Reports

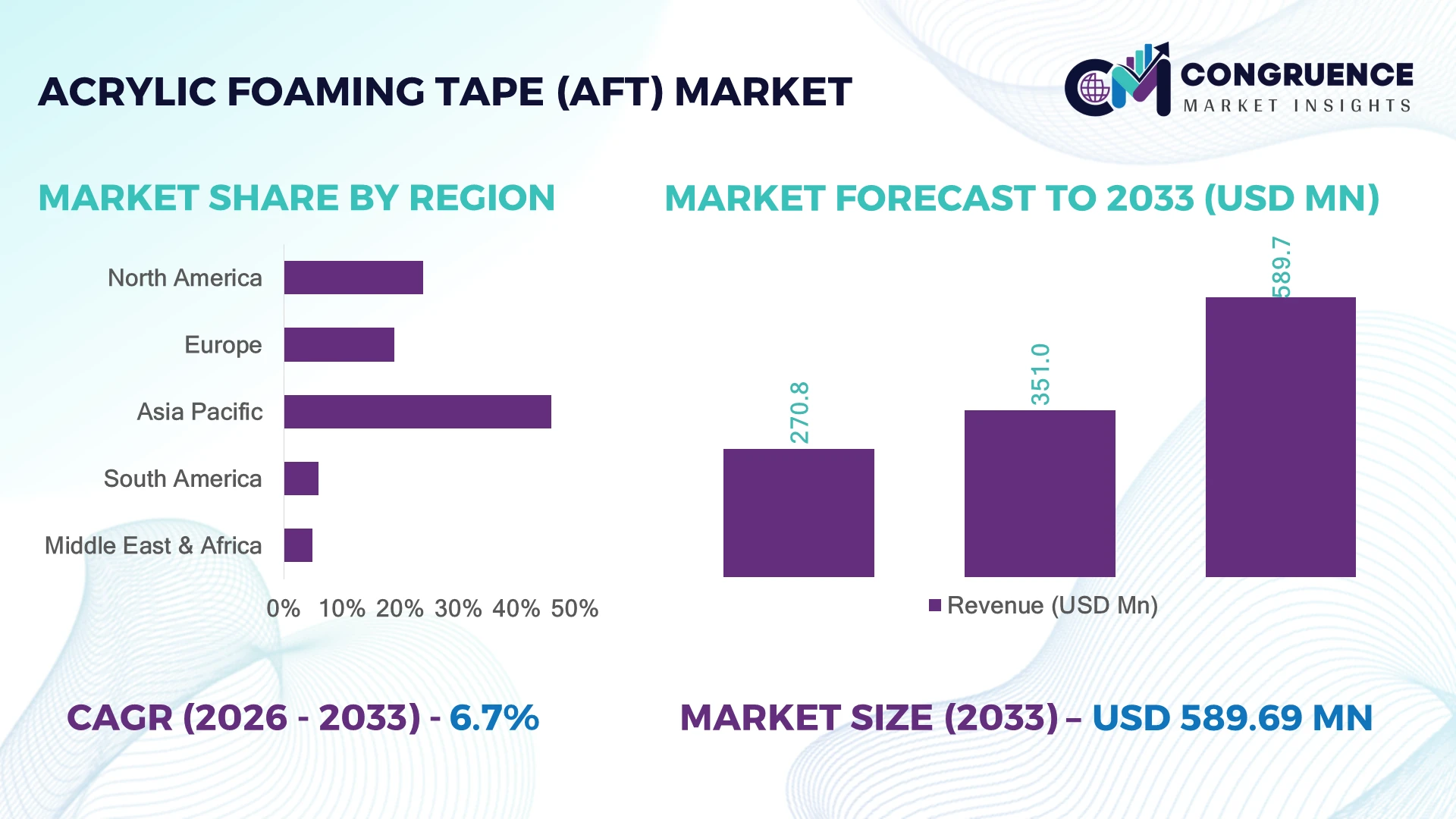

The Global Acrylic Foaming Tape (AFT) Market was valued at USD 351.0 Million in 2025 and is anticipated to reach a value of USD 589.7 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. Growth is driven by rising adoption of lightweight bonding solutions in electric vehicles, advanced electronics, automotive assembly, and construction applications replacing mechanical fasteners.

China dominates the Acrylic Foaming Tape (AFT) market, accounting for approximately 34% share through its large automotive manufacturing base, electronics supply chains, and investments in EV production capacity exceeding 10 million vehicles annually. Japan and South Korea follow with strong demand from precision electronics and automotive sectors, while the United States focuses on aerospace and infrastructure applications. China’s industrial output scale remains significantly higher, with nearly 40% more manufacturing capacity than Japan in key end-use sectors.

Strategic sourcing shifts after global supply-chain disruptions are accelerating regional production diversification and supplier partnerships.

Market Size & Growth: USD 351.0 Million (2025) to USD 589.7 Million (2033), 6.7% CAGR, driven by EV lightweighting and high-performance adhesive replacement.

Top Growth Drivers: Automotive applications 38%, electronics assembly 27%, construction bonding 21% driving market expansion.

Short-Term Forecast: By 2028, advanced adhesive adoption reduces assembly time by 20% and improves bonding efficiency by 25%.

Emerging Technologies: AI-based adhesive formulation, automated tape application systems, and nanostructured acrylic materials reshape production.

Regional Leaders: Asia-Pacific reaches USD 340 Million by 2033 with EV expansion; North America reaches USD 140 Million with aerospace adoption; Europe reaches USD 95 Million through sustainable manufacturing.

Consumer/End-User Trends: Over 60% of automotive manufacturers prioritize lightweight bonding technologies for next-generation vehicle platforms.

Pilot/Case Example: 2024 EV assembly projects using acrylic foam tapes achieved approximately 30% faster component installation compared with conventional fastening methods.

Competitive Landscape: 3M leads with around 25% share, alongside Tesa, Avery Dennison, Nitto Denko, and Scapa Group competing through material innovation.

Regulatory & ESG Impact: Lightweight adhesive solutions support up to 15% material reduction in vehicle assembly while aligning with global carbon reduction policies.

Investment & Funding: Over USD 500 Million invested globally in advanced adhesive manufacturing expansions, automation upgrades, and regional supply-chain localization.

Innovation & Future Outlook: Next-generation AFT products focus on recyclable materials, higher temperature resistance, and smart manufacturing integration.

Acrylic Foaming Tape (AFT) solutions are gaining traction across automotive, electronics, renewable energy, and architectural applications due to superior vibration damping, weather resistance, and seamless bonding performance. Recent product innovations include ultra-thin foam structures and temperature-resistant adhesive formulations, with premium variants representing nearly 45% of demand in advanced industrial applications. Supply-chain localization initiatives in Asia and North America are encouraging manufacturers to expand regional production capabilities, creating new opportunities for high-performance adhesive technologies.

Acrylic Foaming Tape (AFT) is becoming strategically important as manufacturers shift toward lightweight assembly, improved durability, and simplified production processes across automotive, electronics, and industrial sectors. The transition toward electric vehicles and smart devices is accelerating demand for adhesive technologies that reduce component weight while maintaining structural reliability. Global supply-chain restructuring after recent disruptions is encouraging regional adhesive production and multi-source procurement strategies.

Compared with traditional mechanical fastening systems, advanced acrylic foam tapes reduce assembly complexity by eliminating drilling and hardware requirements, improving installation efficiency by nearly 25% while lowering processing costs. Asia-Pacific maintains the strongest manufacturing scale, particularly in China, while North America and Europe lead innovation through automation, premium materials, and sustainability-focused product development.

Over the next 2–3 years, manufacturers are prioritizing automated application systems, recyclable adhesive technologies, and partnerships with EV and electronics producers. Automotive suppliers are increasingly deploying AFT solutions for battery modules, trims, and display systems where precision bonding is critical. Companies expanding localized production networks and investing in high-performance formulations are positioned to secure long-term competitive advantages in this evolving adhesive technology landscape.

The shift toward lightweight manufacturing is accelerating Acrylic Foaming Tape (AFT) adoption, particularly in electric vehicle and electronics assembly applications. Automotive manufacturers are replacing mechanical fasteners with advanced adhesive solutions, reducing component weight by nearly 15% and improving assembly efficiency by 25%. China’s EV production expansion and Japan’s precision electronics ecosystem are strengthening industrial demand. Companies are responding through localized adhesive production facilities, automotive partnerships, and investments in high-temperature acrylic formulations. The growing use of AFT in battery packs, displays, and exterior components provides manufacturers with improved vibration control, corrosion resistance, and streamlined production workflows.

Acrylic Foaming Tape (AFT) manufacturers face pressure from fluctuations in acrylic polymers, specialty chemicals, and silicone-based materials, with raw material costs accounting for nearly 50% of production expenses. Supply disruptions affecting chemical supply chains in China and Europe have increased procurement complexity, while premium-grade adhesive formulations remain 20–30% more expensive than conventional alternatives. These constraints impact pricing flexibility and profitability for tape producers. Companies are reducing exposure through multi-country sourcing strategies, long-term supplier contracts, and regional manufacturing expansion. A key operational challenge remains maintaining consistent adhesive performance while controlling input costs across global production networks.

Emerging opportunities are developing through high-performance acrylic formulations, automated application systems, and sustainable adhesive technologies. Demand for ultra-thin and high-temperature-resistant AFT products is increasing, with premium adhesive grades representing nearly 45% of advanced industrial applications. South Korea and Germany are expanding research into electronics miniaturization and EV component bonding, creating new application areas. Companies are investing in R&D partnerships, recyclable material development, and automated coating technologies to improve production precision. The integration of digital quality monitoring can reduce adhesive application defects by approximately 20%, creating efficiency advantages for manufacturers targeting high-value industrial customers.

Maintaining consistent bonding performance under extreme temperatures, moisture exposure, and long operating cycles remains a key execution challenge for Acrylic Foaming Tape (AFT) suppliers. Automotive and aerospace applications require durability testing standards that can extend product qualification timelines by 15–25%. Increasing customization requirements from EV manufacturers and electronics producers add complexity to manufacturing scalability. Companies must overcome challenges related to formulation optimization, testing infrastructure, and skilled technical expertise. Manufacturers are addressing these pressures through advanced simulation tools, expanded testing laboratories, and collaborative development programs with OEMs. Ensuring reliable performance across diverse environments will determine long-term competitiveness in specialized adhesive applications.

EV Bonding Applications Expand: Electric vehicle manufacturers are increasing acrylic foaming tape usage for battery modules, trims, and lightweight components, with adoption rising above 20% annually in selected automotive supply chains. China-based EV producers are integrating automated adhesive application systems to reduce assembly steps by nearly 25%, while suppliers are developing customized high-strength formulations for vehicle platforms.

Precision Electronics Demand Rises: Miniaturized electronics production is driving demand for thinner and more durable AFT solutions, with advanced adhesive grades accounting for nearly 45% of premium industrial applications. South Korean and Japanese manufacturers are adopting automated coating and inspection technologies, improving production consistency by approximately 15% and reducing material waste through precision-controlled processes.

Sustainable Adhesive Development Accelerates: Environmental compliance pressures and corporate sustainability targets are encouraging manufacturers to introduce recyclable acrylic foam materials, with eco-focused product development programs increasing by around 30% since 2024. European manufacturers are restructuring supply chains and partnering with chemical innovators to improve material traceability and reduce lifecycle impacts.

Localized Production Networks Grow: Supply-chain disruptions have pushed adhesive producers to expand manufacturing closer to end-use industries, with regionalized capacity investments increasing by nearly 25% in automotive and electronics hubs. Companies are building facilities in China, India, and North America to improve delivery reliability, shorten lead times, and reduce dependency on concentrated chemical suppliers.

Based on type segmentation, High Bond Acrylic Foam Tape represents the leading segment due to superior adhesion strength, weather resistance, and suitability for automotive, construction, and electronics applications. These tapes support structural bonding requirements where mechanical fastening alternatives create additional weight and assembly complexity. High bond variants account for approximately 55% of industrial AFT usage, supported by growing EV manufacturing and exterior component applications. Companies such as adhesive manufacturers and automotive suppliers are prioritizing advanced formulations with improved temperature tolerance and durability. Medium Bond Acrylic Foam Tape is emerging as the fastest-growing type as manufacturers seek cost-efficient solutions for lightweight assemblies, interior components, and general industrial applications. This segment benefits from broader applicability and easier integration into existing production workflows. Low bond variants continue serving signage and decorative applications but face limited expansion due to performance constraints. Companies are shifting investments toward hybrid formulations combining flexibility, strength, and reduced material consumption.

Based on application segmentation, Automotive remains the dominant application area for Acrylic Foaming Tape (AFT), driven by increasing use in emblems, trims, sensors, battery components, and lightweight vehicle assemblies. Automotive applications represent nearly 50% of total demand as manufacturers replace traditional fastening methods with adhesive bonding technologies. China, Germany, and the United States are expanding AFT integration in EV and premium vehicle production, encouraging suppliers to develop customized solutions. Electronics Assembly is the fastest-growing application segment due to increasing device miniaturization, display integration, and demand for vibration-resistant bonding. Electronics applications are growing as manufacturers require thinner adhesive solutions with higher precision, contributing to approximately 30% growth in specialized product adoption. Construction, signage, and industrial applications maintain stable demand, supported by weather-resistant bonding requirements. Companies are expanding automation capabilities to improve application accuracy and reduce production downtime.

Based on end-user segmentation, Automotive Manufacturers represent the leading buyer group due to large-scale consumption of AFT products across vehicle assembly operations. The segment contributes nearly 55% of industrial demand, supported by EV production expansion, lightweight design requirements, and increased use of bonded components. Vehicle producers are strengthening partnerships with adhesive suppliers to secure application-specific solutions and improve manufacturing efficiency. Electronics and Consumer Device Manufacturers represent the fastest-growing end-user segment as companies prioritize compact designs, thermal management, and reliable component attachment. Adoption is increasing by approximately 25% in advanced electronics production environments, particularly among manufacturers in South Korea, Japan, and China. Construction firms and industrial equipment producers continue adopting AFT for durable bonding applications, but their purchasing cycles remain more project-dependent. Companies are targeting high-growth users through customized product portfolios, technical support programs, and localized supply networks.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of7.4% between 2026 and 2033.

North America holds a significant position in the Acrylic Foaming Tape (AFT) market, supported by automotive electrification, aerospace manufacturing, and advanced electronics production. The region contributes approximately 24% of global demand, with adoption concentrated across the United States automotive and industrial sectors. EV manufacturers are increasing adhesive-based assembly processes, with lightweight bonding solutions improving manufacturing efficiency by nearly 20%. Investments in domestic supply-chain localization following global material disruptions are encouraging adhesive producers to expand regional production and strengthen OEM partnerships. Companies are focusing on high-temperature and structural-grade AFT products to meet evolving performance requirements.

United States Market Outlook: The United States represents the largest North American market due to its strong automotive, aerospace, and electronics manufacturing base. More than 50% of regional AFT demand is linked to transportation and industrial applications. Expanding EV manufacturing facilities, semiconductor investments, and automation upgrades are creating demand for precision adhesive technologies. U.S. manufacturers are increasingly adopting locally produced bonding materials to improve supply reliability and reduce dependency on imported specialty chemicals.

Europe maintains a strong position in the Acrylic Foaming Tape (AFT) market, driven by automotive innovation, sustainability regulations, and advanced manufacturing standards. The region accounts for nearly 19% of global demand, supported by Germany, France, and Italy’s automotive production networks. Increasing focus on lightweight vehicles and recyclable materials is accelerating adoption of advanced adhesive solutions. European manufacturers are integrating automated adhesive application systems, improving production consistency by approximately 15%. Regulatory pressure around vehicle efficiency and carbon reduction is encouraging companies to invest in environmentally optimized AFT formulations and localized material partnerships.

Germany Market Outlook: Germany leads Europe’s AFT adoption through its automotive engineering ecosystem and premium vehicle manufacturing capabilities. The country contributes nearly 40% of European automotive adhesive consumption, supported by major vehicle producers and component suppliers. Investments in EV platforms, smart factories, and sustainable production methods are increasing demand for durable bonding solutions. German manufacturers are prioritizing high-performance AFT technologies for battery systems, exterior components, and lightweight structures.

Asia-Pacific dominates the Acrylic Foaming Tape (AFT) market due to large-scale automotive production, electronics manufacturing, and expanding industrial capacity. The region represents approximately 46% of global market demand, with China, Japan, South Korea, and India driving consumption. China’s EV manufacturing ecosystem and electronics supply chains remain major demand centers, while regional production capacity continues expanding through localized adhesive manufacturing. More than 60% of new AFT production investments are concentrated in Asian manufacturing hubs. Companies are increasing automation, developing customized formulations, and building partnerships with automotive and electronics OEMs to support high-volume applications.

China Market Outlook: China is the leading Asia-Pacific market due to its extensive EV, consumer electronics, and industrial manufacturing base. The country produces over 10 million electric vehicles annually, creating significant demand for lightweight bonding materials. Strong domestic chemical production capabilities, expanding automation adoption, and government-backed advanced manufacturing initiatives provide companies with cost and supply-chain advantages. Chinese adhesive producers are increasing investment in high-performance AFT technologies for automotive battery systems and electronics assembly.

South America represents an emerging Acrylic Foaming Tape (AFT) market supported by automotive manufacturing, construction activity, and industrial modernization initiatives. The region contributes approximately 6% of global demand, with Brazil and Argentina accounting for the majority of consumption. Automotive plants are increasingly adopting adhesive bonding technologies to improve production efficiency and reduce assembly complexity. Brazil’s manufacturing sector is encouraging localized sourcing, with domestic industrial investments improving supply availability by nearly 10–15%. However, dependence on imported specialty chemicals remains a challenge. Companies are responding through distributor partnerships, regional inventory expansion, and selective manufacturing collaborations.

Brazil Market Outlook: Brazil is the most strategically important South American market due to its automotive production scale and industrial infrastructure. The country accounts for nearly 50% of regional AFT consumption, supported by vehicle assembly plants and construction applications. Increasing adoption of lightweight automotive components and improved industrial automation is creating new opportunities for adhesive suppliers. Companies are strengthening local partnerships to reduce import delays and improve customer support capabilities.

The Middle East & Africa Acrylic Foaming Tape (AFT) market is expanding through infrastructure development, industrial diversification, and growing manufacturing investments. The region contributes around 5% of global demand, with adoption concentrated in construction, automotive servicing, electronics, and industrial applications. Infrastructure modernization programs in Gulf countries are increasing demand for durable bonding materials, while manufacturers are exploring localized distribution networks. Investment in industrial projects has increased adhesive application requirements by approximately 15% in selected construction segments. Companies are developing regional supply partnerships and improving inventory capabilities to support faster deployment.

Saudi Arabia Market Outlook: Saudi Arabia represents the most promising Middle Eastern market due to large-scale infrastructure projects, industrial expansion programs, and manufacturing diversification efforts. Construction and industrial applications account for more than 60% of regional AFT usage. Investments in new manufacturing zones, automotive initiatives, and smart infrastructure projects are increasing demand for advanced adhesive technologies. Suppliers are building strategic partnerships to support localized availability and long-term industrial development.

The Acrylic Foaming Tape (AFT) market features competition between global adhesive leaders and specialized regional manufacturers. Companies such as 3M, tesa, Nitto Denko, Avery Dennison, Scapa, and Saint-Gobain compete through technology depth, OEM relationships, and production scale. The top five players collectively account for approximately 60% of market share, creating a moderately consolidated structure. Global leaders compete on advanced acrylic chemistry, customization, and supply reliability, while regional suppliers target cost-sensitive applications with faster delivery. Technology differentiation remains critical, with premium formulations improving bonding performance by 20–30% compared with conventional tapes. Players are expanding manufacturing capacity, forming automotive partnerships, and developing sustainable adhesive solutions. The competitive shift is moving toward solvent-free materials, EV-focused applications, and localized supply chains. High qualification requirements and OEM approval processes create entry barriers. Winning requires superior material innovation, global availability, and application-specific engineering support.

tesa SE

Nitto Denko Corporation

Avery Dennison Corporation

Scapa Group

Saint-Gobain

Intertape Polymer Group

Lintec Corporation

Teraoka Seisakusho Co., Ltd.

Sekisui Chemical Co., Ltd.

PPI Adhesive Products Ltd.

Achem Technology Corporation

Acrylic Foaming Tape technology is shifting toward advanced viscoelastic materials, solvent-free formulations, and precision-coated adhesive structures. Modern acrylic foam tapes replace traditional mechanical fastening by reducing assembly complexity and improving design flexibility. Advanced formulations deliver approximately 20% higher stress absorption and improved durability compared with conventional bonding systems. Adoption is strongest in automotive and electronics manufacturing, where premium adhesive grades represent nearly 45% of industrial usage.

Automation is becoming a key technology driver as manufacturers integrate robotic tape application, digital inspection, and automated dispensing workflows. These systems improve placement accuracy by around 15% and reduce production inconsistencies in high-volume assembly lines. Companies benefiting most are EV manufacturers, electronics producers, and industrial OEMs requiring repeatable bonding performance.

Between 2026 and 2028, next-generation AFT technologies will focus on recyclable materials, PFAS-free formulations, and application-specific adhesive engineering. New sustainable acrylic foam solutions are improving environmental compliance while maintaining industrial performance. Competitive advantage will shift toward companies combining material science, automation capability, and customer-specific engineering support.

October 2025 — 3M updated its Acrylic Foam Tape 4225N technical portfolio for automotive attachment applications, highlighting a 3.18 mm acrylic foam core and temperature performance from -30°C to +80°C. The update strengthens OEM bonding solutions for exterior trims, supporting lightweight vehicle assembly. Source: www.multimedia.3m.com

2025 — tesa SE advanced sustainable acrylic foam adhesive development with solvent-free automotive tape technologies, including products approved by target customers. The innovation supports electromobility applications and improves sustainability positioning through reduced manufacturing impact. Source: www.reports.beiersdorf.com

October 2025 — Nitto Denko Corporation introduced updated technical specifications for modified acrylic foam tape solutions featuring PFAS-free construction, strong adhesion, and impact resistance. The development supports automotive and industrial bonding requirements while improving regulatory alignment. Source: www.nitto.com

2025 — 3M expanded focus on conformable acrylic bonding technologies for automotive interiors, offering solutions designed for irregular surfaces and wire harness applications. The technology improves installation flexibility and supports OEM production efficiency in next-generation vehicle platforms.

The Acrylic Foaming Tape (AFT) Market Report provides comprehensive coverage of market segmentation across types, including high bond, medium bond, and low bond variants; applications such as automotive, electronics, construction, signage, and industrial uses; and end-users including OEMs, manufacturers, and commercial users. The report evaluates demand patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The study analyzes technology trends, competitive positioning, manufacturing strategies, supply-chain developments, and innovation pathways shaping the market through 2033. It highlights adoption patterns for advanced acrylic formulations, automation integration, sustainable materials, and application-specific solutions. The report supports strategic decisions related to investment planning, geographic expansion, supplier partnerships, product development, and competitive differentiation in evolving adhesive markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 351.0 Million |

| Market Revenue (2033) | USD 589.7 Million |

| CAGR (2026–2033) | 6.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M; tesa SE; Nitto Denko Corporation; Avery Dennison Corporation; Scapa Group; Saint-Gobain; Intertape Polymer Group; Lintec Corporation; Teraoka Seisakusho Co., Ltd.; Sekisui Chemical Co., Ltd.; PPI Adhesive Products Ltd.; Achem Technology Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |