Reports

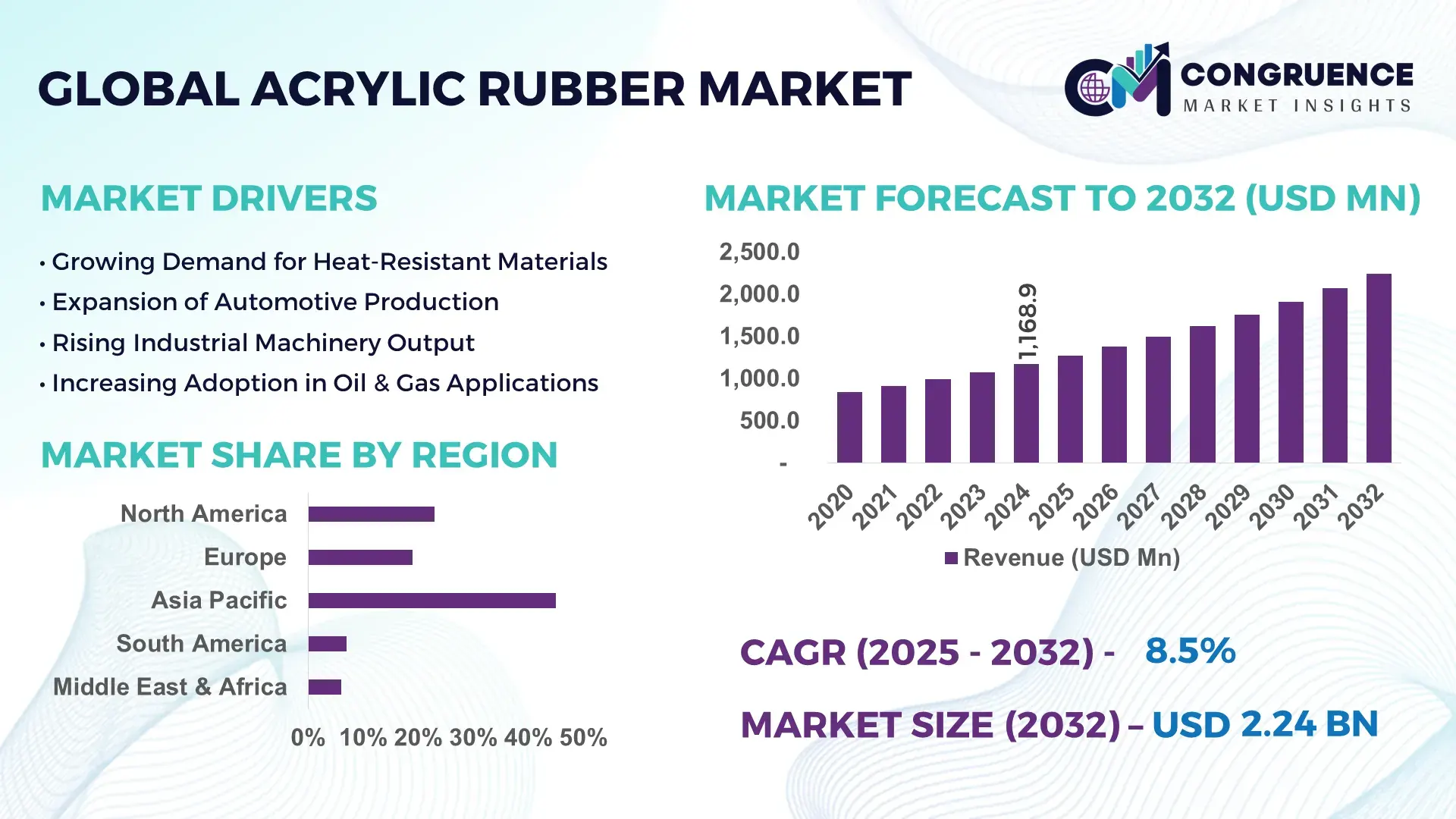

The Global Acrylic Rubber Market was valued at USD 1,168.9 Million in 2024 and is anticipated to reach a value of USD 2,245.0 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032, according to an analysis by Congruence Market Insights — driven by rising demand for high‑temperature and oil‑resistant elastomers in automotive and industrial applications.

Japan continues to lead in acrylic rubber production capacity, with Japanese producers operating multiple large-scale polymerization plants producing over 650 kilotons annually as of 2023. These facilities supply heat- and oil-resistant seals and gaskets to global automotive manufacturers, industrial machinery producers, and hydraulic systems. Recent investments in advanced acrylate monomer processing and improved polymerization reactors increased batch yields by ~12%, supporting expansion into high-performance industrial sealing and hose applications.

Market Size & Growth: Current market value USD 1,168.9 Million (2024), projected value USD 2,245.0 Million by 2032, expected CAGR of 8.5% — driven by growing demand in automotive and industrial sectors for durable elastomers.

Top Growth Drivers: Adoption in automotive sealing & gaskets (≈ 60%), expansion of industrial machinery demand (≈ 25%), growing use in construction and hydraulic systems (≈ 15%).

Short-Term Forecast: By 2028, improved polymerization and processing efficiencies are expected to reduce manufacturing scrap by ~18%.

Emerging Technologies: Bio‑based acrylate monomers, advanced high‑temperature resistant copolymers, improved curing and polymerization systems.

Regional Leaders: Asia‑Pacific — projected ~USD 1,000 Million by 2032 driven by automotive growth; North America — projected ~USD 450 Million by 2032 with stable industrial demand; Europe — projected ~USD 350 Million by 2032 aided by regulatory pressure and specialty elastomer adoption.

Consumer / End‑User Trends: High usage in automotive OEMs, hydraulic & heavy‑machinery manufacturers, aftermarket seal and gasket producers; increasing adoption in oil & gas and construction equipment.

Pilot or Case Example: In 2024, a major Japanese manufacturer increased batch yield by 12% through process optimization, reducing production downtime by 9%.

Competitive Landscape: Leading producers hold ~65% of global capacity; other key players include mid‑size regional manufacturers and specialty elastomer producers.

Regulatory & ESG Impact: Growing regulatory emphasis on emission reduction and material durability drives demand for longer‑lasting acrylic rubber seals, reducing maintenance waste cycles.

Investment & Funding Patterns: Recent capital investments in polymerization capacity upgrades exceed USD 200 million globally, with rising trend toward funding sustainable and high-performance elastomer technologies.

Innovation & Future Outlook: Shift toward bio‑based monomers, development of higher temperature and oil‑resistant grades, and expansion into new sectors such as hydraulic equipment, construction machinery, and renewable energy systems, positioning acrylic rubber as a durable, versatile elastomer of the future.

Acrylic rubber finds widespread use in automotive gaskets and seals, industrial hydraulic hoses, and heavy‑machinery sealing; recent advances include high‑temperature-resistant copolymers and bio‑based monomer formulations; regional demand growth is driven by expanding industrial and automotive sectors across Asia‑Pacific and North America, with increasing regulatory and durability requirements shaping future adoption.

The Acrylic Rubber Market holds strategic significance as a core supplier of high-performance elastomers essential for critical applications in automotive, industrial, and heavy machinery sectors. As global vehicle production and industrial equipment manufacturing expand, demand for oil‑ and heat‑resistant sealing, hose, and gasket solutions continues to rise. Compared to older nitrile or conventional rubbers, advanced acrylic rubber formulations deliver up to 30% more thermal stability under high under‑hood temperatures, offering firms enhanced durability and lower maintenance costs. In this context, Asia‑Pacific dominates in volume consumption due to large-scale automotive manufacturing, while North America leads in adoption of specialized industrial seals and hydraulic hose applications, with over 25% of industrial OEMs reporting use of acrylic rubber components in 2024.

In the next two to three years, by 2028, adoption of bio‑based acrylate monomer technology is expected to reduce carbon footprint in manufacturing by 15–20%, supporting ESG and sustainability goals. Manufacturers are also planning to invest in next‑generation high-temperature-resistant ACM variants, which could cut equipment failure rates by 12–15%, while improving service life under high heat and oil exposure. Firms across Europe and North America are committing to recycling and re-use targets for elastomer components, aiming for 40% component recycling by 2030, which strengthens demand for durable, recyclable elastomers like acrylic rubber.

A micro‑scenario illustrates this: in 2024, a leading Japanese supplier implemented optimized polymerization protocols that increased batch yield by 12% and reduced energy consumption per ton by 8%, improving operational efficiency. Looking ahead, the Acrylic Rubber Market is positioned as a resilient component of industrial supply chains — meeting stricter environmental standards, enabling durable performance in harsh conditions, and supporting long-term adoption across automotive, industrial, and infrastructure applications. Its future lies in innovation, compliance, and sustainable growth trajectories.

The Acrylic Rubber Market is shaped by increasing demand for high-performance sealing, gasket, and hose materials across automotive, industrial, hydraulic, and heavy‑equipment applications. Rising automotive production, particularly in Asia-Pacific and North America, fuels demand for elastomers that can withstand higher operating temperatures and exposure to oils and chemicals. Industrial machinery, oil & gas, and construction sectors add to this demand with requirements for durable, resistant materials. At the same time, volatility in acrylate monomer feedstock prices and regional energy cost disparities influence supply chain stability and pricing. On the technology front, manufacturers are upgrading polymerization and processing capabilities, leading to improved yields, better performance grades, and broader application scopes.

Global automobile manufacturing continues to expand, increasing the demand for high‑performance materials used in transmissions, seals, gaskets, and hoses. Acrylic rubber’s superior heat, oil, and oxidation resistance makes it ideal for these applications. As vehicle output rises, especially in markets with rigorous thermal and durability requirements, the demand for acrylic rubber components grows proportionally to satisfy manufacturing commitments and reliability standards.

Acrylic rubber production depends heavily on acrylate monomers derived from petrochemicals, whose prices frequently fluctuate with crude‑oil markets. Sharp increases in monomer prices elevate production costs, compressing margins for manufacturers. This unpredictability makes long-term contracts tougher to manage and can deter investment in capacity expansion, especially for smaller regional producers sensitive to cost pressures.

As global infrastructure investment and heavy machinery demand surge, requirements for durable, oil‑ and heat‑resistant sealing and hose materials increase. Acrylic rubber’s suitability for hydraulic systems, industrial compressors, and oil‑resistant applications opens new growth avenues. Expanding into oil & gas, construction equipment, and industrial hydraulics presents a substantial addressable market beyond traditional automotive demand, enabling diversification and resilience against automotive cycles.

Alternative elastomers — including fluorocarbon rubbers and advanced silicones — offer wider temperature ranges or better chemical resistance in some premium applications, threatening acrylic rubber’s market share. Additionally, acrylic rubber processing demands specialized polymerization equipment and strict curing protocols; many small-scale manufacturers lack this infrastructure, resulting in higher rejection rates and limited ability to produce specialty grades. Together, these factors can slow adoption and limit penetration in cost-sensitive or highly regulated segments.

Growing adoption of bio‑based acrylic monomers: In 2023–2024, more than 40% of new acrylic rubber formulations globally incorporated partially bio‑based acrylate monomers, aligning material supply with sustainability requirements and reducing reliance on fossil-based feedstocks.

Expansion into industrial hydraulic and oil‑resistant applications: Usage in industrial compressors, hydraulic systems, and oil & gas machinery increased by nearly 22% in 2024 as companies sought durable, oil-resistant elastomer solutions for heavy-duty operations.

Shift toward high‑temperature resistant ACM grades: Manufacturers launched new acrylic rubber variants capable of sustained operation at 175–200 °C, resulting in a 15% increase in demand for heat‑resistant seals and gaskets across automotive and industrial sectors.

Increased demand from emerging markets’ automotive aftermarket and heavy machinery sectors: Demand from developing regions rose by over 25% in 2024 compared to 2021, driven by growth in vehicle production, construction, mining and infrastructure projects requiring durable elastomers.

The Acrylic Rubber Market is segmented by type, application, and end-user, providing a structured understanding of product adoption and sectoral utilization. By type, the market is divided into standard acrylic rubber, high-temperature resistant acrylic rubber, and specialty copolymers, each serving distinct operational needs. Applications cover automotive, industrial machinery, construction, and oil & gas sectors, reflecting the material’s versatility in sealing, gasket, and hose solutions. End-users range from original equipment manufacturers (OEMs) to industrial maintenance providers, with adoption patterns influenced by regional production capacity, regulatory requirements, and performance demands. Globally, automotive remains the primary driver of demand, while industrial machinery and construction sectors show rising adoption rates. The segmentation highlights the alignment between specific product features and targeted operational environments, ensuring decision-makers can tailor strategies based on market needs and performance characteristics.

The Acrylic Rubber Market is classified into standard acrylic rubber, high-temperature resistant acrylic rubber, and specialty copolymers. High-temperature resistant acrylic rubber is the leading type, accounting for approximately 55% of global usage, primarily due to its superior thermal and oil resistance for automotive seals, gaskets, and hoses. Specialty copolymers are the fastest-growing type, fueled by demand in hydraulic, construction, and industrial applications where enhanced chemical resistance is required. Other types, including standard acrylic rubber and blended grades, contribute roughly 25% combined and are commonly used in less demanding sealing and gasket applications.

The market applications include automotive, industrial machinery, construction, and oil & gas sectors. Automotive applications lead, representing around 60% of total usage, driven by OEMs’ need for heat- and oil-resistant seals and gaskets. Industrial machinery is the fastest-growing application, supported by trends such as hydraulic system expansion and heavy equipment usage, with adoption increasing across manufacturing and mining sectors. Construction and oil & gas applications account for the remaining 20% combined, often focused on seals, hoses, and vibration-resistant components. In 2024, over 38% of industrial equipment manufacturers globally reported incorporating high-temperature acrylic rubber for hydraulic hoses, enhancing service life and operational efficiency.

Leading end-users include automotive OEMs, industrial equipment manufacturers, and construction companies. Automotive OEMs account for approximately 60% of consumption due to the critical requirement for durable, high-temperature seals, gaskets, and hoses. The industrial machinery sector is the fastest-growing end-user, driven by increasing demand for hydraulic hoses, compressors, and construction machinery components; their adoption share is projected to rise significantly as OEMs and aftermarket suppliers expand operations. Other end-users, such as oil & gas service providers and infrastructure companies, represent roughly 25% combined. In 2024, more than 40% of OEMs globally reported piloting advanced acrylic rubber grades to improve gasket longevity and reduce maintenance cycles.

Asia-Pacific accounted for the largest market share at 45% in 2024; however, Region North America is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

In 2024, Asia-Pacific consumed over 525,000 metric tons of acrylic rubber, with China leading at 210,000 metric tons, followed by Japan (95,000 metric tons) and India (75,000 metric tons). Key drivers include rising automotive production, industrial machinery manufacturing, and increased demand for high-performance seals and gaskets. In contrast, North America shows accelerated adoption in automotive OEMs, aerospace, and industrial sectors, supported by regulatory incentives and investment in advanced polymer technologies. Europe contributes 20% of total consumption, led by Germany, UK, and France, while South America and the Middle East & Africa collectively account for 15%, with growth driven by energy infrastructure, industrial expansion, and import substitution trends. The market demonstrates strong regional variations in production, end-user applications, and technological integration, highlighting the strategic importance of supply chain localization and advanced manufacturing processes.

North America holds approximately 25% of the global acrylic rubber market by volume. Key industries driving demand include automotive, aerospace, and heavy machinery manufacturing, with OEMs increasingly incorporating high-temperature resistant seals and gaskets. Government incentives for advanced manufacturing and environmental compliance have accelerated the adoption of eco-friendly elastomers. Technological advancements such as digital extrusion monitoring and automated polymer blending have improved product consistency and reduced waste. For example, Arkema Inc. recently expanded its polymer production line in the US to increase output of high-performance acrylic rubbers for automotive applications. Regional consumer behavior shows higher adoption of durable elastomeric components in automotive and aerospace sectors compared to industrial maintenance applications.

Europe accounts for around 20% of the global acrylic rubber market. Germany, the UK, and France are the top-consuming countries, driven by automotive, industrial machinery, and energy sectors. Regulatory bodies such as REACH and sustainability mandates encourage the adoption of environmentally compliant polymers. Emerging technologies, including high-temperature and oil-resistant formulations, are gaining traction. Lanxess AG in Germany has implemented new production techniques to enhance the chemical resistance of acrylic rubber used in automotive seals. Regional consumer behavior reflects a preference for high-durability materials that comply with stringent environmental and performance standards, especially in automotive OEMs and industrial machinery sectors.

Asia-Pacific leads in market volume, with over 45% of global consumption. Top consuming countries include China, India, and Japan. The region benefits from large-scale automotive and industrial manufacturing infrastructure and rising demand for durable, high-temperature-resistant seals and hoses. Technological trends include localized polymer compounding and automated extrusion processes. Sinopec in China recently upgraded production lines to produce specialty acrylic rubber grades for automotive and industrial applications. Regional consumer behavior shows high adoption in OEM production and industrial maintenance, supported by cost-effective production and availability of skilled labor.

South America accounts for approximately 8% of global acrylic rubber consumption, with Brazil and Argentina as key markets. The growth is driven by industrial machinery, oil & gas, and automotive sectors. Government incentives and import substitution policies have encouraged local production. Braskem has expanded its polymer facilities in Brazil to supply high-performance acrylic rubber for hydraulic systems and industrial hoses. Regional consumer behavior highlights demand concentrated in energy infrastructure projects and automotive component manufacturing, reflecting the region’s focus on industrial expansion and reliability.

Middle East & Africa represents around 7% of global market consumption. Major growth countries include UAE and South Africa, with demand concentrated in oil & gas, construction, and industrial machinery. Technological modernization includes adoption of automated mixing and compounding techniques to meet performance requirements. Local regulations and trade partnerships facilitate polymer imports and regional production. SABIC in the UAE has initiated projects to produce high-temperature acrylic rubber for industrial applications. Regional consumer behavior reflects growing adoption in energy and construction sectors, driven by infrastructure development and industrial modernization initiatives.

China – 18% Market Share: Dominance due to large-scale production capacity and significant industrial and automotive demand.

United States – 15% Market Share: Dominance driven by advanced manufacturing technologies and high adoption in automotive and aerospace end-use applications.

The Acrylic Rubber Market exhibits a moderately consolidated competitive structure, with approximately 45 active global competitors operating across key regions. The combined market share of the top five companies accounts for around 55%, highlighting a balance between dominant players and niche specialists. Leading firms are engaging in strategic initiatives such as technology-driven product launches, partnerships for sustainable elastomer solutions, and expansions of production facilities in high-demand regions like Asia-Pacific and North America. Innovation trends include the development of high-temperature-resistant grades, oil- and chemical-resistant variants, and eco-friendly formulations incorporating recycled materials. Companies are also investing in automated polymer compounding and digital extrusion monitoring technologies to enhance production efficiency and product consistency. Emerging collaborations between chemical manufacturers and automotive OEMs are accelerating the adoption of specialty acrylic rubbers for advanced sealing, hose, and gasket applications. The market’s competitive environment is further characterized by continuous R&D investments, patents in proprietary polymer blends, and regional expansions to serve industrial, automotive, and aerospace sectors.

Sinopec

Kuraray Co., Ltd.

Zeon Corporation

ExxonMobil Chemical

Mitsui Chemicals

Current technologies in the Acrylic Rubber Market focus on improving thermal stability, chemical resistance, and mechanical performance of elastomers. Advanced polymerization techniques such as emulsion polymerization and solution polymerization are widely adopted to produce consistent molecular weight distributions and high-purity polymers. Innovations in automated extrusion, compounding, and blending technologies enhance production efficiency, reduce waste, and ensure uniform product quality across batches. Emerging technologies include the development of bio-based acrylic rubber variants and the integration of nanomaterials to improve elasticity and durability. Digital process monitoring systems are increasingly used to track viscosity, temperature, and curing parameters in real time, enabling faster detection of inconsistencies. Additive manufacturing and 3D printing research is also underway to explore the use of acrylic rubbers in custom seals and gaskets for niche industrial applications. Furthermore, high-performance grades designed for automotive, aerospace, and industrial machinery applications are being optimized for energy efficiency, environmental compliance, and extended service life.

In January 2024, Arkema’s facility in Taixing, China secured ISCC‑PLUS certification for its acrylic monomers production — the first plant of its kind in China to receive that certification — enabling bio‑attributed acrylic supply in Asia-Pacific markets. Source: www.arkema.com

In October 2024, Arkema began producing an ethyl‑acrylate monomer derived entirely from bio‑ethanol at its Carling, France site; the bio‑based monomer features ~40% biogenic carbon content and reduces carbon footprint by up to 30%, supporting lower‑carbon acrylic rubber and resin supply chains. Source: www.arkema.com

In February 2024, Zeon Corporation secured ISCC PLUS certification at four of its Japanese production plants (Takaoka, Kawasaki, Tokuyama, Mizushima), enabling mass‑balance allocation of recycled and bio‑based raw materials across its elastomer output, as part of its commitment to cut CO₂ emissions by 50% by 2030. Source: www.zeon.co.jp

In June 2024, Arkema obtained ISCC PLUS certification at its acrylic monomer production facility in Clear Lake, Texas — reinforcing its global supply of bio‑attributed acrylic monomers and supporting sustainable elastomer supply for automotive and industrial customers. Source: www.arkema.com

The Acrylic Rubber Market Report covers an extensive range of product types, applications, and end-use industries. Key segments include standard acrylic rubber, high-temperature-resistant grades, oil-resistant variants, and specialty formulations for industrial, automotive, and aerospace applications. The report evaluates geographic regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing production volumes, consumption trends, and regional technological adoption. It highlights market dynamics such as the impact of sustainable and eco-friendly polymer developments, regulatory compliance, and industrial modernization. Emerging and niche segments, including bio-based acrylic rubbers and high-performance elastomers for additive manufacturing, are examined. The report also considers strategic initiatives like partnerships, production expansions, and technological innovations shaping the market. Key industry focus areas include automotive OEMs, industrial machinery, energy infrastructure, and aerospace components, providing actionable insights for decision-makers to navigate production planning, investment strategies, and technology integration in the global acrylic rubber landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,168.9 Million |

| Market Revenue (2032) | USD 2,245.0 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Arkema Inc., Lanxess AG, SABIC, Sinopec, Kuraray Co., Ltd., Zeon Corporation, ExxonMobil Chemical, Mitsui Chemicals |

| Customization & Pricing | Available on Request (10% Customization Free) |