Reports

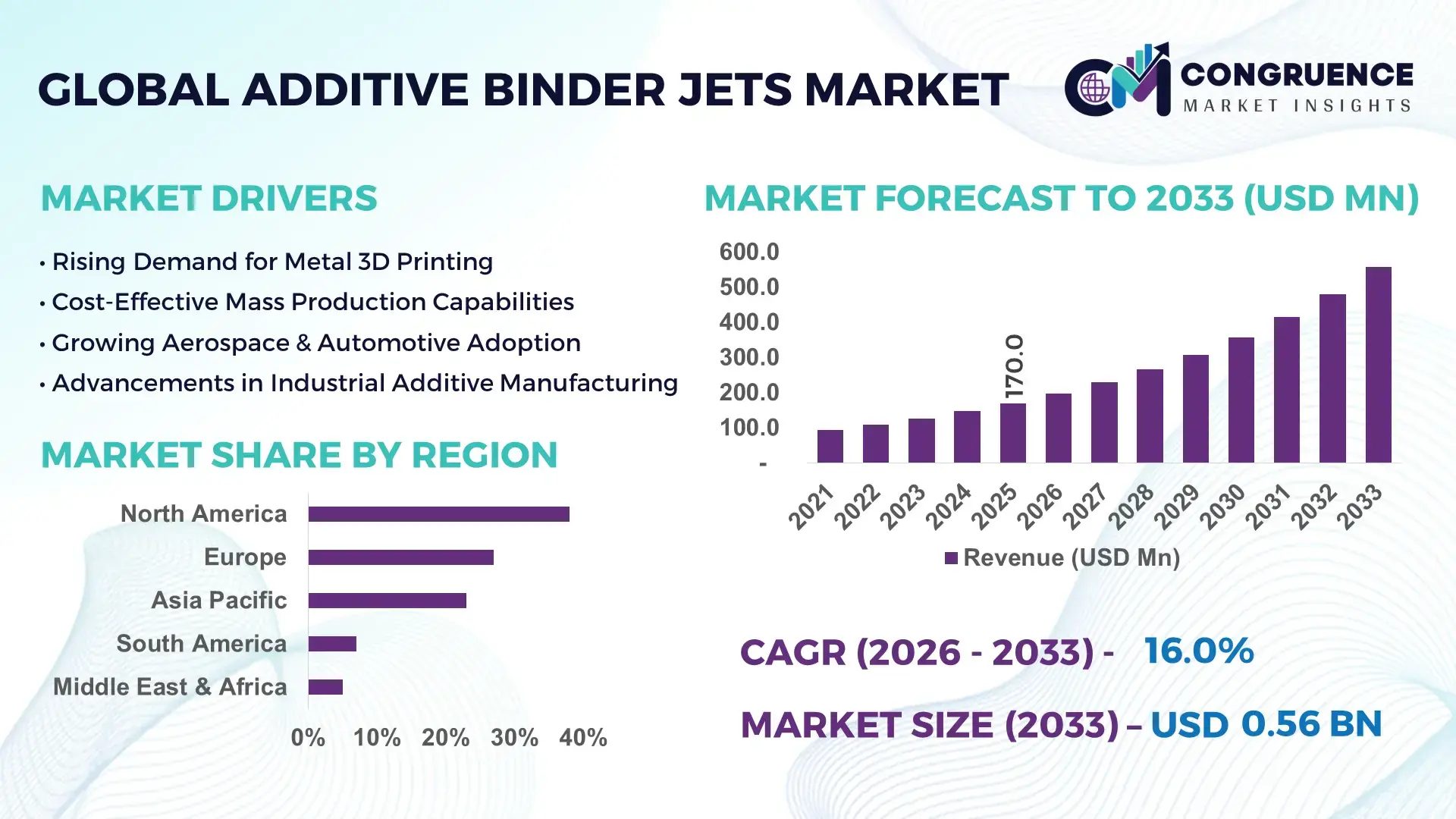

The Global Additive Binder Jets Market was valued at USD 170.0 Million in 2025 and is anticipated to reach a value of USD 557.3 Million by 2033 expanding at a CAGR of 16% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by increasing industrial adoption of high-speed metal and ceramic additive manufacturing for complex, lightweight, and cost-efficient production applications.

The United States represents the dominant country in the Additive Binder Jets Market, supported by strong industrial infrastructure and advanced additive manufacturing ecosystems. The U.S. hosts over 35% of the world’s installed industrial 3D printing systems, with binder jetting increasingly deployed across aerospace, automotive, and defense sectors. More than 60% of aerospace OEMs in the country have integrated binder jet prototypes into production validation cycles. Federal initiatives such as advanced manufacturing grants exceeding USD 2 billion between 2020 and 2024 have accelerated metal binder jet capacity expansion. Additionally, over 40 major U.S.-based manufacturing facilities have adopted high-throughput binder jet systems capable of producing 10,000+ metal parts per week, strengthening domestic production capabilities and industrial scalability.

Market Size & Growth: USD 170.0 Million (2025), projected to reach USD 557.3 Million by 2033, growing at 16% CAGR due to rapid industrial-scale metal additive manufacturing adoption.

Top Growth Drivers: 48% faster production cycles, 35% material waste reduction, 42% tooling cost savings.

Short-Term Forecast: By 2028, production cost per part is expected to decline by 25% through automation and powder recycling optimization.

Emerging Technologies: AI-enabled print monitoring, multi-material binder jetting systems, high-density sintering advancements.

Regional Leaders: North America projected at USD 210 Million by 2033 with aerospace focus; Europe at USD 165 Million driven by automotive lightweighting; Asia-Pacific at USD 140 Million supported by industrial tooling expansion.

Consumer/End-User Trends: Aerospace accounts for ~30% adoption, automotive 25%, and industrial tooling 20%, with growing batch production usage.

Pilot or Case Example: In 2024, a U.S. automotive OEM achieved 32% production time reduction through binder jet-based tooling integration.

Competitive Landscape: Market leader holds ~22% share, followed by ExOne, Desktop Metal, GE Additive, and HP Inc.

Regulatory & ESG Impact: Sustainability mandates target 30% material efficiency improvement and lower carbon-intensive casting alternatives.

Investment & Funding Patterns: Over USD 1.1 Billion invested globally (2021–2025) in metal binder jet capacity and R&D expansion.

Innovation & Future Outlook: Integration with Industry 4.0 platforms and digital twins is shaping scalable, decentralized manufacturing networks.

Metal binder jetting contributes nearly 65% of total market demand, followed by sand binder jetting at 20% and ceramics at 15%. Aerospace and defense collectively account for approximately 30% of application demand, while automotive lightweighting contributes 25%. Environmental regulations promoting 20–30% material efficiency gains are accelerating adoption. Asia-Pacific manufacturing hubs are witnessing 18% annual equipment installations, reflecting strong industrial expansion and digital factory transformation initiatives.

The Additive Binder Jets Market holds strategic relevance as industries transition from prototyping toward full-scale additive production. Binder jetting enables up to 48% faster production compared to traditional CNC machining for complex geometries, while reducing material waste by nearly 35%. In high-volume applications, advanced metal binder jet systems deliver 30% lower per-part cost compared to conventional casting for small and medium-sized components. Compared with traditional powder bed fusion, high-speed binder jetting delivers 25% higher throughput in batch production environments.

North America dominates in production volume due to its established aerospace and defense supply chains, while Europe leads in adoption intensity, with nearly 45% of large automotive manufacturers integrating binder jet pilot lines. By 2028, AI-driven real-time print analytics is expected to improve defect detection rates by 40%, reducing scrap and enhancing yield efficiency across industrial facilities.

From a compliance perspective, firms are committing to ESG metrics including 30% carbon emission reduction by 2030 through substitution of energy-intensive casting processes with binder jet technologies. In 2024, a U.S.-based aerospace manufacturer achieved a 28% reduction in component weight and 22% improvement in fuel efficiency metrics through binder jet-enabled part consolidation initiatives.

Looking ahead, the Additive Binder Jets Market is positioned as a pillar of resilient manufacturing strategies, enabling decentralized production, digital inventory models, regulatory compliance, and sustainable industrial transformation across global supply chains.

The Additive Binder Jets Market is evolving rapidly as industries prioritize high-throughput additive manufacturing for end-use parts. Increasing integration of digital manufacturing workflows, material science advancements, and automation technologies are strengthening market momentum. Metal binder jetting is gaining industrial validation due to its ability to produce complex geometries at scale with minimal tooling. Aerospace, automotive, medical devices, and industrial tooling sectors are expanding pilot-to-production transitions. Additionally, powder material innovation—particularly stainless steel, Inconel, and aluminum alloys—has improved density levels above 97%, enhancing structural performance. Government-backed advanced manufacturing programs and private capital investment are accelerating equipment installations globally, while supply chain localization strategies are reinforcing distributed additive manufacturing adoption.

Industrial manufacturers are increasingly demanding lightweight and topology-optimized components to enhance fuel efficiency and operational performance. Binder jetting enables the production of intricate lattice structures reducing component weight by up to 30% compared to conventionally machined parts. Aerospace OEMs report up to 25% improvement in material utilization using binder jet processes. Automotive manufacturers integrating binder jet tooling have achieved 32% reduction in development cycles. The ability to produce thousands of parts per week using batch-based printing platforms further enhances scalability, making binder jetting attractive for mid-volume production environments.

Industrial-grade binder jet systems require significant capital investment, often exceeding several million dollars per production line. Post-processing stages such as curing, depowdering, and sintering add operational complexity and require additional infrastructure. Sintering cycles can extend production timelines by 20–30%, impacting throughput optimization. Furthermore, achieving consistent density above 97% demands precise process calibration, increasing technical barriers for small manufacturers. Powder handling and recycling systems also necessitate compliance with safety standards, increasing operational overhead and limiting rapid entry of new market participants.

Transitioning from prototyping to serial production presents substantial growth opportunities. Binder jetting systems capable of producing 10,000+ components per week support automotive, consumer electronics, and industrial tooling applications. Adoption in electric vehicle platforms is increasing, where lightweight components can enhance battery efficiency by 5–8%. Medical implant manufacturers are exploring customized porous implants with 20% improved osseointegration performance. Additionally, decentralized manufacturing hubs leveraging digital part inventories can reduce spare part lead times by up to 40%, strengthening supply chain agility.

Dimensional shrinkage during sintering—often ranging between 15–20%—requires precise compensation algorithms and advanced simulation models. Variability in powder particle size distribution can affect surface finish and mechanical strength. Maintaining consistent density and tensile properties across batch production remains technically demanding. Industrial users require repeatability rates above 95% for critical aerospace components, necessitating stringent quality assurance systems. Additionally, certification standards for aerospace and medical applications impose rigorous testing protocols, extending validation timelines and increasing compliance costs.

Industrial-Scale Metal Production Expansion: Over 45% of new binder jet installations in 2024 were configured for batch production exceeding 5,000 parts per cycle. High-speed print heads now improve layer deposition rates by 35%, enabling faster throughput. Aerospace manufacturers report 28% reduction in part consolidation efforts through advanced metal binder jet systems.

AI-Integrated Process Monitoring Adoption: Approximately 50% of newly deployed systems incorporate AI-based defect detection algorithms, improving first-pass yield rates by 40%. Predictive analytics tools reduce unplanned downtime by nearly 22%, enhancing operational reliability across automated production lines.

Powder Material Innovation Acceleration: Development of advanced stainless steel and aluminum powders has improved final part density to above 98% in controlled sintering environments. Recyclable powder utilization rates have increased to 85%, reducing material waste by 30% in industrial facilities.

Growth in Automotive Tooling Applications: Automotive OEMs adopting binder jet tooling solutions report 32% shorter development cycles and 27% lower prototype costs. Electric vehicle manufacturers integrating binder jet heat exchangers and brackets achieved up to 15% component weight reduction, supporting improved vehicle efficiency and thermal management performance.

The Additive Binder Jets Market is segmented by type, application, and end-user, reflecting its expanding industrial footprint across high-precision manufacturing ecosystems. Metal binder jetting systems dominate installations due to their suitability for structural and functional components, while sand and ceramic systems address casting molds and specialized engineering applications. Application-wise, aerospace and automotive remain core adopters, leveraging binder jetting for lightweight, high-complexity parts and tooling optimization. Industrial tooling and medical device manufacturing are steadily expanding, particularly in customized and mid-volume production runs. From an end-user perspective, large enterprises account for the majority of deployments due to capital-intensive infrastructure requirements, although mid-sized manufacturers are increasingly adopting modular systems. Growing digital manufacturing integration, powder material innovation, and automation-driven post-processing are reshaping segmentation dynamics, enabling scalable production across multiple verticals.

Metal binder jetting currently accounts for approximately 65% of total adoption, making it the leading segment due to its ability to produce dense, end-use metal components suitable for aerospace, automotive, and defense applications. Stainless steel and Inconel powders are widely used, achieving density levels above 97% after sintering. In comparison, sand binder jetting holds nearly 20% share, primarily serving foundries for mold and core production, while ceramic binder jetting represents about 15%, addressing specialized industrial and medical uses. Metal binder jetting remains dominant because it enables up to 40% faster batch production compared to laser-based powder bed systems in medium-volume manufacturing. However, ceramic binder jetting is emerging as the fastest-growing type, expanding at an estimated 18% CAGR, driven by demand for high-temperature resistant components in electronics and energy sectors. The remaining segments—composite and hybrid binder jet systems—collectively account for roughly 10% of installations, serving niche prototyping and research applications where material flexibility is critical.

In 2024, a U.S. Department of Energy-backed advanced manufacturing program validated metal binder jet components for industrial heat exchangers, demonstrating 28% improved thermal efficiency compared to conventionally cast parts.

Aerospace currently represents the leading application, accounting for approximately 30% of total adoption, as manufacturers prioritize lightweight, high-strength geometries that reduce fuel consumption by up to 20%. Automotive follows with around 25% share, driven by tooling, brackets, and electric vehicle components. Industrial tooling contributes roughly 20%, supporting rapid prototyping and small-batch production environments. While aerospace leads in adoption, automotive applications are expanding rapidly, with binder jet-based tooling reducing production cycle times by 32%. Medical applications are the fastest-growing segment, projected to expand at approximately 17% CAGR due to increasing demand for customized implants and porous structures that improve osseointegration by nearly 20%. The remaining applications—including consumer electronics and energy components—collectively account for about 25% of market usage, particularly in heat exchangers and structural housings. In 2025, over 38% of global manufacturing enterprises reported piloting binder jet systems within digital factory initiatives. Additionally, 42% of U.S.-based aerospace suppliers are integrating additive manufacturing into certified production workflows.

In 2024, NASA successfully tested binder jet-produced rocket engine components, achieving a 25% reduction in part count and improved structural optimization during propulsion trials.

Large manufacturing enterprises account for nearly 55% of binder jet installations, benefiting from integrated production lines and advanced sintering infrastructure. These organizations leverage binder jetting for serial production and supply chain localization. Mid-sized manufacturers represent about 30% of adoption, increasingly investing in modular binder jet systems for tooling and replacement part production. Research institutions and specialized engineering firms collectively contribute around 15%, focusing on materials innovation and prototype validation. While large enterprises dominate, mid-sized industrial manufacturers represent the fastest-growing end-user group, expanding at approximately 16% CAGR as equipment costs gradually decline and automation improves operational feasibility. Automotive OEMs report that 35% of their additive manufacturing budgets are now allocated to binder jet technologies, reflecting increased industrial confidence. In 2025, nearly 40% of Tier-1 automotive suppliers globally reported integrating binder jet prototypes into supply chains. Furthermore, 45% of aerospace manufacturers are investing in additive-based spare part digitization strategies to reduce inventory overhead by up to 30%.

In 2024, the U.S. Air Force advanced manufacturing division validated binder jet-produced flight-critical components, demonstrating 22% reduction in component weight during structural qualification assessments.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18% between 2026 and 2033.

North America’s leadership is supported by over 40 industrial-scale binder jet installations capable of producing 5,000–10,000 metal parts per build cycle. Europe follows with approximately 27% share, driven by automotive lightweighting initiatives and sustainability-focused manufacturing policies. Asia-Pacific holds nearly 23% share, supported by rapid industrial automation across China, Japan, and India, where more than 30 new additive manufacturing facilities were commissioned between 2022 and 2025. South America contributes around 7%, primarily led by Brazil’s tooling and energy sectors, while the Middle East & Africa account for roughly 5%, with increasing adoption in oil & gas and aerospace maintenance applications. Regional demand patterns indicate that over 45% of global aerospace binder jet adoption is concentrated in North America and Europe combined, while Asia-Pacific leads in new equipment installations, representing nearly 35% of annual system deployments in 2025.

North America holds approximately 38% of the global Additive Binder Jets Market share, supported by strong aerospace, automotive, and defense industries. The region hosts more than 35% of the world’s installed industrial 3D printing systems, with binder jetting increasingly adopted for serial production. Aerospace manufacturers report up to 30% weight reduction in structural components through topology optimization. Government-backed advanced manufacturing initiatives exceeding USD 2 billion between 2020 and 2024 have strengthened domestic additive capabilities. Technological advancements include AI-driven print monitoring systems that improve first-pass yield rates by nearly 40% and automated sintering lines enhancing throughput by 25%. Desktop Metal, a prominent U.S.-based player, has expanded high-throughput binder jet production platforms capable of manufacturing over 12,000 parts per week. Regional consumer behavior reflects higher enterprise adoption in aerospace, healthcare, and defense supply chains, where over 45% of Tier-1 suppliers integrate additive manufacturing into certified workflows.

Europe accounts for approximately 27% of the global Additive Binder Jets Market, with Germany, the UK, and France serving as key industrial hubs. Automotive manufacturers in Germany have integrated binder jet tooling solutions reducing production cycle times by 28%. The European Green Deal and circular economy directives promote 20–30% material efficiency improvements, encouraging replacement of energy-intensive casting methods. Emerging technology adoption includes digital twin integration and automated powder recycling systems achieving up to 85% material reuse. ExOne’s European operations have expanded sand binder jet installations for foundry applications, increasing mold production efficiency by 35%. Regulatory pressure drives demand for traceable and quality-certified additive processes, particularly in aerospace and medical sectors. Regional enterprises emphasize sustainable manufacturing compliance, with over 40% of industrial firms piloting low-carbon additive production workflows.

Asia-Pacific represents nearly 23% of global market volume and ranks as the fastest-growing region in equipment installations. China, Japan, and India are the leading consuming countries, collectively accounting for over 70% of regional demand. More than 30 advanced additive manufacturing centers were established between 2022 and 2025 to support localized production. Manufacturing digitization initiatives and Industry 4.0 integration are accelerating binder jet deployment, with automated production lines improving throughput by 30%. HP’s expansion of metal binder jet solutions across Asian manufacturing hubs has strengthened mid-volume production capabilities. Regional trends indicate strong adoption in automotive and electronics sectors, where lightweight components improve energy efficiency by up to 15%. Growth is further supported by government incentives promoting smart factory transformation and domestic supply chain resilience.

South America accounts for approximately 7% of the global Additive Binder Jets Market, with Brazil and Argentina leading adoption. Brazil’s automotive and energy sectors are integrating binder jet tooling systems that reduce prototyping timelines by 25%. Infrastructure modernization and renewable energy projects are increasing demand for customized metal components. Government-backed industrial innovation programs encourage adoption of digital manufacturing technologies, while trade agreements facilitate equipment imports. Regional manufacturers emphasize cost-efficient tooling solutions, with over 30% of industrial firms exploring additive-based replacement part strategies. Local engineering service providers are collaborating with global binder jet equipment suppliers to establish regional service hubs, improving equipment uptime by nearly 20%. Demand patterns are closely tied to industrial modernization and localized production requirements.

The Middle East & Africa region contributes roughly 5% of global market share, with the UAE and South Africa as major growth countries. Demand is concentrated in oil & gas, aerospace maintenance, and construction sectors. Binder jet applications in energy equipment manufacturing enable up to 22% improvement in part durability under high-temperature conditions. Technological modernization initiatives aligned with national industrial diversification programs are accelerating additive manufacturing adoption. The UAE has established advanced manufacturing innovation centers integrating digital production systems with automated quality monitoring. Trade partnerships with European and North American equipment suppliers strengthen regional capability development. Consumer behavior reflects growing enterprise-level adoption in aerospace MRO facilities, where additive manufacturing reduces spare part lead times by nearly 35%.

United States – 34% Market Share: Strong aerospace and defense production capacity with over 40 industrial binder jet installations supporting serial manufacturing.

Germany – 16% Market Share: Advanced automotive engineering ecosystem and sustainability-driven manufacturing policies accelerating binder jet tooling integration.

The Additive Binder Jets Market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 58% of global market share in 2025. The competitive environment includes over 25 active industrial equipment manufacturers and specialized material suppliers operating across North America, Europe, and Asia-Pacific. Market leaders differentiate through high-throughput printing platforms capable of producing 8,000–12,000 metal parts per week, advanced sintering integration, and AI-enabled process monitoring systems that improve first-pass yield rates by up to 40%.

Strategic initiatives shaping competition include vertical integration of powder material supply chains, expansion of localized service centers, and partnerships with aerospace and automotive OEMs. Between 2023 and 2025, more than 15 strategic collaborations were announced globally to accelerate serial production validation. Product innovation remains central, with multi-material binder jet systems and automated depowdering units improving operational efficiency by nearly 30%. Competitive positioning is increasingly influenced by digital manufacturing ecosystems, where integration with MES and ERP platforms reduces production cycle times by up to 25%. Companies are also investing in sustainability, with powder recycling rates exceeding 80% in advanced installations, reinforcing ESG-driven procurement preferences among industrial buyers.

GE Additive

voxeljet AG

Digital Metal (Höganäs AB)

3D Systems Corporation

Stratasys Ltd.

SLM Solutions Group AG

Markforged Holding Corporation

Renishaw plc

TRUMPF Group

XJet Ltd.

Höganäs AB

Nano Dimension Ltd.

Technological evolution in the Additive Binder Jets Market is centered on throughput enhancement, material density improvement, and digital process control. Modern binder jet systems now achieve layer deposition speeds up to 35% faster than earlier-generation platforms, enabling production cycles under 24 hours for medium-batch components. High-resolution print heads operating at 1200 dpi improve dimensional accuracy to within ±0.1 mm, supporting aerospace-grade tolerances.

Advanced sintering technologies have increased final part densities to above 98% in stainless steel and nickel alloys, narrowing the mechanical performance gap with wrought materials. Automated powder management systems now allow up to 85% powder recyclability, reducing material waste by nearly 30%. AI-powered in-situ monitoring solutions detect defects in real time, improving first-pass yield rates by 40% and minimizing scrap rates below 5% in optimized facilities.

Emerging innovations include multi-material binder jetting capable of integrating metal-ceramic composites within a single build cycle, and digital twin simulation tools that predict shrinkage compensation of 15–20% during sintering. Integration with Industry 4.0 frameworks enables remote diagnostics, predictive maintenance reducing downtime by 22%, and seamless ERP connectivity for supply chain synchronization. These advancements are positioning binder jetting as a scalable alternative to traditional casting and machining in industrial production environments.

• In June 2024, Desktop Metal X25Pro Now Powered by TurboFuse™ Press Release, Desktop Metal announced that its X25Pro production metal binder jet 3D printer can now process TurboFuse™, an intelligent high-strength binder chemistry. TurboFuse eliminates a layer-heating step, improves binder jet 3D printing speeds by ~50%+, enhances green part strength, and extends printhead life, with Eaton beta-testing the binder at its Additive Manufacturing Center of Excellence. Source: www.businesswire.com

• In October 2025, Continuum Powders & INDO‑MIM Qualify OptiPowder Ni718 for HP Metal Jet S100, Continuum Powders and INDO-MIM announced that OptiPowder Ni718 was successfully qualified on the HP Metal Jet S100 binder jet system. Sintered parts achieved >98% density and controlled hardness (74–79 HR15N), enabling production readiness for aerospace, defense, and energy applications. Source: www.globenewswire.com

• At Formnext 2025, HP Drives Additive Manufacturing Adoption with New Materials & Global Collaborations, HP Additive Manufacturing Solutions unveiled expanded Metal Jet binder jet materials including OptiPowder Ni718 and development of OptiPowder M247LC superalloy, alongside the launch of the HP Additive Manufacturing Network (AMN) program to accelerate global adoption and ecosystem growth. Source: www.hp.com

• In February 2025, INDO‑MIM Expands HP Metal Jet Installations, INDO-MIM expanded production by investing in five additional HP Metal Jet S100 systems following success with initial units. The expanded capacity enables series production ranging from 5,000 to 50,000 parts per year depending on component size. Source: www.3printr.com

The Additive Binder Jets Market Report provides a comprehensive evaluation of industrial binder jetting technologies across metal, sand, ceramic, and composite material categories. The scope covers system configurations ranging from mid-volume production platforms to high-throughput industrial systems capable of manufacturing over 10,000 parts per week. It analyzes application segments including aerospace (approximately 30% of usage), automotive (25%), industrial tooling (20%), medical devices, consumer electronics, and energy components.

Geographically, the report examines five key regions—North America (38% share), Europe (27%), Asia-Pacific (23%), South America (7%), and Middle East & Africa (5%)—with detailed assessment of production capacity, technology penetration, and enterprise adoption trends. The study evaluates digital manufacturing integration, AI-based quality monitoring systems improving yield rates by 40%, and powder recycling innovations achieving up to 85% reuse efficiency.

The report further investigates end-user categories such as large enterprises (55% adoption), mid-sized manufacturers (30%), and research institutions (15%). It includes analysis of regulatory frameworks, ESG-driven manufacturing shifts targeting 30% material efficiency improvements, and emerging opportunities in serial production and decentralized manufacturing models. The scope emphasizes operational scalability, technological competitiveness, and supply chain resilience within advanced manufacturing ecosystems, offering actionable insights for strategic investment and capacity planning decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 170.0 Million |

| Market Revenue (2033) | USD 557.3 Million |

| CAGR (2026–2033) | 16% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Desktop Metal; ExOne; HP Inc.; GE Additive; voxeljet AG; Digital Metal (Höganäs AB); 3D Systems Corporation; Stratasys Ltd.; SLM Solutions Group AG; Markforged Holding Corporation; Renishaw plc; TRUMPF Group; XJet Ltd.; Nano Dimension Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |