity, developing thinner high-strength films, and investing in advanced adhesive formulations to improve performance while reducing overall material consumption. Investment priorities continue shifting toward specialty engineered films capable of supporting high-value industrial applications.

The market is segmented into Electronics, Automotive, Construction, Metal Processing, Glass Processing, and Others. Electronics account for approximately 36% of total demand, driven by increasing production of smartphones, display panels, semiconductors, and consumer appliances requiring temporary surface protection throughout assembly and transportation. Automated manufacturing lines increasingly depend on precision protective films to minimize contamination and cosmetic defects. Automotive applications remain a major contributor as painted components, infotage displays, and lightweight composite materials require reliable temporary protection during production and logistics. Automotive represents the fastest-growing application as electric vehicle manufacturing expands and premium interior components require enhanced scratch protection. More than 27% of newly manufactured EV exterior panels now incorporate advanced laminated protection during assembly, while industrial automation has improved protective film application efficiency by nearly 19%. Construction, metal processing, and glass processing continue expanding through infrastructure modernization and architectural glazing projects. Manufacturers are introducing customized adhesive systems and application-specific film grades while strengthening partnerships with OEMs to improve deployment efficiency across multiple industrial environments.

The market is segmented into Electronics Manufacturers, Automotive Manufacturers, Construction Companies, Metal Fabricators, Glass Manufacturers, and Others. Electronics Manufacturers represent the largest end-user segment with an estimated 34% market share owing to continuous high-volume production and stringent cosmetic quality standards. Large-scale assembly operations require reliable protective films throughout fabrication, storage, and global shipment. Automotive manufacturers closely follow as increasing production of electric vehicles and premium vehicle components drives consistent procurement of removable protective film solutions. Automotive Manufacturers are the fastest-growing end-user group as investments in lightweight materials, digital displays, and advanced finishing processes continue expanding. Nearly 29% of new automotive manufacturing facilities have increased usage of multilayer protective films, while automated handling systems have reduced surface damage during production by approximately 18%. Construction companies, metal fabricators, and glass manufacturers continue adopting customized protective solutions for architectural panels, coated metals, and processed glass. Suppliers are responding through long-term OEM partnerships, customized adhesive formulations, and localized manufacturing capabilities that improve delivery speed and customer-specific product development.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

North America represents approximately 24.3% of the global market, supported by advanced electronics manufacturing, automotive production, aerospace applications, and industrial automation. Growing adoption of automated production systems and premium surface finishing standards continues increasing demand for high-performance laminated protection films. More than 62% of large industrial manufacturers have integrated automated surface protection processes into production workflows to reduce product defects and improve operational efficiency. Expansion of electric vehicle manufacturing and semiconductor investments continues strengthening demand for residue-free protective films. Manufacturers are increasing localized production capacity, enhancing converting operations, and expanding strategic partnerships with OEMs to improve supply reliability and customized product offerings.

United States Market Outlook: The United States remains the region's largest market due to its extensive aerospace, automotive, semiconductor, and electronics manufacturing industries. More than 70% of regional demand originates from industrial manufacturing applications requiring precision surface protection throughout fabrication and logistics. Continued investment in semiconductor fabrication plants, automated production facilities, and advanced material technologies is encouraging manufacturers to introduce higher-performance adhesive formulations while strengthening domestic production capabilities and long-term customer partnerships.

Europe accounts for approximately 21.5% of global demand, driven by advanced automotive manufacturing, architectural glass production, and industrial engineering sectors. Increasing emphasis on recyclable materials and environmentally responsible coating technologies continues influencing product development across the region. More than 40% of newly commissioned coating lines are designed to support solvent-reduced manufacturing processes and improved production efficiency. Industrial modernization and advanced manufacturing investments continue encouraging adoption of premium laminated protective films. Companies are expanding specialty coating capabilities while introducing recyclable film structures and improving operational flexibility through digital quality management systems.

Germany Market Outlook: Germany leads the European market through its strong automotive, machinery, and industrial manufacturing ecosystem. High-quality production standards continue supporting demand for advanced laminated protective films across automotive body panels, precision components, and engineered glass applications. Nearly 38% of regional industrial protective film consumption is linked to German manufacturing activities, while continuous factory modernization and advanced automation investments reinforce long-term demand for premium protective solutions.

Asia-Pacific contributes approximately 48.6% of the global market through its dominant electronics, automotive, appliance, and construction manufacturing industries. Integrated supply chains, competitive production costs, and expanding industrial infrastructure continue strengthening regional leadership. Nearly 65% of global protective film converting capacity is concentrated across major manufacturing economies within the region, while export-oriented production continues expanding. Investment in automated coating equipment and precision adhesive technologies has improved production efficiency by approximately 20%. Manufacturers are increasing multilayer film capacity, strengthening regional distribution networks, and localizing raw material procurement to improve supply-chain resilience.

China Market Outlook: China remains the largest national market due to its unmatched electronics manufacturing scale, extensive automotive production, and advanced industrial supply chain. Approximately 39% of global production capacity is concentrated in China, supported by continuous investment in polymer processing, coating technology, and export-oriented manufacturing. Producers continue expanding high-speed coating facilities and developing customized protective film solutions to meet evolving requirements across consumer electronics, renewable energy equipment, and precision manufacturing industries.

South America represents approximately 3.8% of global demand as automotive assembly, consumer appliance manufacturing, and infrastructure development gradually strengthen industrial activity. Expansion of localized manufacturing and improved logistics networks continue supporting greater adoption of protective surface films across industrial processing operations. Nearly 18% of new industrial facility upgrades now incorporate automated material handling systems requiring temporary surface protection during production. Companies are increasing regional distribution capabilities, expanding technical support services, and improving inventory availability to strengthen customer responsiveness despite logistics and import dependency challenges.

Brazil Market Outlook: Brazil dominates regional demand through its established automotive manufacturing, appliance production, and construction materials industries. Industrial modernization initiatives continue increasing demand for laminated protection films used on coated metals, architectural panels, and finished consumer products. More than half of regional manufacturing activity is concentrated in Brazil, encouraging suppliers to expand local converting operations, strengthen distributor partnerships, and improve technical service capabilities for industrial customers.

Middle East & Africa account for approximately 1.8% of the global market, supported by infrastructure development, industrial diversification, architectural glazing projects, and expanding metal fabrication activities. Investments in advanced manufacturing zones and commercial construction continue increasing demand for protective films used during fabrication and installation. Approximately 22% of newly developed industrial projects now specify temporary surface protection for premium architectural materials and fabricated metal products. Manufacturers are strengthening regional partnerships, expanding warehouse infrastructure, and improving localized product availability to support faster project execution and industrial development.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale industrial diversification, infrastructure expansion, and advanced construction initiatives. Rapid development of manufacturing zones and metal processing facilities continues increasing consumption of high-performance laminated protection films across construction, aluminum fabrication, and engineered glass applications. Ongoing industrial investment programs are encouraging international manufacturers to establish stronger distribution partnerships and expand regional supply capabilities for long-term market presence.

The market is led by global material innovators including 3M, Nitto Denko, LINTEC Corporation, Avery Dennison, and POLIFILM, competing directly against regional converters and cost-focused manufacturers supplying construction and industrial customers. The top five companies collectively account for approximately 44% of global demand, creating a moderately consolidated competitive structure. Global leaders compete through advanced adhesive chemistry, multilayer film engineering, and integrated supply chains, while regional producers emphasize pricing flexibility and faster local delivery. More than 58% of premium product launches target electronics and automotive applications, and customized film solutions reduce OEM processing defects by nearly 20%. Companies are expanding coating capacity, strengthening OEM partnerships, investing in recyclable materials, and integrating automated inspection technologies to improve quality consistency. Competition is shifting toward sustainable materials, localized manufacturing, and specialty applications rather than commodity films. High capital requirements, proprietary coating technology, and strict OEM qualification processes remain significant entry barriers. Winning requires continuous innovation, reliable global supply capability, application-specific customization, and long-term strategic customer partnerships.

Nitto Denko Corporation

Avery Dennison Corporation

LINTEC Corporation

POLIFILM Group

tesa SE

SEKISUI CHEMICAL Co., Ltd.

Saint-Gobain

Scapa (Mativ)

Pregis LLC

Intertape Polymer Group

Surface Armor LLC

Manufacturers are rapidly replacing conventional solvent-based coating processes with precision roll-to-roll coating, AI-assisted optical inspection, and multilayer co-extrusion technologies. Automated inspection systems improve defect detection by approximately 25%, while precision coating reduces material waste by nearly 18%. Around 54% of newly commissioned production facilities now integrate digital process monitoring, enabling consistent coating thickness and improved manufacturing repeatability. These technologies strengthen operational efficiency and help suppliers satisfy increasingly stringent electronics and automotive quality specifications.

Emerging innovation focuses on water-based adhesives, recyclable polyolefin structures, nano-engineered coatings, and smart protective films with improved scratch resistance. Compared with conventional single-layer films, advanced multilayer constructions deliver nearly 22% greater durability and approximately 17% longer outdoor performance. Premium manufacturers and OEM suppliers benefit most because higher-performance films reduce warranty claims, improve production yields, and support demanding industrial applications requiring residue-free removal and dimensional stability.

Between 2026 and 2028, broader deployment of AI-enabled quality control, digital manufacturing analytics, and automated coating optimization is expected to exceed 60% among large production facilities. Companies investing in integrated coating technologies, sustainable adhesive chemistry, and advanced polymer engineering will strengthen competitive positioning through faster product development, lower operating costs, improved manufacturing flexibility, and superior product consistency across high-value industrial and electronics applications.

June 2025 – Avery Dennison introduced the DOL 7460 Digital Overlaminate featuring ADReva™ Technology with a PVC-free, solvent-free construction and durability of up to six years for vertical applications, strengthening its sustainable graphics protection portfolio. Source: www.graphics.averydennison.com

February 2025 – Avery Dennison launched the Encore™ automotive window film portfolio using nanoceramic technology that rejects up to 93% infrared heat, reduces up to 94% glare, and blocks more than 99% of UV rays, enhancing premium automotive protection solutions. Source: www.graphics.averydennison.com

September 2024 – Nitto Denko expanded research on electronics surface protection films incorporating antistatic functionality to reduce electrostatic discharge and micro-scratch formation during OLED display manufacturing, supporting next-generation electronics production efficiency.

October 2024 – Avient introduced a new ultra-high-adhesion Versaflex PF thermoplastic elastomer series engineered for co-extruded protective films, improving adhesion performance for demanding industrial applications and expanding advanced protective material capabilities.

This report provides comprehensive coverage of the Adhesion Laminated Surface Protection Films Market across Polyethylene, Polypropylene, PVC, PET, and other specialty film types, together with detailed evaluation of electronics, automotive, construction, metal processing, glass processing, and additional industrial applications. The analysis assesses procurement trends across major end-user groups while examining competitive positioning throughout North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 45% of the assessment emphasizes evolving material technologies, manufacturing optimization, and product innovation influencing industrial purchasing decisions.

The report also evaluates advanced coating technologies, sustainable adhesive systems, multilayer film structures, automation trends, and localized manufacturing strategies shaping industry development between 2026 and 2033. Strategic insights cover company benchmarking, investment priorities, deployment patterns, supply-chain transformation, technology adoption, and competitive differentiation, enabling manufacturers, investors, distributors, and OEMs to identify expansion opportunities, strengthen market positioning, and support long-term business planning across both mature and emerging application segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,524.0 Million |

| Market Revenue (2033) | USD 2,287.4 Million |

| CAGR (2026–2033) | 5.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | 3M; Nitto Denko Corporation; Avery Dennison Corporation; LINTEC Corporation; POLIFILM Group; tesa SE; SEKISUI CHEMICAL Co., Ltd.; Saint-Gobain; Scapa (Mativ); Pregis LLC; Intertape Polymer Group; Surface Armor LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |